LMB - Limbach Acquires Industrial Air: Buy Rating Reiterated After A 180%+ Gain

2023-11-04 01:24:17 ET

Summary

- Limbach Holdings, Inc. has agreed to acquire Industrial Air in an all-cash deal worth approximately $13.5 million, and significant financial benefits are expected.

- The stock has surged by more than 180% since our latest coverage. However, we believe there's more to come as the firm's fundamentals look robust.

- Limbach's price multiples speak volumes, suggesting the stock is grossly undervalued.

- Sure, various risks are embedded in Limbach's stock. Nevertheless, we netted it all out and hold a positive view of the asset.

Limbach Holdings, Inc. (LMB) has agreed a deal to acquire Industrial Air in an all-cash deal at an enterprise value of approximately $13.5 million. We covered the stock back in 2021 , and it is safe to say that our buy rating panned out quite well, as Limbach's stock has surged by 180% ever since. However, we felt it was necessary to update our outlook on the stock given that various material events have unfolded, such as its acquisition of Industrial Air and a recent earnings release.

Pearl Gray's Previous Limbach Rating (Seeking Alpha)

Let's get into a deeper discussion about Limbach Holdings' prospects.

Limbach's Industrial Air Acquisition Debunked

The Deal's Details

Limbach announced on Thursday that it will acquire Industrial Air, a company situated in North Carolina that provides environmental mechanical and air filtration offerings and custom air handling equipment to a range of industrial customers.

Limbach is set to acquire the firm at its enterprise value of $13.5 million, subject to adjustments for working capital. The firm will tap into $7 million of its cash reserve and structure the rest in earn-outs over two years. For those unaware, an earn-out clause in an acquisition means the underlying entity's performance must meet certain benchmarks for the acquisition price to be realized.

According to Limbach, Industrial Air will contribute $30 million in revenue and $4 million in EBITDA annually. Moreover, the acquisition onboards regional exposure in North Carolina, providing Limbach with the necessary latitude to engage in cross-sales.

Further, Limbach thinks the acquisition will enhance its ODR segment (a business that provides maintenance and servicing to HVAC, plumbing, or electrical systems).

In essence, Limbach suggests the deal adds financial benefits and non-financial synergies.

Our Take

To our knowledge, Limbach's Industrial Air acquisition holds no premium, which is rare in an acquisition unless you're looking at a distressed buy. Therefore, our first instinct tells us merger arbitrage will not be present here, phasing out a temporary stock price slump.

Furthermore, from a fundamental vantage point, $4 million in additional annualized EBITDA boosts Limbach's existing 5-year average EBITDA of $22.78 by 17.56%, which is significant.

It's difficult to determine the fair value of the deal, given that Industrial Air is a private entity. However, an eyeballed valuation suggests the firm could be worth $20.6 million if incorporated into Limbach's framework. Of course, the cash outflow will have to be accounted for if you want to net it all out.

Side note: The table below pertains to the target company alone and does not consider bilateral cash movements that could influence the EV.

Author's Work, Data from Seeking Alpha & Limbach

In addition to the above, I drafted up the target's price multiples and compared it to Limbach's for your convenience. Notice that the EV/Sales is slightly weaker, but the EV/EBITDA is better. Moreover, it must be considered that the embedded synergies will take time to pan out.

Author's Work, Data from Limbach & Seeking Alpha

As mentioned before, we think the acquisition will be beneficial in terms of regional representation and the depth that it adds to Limbach's AOR business. Moreover, the company onboard intellectual capital as its founding in 1964 means it hosts various veterans that can provide critical input to Limbach during the transition phase and thereafter.

