LGIH - LGI Homes: Buying Into The Margin Recovery

2023-11-23 10:42:49 ET

Summary

- LGI Homes, Inc. stock gained 6.3% after reporting earnings, with a return to pre-pandemic margin levels.

- The company's gross margins have improved, driven by pricing power through strong demand, lower input costs, and mix improvements.

- LGIH's revenue growth is modest but is expected to continue as the company plans to expand its number of communities.

Introduction

LGI Homes, Inc ( LGIH ) gained 6.3% after reporting earnings the morning of October 31. The timing was fortuitous. The good news of a return to pre-pandemic margin levels coincided with the beginning of the period of seasonal strength for the stocks of home builders which in turn is riding the coattails of a market celebrating a presumed end to Fed rate hikes (thanks to a well-liked October CPI report). Altogether, LGIH is up over 35% at the time of writing.

Still, the stock looks like a “cautious” buy for at least the duration of the seasonal period. As I demonstrated in an earlier article , analysts ratings on home builders appear highly correlated to margin and revenue dynamics. The margin story works in LGIH’s favor for this model while the revenue growth story is still unfolding. Analysts currently have a hold rating on LGIH with only one buy rating and an average price target of $118 (a dollar below the current price). So if my read on LGIH is correct, the stock has more upside assuming upgrades are forthcoming. Even so, the Quant ratings are on my side with a clear buy signal.

Margins

LGIH has been striving to get back to and sustain pre-pandemic gross margins. Four years ago the company reported a quarterly gross margin of 24.1% and adjusted gross margin of 26.3%. For this year’s Q3 earnings report , LGIH delivered a gross margin of 25.7% and adjusted gross margin of 27.2% (190 basis points above guidance). The nine months ending with Q3 delivered 22.8% and 24.5% gross margin and adjusted gross margin respectively compared to 2019’s 23.9% and 26.0%. Thus Q3 delivered the turn toward the company’s goal. Management explained the margin drivers in prepared remarks and during Q&A. Directly quoted from the Seeking Alpha transcript :

- Success in maintaining and where possible raising prices in many communities [driven by a very strong demand environment]

- Lower input costs

- New and replacement community openings at normalized margin profiles

- [Not] a lot of wholesale closings [which carry lower margins]

Given the current momentum, LGIH boosted the lower end of its margin guidance by 150 basis points. The company now expects full year gross margin between 23% to 23.5% and adjusted gross margin between 24.5% and 25%. Geographic mix, wholesale mix, and incentive levels during Q4’s “Make Your Move National Sales Event” cause variability in the margin guidance.

The stronger gross margins helped LGIH deliver record pre-tax profit margin of 14.5%, excluding the pandemic period.

On the cost side, although development costs are increasing, LGIH explained that input costs have been very stable. A declining cost in lumber will support margins starting in Q1 of 2024.

Revenues and Demand

LGIH reported home sales revenues of $617.5M for Q3 and home sales revenues of $1.8B for the 9 months ending with Q3. The growth from Q3 2002 was 12.9% and 0% respectively so revenue momentum has improved over the course of the year. Accordingly, LGIH described demand as “healthy”:

“A great example of [demand] is the 1,751 homes we closed in the third quarter. This was a 13.2% increase over the same period last year and represented a strong pace of 5.6 closings per community per month.”

LGIH tightened the range on expected closings for the year to between 6,700 and 7,000 homes from 6,500 and 7,200 homes . So while uncertainty dropped and the lower end of the range went higher, the potential upside was clipped by 200 homes. The projected average selling price ((ASP)) went from a range of $345,000 to $360,000 to $350,000 and $355,000 for the full year. Again, uncertainty went down with a higher floor but clipped upside. The presumed range for 2023 revenue is $2.35B to $2.49B, a small potential increase of 2.2% to 8.9% from 2022’s home sales revenue of $2.3B .

While this revenue growth looks modest, management’s announcement that “we now expect to end 2024 with over 150 communities and to be operating in over 180 communities by the end of 2025” suggests that the overall revenue momentum should continue into the next two years. LGIH ended Q3 with 106 active communities, a 14% year-over-year increase and 4% quarter-over-quarter increase. The company is aggressively targeting 115 to 125 communities by the end of the year.

