LNVGF - Lenovo: Market Leader With Unattractive Margins

2023-05-17 09:00:47 ET

Summary

- Lenovo Group Limited is a technology and hardware company.

- Revenue has grown at a CAGR of 7%, driven by the development of its Services business and a compelling PC offering.

- Margins are unattractive, with a NIM of 3%. We see scope for gradual improvement.

- The hardware segment is experiencing a significant slowdown as consumers and businesses defer spending.

- Lenovo's valuation implies upside but we suspect sales will continue to decline in 2023.

Investment thesis

Our current investment thesis is:

- Lenovo ( LNVGF ) is a strong business with a leading position in the PC market. It is continuing to develop its Services offering which should help improve margins.

- Demand is declining for its hardware products as economic conditions bite. We suspect 2023 will be a tough year for the company.

- Despite the business being undervalued, we see no positive catalysts to cause price action.

Company description

Lenovo Group Limited is a technology and hardware company that produces and sells personal computers, mobile internet devices, servers, workstations, and accessories, as well as offers IT and management services.

The company operates through three segments: Intelligent Devices Group, Infrastructure Solutions Group, and Solutions and Services Group.

Share price

Lenovo's share price has performed poorly in the last decade, with the share price trading sideways while experiencing bouts of volatility. This is a reflection of Lenovo's financials being considered unattractive.

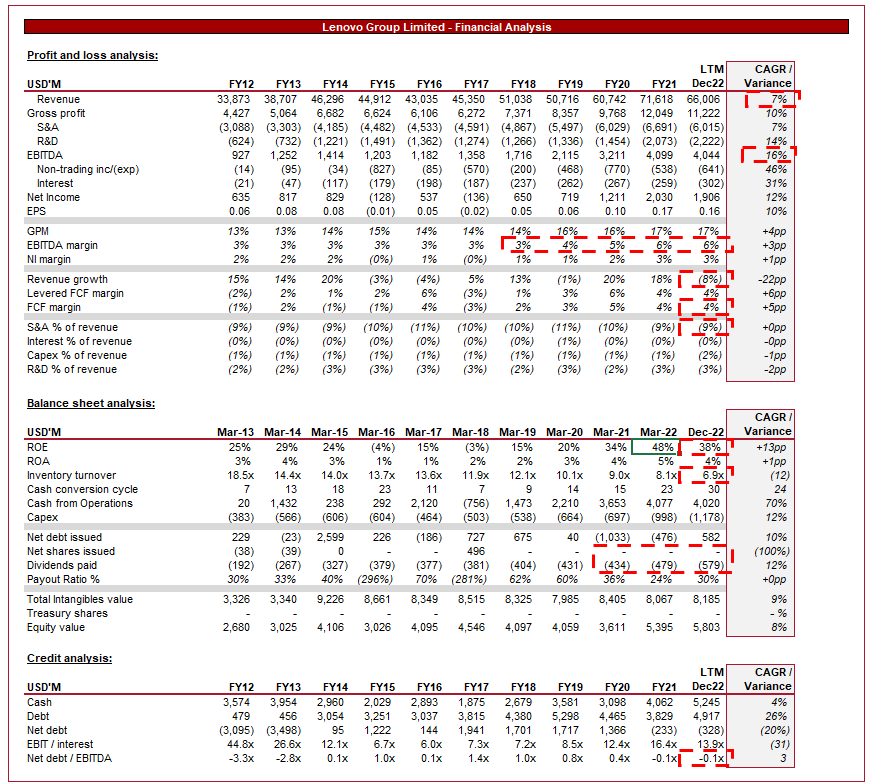

Financial analysis

Lenovo financial performance (Tikr Terminal)

{kind=link}

Presented above is Lenovo's financial performance for the last decade.

Revenue

Lenovo's revenue has grown at a CAGR of 7%, driven by its mass-market strategy to expand globally through competitive pricing and cost-effective products.

