PSA - Life Storage: Merger Play Not Worth It

2023-03-16 14:34:13 ET

Summary

- Life Storage has declined the merger offer from Public Storage, but given a high potential for synergies, I think there's an increased offer coming.

- A higher offer will most likely drive the LSI stock price higher and could provide 10% upside in a matter of months.

- Still there are risks to this. I argue why you may not want to be stuck with LSI shares if the deal falls through.

Dear readers/followers,

If you've read my recent article on CubeSmart (CUBE) you know that I am not particularly bullish on Public Storage (PSA), especially in established legacy markets. My main worry which I described in detail in the article had to do with people leaving cities like NYC or DC and moving south which will inevitably lead to lower demand over time. In short I fear that the public storage has peaked and could stagnate going forward.

Today I want to analyze one more public storage REIT - Life Storage ( LSI ) which I believe may be better positioned than CubeSmart. In particular there are two factors that could make it a better investment. Firstly a portfolio concentrated more in southern growing markets and secondly a recent take-over offer which the company received from Public Storage and which I believe makes sense for both parties. Let's first have a look at these two factors, before analyzing the company in detail.

Portfolio

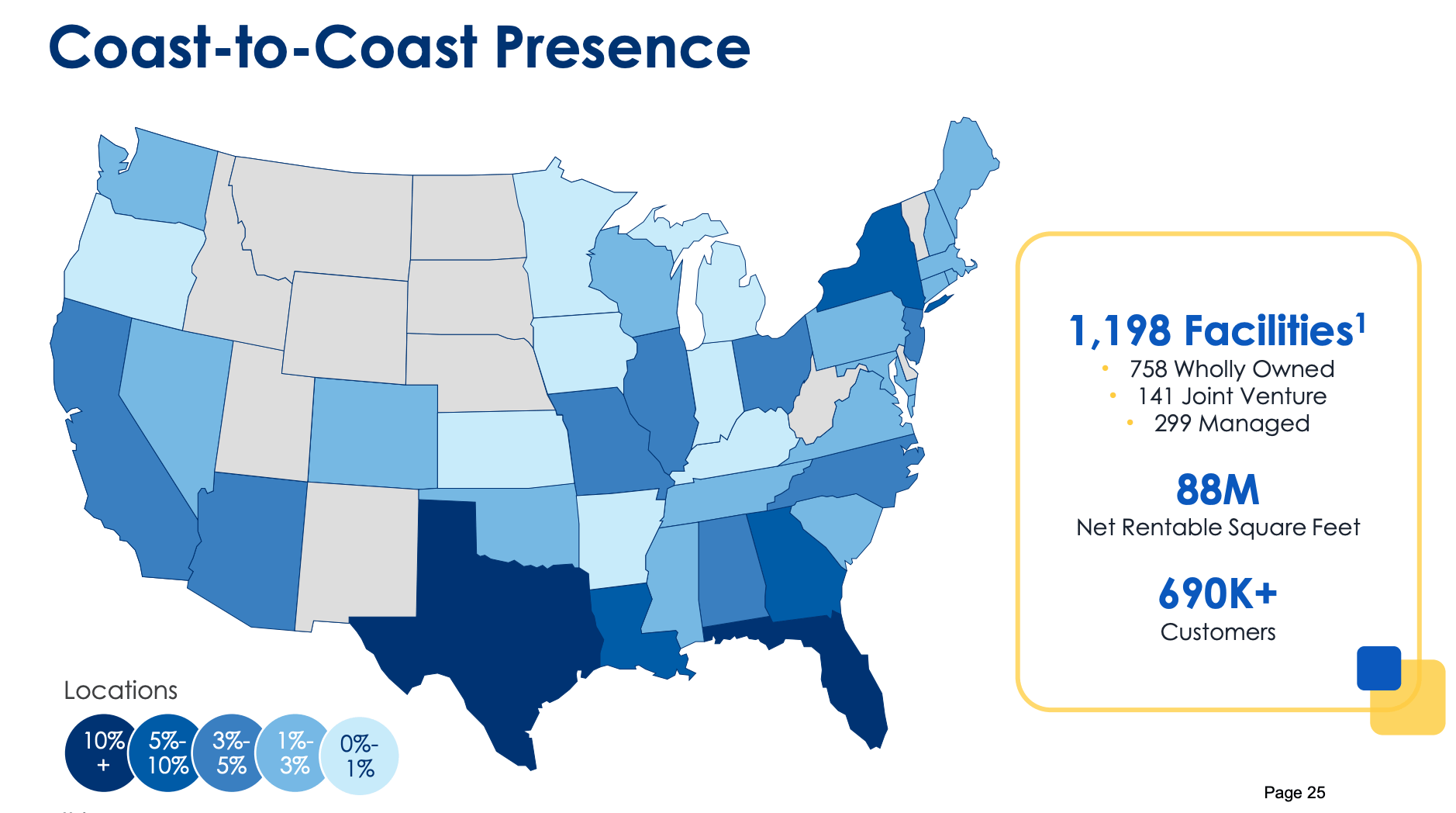

Life Storage is the fourth biggest player in the highly fragmented public storage industry with a 4% market share. It owns and operates about 1,200 facilities across the US with heavy exposure Florida (17% of total) and Texas (12% of total). Just like CubeSmart, the portfolio is located from coast-to-coast, but I like LSI's portfolio better because it is more heavily concentrated in the Sunbelt and not as present in the Northeast.

{kind=link}

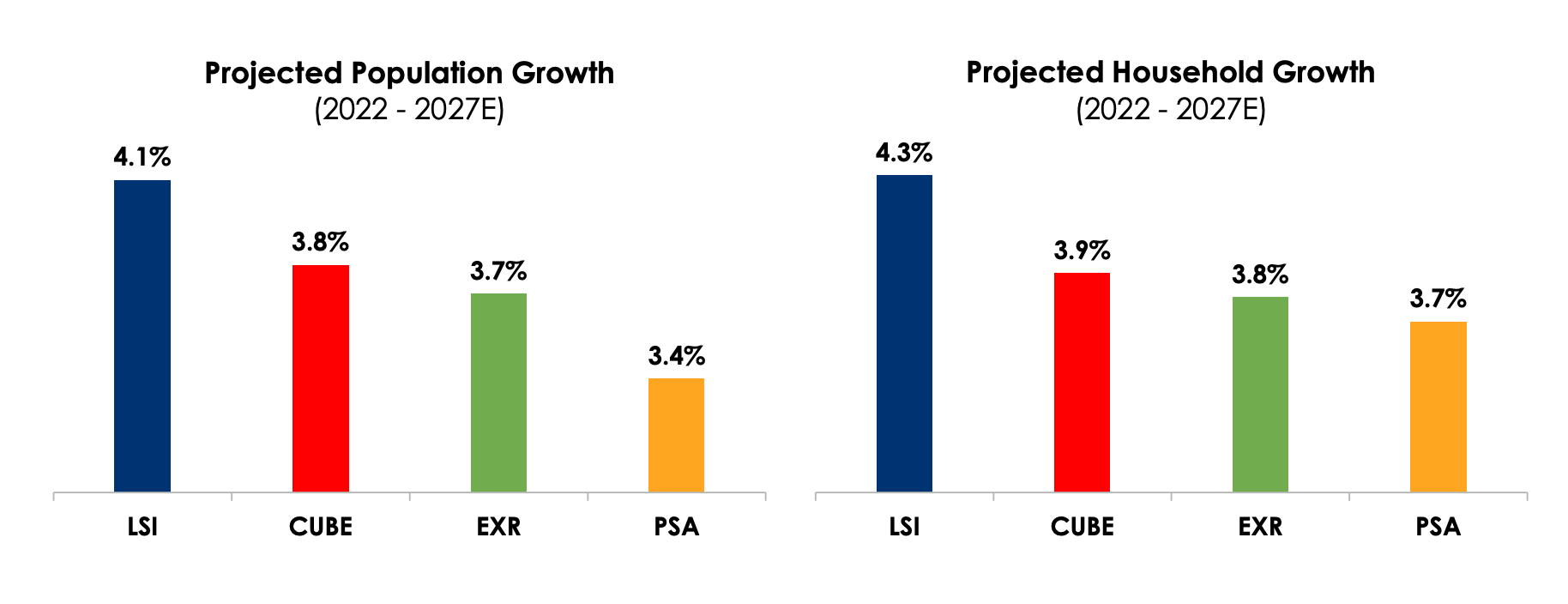

It's also worth pointing out that LSI's geographical focus has put its portfolio ahead of its peers in terms of projected population growth as well as projected household growth.