The change in revenue dynamics is also driven by affordability issues. Smaller homes weigh on revenue upside. While LGIH did not discuss average home size, the housing market is generally trending toward smaller homes. According to a recent report from the National Association of Home Builders (NAHB), average home size in Q3 hit its lowest level since 2010. Historically low interest rates in the wake of the pandemic briefly interrupted a downtrend that started from a peak in 2014. (I would like to see builders more consistently report on the distribution of square footage of sales, at least something like a revenue per square foot measure).

Valuation

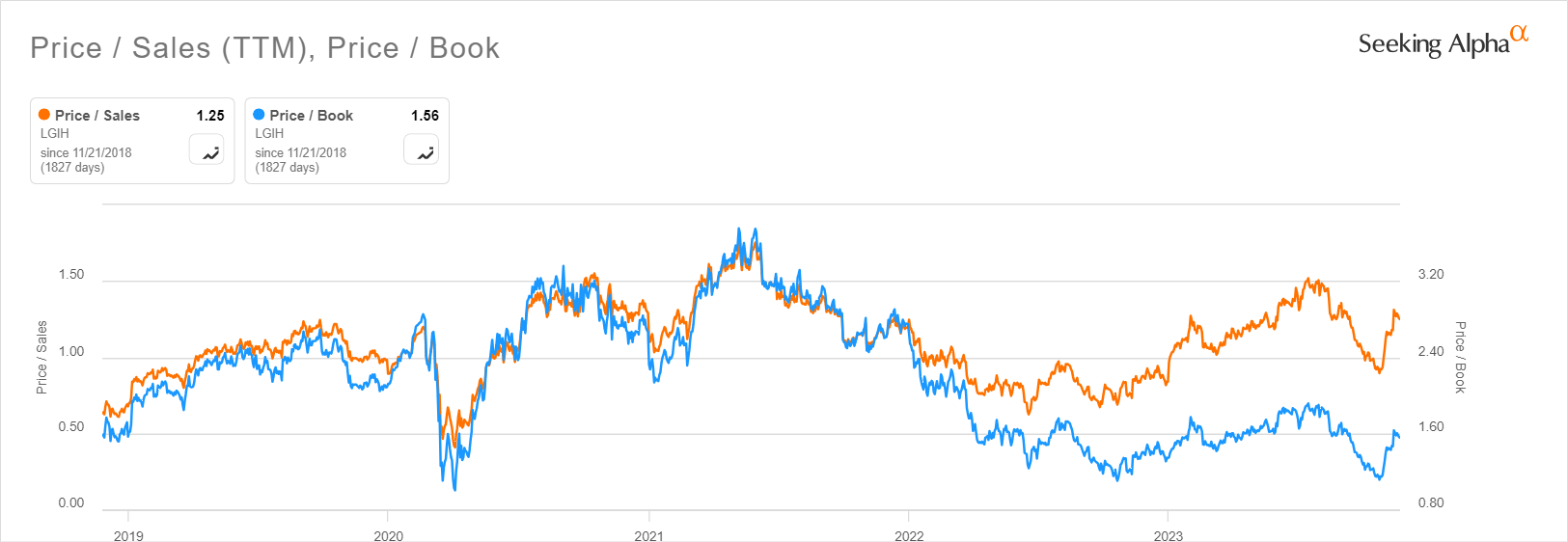

LGIH has typically been one of the more expensive builders because of a strong growth profile. The housing recession (the decline in sales and transactions) hit the stock LGIH particularly hard. The stock fell from an all-time high of $178 in May, 2021 to a trough of $74 in June, 2022, a plunge of 58%, almost as bad as the most speculative of tech stocks. LGIH’s price/book ratio troughed 4 months later at 1.1, a typical recession valuation for builders. Price/book is now at 1.5, below the year’s high of 1.8 and the peak of 3.7 in 2021.

The most interesting feature of LGIH’s valuation is a distinct divergence between the price/book and price/sales ratios . These valuation metrics were perfectly correlated from at least 2019 to 2022. This year, the price/sales ratio took off while price/book lagged.

