ANCTF - Lifco: An Undervalued Swedish Gem

2023-10-17 10:00:00 ET

Summary

- Lifco is an acquirer and long-term owner of European dental and industrial companies.

- The company has a decentralized profit-focused culture with a long track record of outperformance.

- With the current valuation, Lifco looks to be undervalued.

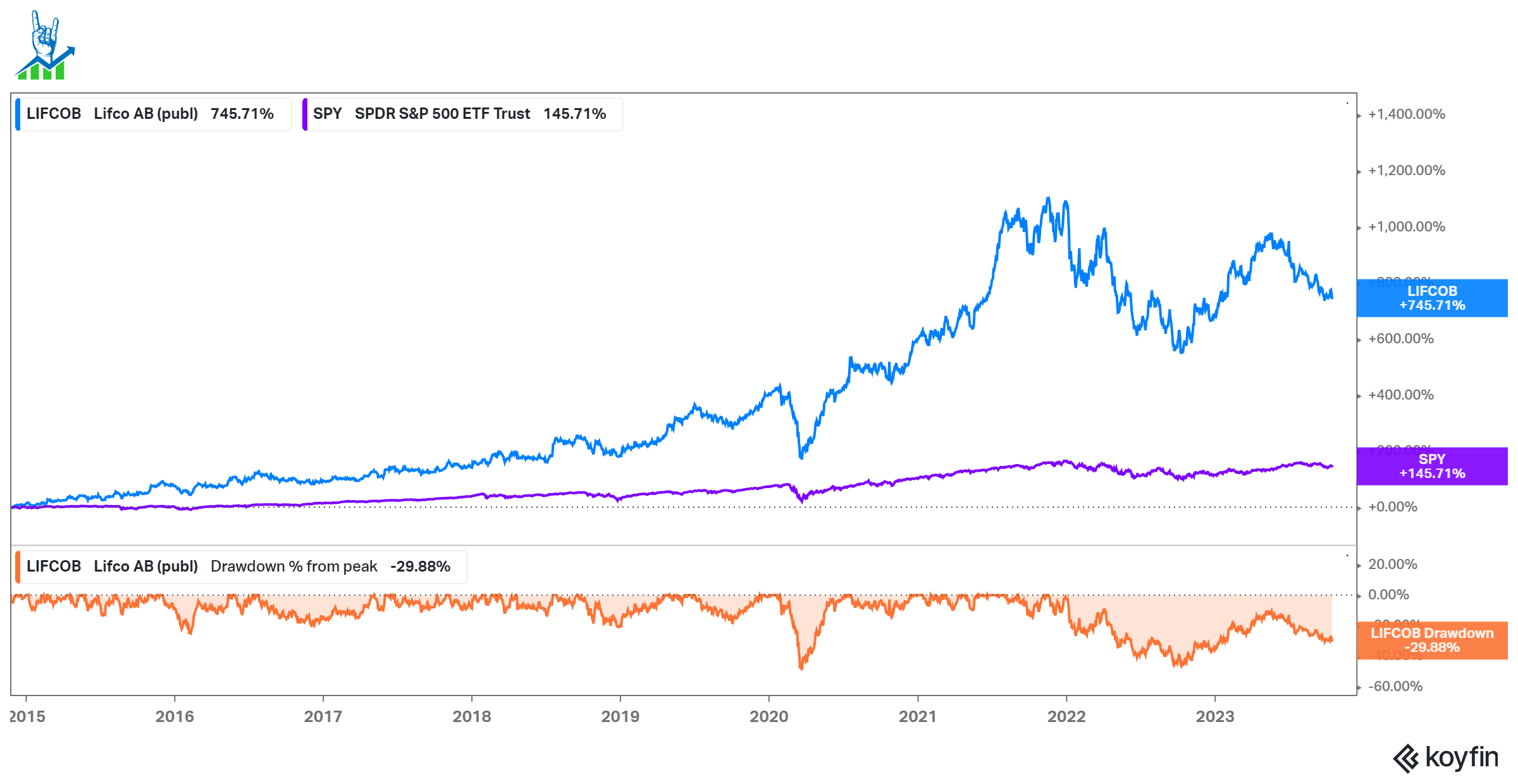

Lifco (LFABF) is a Swedish industrial serial acquirer that has widely outperformed the S&P 500 since it IPOed a second time in 2014. The company was taken public in 2000 by Carl Bennet and restructured: Health and self-care operations were divested and the focus was set on dental product distribution. In 2006, after the merger with Sorb Industri AB, the company also had an