LSXMB - Liberty SiriusXM: The Discount Being Closed

2023-09-27 02:13:47 ET

Summary

- Liberty SiriusXM plans to merge with Sirius XM, eliminating the tracker discount in LSXM shares.

- LSXM shares could be worth up to $40 when converter to the NewSiri. But leverage will increase.

- Transaction still needs to be approved.

Intro

The Liberty SiriusXM Group ( LSXMK ; LSXMA ; LSXMB ) is a holding carrying Liberty Media’s interests in Sirius XM ( SIRI ) and has been trading at a significant discount to the value of the assets for a number of years, though as of late management has stepped up efforts to close this discount. Today the company reported that it plans to merge with Sirius, thus giving LSXM shareholders a direct access to Sirius XM cash flows.

As we have mentioned in our previous article, the streamlined LSXM and SIRI securities essentially had the same value and the same risk exposures and therefore were supposed to trade in line. However streamlined LSXM continued trading at a discount to net book value. The new transaction will remove this discount for good.

The Current Valuation

| Liberty Sirius XM |

| Shares |

| Price |

| Value million |

| SIRI |

| 3,205.8 |

| 3.6 |

| 11,541 |

| Cash |

| 225 |

| Debt |

| 1.375% Cash Convertible due 2023 |

| 993 |

| 2.125% SiriusXM Exchangeables due 2048 |

| 387 |

| 2.75% SiriusXM Exchangeables due 2049 |

| 586 |

| SiriusXM Margin Loan |

| 875 |

| Net Debt of LSXM |

| -2,616 |

| A |

| NBV |

| 8,925 |

| LSXM market value |

| 326.58 |

| 28 |

| 9144.24 |

| B |

| Upside |

| -2% |

our estimates

According to our estimates, LSXM shares should be worth about $28 per share given that the SIRI price goes down to $3.6.

It is quite possible that SIRI will experience some price pressure in the upcoming weeks as arbitrageurs start going long LSXM and shorting SIRI in order to lock in the profit. We believe some other funds also took long positions in SIRI hoping to be bought out above the market and they will also likely sell now. So negative price pressure in SIRI will translate into a lower optimal target price for LSXM. We should not rush to close our positions just based on the current market prices, we should instead value SIRI based on its fundamentals as soon we will be the direct shareholders of it anyway. If anybody is concerned, SIRI is not going anywhere anytime soon and it is not a value trap as I have outlined in my article on it. So we have the time to wait for our price.

Underlying value of SIRI

A little recap of our Jun. 17, 2023 article on SIRI:

Sirius XM has continued performing well even after online music streaming services entered the in-vehicle market. Currently, Sirius is a profitable and cash-generative business capable of paying out a generous dividend. We want to find out if they can continue maintaining their strong position going forward.

Over the past 5 years:

- Self-pay subscribers grew from 26m to 32m (23%)

- ARPU has increased from $13.3 to $15.6 (17%)

- Satellite radio revenues increased from $5.4 bn to $6.9 bn (28%)

- Churn has gone down from 1.8% to 1.5%

We believe this solid performance in an adverse market can be attributed to distribution gains and differentiated content offerings. An increasing number of new vehicles are equipped with satellite radios and this gradually drags up rates of satellite radio penetration among remarked used vehicles. Sirius XM has been signing up new manufacturers and also expanded partnerships with used car dealerships. Going forward, the used car segment has a significant growth opportunity, and new car penetration will also increase further. Increasing penetration would not be possible without a strong content package as automakers would not be installing satellite radios if their customers did not see any value from them.

| Sirius XM |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| New car sales |

