FINMY - Leonardo: We Should Take Advantage Supportive Order Pipeline

2023-05-06 21:16:07 ET

Summary

- Supportive order intake in the quarter and 2023 guidance confirmed.

- Free cash flow evolution compensates for worse profitability.

- Moody's raised its rating and we wait for an investment grade upgrade from S&P. Our buy rating is then confirmed.

The Leonardo ([[FINMF]], [[FINMY]]) stock price is falling in Piazza Affari with a minus -4.57% to €10.45 per share and an intraday minimum at €10.125; however, in the last month, Leonardo's stock grew by 14%. Here at the Lab, in mid-December 2022, we provided a buy target and since then, we are up by almost 40%.

{kind=link}

In our last update called ' Positive Catalysts Likely To Price In ', we were expecting a mixed quarter. In detail, we reported that Q1 is " usually the least significant " account, and we were forecasting " a good start both in terms of top-line sales and order collection ". Concerning the cash flow development, we anticipated a reduction in Leonardo's cash flow absorption to €750 million from €1 billion (delivered as a comps analysis last year in the same quarter). Double checking our internal estimates, revenues were below expectation, but cash flow significantly stepped up and signed just a minus €688 million.

{kind=link}

Source: Leonardo Q1 press release

Q1 results

Starting with the positive news, it was a growing first quarter for Leonardo. The company recorded a step up in order collection for an additional €4.9 billion with a +29.3% on a quarterly basis, which brings the current order portfolio to over €39 billion which is equal to more than 2.5 years of production. In addition, in the Q1 conference call, Leonardo's CEO underlined that there is a positive feeling toward the 2023 new order collection, but it is too early to improve it. As already mentioned, top-line sales slightly increased to €3 billion (+2.6%), but Leonardo's operating leverage is working well and recorded an adj. operating profit increase by 4.4% compared to Q1 2022. Below expectations was the EBITA which signed a minus 20% to €105 million. This was due to the lower contribution of the strategic joint ventures and Hensoldt's performance, in which Leonardo holds a 25% equity stake. As a result, net income decreased 46% on a yearly basis to $40 million (consensus was estimating a net profit of €48 million).

{kind=link}

Source: Leonardo Q1 results presentation

More important to note is the debt evolution, this is key in our initial investment. Debt evolution has always been a negative takeaway in the Wall Street investor community. In detail, debt decreased by €1.1 billion compared to the first quarter of 2022, thanks to the strengthening of the group's organic cash generation. Operating cash flow is still negative by €688 million but marks an improvement of approximately €400 million.

Upside on Agency Rating upgrades

Just before the quarterly accounts, Moody's debt promotion was also announced. Leonardo is back at an Investment Grade level, and the rating agency revised its long-term rating upwards to Baa3, with a stable outlook. The upgrade, as the rating agency underlines " reflects the group's resilience during the pandemic, a substantial deleveraging, and the solid growth prospects of the defense sector ". According to Moody's and thanks to the increase in the defense budget, we are forecasting favorable market conditions in the next 12-18 months.

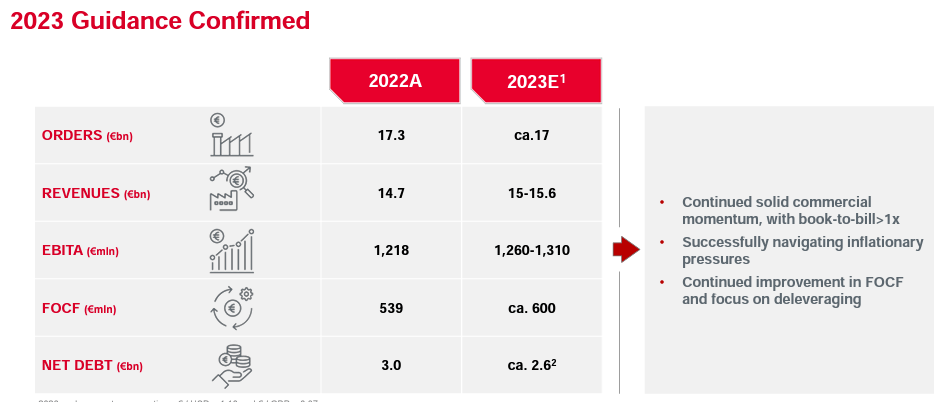

S&P remains the only one of the three major rating agencies that consider Leonardo junk; however, the last update dates back to May 2022. Here at the Lab, we expect an imminent upgrade. Indeed, based on a €/$ exchange rate of 1.10, Leonardo confirmed its 2023 estimates, forecasting orders of around €17 billion and revenues in a range between €15 and €15.6 billion, and a net debt decrease to €2.6 billion, assuming a dividend payment of €0.14 per share.

Conclusion and Valuation

According to our calculation, including IFRS and a lower EBITA, Leonardo's leverage ratio reached 2.1x in Q1 2023 compared to the 2.9 times last year-end quarter. Leonardo's operating results are lower than expected but strong order collection and the best free cash flow evolution thanks to the net working capital more than offset this negative performance. Here at the Lab, we are not forecasting this WC improvement entirely recurring. In detail, this positive outcome benefited from significant milestones for order deliveries in progress that were not quantified during the call. The financial year target is substantially in line with our guidance and order intake enhances more visibility on 2023 estimates. Therefore, we reaffirmed our buy rating with a price target of €14 per share. As a reminder, Leonardo is currently trading in the bottom P/E quartile in the defense sector and is offering an FCF of 12.5% by 2025. Even looking at the Italian comps, Fincantieri is trading at a higher valuation with no justification. We suggest to our readers to benefit from this -5% at the stock price level and take advantage of the momentum to start a position (or increase it).

{kind=link}

For further details see:

Leonardo: We Should Take Advantage, Supportive Order Pipeline