Other Events

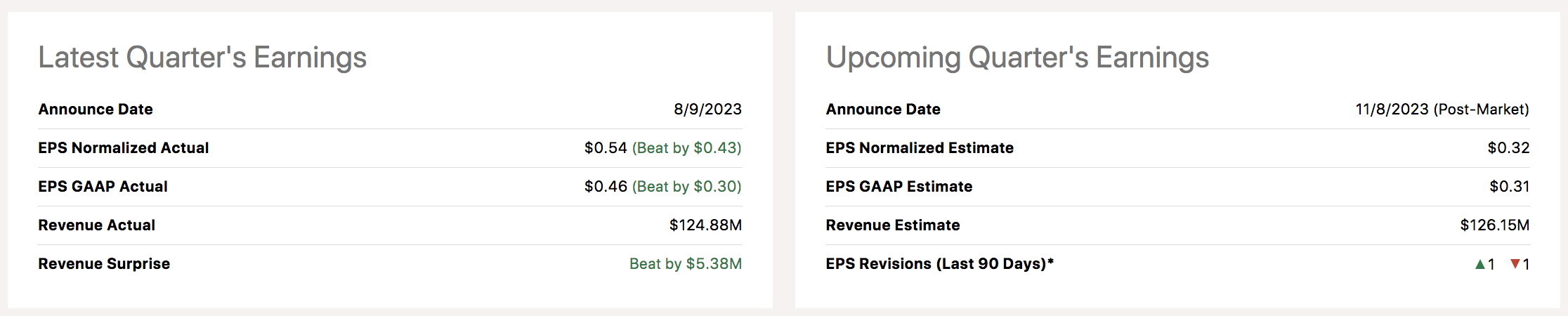

In another recent event, Limbach strolled past its second-quarter earnings estimate. The firm achieved $124.88 million in quarterly revenue coupled with earnings-per-share worth 46 cents.

{kind=link}

Impressively, the firm's gross profit margin increased by 22.8% due to working directly with building owners in ODR, which has the set segment's gross profit margin between 25% and 28%. I cannot comment on whether structural matters will increase the firm's broad-based gross margin. However, we think lower broad-based inflation will enhance the company's income statement even further, assuming it sustains its product pricing structure.

I mentioned the direct building approach of Limbach in the previous paragraph. However, I would like to re-emphasize this value proposition as it allows the firm to achieve smoother revenue with subscription-esque sales with owners while allowing for additional capacity in ancillary projects instead of only relying on prolonged core contracts.

