LXRX - Lexicon Pharmaceuticals: May 27 PDUFA Date For Heart Failure Drug Looks Crucial

2023-05-19 14:38:24 ET

Summary

- Lexicon ought to find out whether its heart failure candidate sotafligozin will be approved on May 27.

- The drug has been rejected before - in 2019, in patients with Type 1 diabetes, on safety grounds.

- Astrazeneca's Farxiga and Lilly's Jardiance have the same MoA as sotafligozin and have been approved in heart failure, generating blockbuster sales.

- If sotafligozin is approved it could open up a blockbuster market opportunity for Lexicon - provided it can compete with big pharma rivals.

- The fact that Sanofi was originally Lexicon's big pharma partner with sotafligozin, but pulled out of the partnership after the FDA rejection in 2019 could be telling.

Investment Overview

Texas based biotech Lexicon Pharmaceuticals ( LXRX ) was incorporated in 1995, and has been listed on the Nasdaq since 2000. According to a statement in the company's 2022 10K submission, Lexicon is:

... devoting most of our resources to the research, development and preparation for commercialization of our most advanced drug candidates: Sotagliflozin , which we are developing as a treatment for heart failure and type 1 diabetes, and LX9211, which we are developing as a treatment for neuropathic pain. We have also advanced a number of additional compounds into various stages of clinical and preclinical development.

On May 27 Lexicon expects to find out from the FDA whether sotagliflozin has been approved for commercial use. The Prescription Drug User Fee Act ("PDUFA") date - when the FDA makes its final determination based on clinical evidence from late stage studies - was set after Lexicon submitted its New Drug Application ("NDA") last year. That NDA was, according to its 10K:

supported by positive results from two Phase 3 clinical trials evaluating the effect of sotagliflozin on long-term outcomes related to cardiovascular death and heart failure in approximately 10,500 and 1,200 patients, respectively.

If approved, sotaglifozin will be commercially available to:

... reduce the risk of cardiovascular death and hospitalization for heart failure in adults with heart failure and in adults with type 2 diabetes mellitus, chronic kidney disease and other cardiovascular risk factors.

If approved, Sotaglifozin - which is a member of a class of drugs known as SGLT2 inhibitors - would compete against SGLT2 inhibitors developed by AstraZeneca ( AZN ) - dapagliflozin, brand name Farxiga, 2022 revenues of $4.3bn in FY22 - and Boehringer Ingelheim and Eli Lilly ( LLY ) - empagliflozin, brand name Jardiance, 2022 revenues of >$2bn.

Lexicon's current market cap is just $548m - its share price is +71% across the past 12 months, but -71% across the past five years - hence it's easy to reach the conclusion that, should sotaglifozin be approved later this month, Lexicon's share price will surely climb substantially higher, based on the market opportunity in play.

PDUFA dates are stand-out catalysts for biotech companies, and especially pre-commercial biotechs like Lexicon, since an approval marks the transition from pre-commercial to commercial, and in Lexicon's case, an opportunity to target a double-digit-billion dollar market opportunity, as defined by the company's President and Chief Financial Officer ("CFO") Jeff Wade on its Q123 earnings call:

There are nearly 7 million people in the United States living with heart failure, a number that is expected to increase to 8 million by 2030. Heart failure is the leading cause of hospitalization for Americans over 65, with approximately 1.3 million hospitalizations for heart failure annually. Patients who are hospitalized for heart failure are highly likely to return with approximately 25% of patients being readmitted to the hospital within 30 days of discharge and 65% within one year.

Hospital readmissions are burdensome not only for patients but also to the healthcare system, annual cost from heart failure expected to increase to nearly $70 billion by 2030 with 80% of those costs due to hospitalizations. There is a substantial unmet need for better treatment options for patients, and as these data make clear, a strong incentive for providers, hospitals and payers to identify new approaches to reduce hospital readmissions.

Of course, if sotaglifozin is not approved on May 27, it will likely spell trouble for Lexicon and its share price. The company has made a net loss of $(102m), $(88m), and $(59m) in FY22, FY21 and FY20, respectively, and in Q123 net loss was $32m, or $0.17 per share, and cash position was reported as just $106m. Lexicon's total accumulated deficit is in excess of $1.6bn.

Sotaglifozin has already been rejected by the FDA in the indication of Type 1 diabetes - in 2019, on safety grounds, when the French pharma giant Sanofi ( SNY ) was a partner. Sanofi subsequently ended its interest in the drug, whilst Lexicon has twice appealed the decision, saying that its NDA was:

... supported by positive results from three Phase 3 clinical trials evaluating the effect of sotagliflozin on type 1 diabetes in approximately 800, 800 and 1,400 patients, respectively.