{kind=link}

Takeover

The fact that the industry is very fragmented means immense competition for tenants and also a relatively high likelihood of potential mergers between players. That's exactly what happened recently as the largest player on the market (9% market share) Public Storage made an unsolicited offer to acquire Life Storage.

The offer obviously had many moving parts, but the most important one for LSI's shareholders was that post-merger they would get 0.4192 shares of PSA for each share of LSI. With PSA trading around $300 per share, the offer was essentially to buy LSI at a 13% premium vs the price at the time. Assuming the deal will go through, this essentially puts a floor price on the shares of LSI of $125 per share (I will call this the target price). Consequently after the announcement the share price jumped by over 10% to just under $125 per share.

Management has declined the offer, stating that it was not in the best interest of shareholders, mainly for the reasons below:

{kind=link}

So let's see if the offer was decent. LSI guides towards a 2023 AFFO of $6.85 per share. With the target price of $125, the offer was to buy LSI at a forward P/AFFO of 18.25x. That's in line with the multiple it has traded at over the past five years and above its historical multiple since IPO. So on a purely mathematical level the offer wasn't bad at all. Of course there are other things at play here. Management definitely wants to keep their job, which is unlikely if the deal goes through so their incentive is to look for reasons why it is not a good deal (which they've done). Additionally, it is entirely possible that they intend to sell, but want to squeeze PSA a little harder for an extra 5-10%.

Whether PSA comes back with a stronger offer will ultimately depend on how much they want the deal to go through. Given the currently fragmented nature of the business, I imagine they are keen to acquire a competitor and become by far the largest player in the market (they would have a 13% market share while the second biggest player Extra Space Storage (EXR) is at just 8%).

Moreover, there are significant synergies to be had. In particular given that both companies operate in exactly the same business and in similar locations, almost the entire G&A expense of LSI could be eliminated. It stood at $77 Million in 2022 and I think it is quite likely that at least 50-70% of that could be saved so call it $50 Million in synergies each year going forward. With 85 Million shares of LSI outstanding, PSA is potentially getting an additional $0.59 if AFFO which effectively means that they are not paying 18.25x AFFO, but only 16.80x if we include synergies. That's arguably below market value and also below their own multiple of 18x. I think it makes sense for them to come back with a slightly higher offer which they should still be able to justify to their shareholders and one that LSI's management likely won't be able to refuse.

Assuming a 5% higher offer which goes through, LSI shareholders would be bought out for $131 per share which is 9% above the current share price. That's solid upside considering it could happen within the next 6 months or so. But the question remains, what if the deal doesn't go through? Let's have a look at the rest of their business to see if it's a company we want to hold.

Financials

It is no surprise that their 2022 operating results have been good. Their revenue grew by 15.5% YoY mainly driven by same store rent growth fueled by inflation and very short lease durations. Their NOI increased by 19.4% signaling that they were able to keep their expenses under control in the inflationary environment. Unfortunately past performance is no guarantee of future results so let's have a look at some data points that can help us determine where the company is headed.

First, occupancy has decreased throughout the year. From weighted average quarterly occupancy of 94.1% in 2021 to just 91.5% in 2022. The decline has been pretty linear and similar to that of CubeSmart. The trend of declining is somewhat worrisome as it confirms my thesis of declining demand. It is definitely something to keep a close eye on if you decide to invest in the space.

