LGIH - LGI Homes: Near-Term Risks Remain Initiate At Hold

2023-09-27 07:10:38 ET

Summary

- LGI Homes has benefited from the lack of resale inventory driving new home sales.

- Housing market remains challenging amidst high mortgage rates and affordability index at record lows.

- We believe downside risks remain on the ASP as consumers increasingly look for smaller sized homes.

Investment Thesis

LGI Homes ( LGIH ) had a strong year along with rest of the homebuilders due to the lack of resale inventory driving new housing sales. Its positioning within entry level home segment enables them to capitalize on a rising segment which has led to an uptick in the housing closings. We believe the challenges remain in the near term as consumers continue to look for smaller sized homes (which now forms 27% of Q2 2023 closings) and declining ASP of homes. Housing market remains challenging with the Fed's narrative to hold rates for longer and a persistently higher mortgage rates which has crossed 7% now. Despite the 25% decline in its market value over the past two months, LGIH stock still trades at a premium to its peers and historical averages. We initiate at Neutral.

Company Background

LGIH is engaged in providing attached and detached entry-level homes with average home size ranging between 1,000 to 4,100 sq. feet across 20 states in the US. Its average home sales price ranges about $350k and currently offer homes for sale in about 100 communities across the US.

Historical Track Record

LGI Homes has reported a strong growth historically with robust revenue and earnings momentum which grew 34% and 41% respectively during 2014-2021 period, however stumbling in 2022 amidst record rise in mortgage rates. Home closings has also witnessed a strong growth jumping over 5x over the similar period along with a consistent uptick in the average sales price. It has been able to maintain stable gross margins over the period along with improvements in net profit margins driven by revenue growth outpacing SG&A costs.

| Particulars |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Home Closings |

| 2.4k |

| 3.4k |

| 4.2k |

| 5.8k |

| 6.5k |

| 7.7k |

| 9.3k |

| 10.4k |

| 6.6k |

| ASP ($ '000) |

| 163 |

| 185 |

| 201 |

| 215 |

| 231 |

| 239 |

| 254 |

| 292 |

| 348 |

| Revenue () |

| 383 |

| 630 |

| 838 |

| 1,258 |

| 1,504 |

| 1,838 |

| 2,368 |

| 3,050 |

| 2,304 |

| Gross Margin |

| 28% |

| 28% |

| 28% |

| 27% |

| 27% |

| 26% |

| 27% |

| 28% |

| 29% |

| Diluted EPS |

| $1.3 |

| $2.4 |

| $3.4 |

| $4.7 |

| $6.2 |

| $7.0 |

| $12.8 |

| $17.2 |

| $13.8 |

Steady Earnings Amidst Weak Macro

LGIH reported a steady set of earnings for Q2 2023 with home closings down 9% YoY, but up 35% sequentially, driven by absorption declining by 18% to 6.1/month. It reported a 2% decline in average selling price sequentially as buyers continue to purchase smaller-sized homes less than 1,500 sq. feet amidst record mortgage rates and rising unaffordability to purchase homes.

It reported a 11% decline in revenues driven by a decline in home closings while average selling price remained flattish. There has been a sequential improvement through the quarter with April closings down 21% YoY, while May fell 9% and June rose 6% and absorption also improved from 5.4 in April to 6.3 in May and 6.5 in June.

The company reported a gross margin improvement of 170 bps sequentially and ahead of estimates driven by price increases across majority of communities, normalization in construction costs and new community openings at higher margins. SG&A as % of revenue declined 300 bps sequentially while up 190 bps YoY driven by a strong revenue growth sequentially outpacing the growth in fixed costs. It reported an EPS of $2.25 ahead of the estimates pegged at $1.76 driven by strong gross margins and lower SG&A.

Balance sheet position remained stable as the company ended with total liquidity of $385 mn including $43 mn of cash and a net debt/cap ratio of 36.8%

Following YTD closings through July down 7% YoY, the company increased its guidance for 2023 home closings by 2% at mid point to 6,850 driven by continued momentum and sales backlog. It reported August closings up 24% YoY implying a 4% decline in YTD closing through August and further demonstrating the management's ability to meet its guidance. It increased its gross margin guidance by 50 bps driven by pricing actions and higher margin in new community openings in Q4.