According to the 2022 10K:

In November 2020, we requested an opportunity for an administrative hearing on whether there are grounds for denying approval of our NDA. In response to such request, the FDA issued a public Notice of Opportunity for Hearing in March 2021 and the hearing process is ongoing.

The investment opportunity therefore feels like a case of "feast or famine." If the FDA declines to approve sotagliflozin in a week's time, then Lexicon may have to accept that it is no longer worth pursuing approval in the US, despite the fact the drug has won approval to treat Type 1 Diabetes in Europe.

If the FDA opts to approve the drug, it will open up an opportunity of real significance for Lexicon, although it has to be said, the small biotech will be up against some fierce Big Pharma competition as it attempts to gain a share of the market.

We will therefore almost inevitably see a sharp spike or decline in Lexicon's share price in a week's time - but which way will the decision go? Let's try to consider the arguments for and against in the remainder of this post.

Sotaglifozin - Studies and Data

A question worth asking about sotaglifozin is whether it offers any advantages that Farxiga and Jardiance, its approved rivals with a broadly similar mechanism of action ("MoA") do not?

Farxiga was initially rejected for approval by the FDA in 2012, after the agency requested more data, but was approved to treat Type 2 Diabetes in 2014, and then in 2019 "to reduce the risk of hospitalization for heart failure" for the same patients, before securing approval for treatment of heart failure with reduced ejection fraction in 2020, then for Chronic Kidney Disease in 2021, and finally, this month , to "reduce the risk of cardiovascular ( CV ) death, hospitalisation for heart failure (hHF) and urgent heart failure ( HF ) visits in adults with HF."

Jardiance also was initially rejected in 2014, then approved to treat Type 2 diabetes in 2014, then to "reduce cardiovascular death in adults with T2D" in 2016, then for heart failure with reduced ejection fraction in 2021, and in February last year, for "adults with heart failure regardless of left ventricular ejection franction.

Clearly, both of these drugs are now trusted by the FDA on both safety and efficacy grounds.

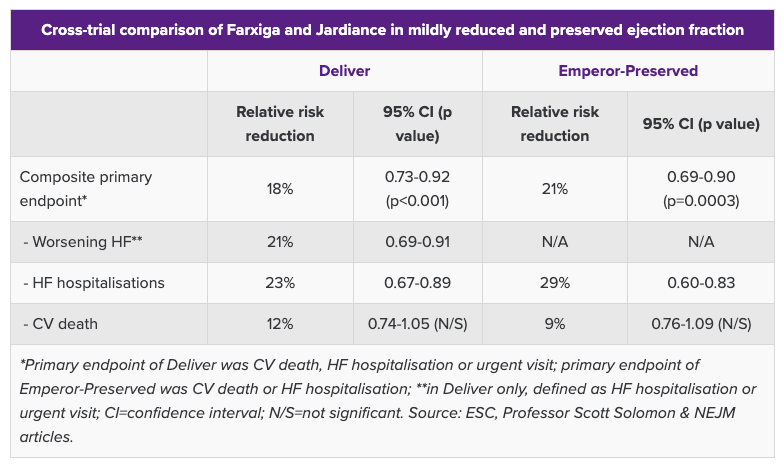

Farxiga / Jardiance compared in heart failure studies (Evaluate Pharma)

{kind=link}

The above table compiled by Evaluate Pharma shows that in their pivotal studies, Farxiga and Jardiance reduced the risk of death of hospitalization by 18% and 21% respectively, and reduced the risk of hospitalisations only by 23% and 29%.

