LWLG - Lightwave Logic: Never Trust Commercialization Timelines

Summary

- Lightwave Logic is an interesting company that is putting together methodologies based on its patented material sciences that could be revolutionary for network companies and semiconductors.

- They are using the advantages of non-crystalline and organic compounds that have more stability in harsher operating conditions.

- The problem with them is that they haven't commercialised their products yet, and are still in the process of demonstrating and qualifying their technology.

- With the cost of delays on timelines being higher now than they have been for a while, stay away from LWLG.

Lightwave Logic (LWLG) is certainly an interesting prospect. It is pre-commercial with patents associated to material sciences focusing on the pretty large market of hardware photoelectronic products that have potentially revolutionary advantages over the currently used, inorganic crystalline structures for modulating and affecting electricity and light. With far better price performance characteristics in terms of providing high internet speeds, high volumes of data and energy with less intensive infrastructure, the opportunity is in principle very vast. But LWLG is a total VC style investment. In fact it's much riskier than a typical VC investment - it is very early stage. There's a reason VC is dead right now, and if you're an investor in LWLG, its stock in your portfolio too. With it being a bet on commercialisation timelines, it's best to stay away given cash burn and balances.

A Short Primer

LWLG has lots of patents and is working on products that are based on its own material science, which is more flexible than the key methods for making electro-optic products with inorganic chemistry, so easily contaminated crystals of various types for affecting light, and more resistant than other polymer-based paradigms to more trying environments and higher bandwidth connectivity. Their solutions could be used in the manufacture of components for datacenters like modulators, a product which LWLG is in the process of developing themselves, as well as integrated circuits leveraging this technology which could lead to greater levels of miniaturisation.

