SCPL - Light & Wonder: SciPlay And Further R&D Efforts Would Imply Undervaluation

2023-06-18 23:44:31 ET

Summary

- Light & Wonder's acquisition of SciPlay could bring more attention to the company's business model and potentially lead to a larger valuation.

- SciPlay's impressive growth of 40.7% CAGR and average payer conversion of 10.3% could positively impact Light & Wonder's financial figures.

- Risks include lower legislation efforts for iGaming, failed branding, and recession, but despite these risks, Light & Wonder appears undervalued.

Light & Wonder, Inc. ( LNW ) recently noted the acquisition of 100% of SciPlay ( SCPL ), which could, in my view, bring more attention to the business model of LNW. Considering that SciPlay saw growth of close to 40.7% CAGR in its business, I would expect beneficial expectations after the acquisition. Also, assuming that the average daily revenue per unit will continue to trend north as seen in the last quarter, I believe that Light & Wonder could trade at a larger valuation. I saw risks from lower legislation efforts to implement iGaming in new regions, failed branding, and recession. With that, even considering the risks, the company appears undervalued.

Business Model And Recent Acquisition Proposal

Light & Wonder, Inc is a cross-platform global games business model focusing on content and digital markets. The company supplies game content and gaming machines, CMSs, and table game products and services to licensed gaming entities. Besides, management is specialised in providing social casino and other mobile games, including casual gaming, to retail customers.

Source: Investor Presentation

I believe that Light & Wonder, Inc is not correctly valued by the market, but the company may become even more undervalued after the full acquisition of SciPlay. The transaction will most likely be approved because Light & Wonder already owns a majority stake in SciPlay.

Source: Investor Presentation

I believe that the figures reported by SciPlay are quite impressive. I feel a bit bad for the shareholders of SciPlay now that Light & Wonder, Inc expects to buy the whole company. SciPlay reported substantial growth of close to 40.7% CAGR with an average payer conversion of 10.3%. With ownership of 100% of SciPlay, Light & Wonder, Inc will most likely see an increase in its financial figures.

Source: Investor Presentation

Quarterly Report Figures Were Not Impressive, And The Acquisition Of SciPlay Corporation Was Not Celebrated, However The Stock Price Did Trend North

I believe that the recent figures reported in the last quarter were not that impressive, however most shareholders may want to have a look at the new figures. The company did report quarterly sales growth y/y, but increases in SG&A and research and development expenses growth resulted in a smaller net income.

More in particular, the company noted total revenue worth $670 million , selling, general and administrative expenses close to $192 million, research and development worth $54 million, depreciation, amortization and impairments of $101 million, and interest expense of -$75 million. As a result of net income from discontinued operations, net of tax of $0 million, quarterly net income stood at $27 million.

Source: 10-Q

A few days later after Light & Wonder delivered its quarterly figures, management reported the acquisition of SciPlay for $422 million. Light & Wonder already owned close to 83% of the total amount of shares, however the market did not really react well to the transaction.

Light & Wonder, Inc. (NASDAQ: LNW) (“Light & Wonder,” “L&W” or the “Company”) today announced that it has submitted a proposal to the Board of Directors of SciPlay Corporation under which Light & Wonder would acquire the remaining 17% equity interest in SciPlay that it does not currently own for $20.00 per share in an all-cash transaction (the “Transaction”) valued at $422 million. Source: Investors | Light & Wonder

Right after the M&A news, the stock price declined a bit to around $56 per share, where there seems to exist a lot of buyers, and rebounded to around $64-$65 per share.

Source: SA

Balance Sheet

As of March 31, 2023, the company reported cash and cash equivalents worth $931 million, a bit more than that in 2022, and restricted cash close to $93 million. Also, with accounts receivables of $458 million and inventories close to $172 million, prepaid expenses, deposits and other current assets stood at about $108 million. Finally, total current assets were equal to $1.762 billion.

Non-current assets include property and equipment worth $214 million, with operating lease right-of-use assets of about $47 million, goodwill close to $2.922 billion, and intangible assets worth $743 million. In sum, total assets were equal to $6.022 billion, more than 1x the total amount of liabilities.