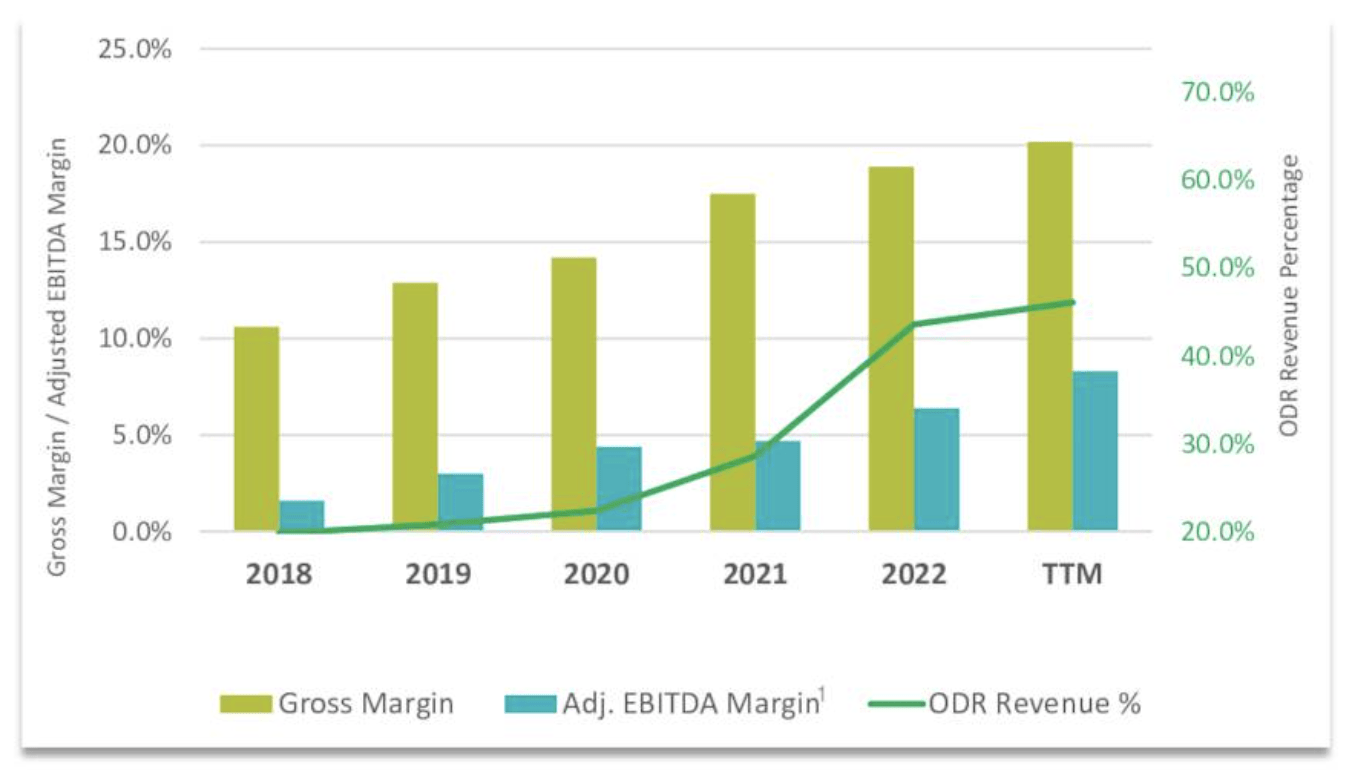

As visible in the following diagram, Limbach has extended its EBITDA margin in every financial year since 2021, which is an impressive feature considering the exorbitant input costs that plagued the economy during late 2021 and the entirety of 2022.

{kind=link}

As illustrated with the Industrial Air acquisition, Limbach's management has the ability to spot a good deal, which is key because it has a growth-by-acquisition business model. In fact, it has a 70% hit rate when it comes to its targets and has onboarded significant synergies via other acquisitions. Moreover, the depressed M&A environment allows cash-heavy businesses (in the context of LMB's acquisition sizes), such as Limbach, to capitalize on undervalued opportunities and unlock substantial value when the targets are incorporated under its umbrella.