industrial business. After a successful turnaround and 16.8% EBITA CAGR between 2006 and 2014, Carl Bennet IPOed Lifco again and retained a 50.1% ownership stake. Bennet still owns 50.2% of the capital and 68.9% of the votes and is a committed long-term owner.

Lifco outperformance since IPO (Koyfin)

{kind=link}

What does Lifco do?

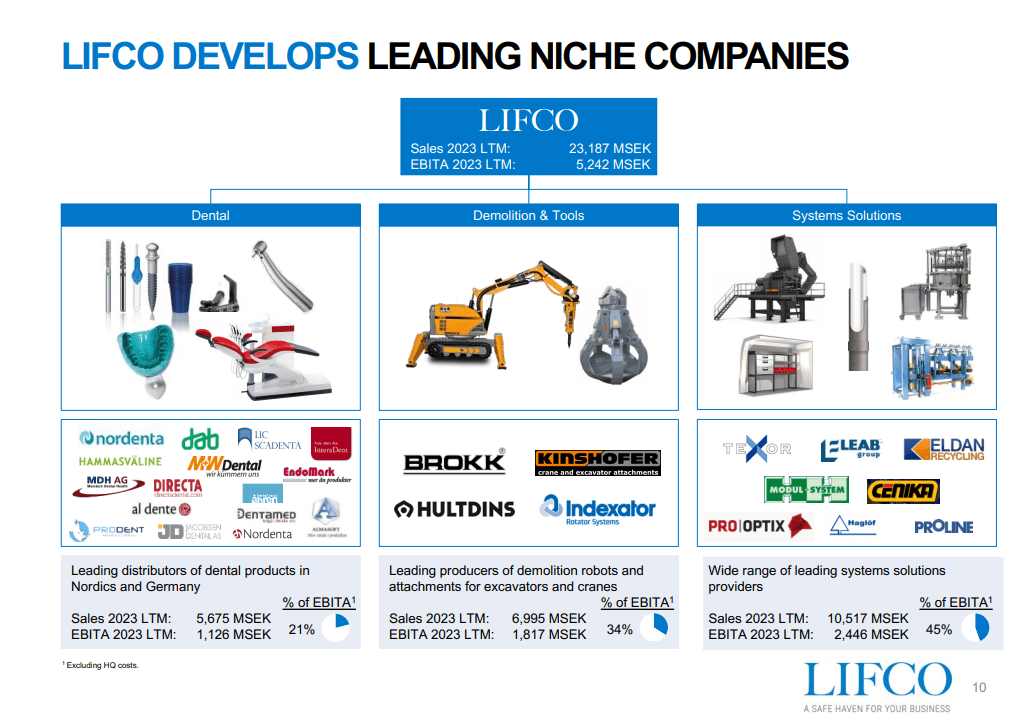

Lifco is a serial acquirer predominantly in the Nordics (22% of sales) and Europe (44% of sales). The company operates in three main segments: Dental, Demolition & Tools and System Solutions. Dental represents the smallest part of the company and has the smallest EBITA margin, at just 21%, but the dental business is the least cyclical part of Lifco and adds stability.

