BYDDF - Li Auto: Hybrids Bridge The Gap Toward EVs Boosting Profit Margins

2023-12-26 09:00:00 ET

Summary

- LI has delivered another quarter of excellent profitable growth, with growing automotive profit margins despite the lower ASPs, implying its improved manufacturing/ operating scale.

- The automaker is also set to record an impressive 375.67K delivered units in FY2023 (+181.9% YoY), beating its previous two guidances, despite the ongoing price war in China.

- The LI management already targets 1.6M annualized deliveries by 2025, expanding at an impressive CAGR of +62.09% from current levels.

- We maintain our conviction that the management has been highly competent in bridging the gap between ICE and EV demand in China with its PHEV offerings.

- Combined with its growing cash hoard, LI remains a Buy for investors seeking high growth PHEV/ EV stocks, preferably at its previous support levels of $28s for an improved margin of safety.

We previously covered Li Auto ( LI ) in October 2023, discussing its excellent prospects, given the robust consumer demand for its offerings despite the uncertain domestic economy and ongoing price war.

We had attributed this success to the management's prudent choice of going with a hybrid vehicle approach, giving consumers the strategic option between ICE and pure EVs.

Combined with its growing profitability and balance sheet, we had rated the LI stock as a Buy then.

In this article, we shall discuss why LI remains a Buy, though at its previous support levels of $28s for an improved margin of safety, since it appears that Mr. Market may prefer to wait for the automaker to grow into its premium valuations, while potentially rerating the stock's valuations nearer to the sector median.

However, we maintain our long-term conviction that the automaker is likely to be one of the long-term winners in the electrification trend, further aided by its profitable growth and the consensus raised top and bottom line estimates.

The LI Investment Thesis Remains Highly Profitable

For now, LI has reported an excellent FQ3'23 earnings call , with revenues of $4.74B ( +20.3% QoQ / +261.7% YoY ) and adj EPS of $0.45 (+25% QoQ/ +350% YoY).

Most importantly, it appears that the Chinese automaker has been able to improve its manufacturing/ operating scale thus far, attributed to its declining ASPs and growing automotive margins.

For example, LI reported automotive revenues of $4.61B and 105,108 units delivered in the latest quarter, implying a declining ASP of $43.85K (-1.6% QoQ/ -8.4% YoY).

At the same time, it has been able to report more than healthy automotive margins of 21.2% (+0.2 points QoQ/ +9.2 YoY), with the automaker able to pass off savings to its consumers, at a time when Tesla ( TSLA ) had to engage on an aggressive price war while drastically impacting its own margins.

Perhaps this explains why LI has been able to report excellent FQ3'23 deliveries of 105.1K units (+21.4% QoQ/ +296.2% YoY).

The management's FQ4'23 delivery guidance of 126.5K units at the midpoint is not overly ambitious as well, with 40,422 units delivered in October 2023 (+12% MoM/ +302% YoY) and 41,030 units in November 2023 (+1.5% MoM/ +172.9% YoY).

This is on top of the 50K delivery guidance for December 2023 (+21.8% MoM/ +135.5% YoY), implying that LI may very well beat its previous FQ4'23 guidance with up to 131,452 units delivered (+25% QoQ/ +183.7% YoY).

It appears that the management may also break its original FY2023 delivery target of 360K units (+170.1% YoY), before the subsequent downgrade to 300K units (+125.1% YoY), based on the cumulative YTD sum of 325,677 units (+190.7% YoY) and 50K units for December 2023.

We believe that most of LI's demand tailwind is also attributed to its attractive estimated FQ4'23 ASPs of $42.13K per unit (-3.9% QoQ/ -21.8% YoY), based on the management's revenue guidance of $5.33B and delivery of 126.5K at the midpoint.

The attractive ASP further underscores why consumer demand remains healthy, with the management already targeting 1.6M annualized deliveries by 2025, expanding at an impressive CAGR of +62.09% from current levels.

Moving forward, LI is also not resting on its laurels, with the launch of its super flagship Li Mega BEV MPV model in November 2023. Despite the higher ASP of approximately $70K, it is apparent that demand for the premium BEV SUV offering remains healthy, with pre-orders already exceeding 10K units within two hours of launch.

