LNW - Light & Wonder: A Look At If Its Optimism Reflects Reality

Summary

- So far, the company has shown it can generate momentum after completing its transformation.

- In the latest earnings call, the company reported top and bottom line growth in the double-digits, with revenue beating by $18.17 million, but EPS missing by $0.06.

- With a delevered balance sheet, more streamlined organization, and premium products offered in all its segments, it's on the company to prove it can consistently execute.

- Since the tailwinds are now at its back, coming close to meeting or beating expectations could surprise the upside.

The last time I covered Light & Wonder, Inc. ( LNW ), I wrote about the company being close to finishing its transformation into a leaner, meaner organization that had the potential to surprise to the upside if it proved it could execute on its growth strategy going forward.

Based upon its latest earnings report and the current quarter, it appears it has generated the type of momentum that could break it out of its trading range and bring the stock to the next level.

Taking into account the fact the company now has a premium product available in all the segments it competes in, the next couple of quarters will prove whether or not those products are the right ones for the market, and if it'll be able to maintain its momentum in the quarters ahead.

In this article we'll look at some of its recent numbers, its current momentum, and the potential headwind that could still disrupt the momentum the company is now enjoying, as well as the strong optimism inherent in management.

{kind=link}

Some of the numbers

Revenue in the fourth quarter of 2022 was $682.00 million, compared to revenue of $580 million in the fourth quarter of 2021, an increase of 18 percent. Full year revenue came in at $2.51 billion, compared to $2.15 billion for full year 2021, a gain of 17 percent year-over-year.

Net income in the reporting period was $21.00 million, compared to net income of $62.00 million in the fourth quarter of 2021. Most of the decline in net income came from a tax benefit associated with a reversal of the company's valuation allowance, which had a positive impact on the fourth quarter of 2021. Net loss for full year 2022 was -$(176.00) million, compared to net income of $24.00 million for full year 2021.

Consolidated AEBITDA in the fourth quarter of 2022 was $265.00 million, compared to consolidated AEBITDA of $216.00 million in the fourth quarter of 2021, an increase of 23 percent year-over-year. The improvement was primarily attributed to the performance of its Gaming business. Consolidated AEBITDA margin in the fourth quarter was 39 percent, up from 37 percent year-over-year.

Consolidated AEBITDA for full year 2022 was $913.00 million, compared to consolidated AEBITDA of $793.00 million for full year 2021, a gain of 15 percent. The improvement was attributed to double-digit revenue growth.

Net cash from operating activities in the reporting period was -$(87.00) million, compared to net cash of $226.00 million in the fourth quarter of 2021. Net cash from operating activities for full year 2022 was -$(381.00) million, compared to net cash of $685.00 million for full year 2021.

Free cash flow in the fourth quarter of 2022 was -$(148.00) million, compared to free cash flow of $100.00 million in the fourth quarter of 2021. Free cash flow for full year 2022 was -$(674.00) million, compared to free cash flow of $443.00 million for full year 2021.

Much of the negative net cash and free cash flow decline was associated with taxes associated with divestitures. That said, it's an important set of data to watch closely in the earnings reports ahead to see what the cost of generating revenue growth will be going forward.

Performance by segment

{kind=link}

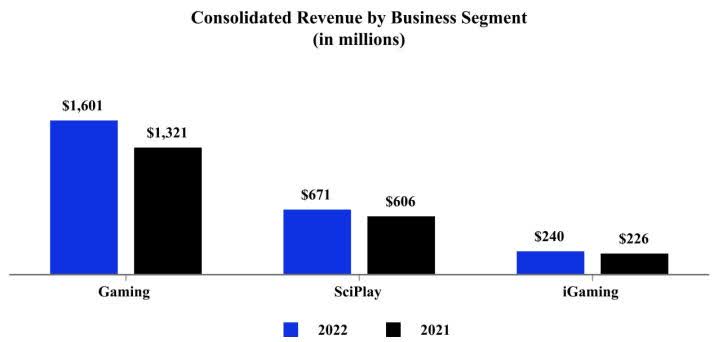

Gaming

Gaming is easily the largest segment of the company, and in the fourth quarter it generated revenue of $438 million, up 18 percent year-over-year. For full year 2022 gaming revenue was $1.6 billion, up 21 percent.

The premium installed base in North American gaming operations climbed 8 percent year-over-year, while global game revenue increased 11 percent sequentially in the fourth quarter. Full year gaming revenue in the global market was up 41 percent year-over-year. An increase in demand for its cabinets was the main catalyst there.

AEBITDA jumped to $215 million, a gain of 16 percent over the fourth quarter of 2021. AEBITDA margin in the segment for the reporting period was 49 percent. Full year AEBITDA increased by 16 percent to $767.00 million.

The growth in the gaming segment was attributed to double-digit growth in tables and systems, along with strong growth in its product revenue.

Systems revenue was up 26 percent year-over-year, based upon an increase in installs and domestic cargo sales volumes. This part of the gaming segment includes a meaningful amount of recurring revenue, which is expected to increase in the quarters ahead based upon new loyalty features is adding to the mix. In tables, the company improved sales by 11 percent year-over-year, primarily from growth in sales volumes and bulk subscriptions.

When analyzing the company, its gaming segment is easily the most important to closely watch, because as its gaming segment goes, so will go the company as it stands today.