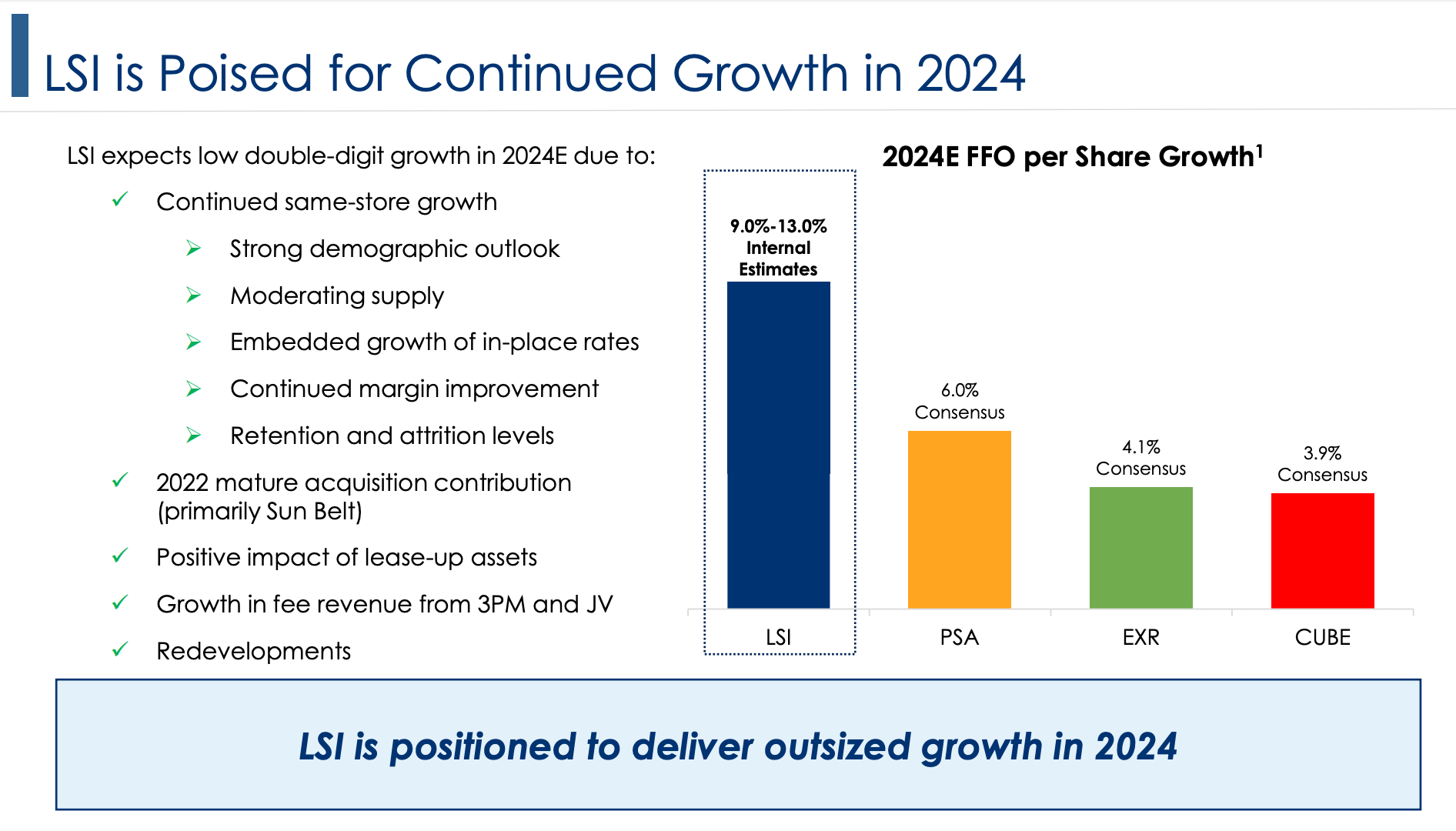

Second, as far as guidance, managements expects same-store revenue to grow by 4-5.5% in 2023. AFFO is expected by a similar percentage from $6.51 to $6.85 per share at midpoint. These expectations are reasonable over the short-term and roughly in line with those of LSI's peers. In their presentation , LSI included a slide where they show that their 2024 growth is magically going to accelerate to 9-13% while their peers will continue to only grow by 4-6%. The reasons listed don't justify this outperformance in my opinion, which is why I will not take this into account in my valuation. I can see 4-5% growth going forward, but remain cautious due to a threat of declining occupancy over the medium to long-term.