This year, LGHI price/sales diverged from price/book (Seeking Alpha)

{kind=link}

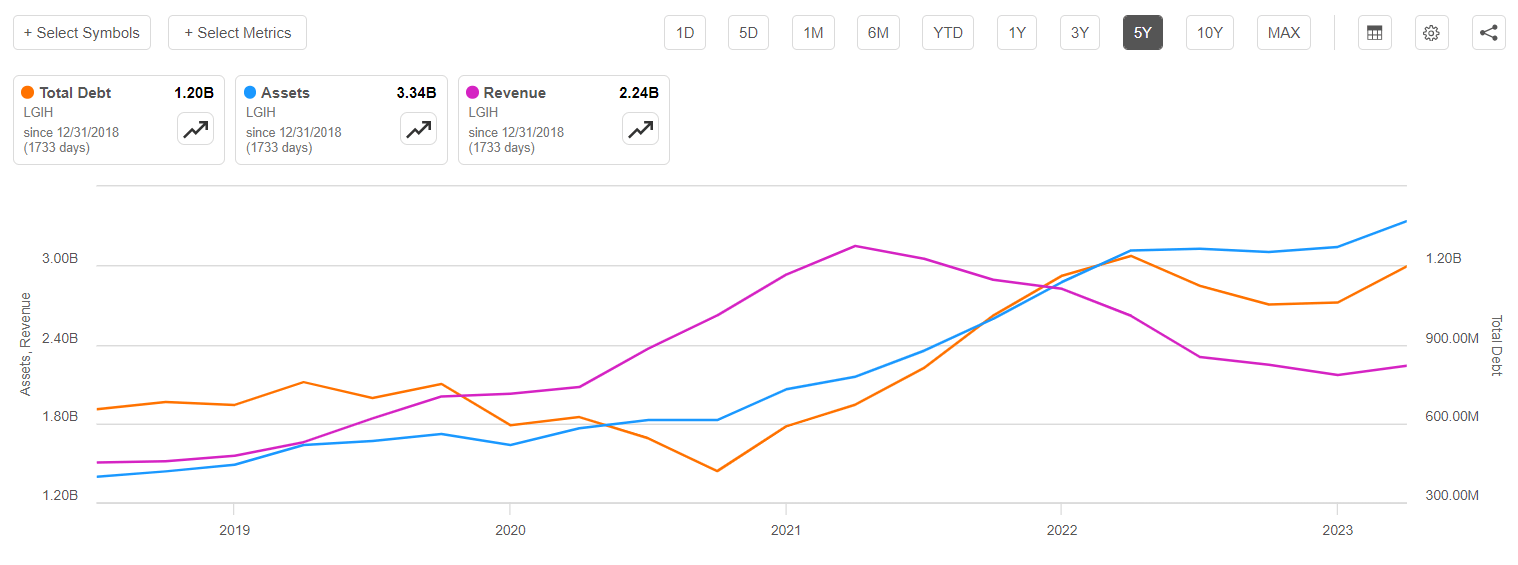

In other words, sales growth is lagging asset value growth. A graph of revenue versus total assets approximately tells the story. Increasing debt appears to support the increasing asset value. LGIH has been investing in its ability to meet future demand which it sees as relatively robust for the next two years. (Note my observations are all approximate).

{kind=link}

Conclusion and The Trade

While the margin story is more compelling for LGIH than its revenue story, I think the mixed picture presents the window of opportunity to start buying into LGIH. Moreover, LGIH has a lot of “head room” before it ever gets back to peak (boom time) valuations.