| 17 |

| 14.6 |

| 15 |

| 13.9 |

| 16.5 |

| Penetration by volume |

| 79% |

| 80% |

| 82% |

| 83% |

| 84% |

| Conversion |

| 34% |

| 34% |

| 34% |

| 34% |

| 31% |

| New car gains |

| estimate |

| 4.6 |

| 4.0 |

| 4.2 |

| 3.9 |

| 4.3 |

| Used Car Sales |

| 39 |

| 39 |

| 43 |

| 36 |

| 38 |

| Vehicle Penetration |

| 44% |

| 51% |

| 51% |

| Channel Penetration |

| 62% |

| 62% |

| 62% |

| Conversion |

| 25% |

| 25% |

| 25% |

| 25% |

| 25% |

| Used car gains |

| estimate |

| 2.7 |

| 2.8 |

| 3.0 |

| Share of gross adds |

| 35.0% |

| 36.8% |

| 42.0% |

| 41.1% |

| Gross additions |

| 7.2 |

| 6.8 |

| 7.3 |

| Churn |

| 5.9 |

| 6.6 |

| 6 |

| Monthly |

| 1.7% |

| Annualised churn rate |

| 20.4% |

| 20% |

| 20% |

| Net Addition |

| 1.3 |

| Self-pay subs |

| 29 |

| 30 |

| 33 |

| 34 |

financial reports and our estimates

Overall, subscriber numbers of Sirius XM seem to be driven by multiyear new and used car penetration growth trends, relatively low rates of churn and decreasing conversion. Penetration is increasing predictably, churn has been low for years and conversion has been trending down gradually. We believe it is very unlikely that Sirius XM would start losing customers rapidly. Having said, decelerating conversion is the best indicator of increasing competition for Sirius XM. The company has no control over the technological advances of the industry, therefore it has to focus on content to manage competitive threats.

Q2 2023 Update

Profits were resilient: Adjusted EBITDA was $702 million in the second quarter of 2023, up 3% compared to the second quarter of 2022.

Free cash flow guidance was increased:

Our solid second quarter performance and greater visibility into full-year cash taxes and working capital leads us to increase our 2023 free cash flow outlook to $1.15 billion. We also expect to continue to see improving financial and operating performance in the second half of the year”. Adjusted EBITDA is guided at $2.75 billion.

Sirius XM total subscribers were flat at 34 million. In q2 self-pay subscribers decreased by 132,000 and paid promotional subscribers increased by 155,000. Promo subscriber growth is related to new car sales normalising. Monthly churn stayed low at 1.5%. ARPU was essentially flat also.

Pandora continued losing active listeners, though growth in podcasting has helped to maintain revenues flat. However the cost of services, including content has increased, thus pushing the gross profit in the division down. Sirius XM is still the dominant profit maker of the business though.

Value overview

Given our quality assessment we believe that SIRI is very unlikely to turn into a declining traditional media company and de-rate to a significantly lower valuation multiple than it trades at today.