Lifco portfolio (Lifco Investor Presentation)

{kind=link}

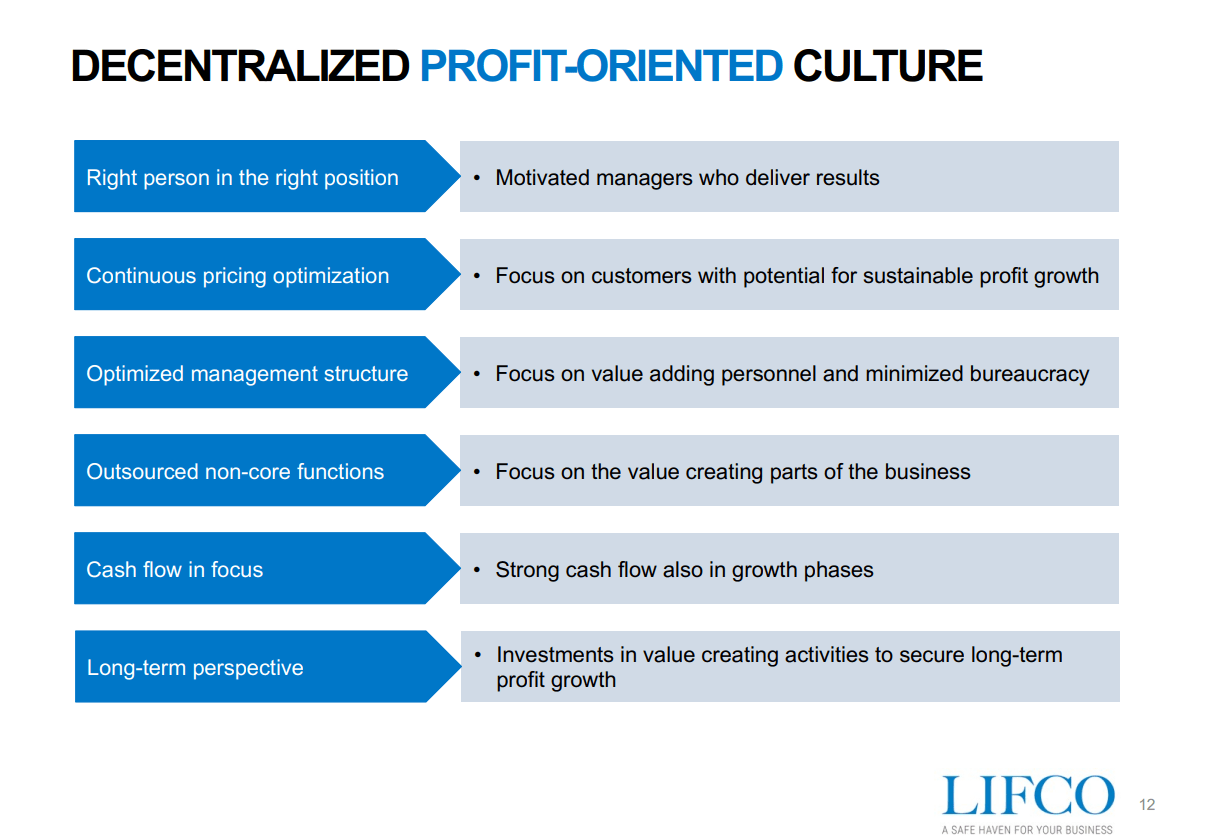

Lifco focuses on increasing profits (measured in EBITA) every year. It leverages its strong cash flow generation and strong balance sheet to acquire companies. The companies are then integrated into the decentralized culture of Lifco. Decisions should be taken locally, and Lifco doesn't force anything on the business. Generally, companies are optimized and left to operate independently by outsourcing non-core parts of the business. The focus should be on generating value for customers and ultimately cash flow for Lifco to reinvest in more acquisitions. Lifco rarely sells businesses; one of the few exceptions was the divestitures of companies with a focus on the Russian market in 2022 due to the Ukraine conflict. This long-term ownership perspective is very similar to the approach of Constellation Software (CSU: CA), another company I own. As a predominantly industrial company, Lifco has a low maintenance capex need of just 1-2% of sales due to these measures and tight working capital management to enhance cash flows further. A lot of basic manufacturing is outsourced as well. The strong operating cash flows then get reinvested into acquisitions. Lifco also pays a small dividend. If there are additional opportunities after cash flows have been reinvested, Lifco will use debt for further M&A. The leverage ratio currently sits around 1.5 times net debt/EBITDA. At the same time, Lifco aims to be at a 2-3 times range (since going public, Lifco actually only has been inside of this range in 2016 briefly and is mostly around 1.6 times).