{kind=link}

SciPlay

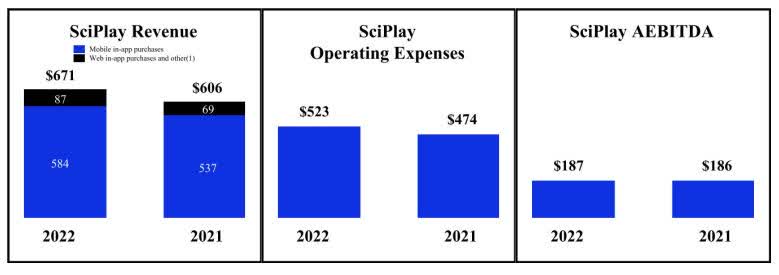

Revenue from its SciPlay segment in the fourth quarter was a record $182 million, a gain of 18 percent year-over-year. The primary catalysts there were Jackpot Party and Quick Hit Slots, two of its larger games.

Full year revenue for 2022 in SciPlay was $671.00 million, up 11 percent from full year 2021 revenue of $606.00 million.

AEBITDA in the fourth quarter was $59.00 million, up 24 percent year-over-year. Full year AEBITDA was $187.00 million, compared to full year 2021 AEBITDA of $186.00 million. Among some of the highlights in the segment for 2022 was a record number of payers - up 13 percent from 2021, a record payer conversion of 10.4 percent, an average monthly revenue of almost $100.00 per paying user, and record quarterly ARPDAU of $0.87, up 18 percent year-over-year. With the segment having more payers than it has had in its history, it resulted in it taking market share, and management sees that momentum continuing throughout 2023.

{kind=link}

iGaming

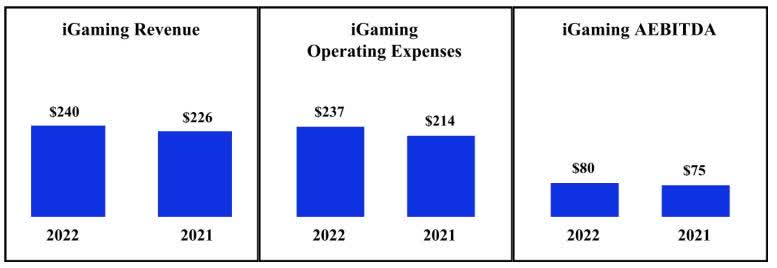

Its iGaming unit also had a solid quarter, generating $62.00 million in the reporting period. Full year revenue in the segment was $240.00 million, compared to $226.00 million in full year 2021.

Revenue in the U.S. market was up 41 percent for the quarter on a year-over-year basis; revenue in the U.K. was up 27 percent year-over-year; and revenue in Europe was up 12 percent year-over-year. The company attributed growth in those markets to successful, regional product launches. AEBITDA for iGaming was $19.00 million in the fourth quarter, up 27 percent year-over-year. Full year AEBITDA was $80.00 million, compared to AEBITDA of $75.00 million for full year 2021.

AEBITDA margin for its iGaming segment was 31 percent in the fourth quarter, up 300 basis points. The improvement was driven by growth in revenue, which resulted in AEBITDA margin of 33 percent for full year 2022.

Taken together, three segments are expected to maintain momentum, the management says it's the first time the company has a premium product in every major category and every major segment.

This is what is the key driver of company optimism, and if it can execute and deliver the goods in 2023, the company could definitely surprise to the upside.

{kind=link}

The potentially disruptive headwind

As most readers know, there remains a lot of uncertainty on the economic front in 2023, with the Federal Reserve expected to continue raising interest rates to combat inflation, and a significant number of companies cutting back on their headcount.

If things get worse before they get better, a lot more people are going to either lose their jobs or prioritize spending in anticipation of the possibility. With that in mind, LNW is definitely exposed to a potentially strong headwind if that's how it plays out.

Depending on the sector, there have been mixed messages as to the impact of higher interest rates on various industries. The high-tech sector, construction, some retail, and real estate have taken hits, and if that spreads to other industries in the months ahead, spending on gaming and associated businesses are going to take a big hit.

That would of course be disruptive to LNW, and would at minimum, temporarily weaken its momentum. And if a deep and lengthy recession occurs, it could take a significant period of time for LNW to regain that momentum.

With current visibility, there is simply no way of knowing which way the global economy is going to go in 2023, and that uncertainty hangs over LNW.

Conclusion

LNW is heading in the right direction, and after divesting of some assets and streamlining the company, improving its balance sheet, and having a solid set of products competing in the market at the same time, the company has done what it can do to give it a chance to maintain its growth momentum in 2023, and possibly 2024 if it isn't disrupted by economic factors outside its control.

But even if there isn't much of an impact from weak economic conditions, the company is still in the early stages of post-transformation, and it has yet to prove it can generate sustainable growth while improving its bottom line.

It has made a nice move since trading at its 52-week low of $40.10 on September 23, 2022, closing at $63.17 on March 2, 2023. That's a concern to me because a lot of what the company has been doing has been visible to investors, and much of its performance is probably already priced in.

For that reason, it would probably be wise to wait for a pullback for those that believe the company is positioned well for long-term growth. The next earnings report should reveal how its premium products are doing in its various segments, and if the numbers confirm they are contributing significantly to the top and bottom lines, that would be the confirmation I would look for to consider taking a position.

And for those that think the company may get out and have some FOMO, dollar-cost averaging with disciplined position sizes will reduce risk if the play goes against you.

My conclusion is the company is competing in a growth sector that it has positioned itself fairly well to generate long-term growth. But I see that taking some time to play out, and there's no reason I can see that should pressure investors to take a position because the stock price is about to take off.

As for management, I see them as being a little overly optimistic in relationship to where the company stands today.

For further details see:

Light & Wonder: A Look At If Its Optimism Reflects Reality