{kind=link}

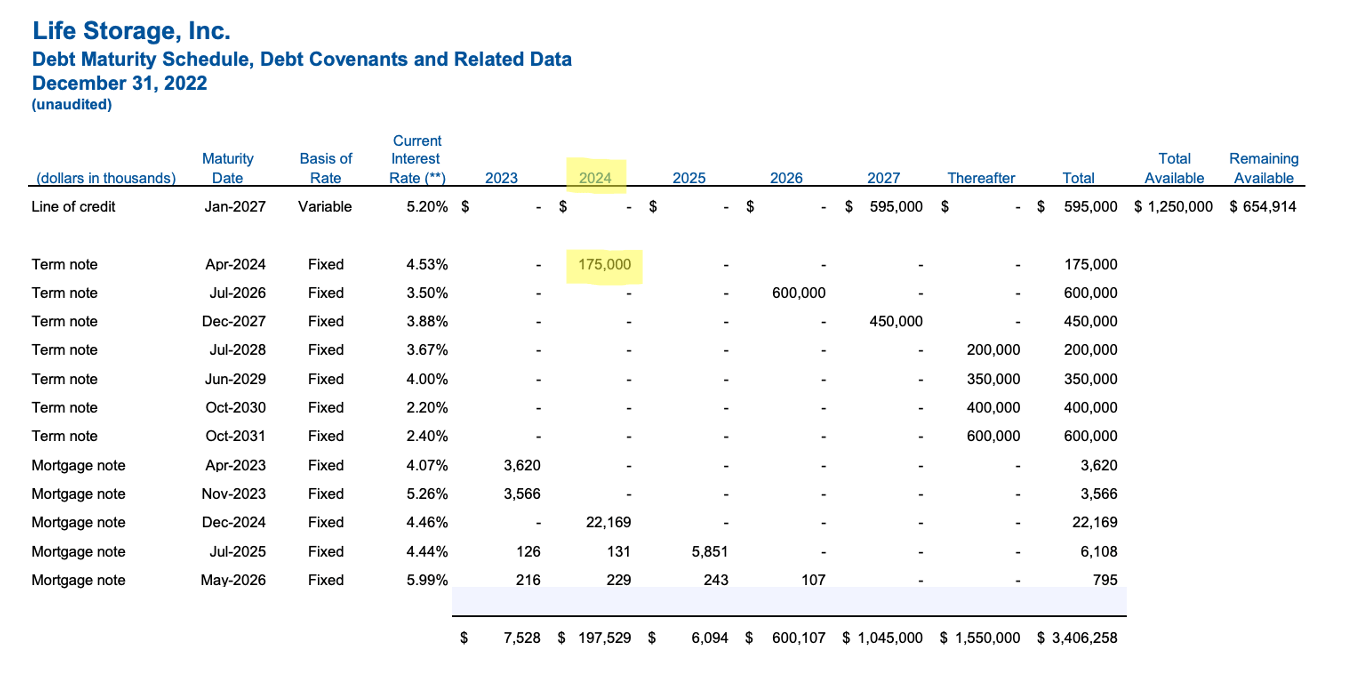

LSI has a BBB-rated balance sheet with $3.4 Billion in debt. The only notable maturity until 2026 is a $175 Million note due in 2024. The note already has a relatively high interest rate of 4.53% (vs weighted average rate of 3.6%) so I expect their interest expense to be relatively stable going forward. This is reaffirmed by the fact that all of their debt except for the line of credit is fixed rate. It's worth noting that their cash balance is very low at just $24 Million, though they still have over $650 Million available on their line of credit which should provide enough liquidity.

{kind=link}

Because 2022 operational results were so good, management approved an 11% increase to its quarterly dividend to $1.20 per share, or $4.80 per share annualized. This translates into a dividend yield of 4.0% which is well covered by FFO.