Cash Burn and Other Remarks

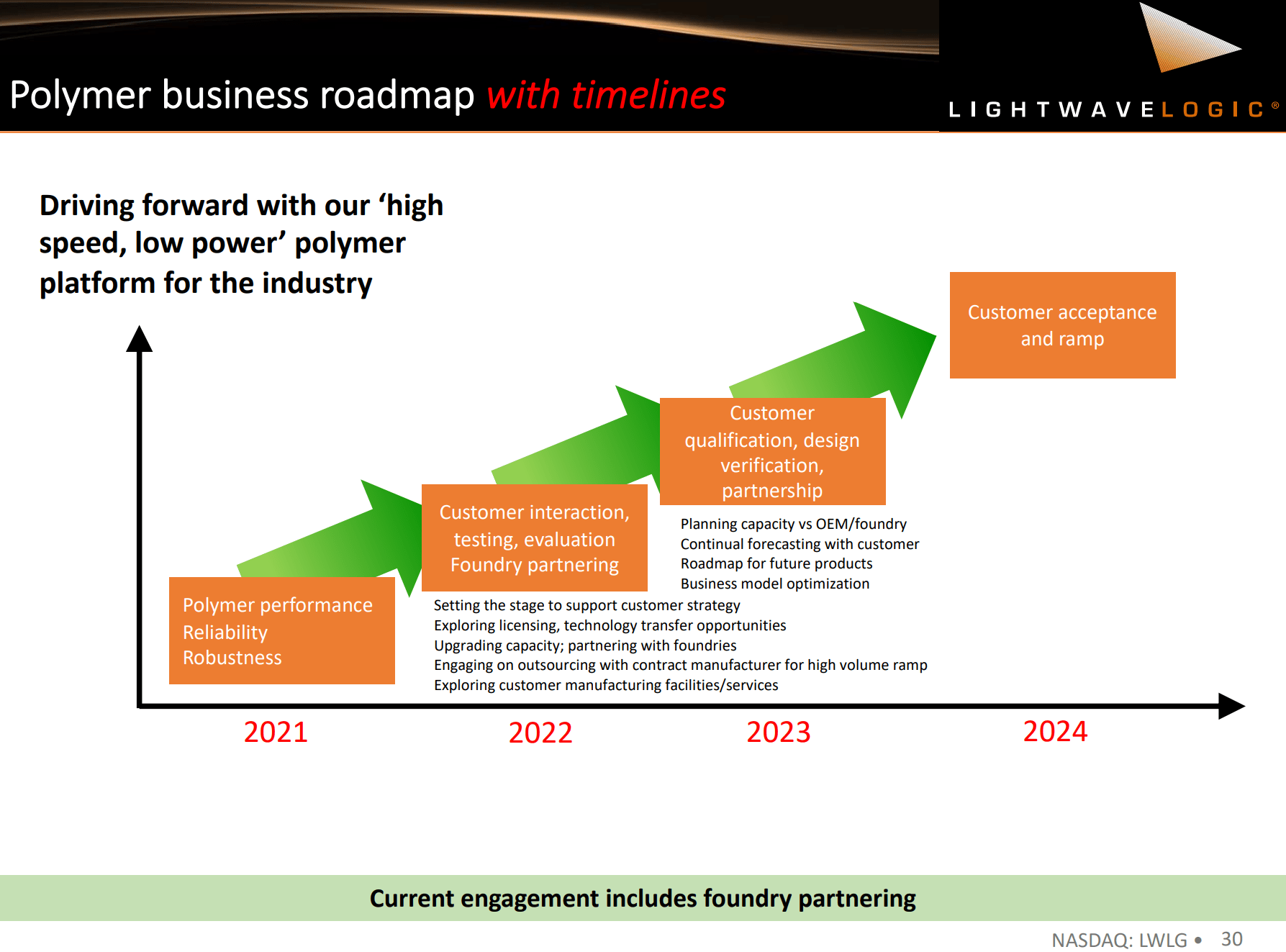

The company has been working with foundries to see if they can demonstrate their technology and implement it within foundry systems. Dr. Lebby, the CEO, reports that they've fabricated good-performing modulators and have gotten somewhere in demonstrating performance of their integrated circuit concepts on silicon wafers, and working with packaging methodologies to start getting closer to manufacturing their products in a typical foundry setting. The concepts they have for how to package their products are helped by a recent acquisition of Chromosol , which has patents for this part of the manufacturing of the products. They are getting patents on fabrications processes that apparently mesh with current set-ups in foundries, and the hope is that this should help to validate their products, and get them closer to being manufactured and shipped. He claims that the performance of their polymers after being applied by foundries has broken records and that they are getting closer to some license agreements in 2023, meaning that they'll have an agreement to both supply the polymers , and then receive a royalty for the use of the polymer in the manufacture of related products, working with foundries that are able to use LWLG polymers in fabrication. 2023 is the year they expect to start working on deciding on how much capacity they need, and how much they are going to outsource to meet their commercial agreements.

{kind=link}

The problem is there's no guarantee that they'll actually come to an agreement, and that foundries are going to be moved to provide capacity for LWLG's products. Moreover, there's a lot that goes into a corporate moving forward to produce a product with LWLG polymers. The idea of licensing is that it puts marketing in someone else's court, and they'd have to be the ones to convince customers that a new form factor is going to be worth putting into datacenters and our communication systems today. There are a lot of unanswered questions, assuming of course that the technology is the real deal, which we aren't capable of determining.

Then there's the matter of cash burn. Being pre-commercialisation there are only costs, and they are running at almost $10 million per year. Cash balances are $25 million , and free cash flow positive operations would be required to stop another equity raise within the next 2 years at the maximum. Dilutions are likely to come in, and because of reflexivity in the stock price, where a lower value for the company means more costly equity financing, there is the risk that the market appetite for VC-style investments remains muted when equity raising needs to happen. While licensing is capital lite, it seems like commercialisation could be far away. An agreement may happen in 2023, but the royalties will take much longer than that, as customers will actually need to start selling products with LWLG's polymers. We have our doubts about when the company might start generating cash - it could still be years, even if an agreement happens in 2023.