{kind=link}

tikr.com

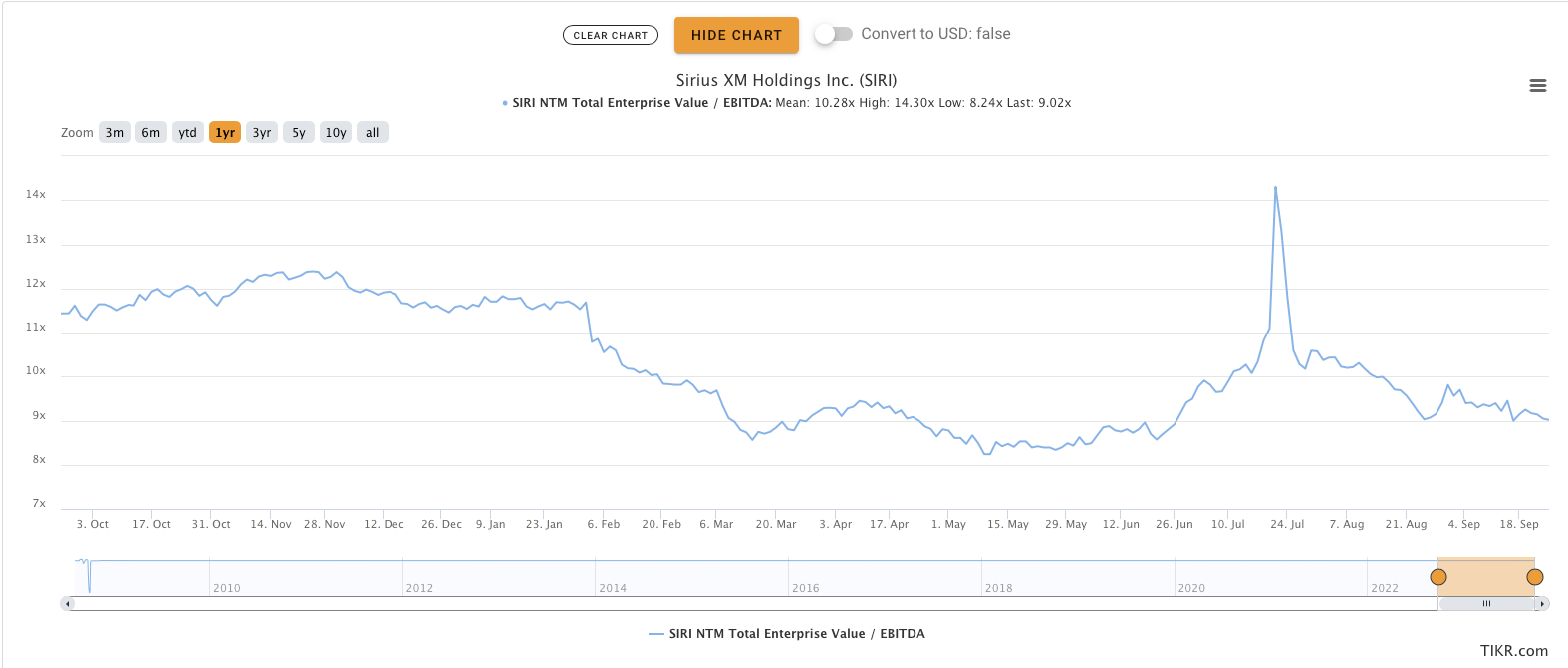

We believe that the current valuation multiple of c10x EV/EBITDA is more less conservative given the quality of subscription based revenue model, low rates of churn, increasing penetration and high cash generation.

The current forward EV/EBITDA of the business is c9x and the Company’s equity is trading at a 7.2% free cash flow yield during a peak capex cycle as satellites are being replaced. Adjusting for satellite capex, SIRI would be trading at a c9x Free Cash Flow Yield. We believe that such a valuation yield is excessive for a stable, well entrenched and somewhat growing business. The mature Consumer Staple businesses, for example, P&G or Heineken, trade at FCF yields of 4-6%. Applying a really conservative 7% yield on capex adjusted FCF of SIRI of c$1.35 billion, we would obtain an equity value of c$5 per share. The current share price of SIRI is closer to $4.

If the market price of SIRI today would be $5 per share, the fair market value of LSXM shares would be about $40 per share, 60% higher than today's price.

Part of the reason for such a big differential is the extra layer of leveraged at the LSXM holding company level. To figure out the return that LSXM holders will obtain we need to look into the details of the transaction to see how the LSXM debt will be treated.

The upcoming transaction

Liberty (“SplitCo”), which would own all the assets and liabilities attributed to LSXM.

LSXM holding of 3,206 SIRI shares will be exchanged at a conversion rate 0f 1.05x to 3366.1 shares of NewSiri.

Each Stock of SIRI will be exchanged at a conversion of 1.0x to shares of NewSiri.

NewSiri will have c4,000 K shares. Past LSXM holders will own 84% of the combined entity.

Minority shareholders of SiriusXM would receive a pro-rata cash payment calculated based on the amount of the outstanding net debt of LSXM assumed by New SiriusXM in the proposed transaction.

Outstanding net debt of LSXM was $2.6 billion and current SIRI holders will then be paid 16% of this amount, equating to $400 million.

By way of example,… LSXM common stock would receive 10.3 shares of New SiriusXM common stock for each share of LSXM common stock … , and, based on the projected outstanding principal amount of LSXM net debt at year-end, the minority shareholders of SiriusXM would receive one share of New SiriusXM common stock plus $0.55 in cash for each share of SiriusXM common stock held at closing.

What this means is that the equity value of SiriusXM will incur extra leverage, thus boosting the returns for the old LSXM holders. That is if the market decides that such a leverage level is sustainable and the risk profile of the business did not increase meaningfully.

The new capital structure

We are unsure what funds will be used to pay the extra dividend for SIRI minorities, but most likely it will come from SIRI cash reserves. We therefore expect that the net debt of NewSiri will increase by $3 billion.

The current Net debt of SIRI is about $9.4 billion, the new level will be c12.4x. Assuming that the business can deliver on its EBITDA guidance, NewSiri is expected to have Net Debt to EBITDA of 4.5X. This level of leverage is not small, but should be manageable for a stable, subscription based and capital light business.

The extra leverage will also have an interest cost and reduce the Free Cash Flow that the business can generate. Assuming a 4% average interest cost on the extra debt, we will see NewSiri interest cost to increase by $120 million.

Previously we assumed the capex adjusted FCF to be about $1.35 billion, thus NewSiri is likely to generate about $1.23 billion after interest payments. Re-applying the 7% FCF yield assumption, we would obtain an equity value of $17.6 billion, or $4.4 per NewSiri share.

As mentioned, the old LSXM holders will be entitled to 10.3 shares of NewSiri. By extension, LSXM should then be worth about 10.3X4.4 = $45 per share.

Assuming a more conservative 9% FCF yield in valuation to reflect increased leverage, we would obtain a value of $3.42 per share of New Siri and $35.2 value per LSXM share, - a 46% premium to today's price of $24.

Conclusions

The proposed transactions, if approved, will likely finally mitigate the longstanding discount between Sirius XM and its tracking stocks. On top of this, the effect of Net Book Value discount mitigation will be leveraged for the holders of LSXM, assuming that the risk profile of the business will not be affected in a significant way. Overall, we believe it is worthwhile to keep on holding LSXM and wait for the transaction to go through.

For further details see:

Liberty SiriusXM: The Discount Being Closed