LGIH - LGI Homes Faces Headwinds In 2023 But Presents Long-Term Investment Opportunity

2023-03-09 05:37:32 ET

Summary

- LGI Homes is a very successful homebuilder that offers affordable housing for first-time home buyers.

- Underperforming other builders, sales dropped by 24% in 2022.

- LGIH's emphasis on price-sensitive customers makes it vulnerable to asymmetric impacts from macro headwinds.

- Despite short-term pessimism, the long-term outlook for the stock remains promising.

LGI Homes, Inc ( LGIH ) is a leading affordable and spec home builder based in Woodland, TX. With its focused and unique strategy, LGIH has established itself as one of the fastest-growing builders in the nation. However, as the macro environment is expected to remain turbulent in 2023, LGIH may face significant challenges in navigating the market. Despite this, a downturn in the market could also present an opportunity for long-term investors to buy into the company's growth potential.

Recent business update

LGIH has recently released its 2022 full-year report and unfortunately, the results were not up to par. Sales were down by a significant 24% to 2.3B and net income was only 34.1M. The number of home closings for the year was 6621, a 36.6% drop and a slight miss of expectations. These results highlight the cyclical nature of the business, and during macroeconomic headwinds, companies like LGIH need time to adjust. Despite the challenging conditions, profitability remained at a high level, with a gross margin over 28% and net income margin exceeding 14%. Furthermore, the net-to-debt ratio improved by 2.5% to below 40%.

Inventory level surges with lower orders and higher canceling rate

The chart above clearly indicates that LGIH has been experiencing a significant slowdown in its revenue growth while its inventory levels continue to grow at a high pace. Despite canceling many controlled lots, the total lot inventory was still relatively high at 71904, which is a 22% decrease compared to the previous year. Interestingly, the company-owned lots have increased by 7% to 58720, with 47857 being unfinished lots. This suggests that LGIH remains very aggressive in developing land and expansion compared to other builders.

LGIH, as an affordable housing company, faces a significant challenge when inflation is high and mortgage rates exceed 7%. This is evident from the cancellation rate, which has increased by 500 basis points to 24.4% this year. LGIH intends to maintain its construction pace, but lower orders and higher cancellations will put a lot of pressure on its cash flow. The company's operating cash flow has recorded its worst ever at negative 370 million dollars. As a result, the management has decided to pause stock repurchases in the fourth quarter and focus instead on maintaining liquidity. Commenting on the situation, CEO Eric Lipar stated :

And when interest rates spiked up to 7% in Q4 and our sales were slower, we focused on cash, we focused on moving the standing inventory.

In the short term, it seems that the management team at LGIH made a mistake in predicting market trends and didn't respond quickly enough to the decline in customer demand. However, looking at the bigger picture, it is understandable that LGIH is committed to developing and maintaining its relationships with local contractors. By doing so, the company can continue to operate under its low-cost model, ensuring long-term profitability.

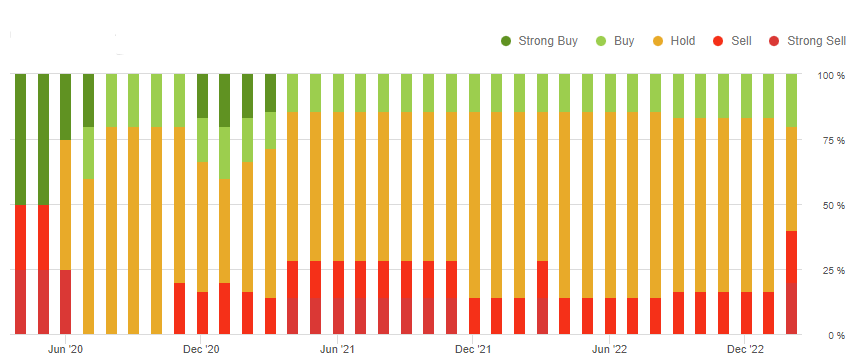

Wall Street Downgrades

{kind=link}

Given the macroeconomic concerns, there has been an increase in sell ratings from Wall Street analysts recently. The analysts believe that there is a potential risk to margins and volumes, which could affect the performance of companies like LGIH. LGIH's customer base is considered to be the most sensitive to interest rates among all the builders, which makes the earnings per share estimates potentially more fragile. Serving first-time home buyers is a double-edged sword. On the one hand, LGIH can benefit from higher closing and absorption rates compared to other builders. However, first-time home buyers are often barely qualified for home purchases, and when rates change dramatically, they could be qualified one week and out of luck the next. This makes it difficult to accurately estimate the company's future earnings and growth potential.

Historically, LGIH has been known to trade at a premium compared to other builders. However, after 2022, this trend began to change as interest rates became a significant factor affecting LGIH's earnings power. As a result, we can observe that LGIH's multiples began to decline (chart below).

LGI's Resilience and Quality Under Scrutiny in 2023

Home builders are constantly faced with the challenge of dealing with cynical economic trends. For LGIH, maintaining their market positions, pricing powers, and business relations with their suppliers will be crucial in 2023. In response to these challenges, LGIH's management has taken measures to increase affordability, including offering smaller home plans and financing incentives. They are also working with their contractors and suppliers to reduce high-cost items. Fortunately, there is good news, as the closing number for February 2023 looks promising, with a 1.4% year-over-year increase and 506 homes sold. However, it's worth noting that LGIH has 97 active selling communities, compared to 89 in the previous year.

Bottom Line

LGI Homes has shared their outlook for the year 2023, they anticipate closing between 6,000 to 7,000 homes. These homes are expected to have an average sales price between $335,000 to $350,000, resulting in sales of about 2.1B to 2.5B, which is similar with 2022. The company also predicts that their full-year gross margins will remain similar to pre-pandemic levels, with a decline of between 21% and 23% and adjusted gross margins ranging between 22.5% to 24.5%. With new communities set to come online, LGI Homes expects to end 2023 with 115 to 125 active selling communities. It appears that the management is not expecting the significant company-wide downturn that occurred in 2022, with a year-on-year decrease of 24%.

It is expected that the media will report a lot of negative news on the housing market in 2023. Despite this, I think LGIH may not have as bad financial results due to their management's preparation and the current low housing supply in the country. LGIH's affordability may also be a potential strength, as it could attract higher-level home buyers who are looking for affordable housing options. This may present an opportunity for contrarian traders. Despite facing some temporary headwinds in 2023, LGIH is still in a strong position to emerge as a leading builder in the United States over the long term due to the increasing income inequality in the US. The management has expressed a clear objective of doubling the size of its business, and LGIH has shown the best revenue growth at a per share basis in the last ten years. Given the current enterprise value of 3.48B and net income of 0.3B, I anticipate that LGIH's stock price will significantly increase in the next five years.

For further details see:

LGI Homes Faces Headwinds In 2023 But Presents Long-Term Investment Opportunity