It reiterated its guidance for ASP for the year to be between $345k - $360k despite a jump in smaller sized homes (which formed 27% of Q2 2023 closings vs 19% last year) and ASP down sequentially as it expects higher priced ASPs in new communities will likely offset the decline. We believe the ASP is likely to fall below the lower end of its guidance as the increasing unaffordability and rising mortgage costs will continue to impair buyer's ability to purchase bigger homes. While the current backlog and demonstrated improvement in closings highlight the company is likely to be at or above the mid point of its home closings guidance, a decline in ASP could lead to a deterioration in gross margins to the lower end of its guidance. While management expects community count to grow 20-30% YoY in 2024 over and above the 16-26% YoY growth it expects for the current year (guidance being 2H weighted), there are increasing concerns on its ability to deliver strong growth amidst current housing turmoil and we await its ability to drive an increase in community growth for the coming quarters.

Challenges in Housing Market

Housing market continues to remain challenging as the Fed's vow to keep rates higher for a longer period continues to dampen demand which has been reeling under record mortgage rates. August new home sales declined 8.7% MoM to 675k below the consensus pegged at 700k while total existing home sales declined 0.7% sequentially driven by a 1.4% decline in single-family homes.

Inventory levels of existing homes available for sale remained at record lows, down over 53% from its peak, as a result of reluctance of sellers to sell their existing homes after locking in at record low rates amidst the pandemic. While the housing starts improved as a result of shortage in inventory, it continued to stumble with August housing starts declining 11.3% sequentially and 14.8% YoY as a result of continued challenge in housing affordability.

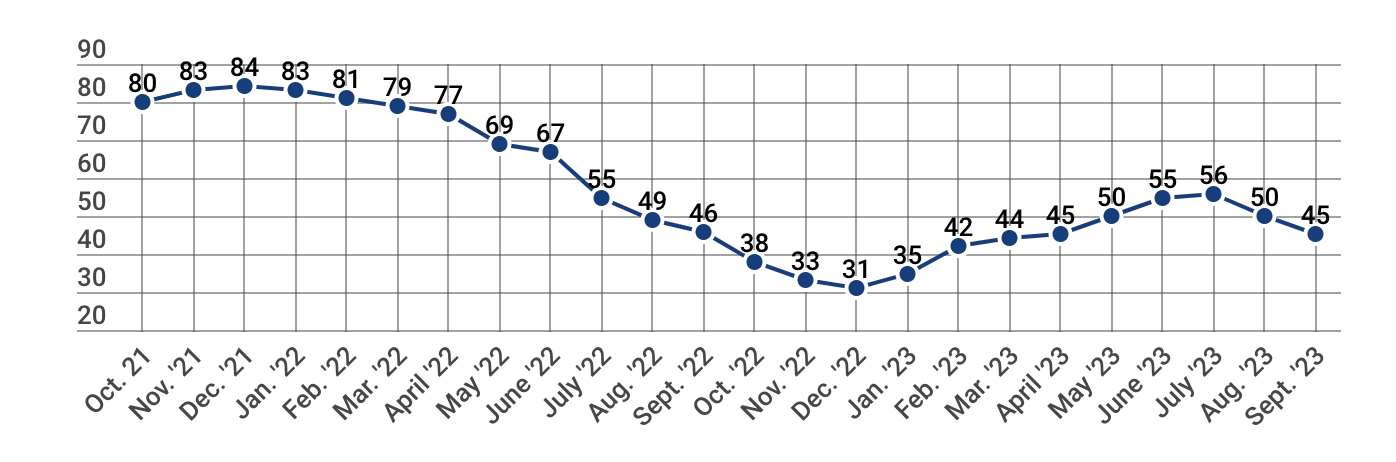

Builder's confidence continues to weaken which dropped 5 points in September following a 6 point decline in August as a result of mortgage rates persisting above 7% mark eroding purchasing power and continued challenges in housing affordability. Housing affordability index continued to be at record lows and took further jolt post the comments from US Federal Reserve which points to prolonged pain to the sector.