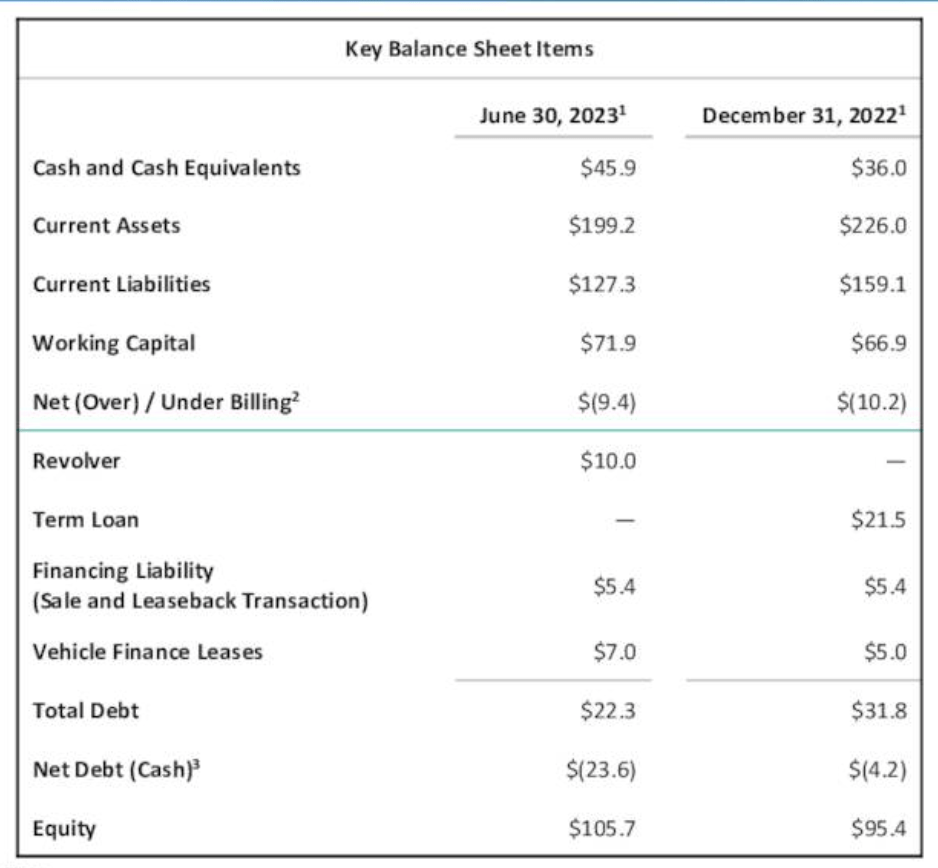

A quick look at Limbach's balance sheet confirms my claim that it is liquid and has plenty of residual value in-store via equity. Moreover, Limbach repaid its term loans this year, meaning it isn't burdened by debt apart from a $50 million revolving credit facility that it has access to in case of emergency. Therefore, we would not be surprised if the acquisition spree continues, whereby Limbach will likely, In turn, add to its shareholders' residual value.

{kind=link}

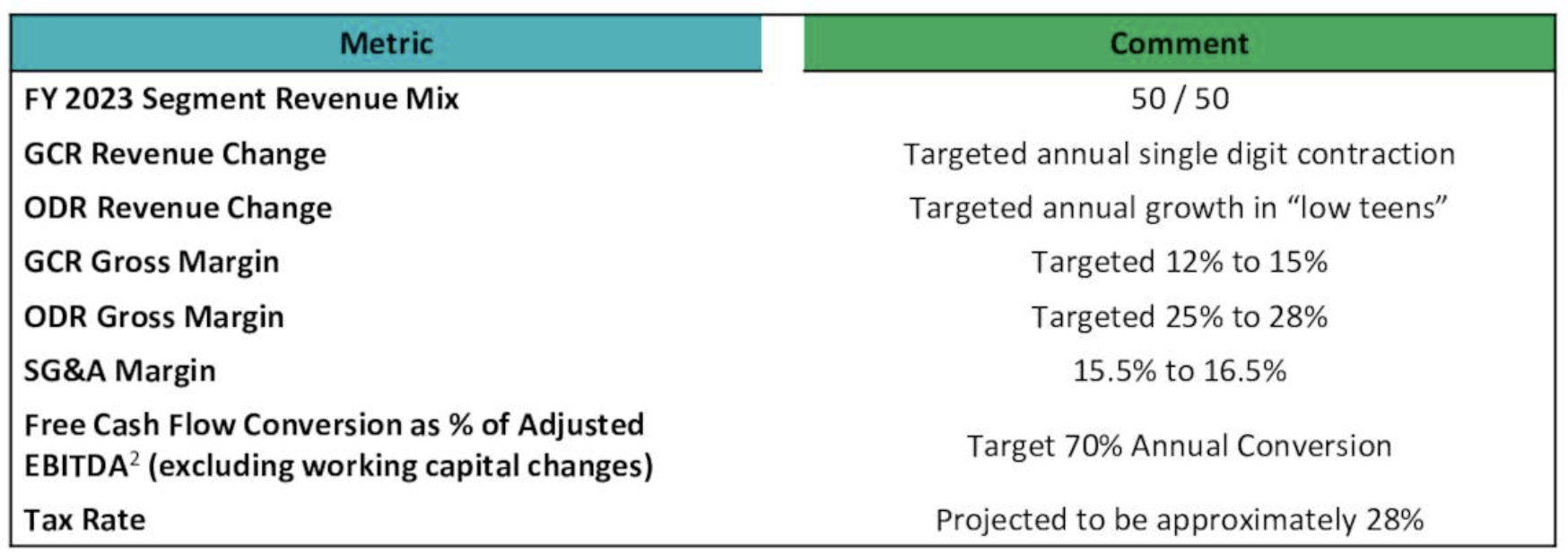

Lastly, Limbach's guidance speaks volumes. As previously mentioned, the company is receiving significant support from its ODR activities. In our opinion, a broad-based cooldown in topline growth will occur at some stage, but Limbach's general fundamentals imply that secular growth isn't out of the question.