Source: 10-Q

With regard to the list of liabilities, the company reported current portion of long-term debt worth $23 million, with accounts payable close to $189 million, accrued liabilities of $362 million, and total current liabilities of $642 million. The ratio of total current assets/current liabilities stands at more than 1x, so I am really not afraid of any liquidity issue in the near future. Also, with deferred income taxes worth $71 million, long-term debt, total liabilities, were equal to $4.838 billion.

Source: 10-Q

Expectations From Other Analysts Include Net Sales Growth And Net Income Growth

The expectations from other analysts are quite beneficial. I believe that investors may want to have a look at them. They expect sales growth from 2023 to 2025 as well as net income growth. 2025 net sales would stand at $3.216 billion, with 2025 EBITDA of $1.305 billion, operating margin of 22%, and 2025 net income of $391 million.

Source: Marketscreener.com

My DCF Model Implied A Valuation Of $77 Per Share

Under my financial model, I assumed that Light & Wonder, Inc would successfully create a fully cross-platform with evergreen franchises available in any platform. As a result, the new games designed would be profitable for a longer period of time.

Besides, I assumed that future research and development would offer higher growth market products, and future R&D expense growth would be as high as in the past. In this regard, I believe that investors may appreciate having a look at the following slide.

Source: Investor Presentation

Under my FCF model, I also assumed that Light & Wonder, Inc will continue to hire new personnel focused on research and development. Management reported a significant number of employees all over the world, and the headcount exploded in the 20 years. I assumed that the headcount will continue to trend north in the coming years. More personnel working in R&D will most likely bring more products, net sales growth, and FCF growth.

We have Gaming R&D personnel located in our Las Vegas, Nevada and Chicago, Illinois facilities. We have SciPlay personnel located primarily in Austin, Texas; Cedar Falls, Iowa; and Tel Aviv, Israel. We have iGaming R&D personnel based primarily in the United Kingdom, Greece and India. We also have game development studios in Las Vegas; Sydney, Australia; Bristol, England; Montreal, Canada; Stockholm, Sweden and additional R&D staff in Reno, Nevada and Vienna, Austria and in various other smaller locations. Source: 10-k

Source: YCharts

Besides, I assumed that further agreements with large brands and third parties to produce games will be most likely successful. Note that Light & Wonder, Inc designed games using well-known brands from Warner Bros. ( WBD ), Metro-Goldwyn-Mayer, and Frank Sinatra.

We continue to invest in the recognition of our brands and brands that we license. Certain of our games are based on popular brands licensed from third parties, such as Hasbro, Inc.; Warner Bros. Consumer Products Inc.; Frank Sinatra Enterprises, LLC; ABG EPE IP LLC, Elvis Presley Enterprises, LLC; Danjaq, LLC and Metro-Goldwyn-Mayer; John R. Cash Revocable Trust; and Universal Studios, parent company NBC Universal Film and Entertainment. Source: 10-k

It is also worth noting that Light & Wonder, Inc was ready to divest certain parts of the business, or discontinued certain operations that were not aligned with the current business direction. Further sale of business segments will most likely bring cash in hand, which investors would most likely appreciate. In my financial model, I assumed that new sales of subsidiaries could occur. In this regard, I believe that investors may want to read the following lines:

Our prior line of business that provided sports betting services which enable customers to operate sports books, including betting markets across both fixed-odds and pari-mutual betting styles. This business was divested during the third quarter of 2022 and is included in discontinued operations in our financial statements. Source: 10-k

With the completion of the Divestitures, we have significantly de-levered our balance sheet, enabling us to invest organically and inorganically in our core growth areas to accelerate our strategies by investing and unlocking shareholder value. Source: 10-k