Lifco culture (Lifco Investor Presentation)

{kind=link}

Lifco by the numbers

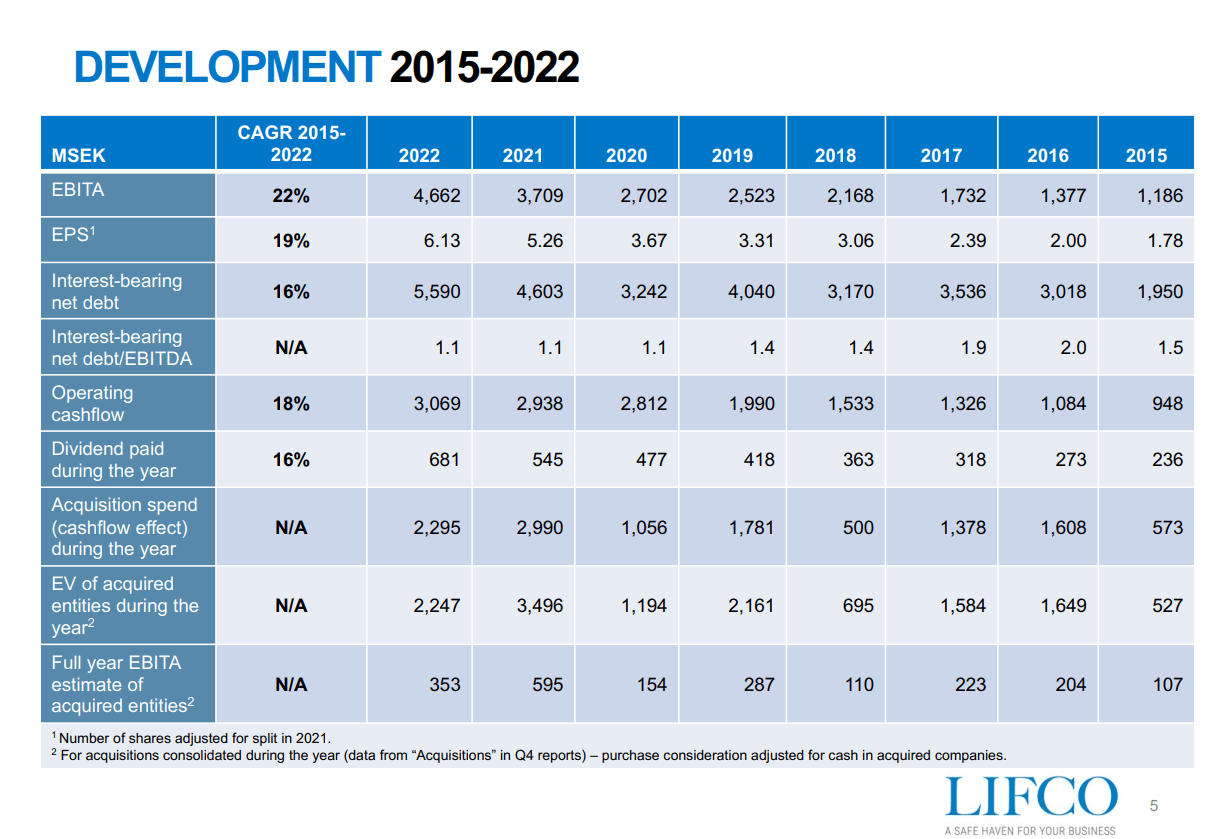

The company proudly displays its development with CAGRs for the most important KPIs in all its presentations. It's rare for companies to give detailed tables like this over long periods. Another example would be Alimentation Couche Tard (ATD: CA), which provides 10-year tables on all its presentations.

