ALC - Lifecore Biomedical: Quality CDMO Potential Sale

2023-09-05 01:20:00 ET

Summary

- Lifecore Biomedical has divested its food-related assets and now focuses solely on its high-quality CDMO business.

- The company faced a rough patch earlier this year but has since refinanced its debt, secured a major customer contract, and is on the verge of doubling its theoretical capacity.

- There is a potential opportunity for significant returns if the company gets acquired, with a legitimate chance for +100% upside in the near term.

Investment Thesis

Lifecore Biomedical ( LFCR ), formerly known as Lander Inc, was until recently an amalgamation of no-sense entities. It encompassed a pre-made salad business, a processed avocado business, various other food-related assets, and a high-quality CDMO specializing in fill-finish processes for highly viscous liquids. During the past two years, management focused on selling and divesting the food-related assets, leaving the CDMO as its sole focus.

The company encountered a rough patch at the start of the year, finding itself in violation of its debt covenants, which triggered a technical default. Concurrently, they announced a strategic review process and the likely sale of the company. However, since then, the debt has been refinanced, a major customer committed a 10-year contract, and the business is on the verge of doubling its theoretical capacity, which will lead to substantial revenue and EBITDA growth in the coming years. Given the current share price, we believe there is an interesting opportunity to potentially earn a significant return in a short time frame if the company gets acquired.

What Happened This Year?

Let's make a recap of all the events that happened this year:

- Jan 9 : Raised $38.75 million through the sale of Series A Convertible Preferred Stock to support working capital and capex needs, while they also amended their credit facilities to increase liquidity and provide financial covenant relief.

- Feb 7 : Announced the sale of Curation Food's avocado product business for $17.5 million in cash.

- March 16 : Reported Q2 F2023 financial results and disclosed that they were in technical default of its debt covenants after hitting a speedbump with revenue tied to major customers adjusting their timing at the same time. Moreover, they announced the intent to explore strategic alternatives (in other words a sale) and a major expansion of business with ~40 year client Alcon (NYSE: ALC ).

- April 6 : Announced the sale of Curation's Food olive oil and vinegar business for $6.23 million (half cash, half notes).

- May 22 : Made public that they had entered into a new $150M financing agreement with Alcon that saw existing term loans repaid, a sale lease back of equipment, and a 10-year agreement with Alcon to supply Hyaluronic Acid ((HA)), a highly viscous ingredient forming the basis of numerous drugs in Alcon's portfolio.

Why did Alcon decide to became LFCR's primary lender? Because of its strategic value. Alcon had 2 suppliers of HA (LFCR and unknown). However, unknown has faced several setbacks and more recently notified Alcon of their intention to cease supplying them within the next 18 months, as they intend to redirect this supply to meet their own internal demands.

As a result, Alcon found itself with no alternative options but to help LFCR out. When a customer extends financing to a supplier, it provides insight into the importance they place on the relationship (or their dependence on it) and the level of switching costs involved.

Business Performance

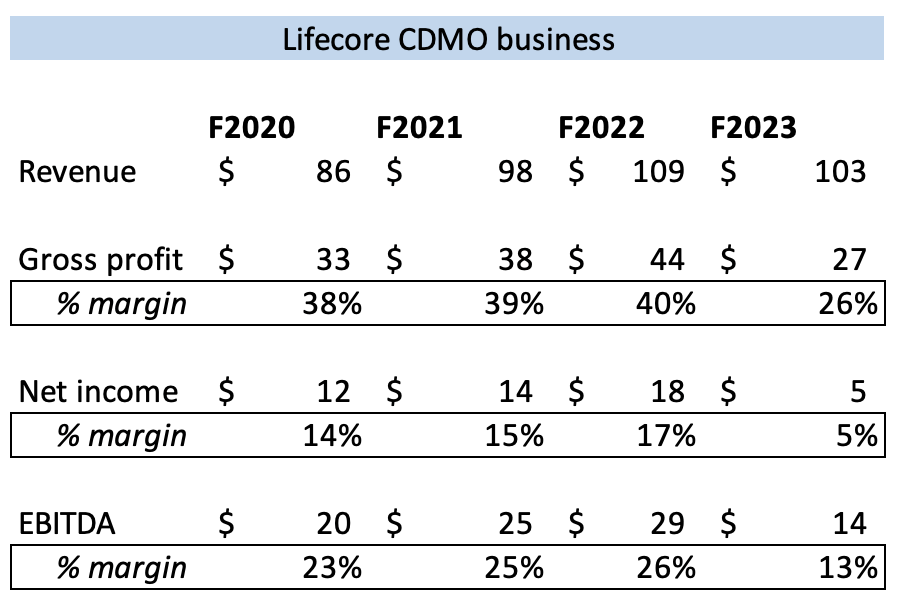

LFCR reported F2023 financial results on August 31. On a consolidated level, the results look horrible given all the costs related to the divestures of Curation Food, restructuring charges and loss on debt refinancing, which is why in this analysis we will solely focus on the CDMO numbers.