{kind=link}

Valuation

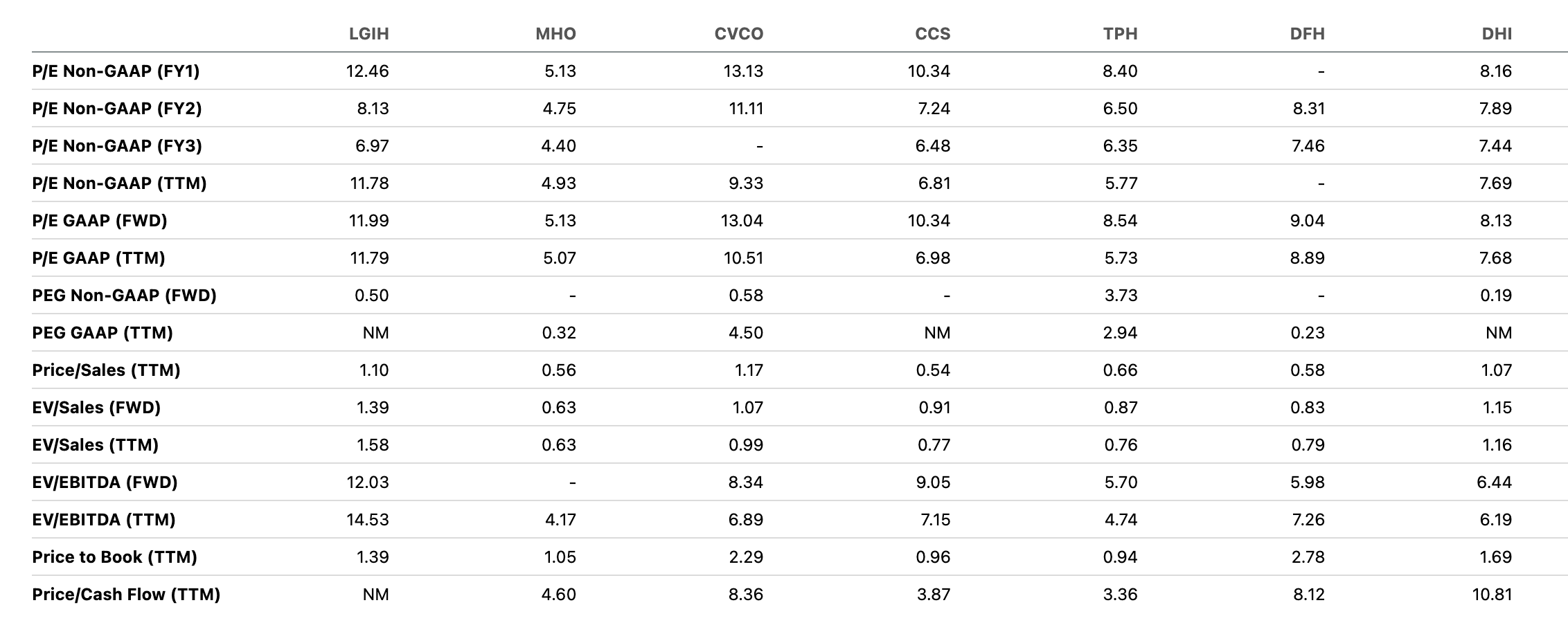

LGIH trades at 12.5x Fwd P/E, a premium to its peers as well as to its long term historical average (5Y Avg: 9.9x). Post the 25% decline in its market value during last two months, we believe there are still potential downside risks as increase in housing starts is likely to be offset by a decline in ASP as more buyers look for smaller sized homes due to persistent mortgage costs. We initiate at Neutral with target price of $95 at 8x 2024 EPS.

{kind=link}

Risks to Rating

1) Affordability challenges amidst persistent mortgage rates and a looming recession for a prolonged time could lead to a significant deterioration in housing activity and decline in order book

2) Rising construction costs as well as higher wages for construction workers could lead to a decline in operating margins

3) Upside risks include supply crunch in existing housing sales inventory could drive up order book and boost sales

Conclusion

LGIH has had a strong track record of growth historically and it reported a steady set of earnings amidst a challenging macro environment. Despite the company raising its guidance for home closings and reiterating the guidance for average selling price, we believe there are significant downside risks to their 2H weighted ASP guidance given the current environment. We believe despite the steep decline in its market value in recent times, there are significant challenges in the near term and we await further clarity on the ASP guidance going forward. Initiate at Neutral.

For further details see:

LGI Homes: Near-Term Risks Remain, Initiate At Hold