We can see that Lifco grew EBITA by 22%, debt by 16%, operating cash flow by 18%, and dividends by 16% in the period. In most years, dividends paid + acquisition spending have roughly equaled operating cash flow. Some years, like 2016 or 2021, saw much higher acquisition spending, while others, like 2020 or 2018 saw lower spending.

Lifco development 2015-2022 (Lifco Investor Presentation)

{kind=link}

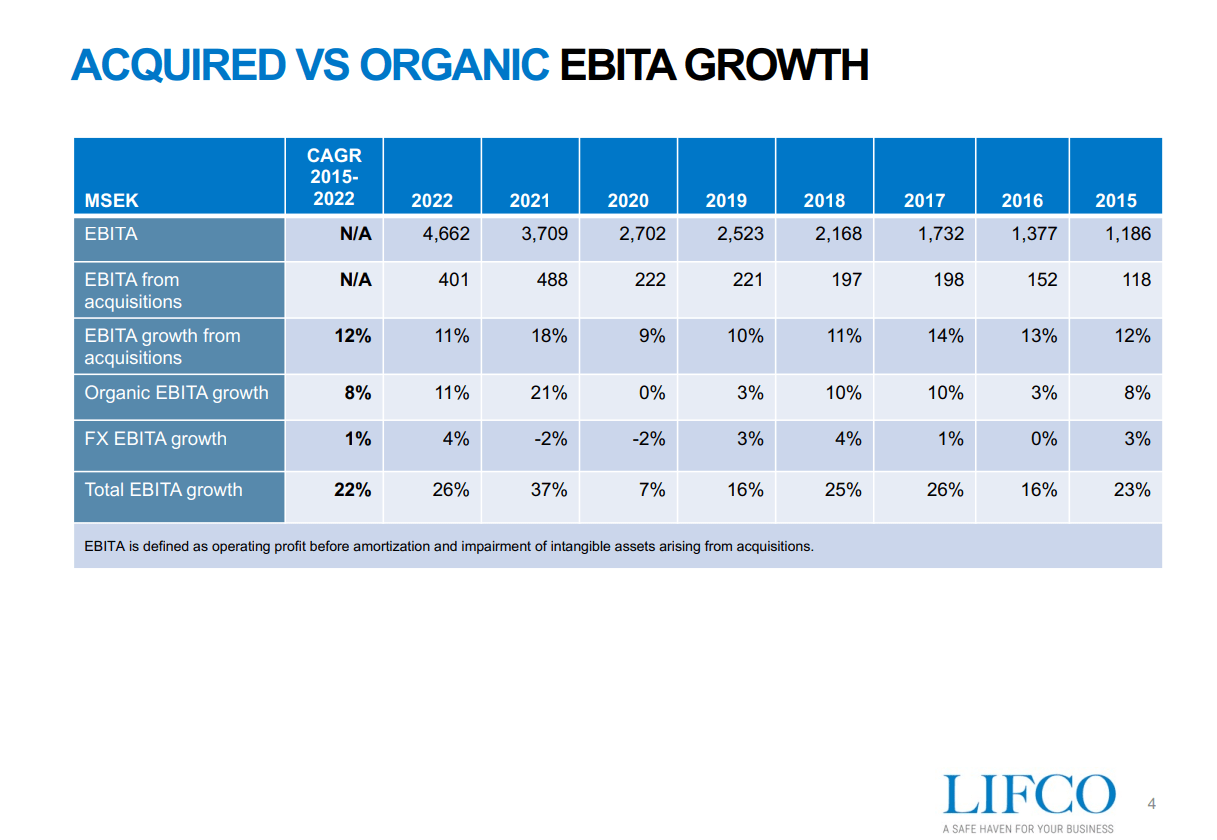

I mentioned Constellation Software earlier; if you're familiar with the company, you'll know that it predominantly requires acquired growth and hardly grows organically. Lifco is a different story, as the table below shows: While acquisitions attributed 12% CAGR to EBITA, organic growth from within the existing companies contributed 8% as well. Acquired growth has been broadly consistent, with most years seeing low double-digit growth, while organic growth is more cyclical, as it is for most industrial companies, ranging from 0% to 21%. It is worth noting that no year saw organic EBITA decline, even in 2020.

Lifco Acquired vs organic growth (Lifco Investor Presentation)

{kind=link}

Risks and upcoming earnings

Lifco is set to publish its Q3 earnings on the 20th of October. I expect that the main driver for the stock will be organic growth. Last quarter saw a 0.9% decline in organic growth and if this worsens we could see a negative reaction to the stock. The company announced a couple of acquisitions over the last months, so acquired growth should be in line with history. Cash conversion and working capital management are other factors investors should look at.

Generally, investors should be aware that 2/3 of Lifco's segments (with the exception of Dental) are cyclical, although Lifco never was very cyclical. This can have short-term impacts on earnings and the stock. Lifco also predominantly operates in Europe, which makes the European macro development an important factor to consider. Finally, if Lifco were to stop finding suitable targets to acquire or lose its discipline in acquiring the right companies at the right price, it could severely hinder the company's long-term trajectory.