Perhaps part of the appeal is attributed to the use of CATL's Kirin 5C battery , which offers an impressive 500 km range within a 12 minute charge, likely to alleviate range anxiety for countries as big as China. Interested readers may note that we have previously covered the Kirin battery technology in a previous Ford ( F ) article here .

As a result of these promising developments, we maintain our conviction that the LI management has been highly competent in bridging the gap between ICE and EV demand in China with its PHEV offerings.

This may allow the automaker to gradually capture market share as the automotive market slowly completes its electrification transition, while building a robust brand recognition for its family friendly offerings ahead.

Most importantly, LI remains highly liquid for its various long-term investments, based on its FQ3'23 cash/ short-term investments of $11.97B (+20.3% QoQ/ +63.9% YoY), further aided by its moderating debts of $218.34M (inline QoQ/ -82.6% YoY).

There is nothing to dislike indeed.

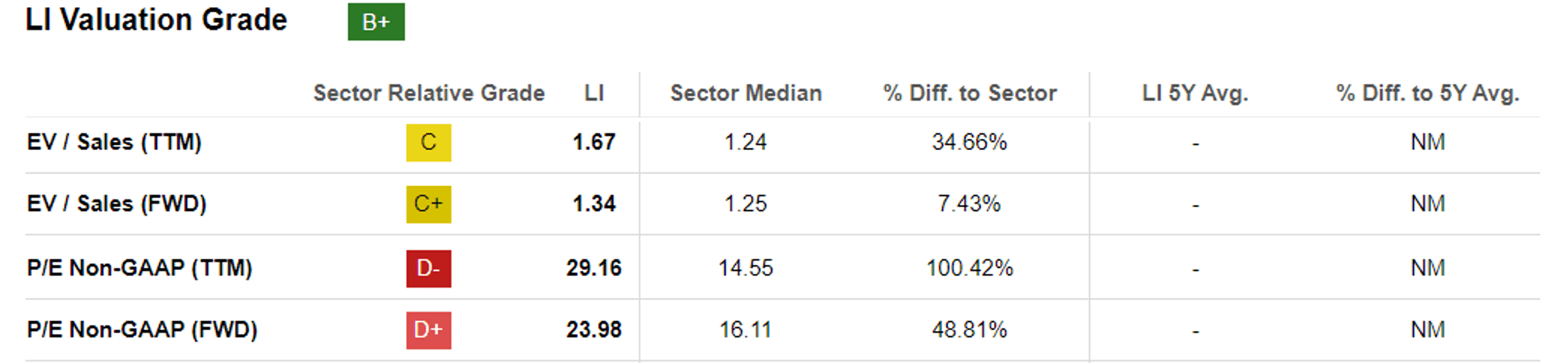

LI Valuations

{kind=link}

Tikr Terminal

For now, LI's FWD EV/ Revenues of 1.34x and FWD P/E of 23.98x have been drastically moderated compared to its 1Y mean of 1.42x/ 48.85x and finally nears the sector median of 1.25x/ 16.11, respectively.

With NIO ( NIO ) and XPeng ( XPEV ) yet to achieve profitability, the other peer that we may use to compare its valuations is BYD Company Limited ( BYDDF ), the "near" king of EVs , at 16.19x.