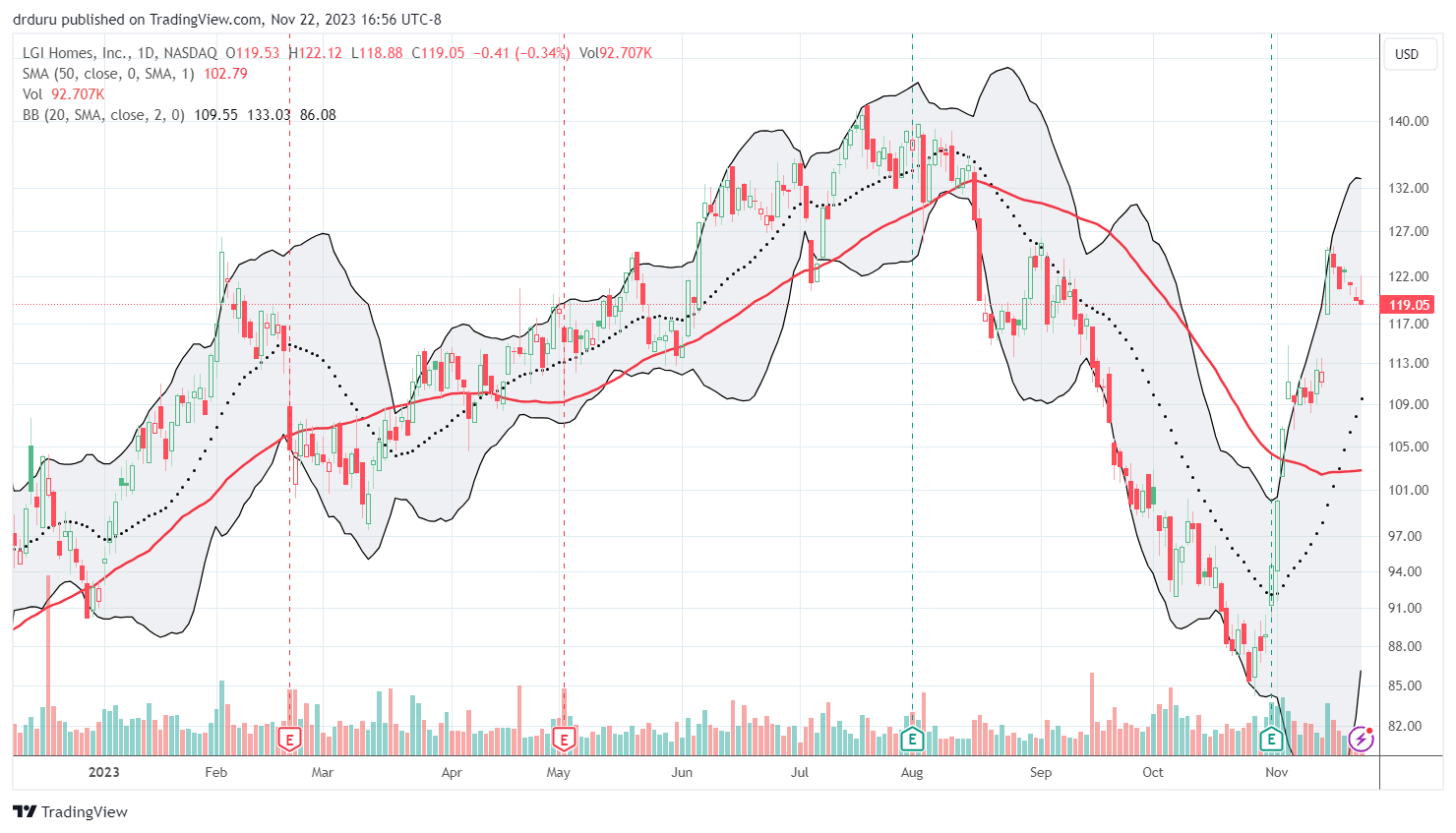

From a technical standpoint, the run-up to current price levels was so swift that LGIH (like other home builders) looks ready for a period of cooling to consolidate gains. For example, LGIH soared 11.3% in just one day as rate sensitive stocks celebrated a favorable October CPI report. That extreme move likely soaked up a lot of future buying enthusiasm, so I am not surprised to see LGIH drifting lower since that big day.

Thus, my buying strategy for this season features accumulating LGIH over time as far down as its 50-day moving average ((DMA)) (the red line in the chart below). In the meantime, I am looking for housing data to show a turn-around in builder sentiment (which in November approached last year’s recession low which was in turn the same low in the wake from the pandemic) to accompany lower mortgage rates and on-going resilience in the economy.

Time to cool for the V-bounce since Q3 earnings? (TradingView.com)

{kind=link}

Be careful out there!

For further details see:

LGI Homes: Buying Into The Margin Recovery