Lenovo's revenue is highly diversified, with no single country generating more than 28% of its revenue. Further, the company's PC to Non-PC ratio has moved toward non-PC in recent quarters, again providing greater diversification benefits.

Revenue b/d (Lenovo)

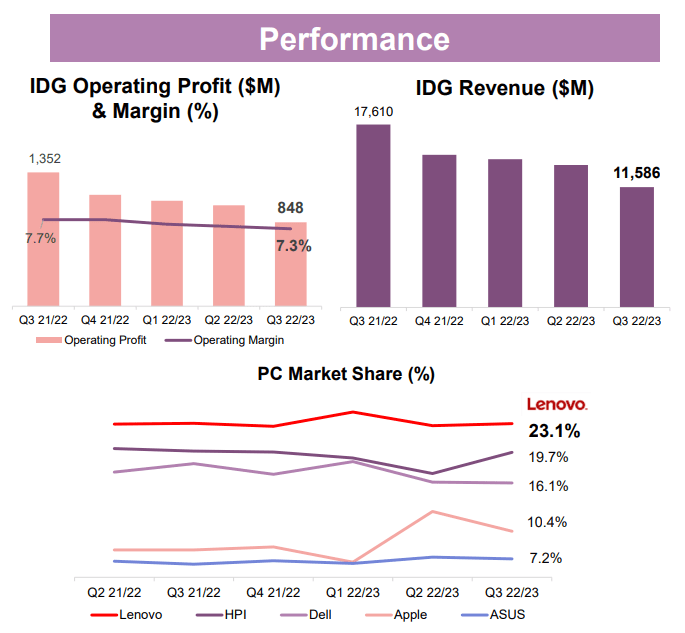

Lenovo's revenue is comprised of 3 different segments and so we will discuss each in detail. The largest is IDG, which is 76% of Q3 revenue, followed by ISG and SSG.

Revenue breakdown (Lenovo)

Intelligent Devices Group (IDG)

This is the primary revenue driver for Lenovo. Included within this segment is the sale of PCs and adjacent hardware products, such as mobiles. In recent years, Lenovo has focused on expanding the products it sells, entering the IoT and Smart device market. This looks to be a shrewd decision, as these products are growing at a superior rate and are disrupting several large industries. Further, the company continues to innovate its traditional PC offering.

Lenovo operates in the premium segment. The company's ability to rapidly gain market share is due to its competitive pricing relative to the competition. Many Financial Services firms use Lenovo laptops, they are powerful enough for data analysis while being cost-effective for a large workforce. This has allowed Lenovo to take market share from the likes of HP ( HPQ ) and Dell ( DELL ), who struggled to compete on computing power for the same price. According to the graph below, Lenovo is currently the market leader with a significant gap to the nearest competitor.

We have seen revenue consistently decline in the last 4 quarters, which reflects softening demand for hardware. The reason for this is likely economic conditions, which are forcing businesses and consumers to cut costs, resulting in reduced spending where possible.

This segment generates underwhelming margins, primarily due to the company's strategy of being a price leader. Management's objective is to focus on reducing costs while investing in higher-margin products, as mentioned previously. Although this is positive news, we believe it is unlikely to make a significant dent in its large PC revenue base.