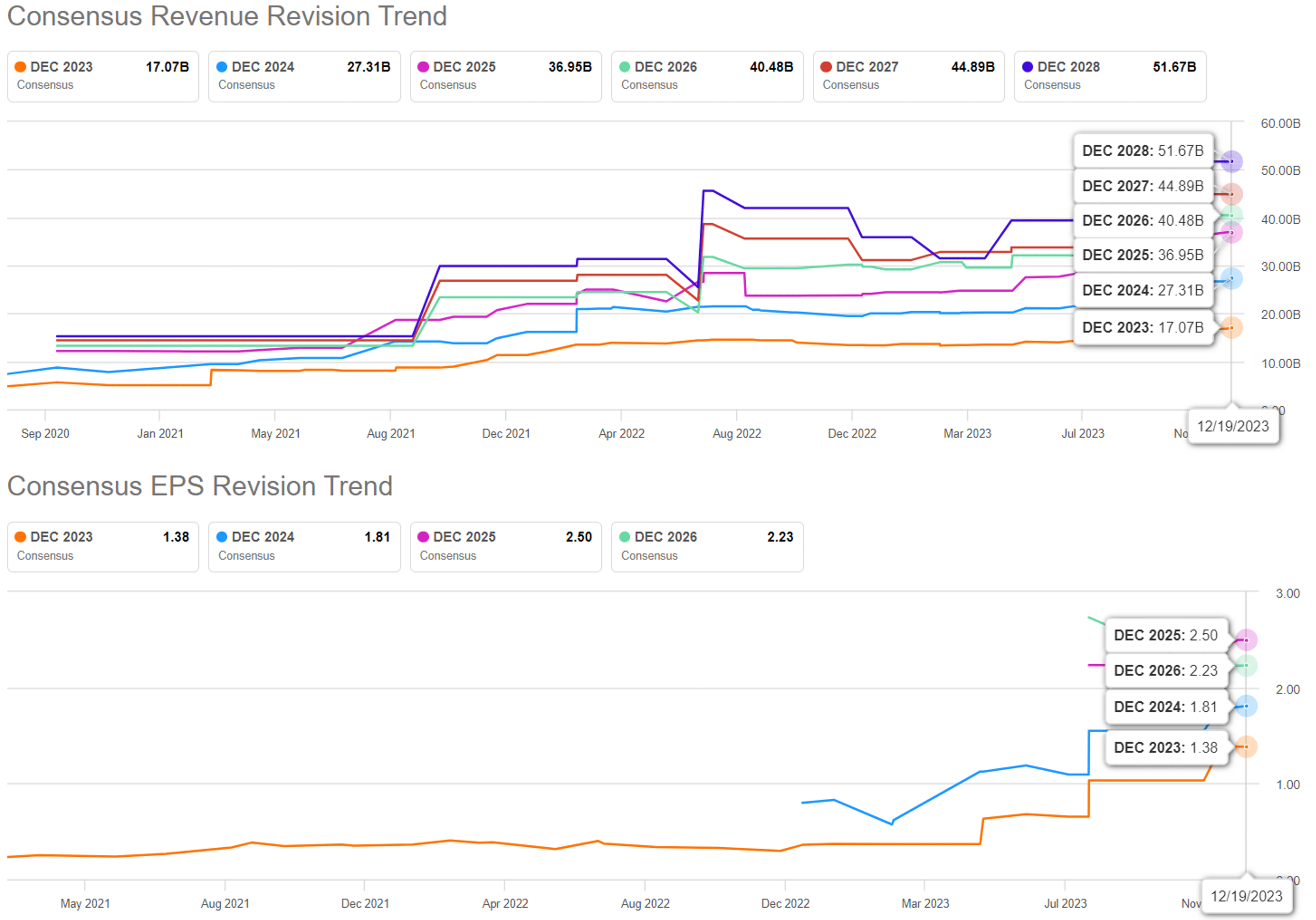

The Consensus Forward Estimates

{kind=link}

Seeking Alpha

It is apparent that LI's and BYDDF's strategy of launching both BEVs and PHEVs have been paying off handsomely, as discussed above, with the former expected to generate a raised top and bottom line growth at a CAGR of +80.2% and +167.9% through FY2025.

This is compared to the previous estimates of +55.2%/ +109.3%, while building upon its historical top-line CAGR of +442% between FY2019 and FY2022.

LI's profitable growth trend also well exceeds BYD at a CAGR of +28.8% and +47% through FY2025, demonstrating why the former has been awarded with the premium valuations.

So, Is LI Stock A Buy , Sell, or Hold?