{kind=link}

Valuation

A relative valuation shows that Limbach's forward P/E is a tad high, as it sits about 11.51% above the sector median and just looks high in general. However, dialing in on the PEG illustrates that Limbach's earnings-per-share is growing at scale, which, in our view, more than justifies Limbach's high trailing and forward P/E ratios.

I outlined Limbach's EV multiples earlier in the article, and they are quite superb if compared to their sector peers. We think the EV/Sales multiple of 0.65x speaks volumes as it shows that the market has yet to price the firm's top-line progress.

| Metric |

| Value |

| Forward P/E |

| 22.15x |

| Trailing P/E |

| 21.63x |

| PEG TTM |

| 0.23x |

Source: Seeking Alpha

Risks

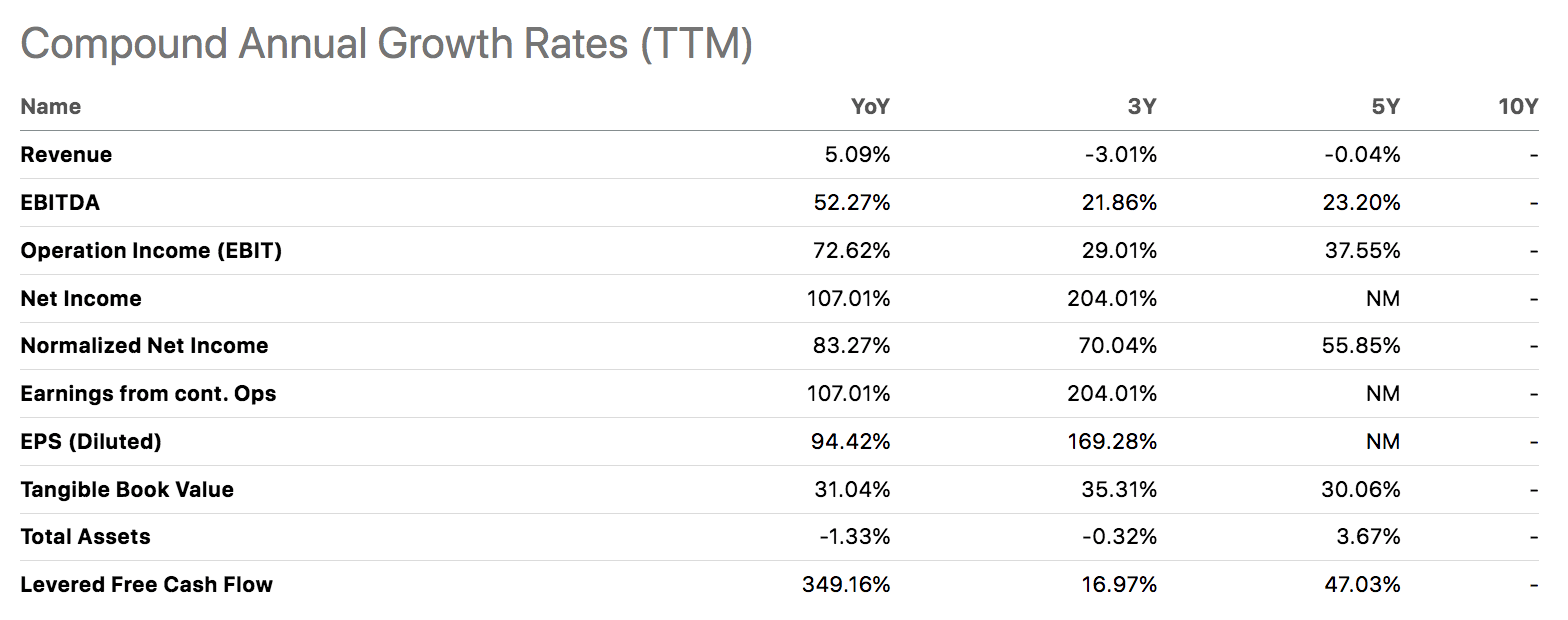

Although Limbach's prospects seem intact, it has a few risks. One of those risks is that its longer-term compound annual growth rates are slightly depleted. Much of it is due to the impact COVID has; nevertheless, secular growth does remain a concern if the company repeats its past economic cycle.