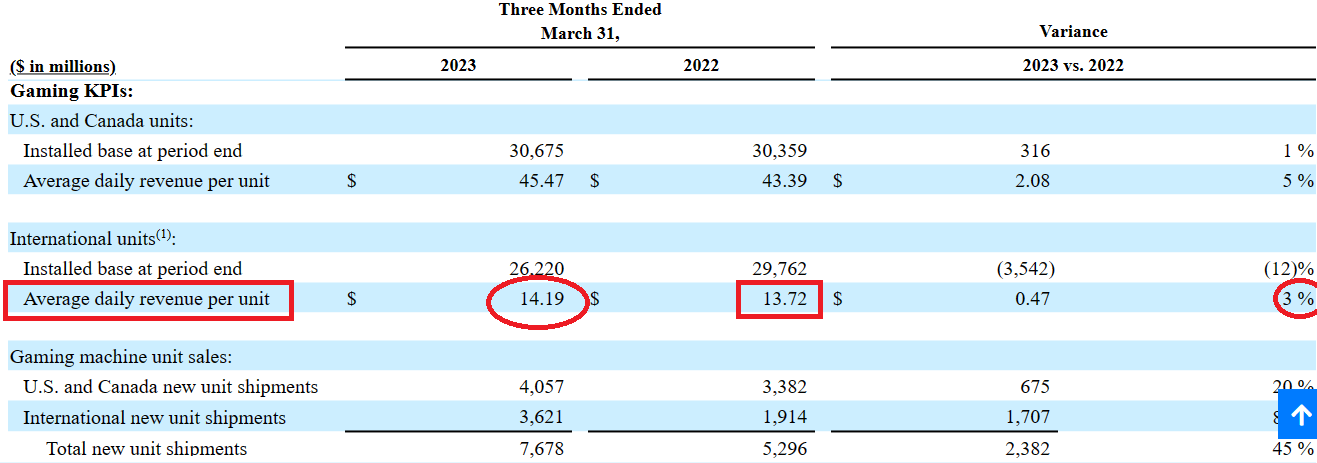

Finally, I believe that assuming further increase in the average daily revenue per unit and more unit shipments as we saw in the last quarter appears reasonable. In the last 10-Q, the company reported 5% more average daily revenue per unit in the United States and Canada. At an international level, the company reported an increase in the average daily revenue per unit of close to 3%. The numbers are pretty impressive.