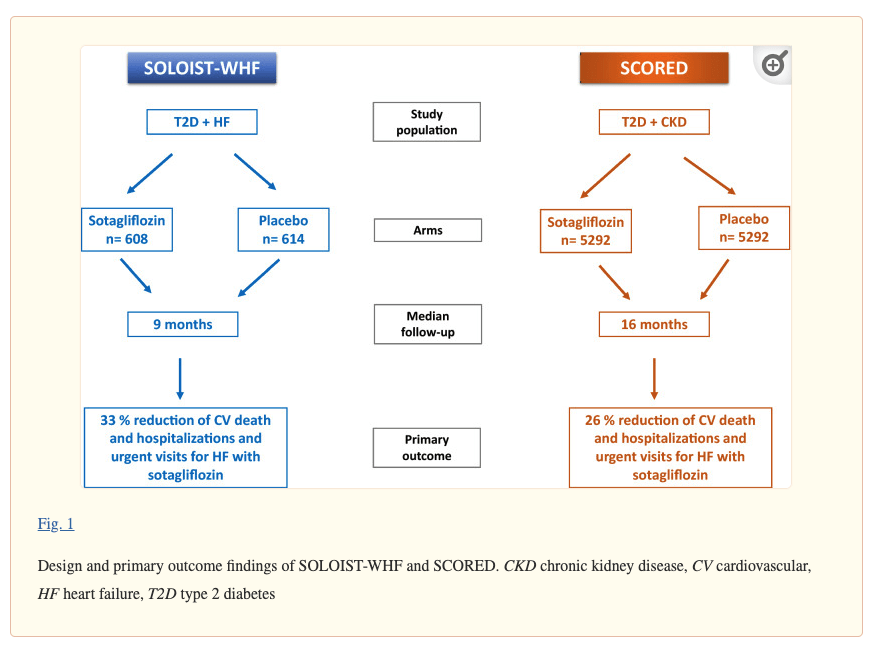

In its pivotal SOLOIST-WHF study of 1,222 "patients with type 2 diabetes who had recently been hospitalized for worsening heart failure," Sotaglifozin met its primary endpoint of number of deaths from cardiovascular causes and hospitalisations and urgent visits for heart failure." Results were published in the New England Journal of Medicine ("NEJM"), indicating the primary end point was met as follows:

Among these patients, 600 primary end-point events occurred (245 in the sotagliflozin group and 355 in the placebo group). The rate (the number of events per 100 patient-years) of primary end-point events was lower in the sotagliflozin group than in the placebo group (51.0 vs. 76.3; hazard ratio, 0.67; 95% confidence interval [CI], 0.52 to 0.85; P<0.001).

The rate of death from cardiovascular causes was 10.6 in the sotagliflozin group and 12.5 in the placebo group (hazard ratio, 0.84; 95% CI, 0.58 to 1.22); the rate of death from any cause was 13.5 in the sotagliflozin group and 16.3 in the placebo group (hazard ratio, 0.82; 95% CI, 0.59 to 1.14).

NEJM concluded as follows:

In patients with diabetes and recent worsening heart failure, sotagliflozin therapy, initiated before or shortly after discharge, resulted in a significantly lower total number of deaths from cardiovascular causes and hospitalizations and urgent visits for heart failure than placebo.

A much larger study, SCORED, evaluated >10,000 patients with Type 2 Diabetes + Chronic Kidney Disease - results from both studies were summarised as below in an abstract published online :

primary outcome findings from SOLOIST-WHF and SCORED studies (ncbi.nlm.nih.gov/pmc/articles/PMC8261816/)

{kind=link}

The results appear to be quite encouraging - although extreme caution should be exercised when comparing the pivotal study results of different drugs as no two studies are ever quite the same - and the abstract concludes that:

... despite their limitations, SOLOIST-WHF and SCORED trials reconfirm the substantial benefits of SGLT2i in people with T2D, renal disease, and/or HF.

The "limitations" mentioned refer to the fact that "both trials were prematurely interrupted due to loss of funding from their main sponsors," i.e. Sanofi, who washed their hands of sotafligozin back in 2019. Nevertheless, there does seem to a be a consensus that the drug can compete with its already approved rivals - another paper published online in February 2019 concludes:

Although the specific CardioVascular Outcome Trial is still under way, it can be affirmed that sotagliflozin seems to share all the advantages of the other, already available, SGLT-2 selective inhibitors. In contrast with other SGLT-2is, however, sotagliflozin has the added advantage of delaying glucose absorption in the intestine.

In conclusion, sotagliflozin seems to represent a promising treatment for both type 1 and type 2 diabetes, either alone or in combination with metformin or DPP-4 inhibitors in type 2 diabetes or, with an adequate insulin protocol, in type 1 diabetes.

The dual inhibition of both SGLT-1 and SGLT-2 improves the efficacy of this SGLT inhibitor also in mild and severe CKD, suggesting an extended use also in frail patients where therapeutic options are currently limited.

What Reservations Does The FDA Harbour About Sotaglifozin?

Safety appears to be the issue that's causing the FDA to be hesitant to approve this drug. It's worth noting that Sotafligozin has a slightly different MoA to Jardiance and Farxiga in that it inhibits SGLT-1 and SGLT-2, whilst Farxiga and Jardiance target SGLT-2 only.