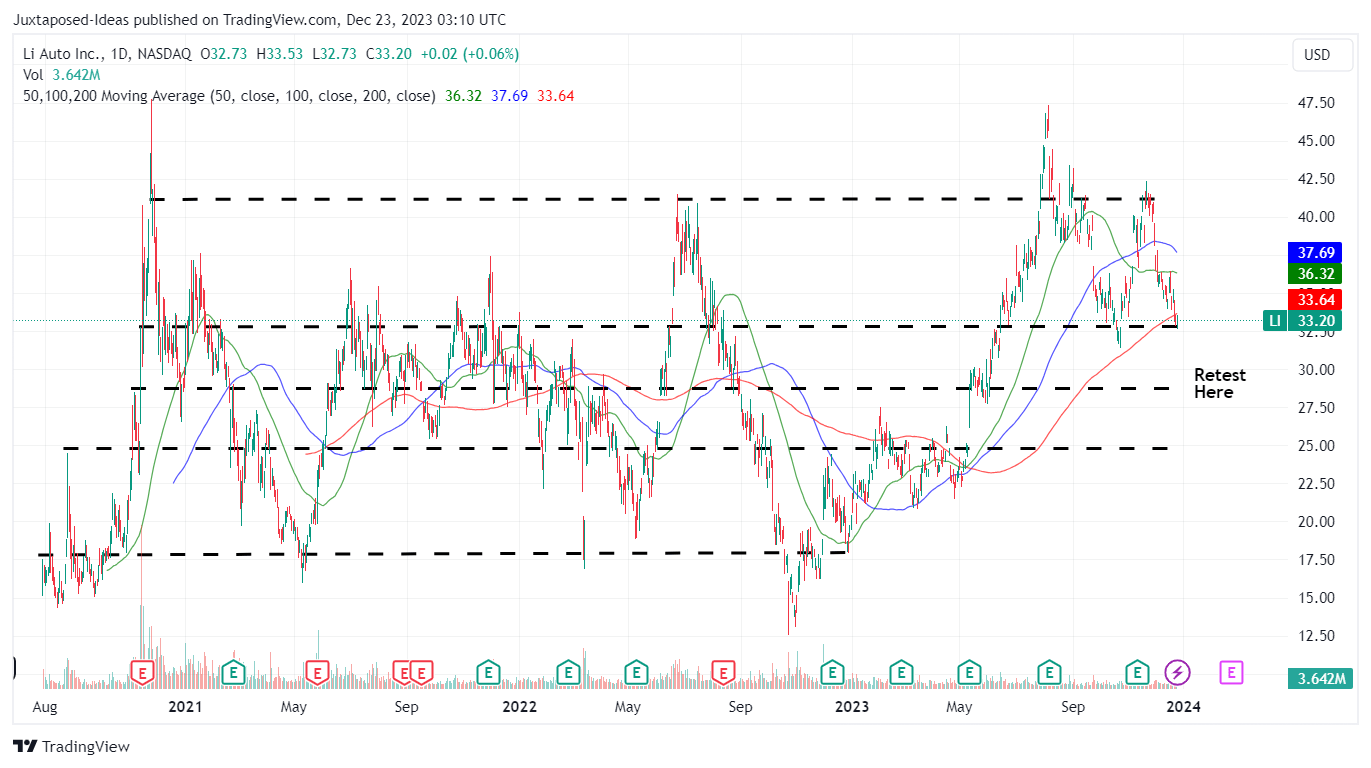

LI 3Y Stock Price

{kind=link}

Trading View

For now, the LI stock has continued its sideways trading pattern since late 2020, with an apparent resistance level of $40s and bottom of $18s.

While the automaker's recent profitable trend has boosted the stock with a notable floor at $33s, this sideways trend implies that Mr. Market may prefer to wait for the automaker to grow into its premium valuations, while potentially rerating LI's valuations nearer to the sector median.

On the one hand, based on LI's YTD adj EPS of $1.01 (+605% YoY), another FQ4'23 outperformance as with FQ3'23 at $0.45 (inline QoQ/ +246.1% YoY ), and the sector median P/E of 16.11x, it appears that the stock is trading above its fair value of $23.50.

On the other hand, based on the consensus FY2025 adj EPS estimates of $2.50, there seems to be a more than decent upside potential of +21% to our long-term price target of $40.20.

Therefore, while we may continue rating the LI stock as a Buy, there is no specific entry point since it depends on individual investor's dollar cost average and risk appetite.

Bottom fishing investors may consider observing the stock's movement for a little longer and wait for a moderate retracement to its previous support levels of $28s for an improved margin of safety.

For further details see:

Li Auto: Hybrids Bridge The Gap Toward EVs, Boosting Profit Margins