{kind=link}

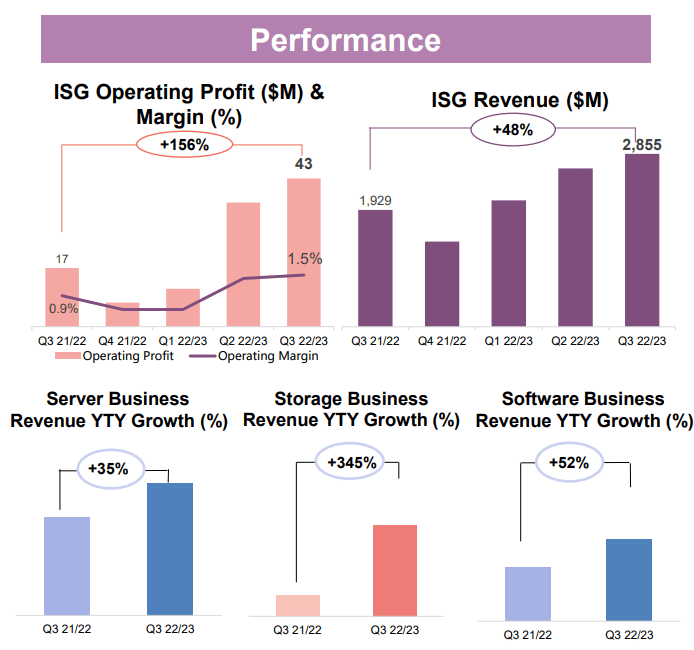

Infrastructure Solutions Group ((ISG))

This segment provides businesses of all sizes IT infrastructure solutions, such as Servers, Storage, and Software. This segment has generated impressive growth for Lenovo, with a 48% gain Y/Y. This has been driven by Lenovo's attractive industry proposition, with the company offering a comprehensive solution to businesses, making their offering cost-effective and convenient. Further, Lenovo's brand and scale of global infrastructure allow the business to convince potential clients it has the capabilities to provide a high-quality service.

Despite the impressive growth, this segment's margins are extremely poor, with an OPM of 1.5%. Margins are improving, however, we doubt the ability to reach an attractive level. This acts as a drag on Lenovo's current performance, especially given this segment is outgrowing IDG.

{kind=link}

Management's objective is to invest further in innovation, particularly AI, as a means of improving its competitive positioning.

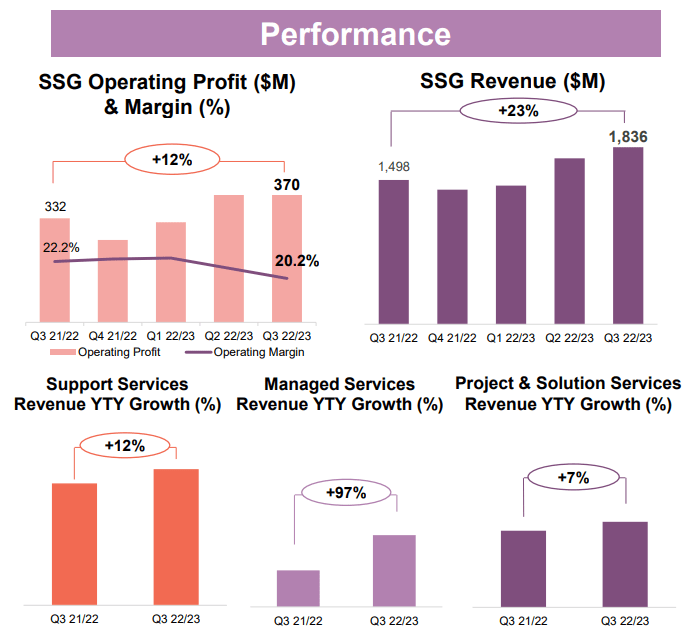

Solutions and Services Group ((SSG))

Lenovo defines this segment as bringing "together all of Lenovo's IT solutions and services across PC, infrastructure, and smart verticals, including attached services, managed services, and as-a-Service offerings, into one dedicated organization". This segment essentially covers all computing/tech Services provided by the business outside of ISG. The key Services Management highlight within this is Support Services, Managed Services, and Project & Solution Services.

This is the attractive part of the business, as Services are usually highly accretive. The marginal cost of providing Services declines noticeably with scale, allowing the business to grow its profitability through expansion.

This segment is also growing well, although not to the degree of ISG. Nevertheless, 23% is a strong performance and continues to positively dilute the margins of IDG.

SSG's OPM is an impressive 20.2%, although has declined in the last year. This looks to be driven by softening demand. Management's focus should be to ensure this does not decline further.