Lifco could be undervalued

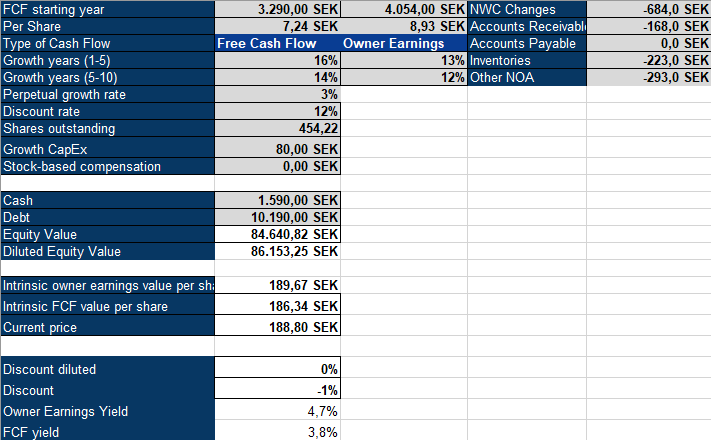

I prefer to value companies using an inverse DCF model because cash flows don't lie. For my owner Earnings, I added back $80/$351 million as growth capex: Lifco is happy to reinvest in the growth of its companies and this looks to be reasonable enough to me. Lifco also has a few Net Working Capital changes that depress cash flows, which I added back. Lifco never issued a share, so there is no Stock-based compensation to worry about. I used a 12% discount rate for Lifco to be more conservative: It is an industrial company, so it's better to be safe than sorry. We can see that Lifco must grow at 13% for the next five years, followed by 12% growth for five years. This looks reasonable; if we look back, we can see that historically EBITA grew by 12% through acquisitions alone. The opportunity is still ample to consolidate the vast, fragmented European market and the balance sheet is very healthy at 1.5x leverage, so there is no reason to expect this to slow. On top of the acquisition growth, we have organic growth as an upside potential: If Lifco did not grow organically from here, it would be fairly valued based on this model. If we can get organic growth (like the 8% CAGR over the last decade), we would have significant potential for outperformance. I like the risk-reward in Lifco, a high quality, long-term oriented serial acquirer, and am happy to increase my position during this period of stock price weakness from my current 5% allocation.

Lifco Inverse DCF Model ( Author's Model )

{kind=link}

For further details see:

Lifco: An Undervalued Swedish Gem