LBTYB - Liberty Global: Wait Until Price Escalations Are Implemented

2023-09-20 12:24:42 ET

Summary

- Liberty Global is implementing price increases, resulting in the loss of customers but slight revenue and profit growth.

- Risks for Ziggo include competition from broadband providers offering full fiber optic broadband.

- Liberty Global's debt maturity terms are favorable, with the potential for lower interest rates upon refinancing.

Introduction

It has been 9 months since my prior article on Liberty Global ( LBTYA ). At that time, the stock was given a hold rating at $18.62 due to its lack of strong growth catalysts. Quarterly results at the time were mixed. The mobile segment did particularly well with net additions in all business segments. There were inflows of new customers for the broadband segment, but VodafoneZiggo saw its customer base decline.

Liberty Global can grow by acquiring new customers, raising prices or acquiring competitors. It is an economic game with stiff competition from multiple players in Europe and the United Kingdom. Liberty Global offers combination discounts for broadband and postpaid mobile to retain customers. A win-win for both consumers and the company.

I'm still not optimistic about the company's prospects. In the Netherlands, there is fierce competition with serious deals to attract new customers. As a result, Ziggo lost 31,000 customers this quarter. Also, Ziggo offers broadband via technology that is no longer supported in new-build homes. Because of this, I see some challenges in the long term. In the short term, Liberty Global is implementing price increases. This may increase revenue at the expense of losing customers.

Second Quarter Results Of 2023

Let's first look at the second quarter results of 2023 . Liberty Global saw many customers leave after it implemented price increases for VMO2 customers. Still, its top and bottom lines rose. The company will increase prices for the other business segments in the second half of this year.

VMO2

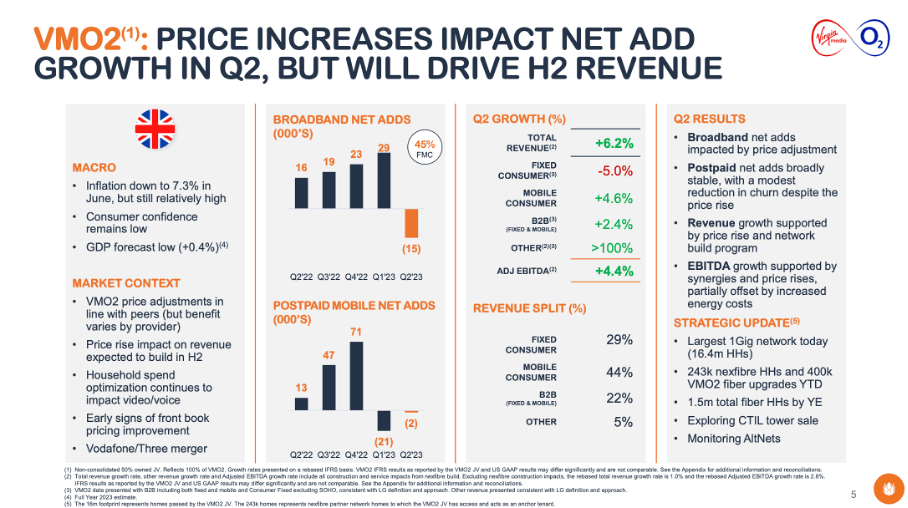

VMO2: Price increases impact net add growth (Liberty Global 2Q23 Results)

{kind=link}

The UK business segment VMO2 has performed well despite the high inflation of 7.3% and low 2023 GDP forecast of 0.4%. However, VMO2 lost 15,000 broadband customers and 2,000 mobile postpaid customers. This was due to price increases in both segments. Overall, quarterly revenue increased by 6.2% and adjusted EBITDA increased by 4.4%. Price increases have compensated for the decline in the customer base. And if more competitors follow suit, customers may return to VMO2. For now, I have mixed feelings about it. The loss of customers is large compared to the increase in revenue.

Sunrise and Telenet

The Swiss economy is not affected by the high inflation as in other euro countries. However, because of reduced promotional activities, the company lost 3,000 customers. The mobile segment performed strongly with 23,000 new customers. Quarterly revenue was only 1% lower and adjusted EBITDA remained about the same.