The FDA told Lexicon in its Complete Response Letter issued back in March 2019 that:

The (pivotal study) data demonstrated that the addition of sotagliflozin to insulin is associated with an increased risk of diabetic ketoacidosis (DKA), a serious and often life-threatening consequence of insulin insufficiency.

Time-to-event analyses of the clinical trial data showed earlier development of DKA in sotagliflozin-treated patients than in patients assigned to placebo, without evidence that the risk stopped increasing.

In other words, the FDA suspects that the drug is unsafe and has some reasonably persuasive evidence to prove it, but Lexicon maintains that Farxiga and Jardiance carry a similar risk, and that the FDA is applying a different criteria of judgment to Lexicon that it did to AstraZeneca and Lilly - a course of action Lexicon has described as "arbitrary and capricious."

Frankly, it's pretty rare for a biotech company to challenge the FDA's approval decisions as robustly and repeatedly as Lexicon has done, and it may not bode particularly well for an approval nod on May 27 as the original dispute rumbles on. Prior to the approval decision back in 2019, according to Endocrine today :

... the Endocrinologic and Metabolic Drugs Advisory Committee voted 8-8 in a decision on whether to recommend approval of sotagliflozin (Zynquista) with several members expressing concerns about an observed risk in diabetic ketoacidosis and calling for a risk evaluation and mitigation strategy if the therapy is approved.

The FDA is not obliged to follow the recommendation of its AdComm, but a split decision may have given the agency food for thought - and perhaps the agency may be prepared to view the safety issues in a more favorable light based on the evidence gathered from so many patients in clinical studies, and the different indication. It's interesting to note that Sotafligozin is approved for both Type 1 and Type 2 diabetes in Europe.

Concluding Thoughts - Upcoming PDUFA Date Has Massive Implications For Lexicon

It's hard to escape the fact that May 27 will be a momentous day in Lexicon's history whether sotafligozin is approved or not.

Drugs that share sotafligozin's MoA have been approved to treat Type 2 diabetes and heart failure in the US, and in Europe, sotafligozin has even been approved in Type 1 diabetes.

The FDA had reservations about whether the use of the drug leads to diabetic ketoacidosis (DKA), causing it to reject the drug in T1D, but the agency also did reject both Jardiance and Farxiga initially, before greenlightling them. The rejections for the latter 2 drugs were not due to the same safety reasons that caused it to reject sotafligozin, however.

The ongoing dispute around the T1D indication is unlikely to play in Lexicon's favour in my view. Although Lexicon seemingly has a point around the FDA's double standards, the agency does have proof from Lexicon's clinical studies that DKA was more common in sotafligozin arms than in placebo arms. Another issue for Lexicon could be the fact its trials were not fully completed owing to a combination of Sanofi's departure, COVID, and a lack of funding.

I wonder if these objections will ultimately lead to the FDA saying "no" to Sotafligozin once again, or requesting more / different data i.e. another expensive clinical study. And even if the agency approves the drug, although any shareholders will doubtless benefit from a short-term spike in the share price, could Lexicon genuinely establish a meaningful market share against the likes of Farxiga, Jardiance, and Johnson & Johnson's ( JNJ ) Invokana, another drug with the same MoA? Is its candidate sufficiently differentiated, or better in any meaningful way?

Recently, the biotech Provention Bio ( PRVB ) was acquired by Sanofi in a deal worth $2.9bn, after its once-rejected T1D prevention therapy, Tzield, gained approval in the US. Provention shareholders (and I was one of them) did very well out of this deal, making gains of >250% in under 1 year.

It's tempting to think that Lexcion could be another Provention, but I think ultimately I'm a little skeptical due to the FDA having concerns around safety (however unfounded they may be). In Proventions' case it was manufacturing issues that caused the initial rejection - generally, the type of issue that is far easier to resolve than a safety issue.

Lexicon does have other assets at a reasonably advanced stage, so if the company is forced to ditch sotafligiozin it won't necessarily be the end of the road, although funding issues will start to become a real problem if there is no prospect of near term commercialization.

I'm not going to state outright whether I think Lexicon will be celebrating an approval or not come May 27, as the FDA is hard to predict - perhaps the European approvals or Lexicon's non-stop lobbying will persuade it to say yes this time. I'm not confident enough to issue a "buy" recommendation however - I'll be staying on the sidelines for this very significant upcoming catalyst.

For further details see:

Lexicon Pharmaceuticals: May 27 PDUFA Date For Heart Failure Drug Looks Crucial