Valuation

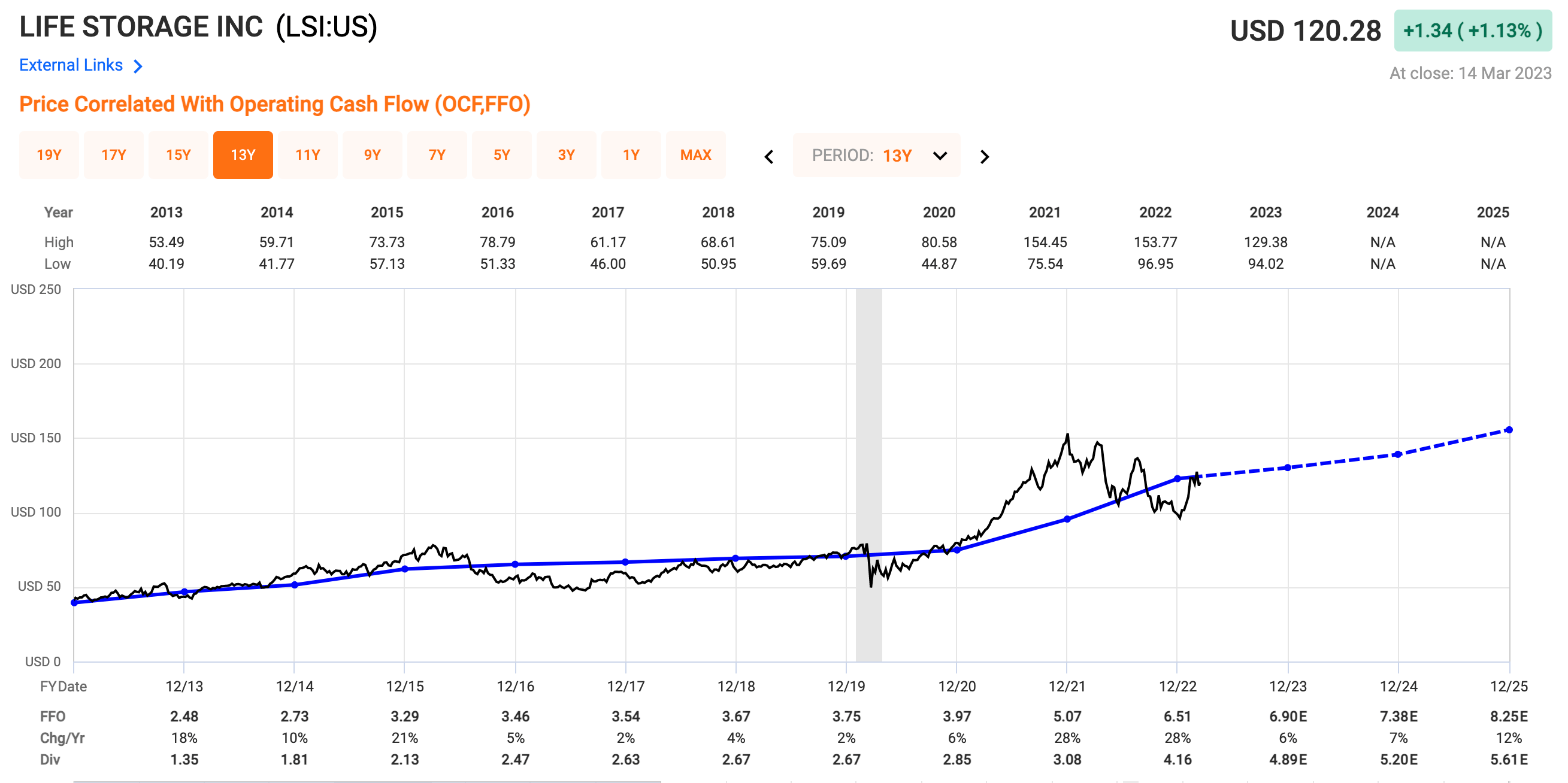

The stock is currently trading in line with their historical P/FFO multiple as seen below. In terms of implied cap rates, it is trading at 5.1%. None of this screams undervalued and in fact both of these metrics are more aggressive than CubeSmart, likely due to the fact that LSI jumped by 10% on the potential merger announcement.

{kind=link}

With that said, if you think that PSA will up their offer by at least 5%, you could buy the stock and likely make around 10% (or more if they up their offer by 10%) if the deal goes through. I think it's quite likely that PSA will make another push, but I am not willing to bet on that alone. I want to make sure that LSI is a company I want to hold for the long-term just to be safe if the merger doesn't go through. With what we've seen I think it's fair to say that LSI is about as attractive as CUBE here. Their portfolio is better positioned which will likely result in higher growth and hopefully more resilient occupancy, but their valuation is somewhat higher because of the merger announcement. Also there's a risk that if the higher offer doesn't come or is rejected, the share price could fall back to where it was prior to the first announcement (9% downside). Therefore I rate LSI as a "HOLD" here at $120 per share and will be watching the merger talks from the sidelines.

For further details see:

Life Storage: Merger Play Not Worth It