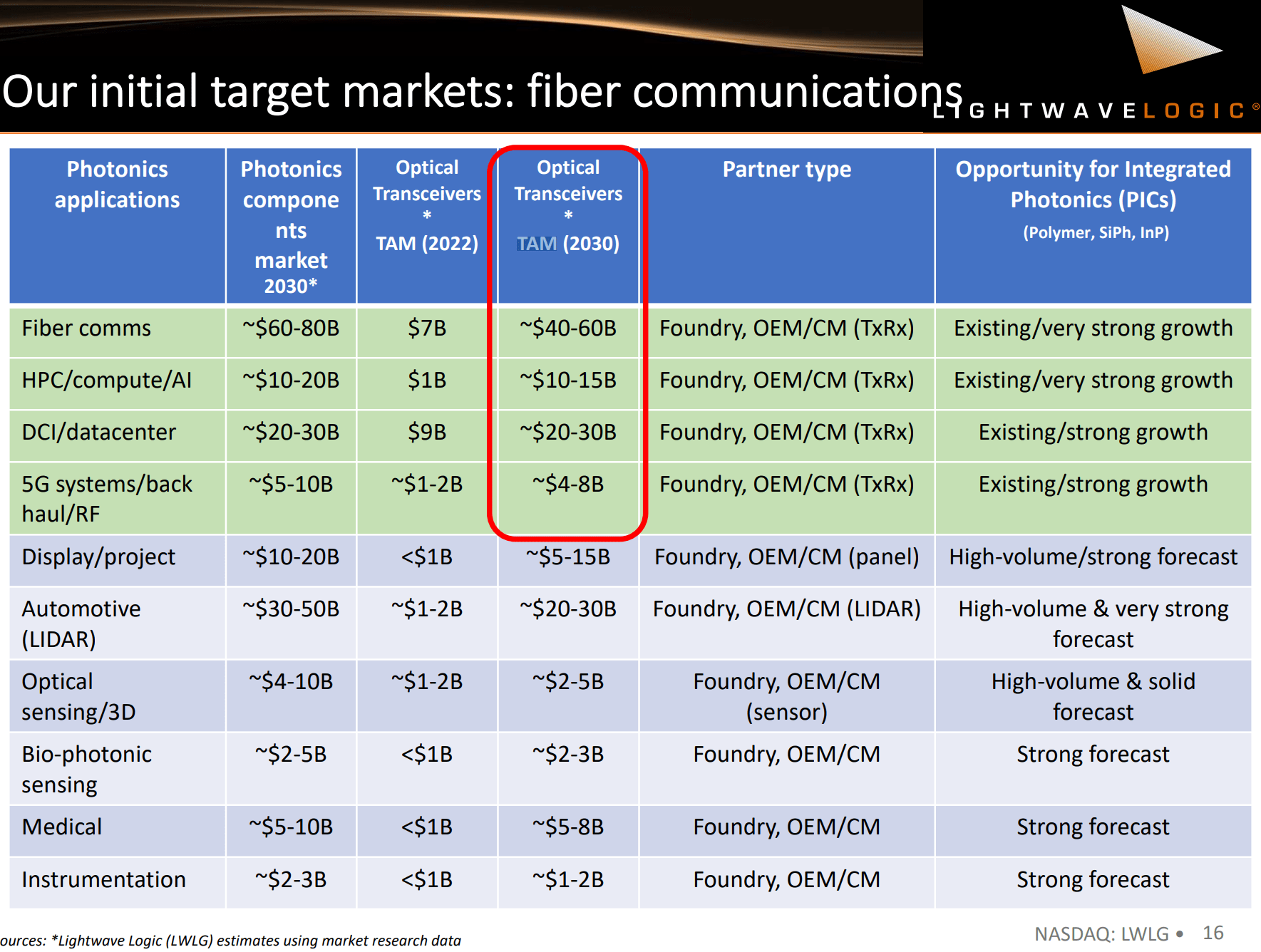

The valuation, considering all this, is actually quite perversely a positive due to reflexivity. With more than $600 million in market value, a major cash balance could be raised with pretty limited dilution, but it's hard to forecast the company's cash needs. If they can license their product at this stage, cash burn may not grow so much beyond now, which is a plus. However, the $600 million valuation also puts a lot of pressure on commercialisation coming quite soon. The benefits of this investment will have to start appearing at some point soon for the current valuation to fairly reflect the risks that an investor today is taking. The TAMs for products that could make use of LWLG's polymers are large, adding up to tens of billions by 2030. A royalty gives them a cut of the revenues there, but the obtainable opportunity might not be more than a few billion dollars even if the product is fully penetrated, maybe $5 billion as a crude estimate. With that being a very tight deadline for LWLG, and still a big risk for the investor, the deal seems weak, especially if the price of LWLG declines around when equity raises need to happen. We'll pass on this.

{kind=link}

For further details see:

Lightwave Logic: Never Trust Commercialization Timelines