LMB - Limbach: Brace For Weakness

2023-10-02 02:25:34 ET

Summary

- Limbach's stock has gained over 22% since my first article about the stock went live, substantially outperforming the broader market.

- The company's recent earnings showed impressive revenue growth and margin expansion.

- However, the challenging macro environment, with higher interest rates and expected revenue decline, leads to a downgrade to "Hold".

Investment thesis

My first bullish thesis about Limbach ( LMB ) aged exceptionally well. The stock gained more than 22% since mid-July, while the broader market declined by about 5%. A lot has happened within the last three months, and today, I want to update my thesis in accordance with the evolving environment. While the valuation still looks very attractive, I think that from now on, the challenging macro environment with interest rates likely to be staying higher for longer will weigh on the stock price. My analysis also suggests that revenue growth is expected to decelerate in the upcoming quarter and will likely decline by more than 10% in the last quarter of the fiscal year. The company's profitability metrics and the balance sheet are strong enough to stomach these challenges, but I think that in the near term the stock price is likely to suffer. All in all, I downgrade my rating for LMB to "Hold".

Recent developments

The latest quarterly earnings were released on August 9, when the company significantly outnumbered consensus estimates. Revenue demonstrated a solid 7.6% YoY growth, which looks impressive in the current harsh environment. The bottom line also demonstrated a solid dynamic, with the non-GAAP EPS expanding from $0.08 to $0.46.

Seeking Alpha

The increase in the adjusted EPS was impossible thanks to a notable margin expansion. The gross margin has improved by more than four percentage points YoY, and so did the operating margin. Solid profitability metrics enabled the company to generate quarterly levered free cash flow [FCF] of $16.7 million. This helped to improve the balance sheet, which looks solid to me. The company is in a net cash position and the leverage ratio is very prudent. Current liquidity metrics and the covered ratio indicate solid near-term liquidity.

Seeking Alpha

The upcoming quarter's earnings are scheduled for release on November 13. Consensus estimates forecast quarterly revenue at $126 million, which indicates a 3% YoY growth, a notable deceleration of the topline growth. The bottom line is expected to be almost flat with a slight adjusted EPS decrease from $0.34 to $0.32.

Seeking Alpha

Earnings consensus estimates expect almost no revenue growth for the full fiscal year, with a mere 0.9% increase. That said, the Q4 revenue of the fiscal 2023 is highly likely to demonstrate a significant YoY drop. In Q4 of the last fiscal year, revenue was at $143.5 million, while my calculations suggest that the last quarter of the current fiscal year will generate $129 million in sales. This indicates a more than 10% YoY revenue decrease.

Author's calculations

The expected deceleration in revenue looks reasonable given the overall near-term challenges for the broader economy. Interest rates are still at their highest since the beginning of the century, which weighs on the intensity of economic activity. And Fed Chair's latest press conference suggests that the door is still open for more hikes and interest rates are likely to stay higher for longer. That said, I expect the next fiscal year to be tough for the revenue side of the business as well. At the same time, the bottom line expectations are far brighter, with a 116% expected increase in the EPS for the full fiscal 2023. It is a good sign for investors, together with a strong balance sheet. The improving bottom line and a solid financial position mean the company has a wide margin of safety to weather the storm.