{kind=link}

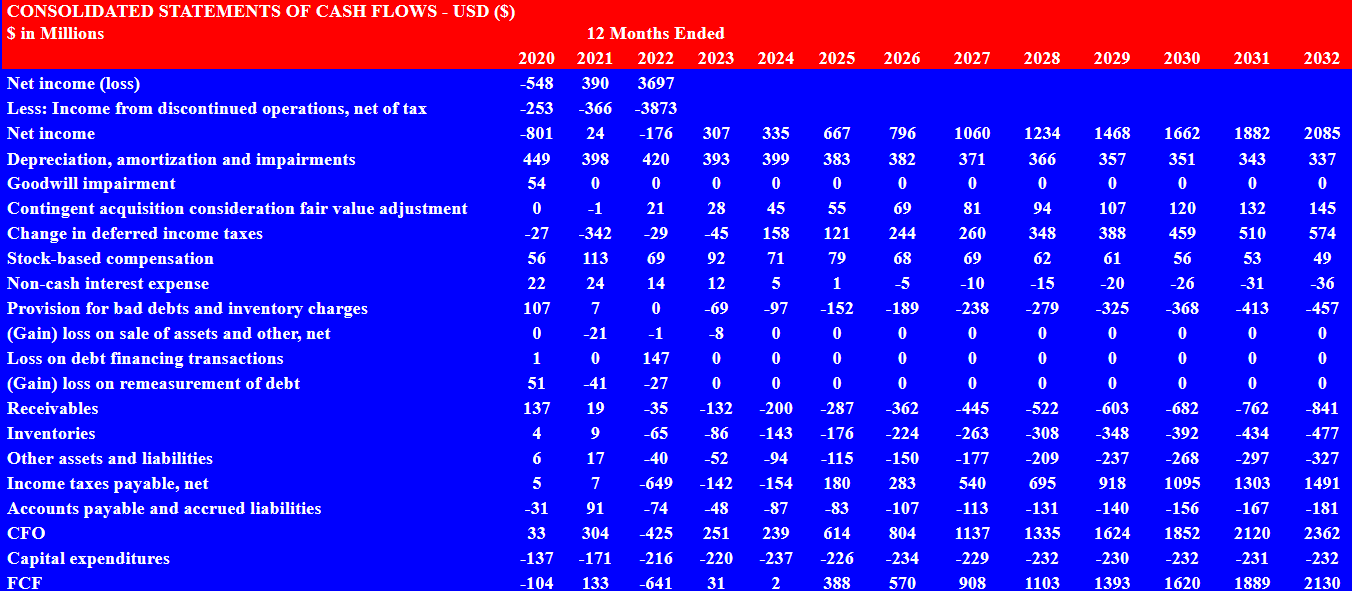

My DCF model included net income growth from 2023 to 2032 and D&A increases in the same time period. Besides, with increases in changes in accounts receivables, changes in inventories, and increases in income taxes payable, I obtained growing CFO and FCF. I believe that my figures are overall quite conservative.

In particular, I assumed 2032 net income of $307 million, 2032 depreciation, amortization and impairments of about $393 million, stock-based compensation of $92 million, and provision for bad debts and inventory charges of close to -$69 million. If we also include 2032 changes in receivables of -$132 million and changes in inventories close to -$87 million, 2032 CFO would be $251 million. Finally, I included 2032 capital expenditures of -$220 million, which would imply 2032 FCF of $31 million.

{kind=link}

With a conservative multiple EV/FCF of 12x and a WACC of 12.8% million, the implied enterprise value would be $9.929 billion. Besides, taking into account the current portion of long-term debt of $23 million, cash worth $931 million, restricted cash close to $93 million, and long-term debt of $3867 million, the implied equity would be $7.063 billion. Finally, the fair price would be close to $77 per share.

Source: My Financial Model

Risks

In my view, lack of brand recognition could be a disaster for the company. Management invests a lot of money to build its brand. If these efforts are not successful, shareholders may suffer a decrease in the margins, which may bring lower stock valuation. In this regard, management offered a certain explanation.

Even if our brand recognition and loyalty increases, this may not result in increased revenue and profitability. For these reasons, our rebranding initiative may not produce the benefits expected, could adversely affect our ability to retain and attract customers, and may have a material adverse effect on our results of operations, cash flows and financial condition. Source: 10-k

Light & Wonder, Inc may also suffer significantly from lower expansion of gaming into new jurisdictions. I am talking about both international expansion and expansion in the United States, where legislation is necessary to approve the activities of Light & Wonder, Inc. Lower growth would most likely bring lower revenue growth, which may lead to lower free cash flow and lower implied valuation.

In addition, the expansion of gaming into new jurisdictions can be a protracted process. In the U.S., U.K. and other international jurisdictions in which we operate, governments usually require a public referendum and legislative action before establishing or expanding gaming. Any of these factors could delay, restrict or prohibit the expansion of our business and negatively impact our results of operations, cash flows and financial condition. Source: 10-k

I also think that recession fears or a recession could be a disaster for the company. Gamers may play a bit less once they think that they may lose their jobs. In the last 10-k, management also noted that suppliers may suffer financial trouble, which could be a problem for Light & Wonder, Inc.

In our iGaming business based on a Participation model, our revenue is largely driven by disposable incomes and level of player activity. Unfavorable economic conditions have previously reduced and may later reduce the disposable incomes of end users consuming the services, which could negatively impact revenues for the iGaming business. Suppliers to our iGaming business may suffer financial difficulties and may not be able to offer their services and products, which could restrict the provision of our services and negatively impact our revenues. Source: 10-k

Conclusion

I believe that after the acquisition of SciPlay, Light & Wonder, Inc. will most likely receive a lot of attention in the market, which may lead to better financial valuation. It is worth noting that SciPlay reported growth of close to 40.7% CAGR. I also think that further investments in research and development and further hiring will most likely bring new successful content for iGaming. Finally, I assumed that the average daily revenue per unit will continue to grow north as we saw in the most recent quarterly report. Yes, there are risks from a potential recession in the United States or elsewhere, underdevelopment of the brand, or lower growth of the gaming industry into new jurisdictions. With that, I believe that the stock could trade at a higher price mark.

For further details see:

Light & Wonder: SciPlay And Further R&D Efforts Would Imply Undervaluation