{kind=link}

Management's focus is to develop additional horizontal and vertical technological solutions, leveraging Lenovo's current IP. This looks to be a reasonable strategy and should be the focus of the group, given the cyclical nature of hardware and the poor margins of ISG.

Other key trends impacting the business

Due to the COVID-19 pandemic, many companies have shifted towards remote work, which has led to increased demand for both hardware, such as Laptops, and infrastructure services. Lenovo is well-positioned to generate outsized returns as a result of this, with scope for all segments to earn a share of growth.

The gaming industry is one of the fastest-growing segments of the technology industry, and Lenovo has been expanding its presence in this space with its Legion line of gaming laptops and desktops. The company has found success with its laptops, which are an area of expertise for the company. Our view is that gaming should continue to generate strong demand and as computing power increases, laptops will only increase in popularity.

Economic considerations

Current economic conditions represent a near-term problems for the business. Global inflation remains high and inflation is only slowly combating this. Consumers are facing difficulties with finances while companies are seeing their costs rise faster than they can raise prices.

Having considered Lenovo's various departments, it is clear that the IDG is seeing a significant slowdown in demand, and we attribute the reason to this. Companies and consumers are deferring or canceling spending, as well as trading down. Our view is that this will likely continue into 2024, as inflation remains elevated.

The good news for Lenovo is that its two other segments have remained robust, with strong demand.

Margin

We have heavily touched on margins from a segment perspective, it is now worth looking at the business as a whole. The company's EBITDA-M is a disappointing 6%, having trended up from 3% a decade prior.

The improvement in margins has been driven by the development of the SSG department, as well as investment into higher margin hardware, such as Gaming PCs. Given the growth rate of these two particular subsectors, our expectations would be for margins to continually improve in the medium term.

Our concern is that ISG will dilute the gains from these segments at an increasing level as growth continues on its current trajectory. Investors considering Lenovo will have to contend with the business remaining a low-margin business long term.

Q3 results

Q3 results (Lenovo)

Presented above is Lenovo's most recent quarterly results.

With IDG generating over 70% of revenue, the segment is the only part of the business that can move the needle. For this reason, the Q3 results are disappointing and a reflection of the slowdown in IDG.

Balance sheet

Lenovo's inventory turnover has significantly declined in the last recent period, reflecting a slowdown greater than Management anticipated. This figure in absolute terms is skewed somewhat by the Services, nevertheless, is a useful directional indicator.

Lenovo is conservatively financed, with a negative net debt. Management has been careful with raising debt while rapidly accumulating cash due to its large scale.

Management's distribution method of choice is dividends, with payments growing at a 12% rate in the last decade. Given the level of cash available and generated, this should be sustainable in the event of a continued slowdown. The current yield is 5%.

Valuation

Lenovo valuation (Tikr Terminal)

Lenovo is currently trading at 3x its LTM and NTM EBITDA, a discount to its historical average.

This discount looks to be a reflection of softening market conditions, with the company's valuation falling below its average in mid-2021.

Our general view of the business is positive when considering its average trading multiple. With margins improving and greater revenue diversification, there is no fundamental reason why the company should be trading at a discount to its historical average.

On a relative basis, however, the company looks less attractive. HP and Dell, for example, are trading at 7x EBITDA while having an EBITDA-M of 9%/8%. Based on this, investors would imply Lenovo's trading range should be sufficiently discounted, implying a fair value closer to 5x.

This still implies upside, although begs the question of if there are any catalysts to drive value. With sales continuing to decline, we suspect the business will see little price action until conditions improve.

Final thoughts

Lenovo has done a fantastic job of gaining market share, offering a compelling price-to-quality trade-off. With a diversified revenue profile, the company is improving its resilience, although currently relies heavily on its PC operations. The biggest issue we have is that the business operates with very slim margins, making it quite unattractive.

With Dell and HP experiencing a contraction in their trading multiples, our view is that Lenovo's fair value should also decline. With trading conditions difficult, we suggest patience in the current year.

For further details see:

Lenovo: Market Leader With Unattractive Margins