In Belgium (Telenet) the picture looked better with a revenue increase of 1% and an adjusted EBITDA increase of 5%. Price increases were introduced in June. This affected both the broadband and postpaid mobile segments. Approximately 5,000 customers left in both segments. The price increases and net additions will mainly be visible in the figures in the second half of this year.

VodafoneZiggo

VodafoneZiggo is active in the Netherlands. I have both broadband and mobile from Ziggo and Vodafone at home. The package is slightly cheaper than competitors KPN ( OTCPK:KKPNF ) and Odido, which is previously called T-Mobile ( TMUS ). T-Mobile and KPN make full use of the fiber optic network. However, VodafoneZiggo combines the fiber optic network and uses coax.

Coax is not the standard for new-build homes. If a household wants this, he or she will have to have it installed separately with the associated costs. I think many households choose another provider and I see this as a major risk in the long term.

Yet coax achieves the same download speeds as fiber optic and Ziggo even claims to be able to achieve speeds of 10 Gbit/s. The difference with fiber optic is that the upload and download speeds are different with coax. But this is not a problem for streaming films or series.

What Dutch people also find important is the quality and reliability of services. In the Netherlands, we have the Consumers' Association . Independent research is conducted here, and the findings are published online. Ziggo scores a total score of 7.4, while competitor KPN scores slightly higher with 7.8. The lower rating is mainly due to internet quality, customers report more internet disruptions at Ziggo than at KPN.

The number of postpaid mobile internet additions in the second quarter amounted to 38,000. Broadband performed worse and Ziggo lost 31,000 customers. Competitors are now offering crazy deals to customers. KPN is currently offering a huge welcome deal. Customers who now take out an internet and TV subscription will receive a Philips UHD Smart TV as a gift. The competition is fierce.

Customers can switch to another provider who also offers a discount when combining mobile plans, making this a major problem. Still, VodafoneZiggo's quarterly revenue remained virtually flat. Liberty Global expects revenue to increase over the next six months following the price hikes.

It seems that these companies are very competitive. If the group raises prices, customers will leave. As a result, the top and bottom rise only slightly. The question remains how customers will react to the price increases over the next six months.

In the long run, I also see challenges for Ziggo due to the lack of a coaxial connection in new-build homes and the reliability of the internet.

Favorable Debt Maturities

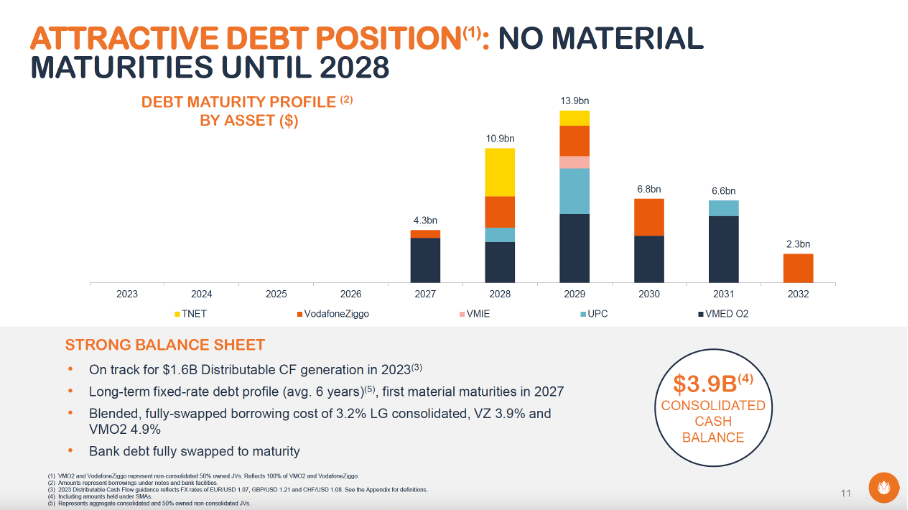

No material maturities until 2028 (Liberty Global 2Q23 Results)

{kind=link}

Like many other companies in the sector, debt levels are high. Liberty Global's debt is $15.1 billion. But if we subtract cash and cash equivalents, we arrive at net debt of $11.4 billion. The debt load is particularly high compared to the twelve-month free cash flow of $1.1 billion. We then arrive at a net debt/FCF ratio of 10.4.