{kind=link}

Furthermore, macroeconomic concerns in the U.S. can deteriorate the company's prospects as building owners, in particular, look to cut back on costs as much as possible to deflect any unforeseen economic headwinds. We think the economy is in a slowdown period that could see it inflict damage on the industrial services industry and Limbach alike.

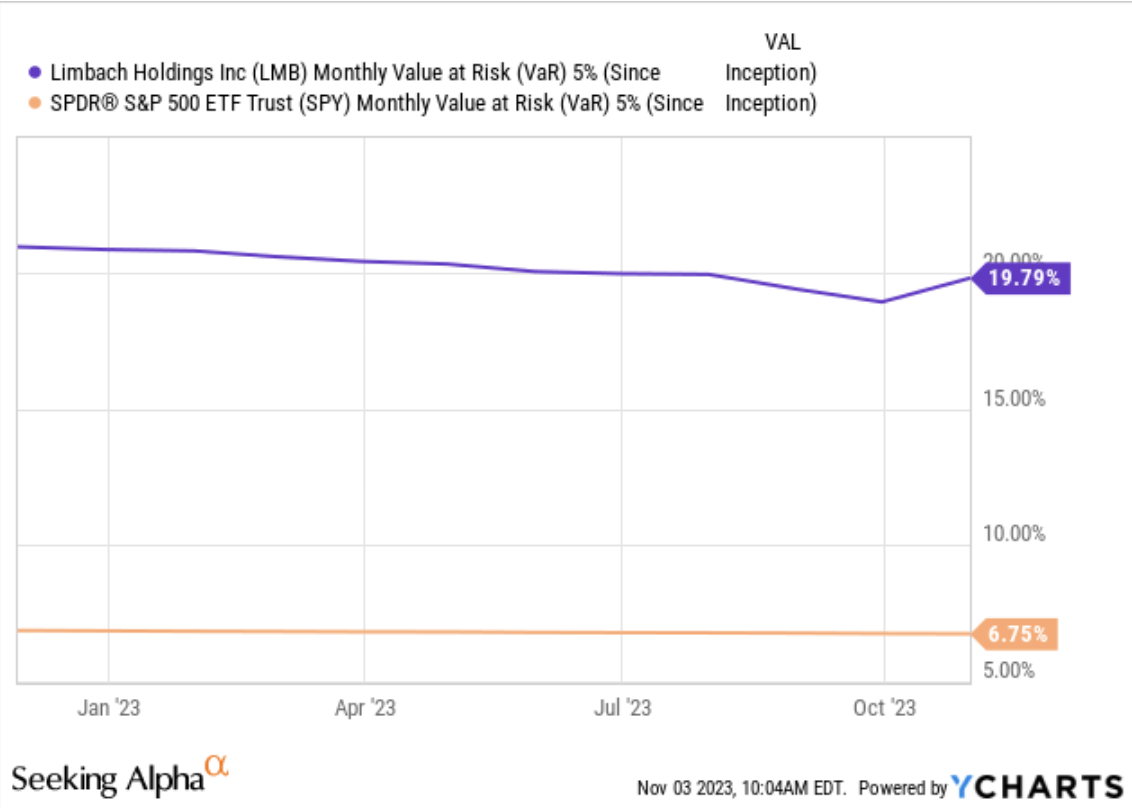

Lastly, Limbach Holdings' stock has a substantial Value-at-Risk figure, meaning it tends to shed a lot of value in tail-risk events. Thus, including the stock in one's portfolio will likely raise your overall risk exposure.

{kind=link}

Final Word

Our analysis shows that Limbach's prospects remain intact after a more than 180% surge since our latest coverage. Moreover, the firm has struck terms on an acquisition that we believe will be accretive.

Furthermore, an analysis of Limbach's price multiples implies that its stock is grossly undervalued and ready to rumble.

Consensus: Buy Rating Assigned

For further details see:

Limbach Acquires Industrial Air: Buy Rating Reiterated After A 180%+ Gain