Revenue came in at $103 million, 5.5% lower than a year ago. The decrease had to do with the timing of shipments to costumers; lower development revenue associated with a delay in onboarding new customer projects as well as a higher mix of earlier stage, lower revenue projects; and inflation associated with legacy commercial products.

As of the end of Q4, LFCR manufactured 29 commercial products for 14 clients, unchanged from Q3. However, their active development projects increased by 5 to 29. These 5 new projects are also with 5 new customers, bringing the total number of costumers to 27. The projects are spread across early phase clinical development with 7 projects, Phase I and II clinical development with 8 projects and Phase III clinical development and scale up commercial validation activity with 14 projects.

Finally, net income for the segment was $5 million and adjusted EBITDA was less than half of what it was a year ago at $14 million. The bottom line was obviously affected by the list of reasons listed above.

{kind=link}

Outlook

Management didn't provide a formal guidance, but they did paint a picture of how the year will look like during the earnings call .

They anticipate Q1 to be the low point for the year, with revenue and adjusted EBITDA expected to decrease sequentially (EBITDA is estimated to be approximately at breakeven).

In Q2, they expect revenues and adjusted EBITDA to show accelerated improvement following delayed commercial shipments. Compared to the same quarter in the prior year, they anticipate Q2 revenues for F2024 to grow by nearly 40% and adjusted EBITDA growing at roughly twice the rate of revenues.

The second half of the fiscal year is expected to generate adjusted EBITDA at more normalized levels, similar to or greater than what it was achieved in the H2 F2022($13.9 million), as they will be able to effectuate pricing offsets under existing contracts to help mitigate some of the impacts of the recent inflationary pressures. It is important to note that all the adjusted EBITDA numbers elude the burden of the overhead corporate costs.

Potential Buyout Price

How much do CDMO businesses sell for? Fortunately, there has been significant M&A activity in this sector over the past few years. Here is a short list of transactions:

- Catalent (NYSE: CTLT ) acquired Cook Pharmacy for $950 million or 17.3x EBITDA.

- Thermo Fisher (NYSE: TMO ) bought Patheon for $7.2 billion or 17x EBITDA.

- Baxter (NYSE: BAX ) divested its CDMO business for $4.3 billion, representing a multiple of 6.6x revenues.

- Cambrex acquired Avista for $252 million at a multiple of 3.9x revenues.

- Lonza acquired Capsugel for $5.5 billion or 16x EBITDA.

The average EV/EBITDA ratio was around 17x. So, what would the upside be if LFCR were to be acquired at similar multiples?

Using F2022 numbers, the stock would appreciate by 46% from current levels if it were to be acquired at a 17x EV/EBITDA ratio, or more than 83% if the takeover is at a 20x EV/EBITDA ratio. This aligns with the historical norm for businesses of this type, and we believe there is no reason for LFCR to receive a discount. On the contrary, we believe it deserves a premium.

Why would LFCR deserve a premium? There are three main reasons:

- Strategic value : LFCR is the sole major manufacturer of pharmaceutical injectable-grade HA, with unmatched expertise in injectable CDMO in the current market, essentially granting it a monopoly. Approximately 55% of all new drug applications are for injectables, and prefilled syringe demand is growing at an estimated 13% per year.

- Capacity doubling : LFCR is set to introduce two new filling lines in the coming months, significantly increasing their theoretical capacity from 22 million to 45 million units. It's crucial to note that this added capacity is already in high demand (CDMOs ensure committed capacity before building it), and the lead time for installing new filling lines typically spans three to four years, from the initial design phase to FDA approval.

- Alcon contract : In order to fulfill the increased HA volume orders associated with their expanded demand (Alcon 10-year agreement), LFCR is in the process of moving from a single-shift HA fermentation production to a 24/7 staffing model, which is expected to increase HA capacity by up to 50% by June 2024. This business could be worth more than $30 million in revenue, which could translate to $8-$10 in EBITDA .

Given the recent price decline last week, we believe there's a compelling opportunity for a +100% return before year-end.

Risks and Takeaway

Despite our belief in the value of the business and potential buyout price, the stock has been performing badly lately because of a few reasons:

- Cove Street sale : Cove Street is a hedge fund that holds a large chunk of LFCR. Recently, they disclosed they reduced their position by a mere 2%, which spoked investors. We think this 2% is an insignificant amount and doesn't related to the potential sale or asset value.

- Disappointing guidance : The restructuring of the company and investments in capex are not done yet and will affect F2024 numbers meaningfully. The market was hoping for more normalizes levels of EBITDA in F2024, and it is not clear whether they will achieve them or not.

- No sale update : Investors were also hoping for an update on the strategic review process, but during the earnings call Jim Hall ((CEO)) said it remains ongoing, and they aren't in a position to provide any updates yet.

Most of the bears argue that no buyer will pay for 2025-26 EBITDA numbers and that the buyout price, if any, will be in the low-teens. But even in that case, you could be looking at a potential 50%-70% return.

In the best case scenario, it gets acquired for +$20 per share. In the worst case scenario, you would be left holding a quality CDMO on a path to generate +$80 in EBITDA in a few years. Either way, there is little chance of losing money in the long run.

For further details see:

Lifecore Biomedical: Quality CDMO, Potential Sale