Liberty Global benefits from a low fixed interest rate, with repayments starting in 2027. However, interest rates have risen sharply, but are expected to fall in 2024/2025. And that's great news for Liberty Global, because they can refinance their debt at a favorable interest rate.

Yet I see some challenges for the coming period. The fierce competition and low interest coverage make it difficult for the company. Interest expense for the twelve months is $737 million, while TTM's free cash flow is only $1,066 million. But for now, there are no worries as Liberty Global expects to generate distributable cash flow of $1.6 billion by 2023.

Stock Valuation

"Price is what you pay and value is what you get," are the words of Warren Buffett. Looking at the stock valuation , it's easy to view Liberty Global as a value stock. The price-to-book value of 0.4 is almost at a historic low. This ratio is also well below the sector average of 1.9. Another ratio to consider is the price/sales ratio, which is 11% below the sector average.

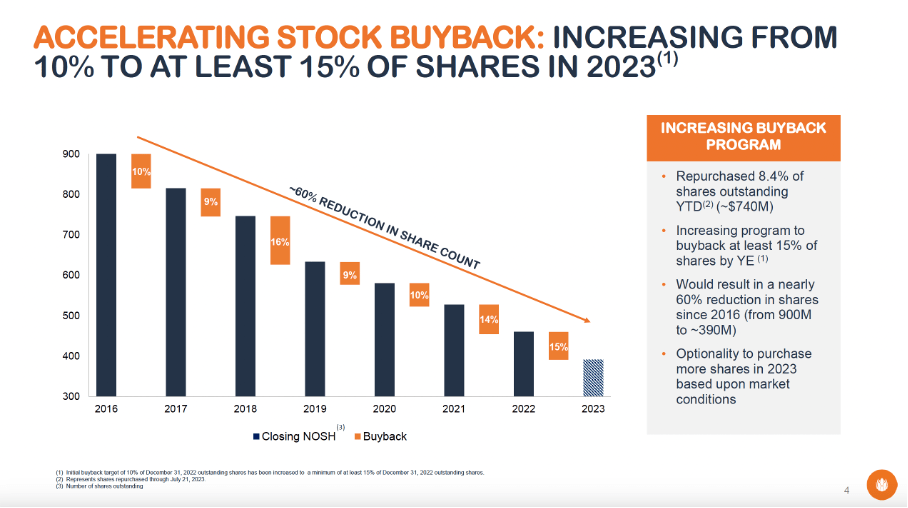

However, value has yet to be unlocked. Industry peers pay an excellent dividend, while Liberty Global does not. It does buy back shares. This has resulted in a massive reduction in the number of shares outstanding, but the share price has lagged. The sharp decline in the share price suggests that shareholders are dissatisfied.

Shares outstanding over the years (Liberty Global 2Q23 Results)

{kind=link}

Repurchasing shares reduces the supply. This scarcity allows the share price to rise. But that didn't happen. In my opinion, management should pay a dividend to supplement the share buyback program. This will unlock value and attract income investors to invest in Liberty Global.

Key Takeaway

While Liberty Global is implementing price increases, it is losing customers. But after it implemented the price increases for VMO2, revenues and profits rose slightly. Customers of Sunrise, Telenet and VodafoneZiggo will pay more for their subscriptions in the second half of the year. The question remains how customers will respond to this, and whether this will lead to bottom line growth.

In the longer term, I see risks at Ziggo. Ziggo uses a combination of fiber optic and coax. New-build homes do not have a coaxial connection integrated as standard. Consumers will have to install this separately. I think they would prefer to opt for full fiber optic from another broadband provider.

I'm satisfied with the maturity terms of the debt. I expect that interest rates will be lower when the debt matures. This will make the refinancing rate beneficial for the company.

I think that an established company like Liberty Global should be paying dividends instead of buying back shares. The falling share price makes it clear that investors are not satisfied to this. When Liberty Global pays dividends, income investors will consider buying the shares. The share is listed cheaply, but for the time being I see no catalyst. I prefer to wait for the next quarterly figures to gain insight in the loss of customers and price increases. For now, the stock is on hold.

For further details see:

Liberty Global: Wait Until Price Escalations Are Implemented