Valuation update

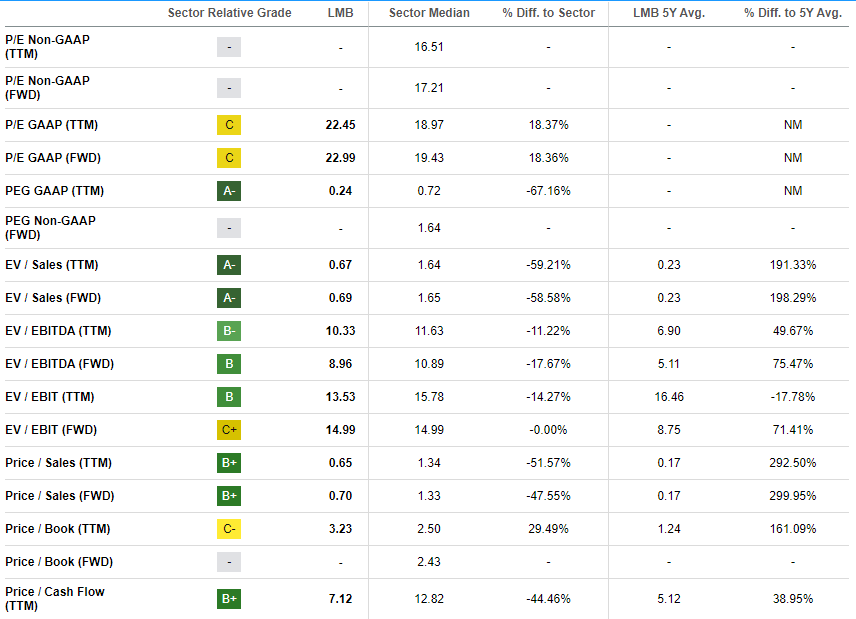

The stock price almost tripled year-to-date, significantly outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a decent "C+" valuation grade because most multiples are still substantially lower than the sector median. On the other hand, most of the current multiples are significantly higher than the company's historical averages.

{kind=link}

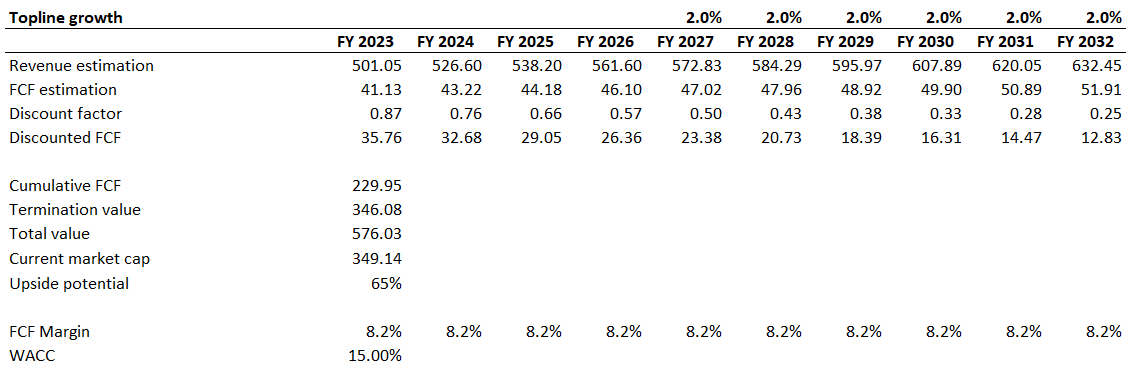

While multiples analysis demonstrates a very mixed picture, I also want to simulate the discounted cash flow [DCF] model. Last time, I used a 14% discount rate; today, I want to raise it by one percentage point to incorporate the Fed's hawkish stance. Revenue consensus estimates are available up to FY 2026, for the years beyond, I project a super-conservative 2% CAGR. I use a constant FCF margin of 8.2% for the whole next decade, which is an ex-SBC TTM level.

{kind=link}

According to my DCF simulation, the stock is still substantially undervalued. The business's fair value is approximately $576 million, indicating a massive 65% upside potential for the stock. That said, the stock's fair price is close to $52. But, it is crucial to remember that it might take several quarters before the stock approaches its fair value, especially given the current weak sentiment in the stock market.

Risks update

The construction industry is highly cyclical, meaning it is significantly dependent on the health of the broader economy. While the recent quarterly economic data suggests the U.S. economy is still expanding at a decent rate, I think that the recession is probable in the foreseeable future. I think that Federal Funds rates will remain high for the next year because the fight against inflation is still far from over. Oil prices are close to turning to triple digits again, which is the major catalyst for the inflation growth. There are multiple reasons why I feel bullish about oil prices, which I described in one of my latest articles. That said, the Fed still has a job to be done to make the inflation capitulate. And I see the tight monetary policy to be the only option for Mr. Powell and his colleagues to do the job. That is likely to be a big negative factor to drag down the construction industry in the near term.

I would also like to mention the company's massive year-to-date rally as a risk. Amid the current uncertain environment, I think that many LMB investors are tempted to realize their massive profits and start selling off the stock. That will also not help the stock price to appreciate in the near term.

Bottom line

To conclude, I downgrade LMB from "Strong buy" to "Hold". While I like the company's massive profitability metrics expansion this year, the tough environment is highly likely to weigh on the topline growth in the nearest quarters. The increasing cost of capital will continue to press on the economic activity, which will ultimately hit near-term prospects of the whole construction industry. The valuation still looks very attractive, but some factors tell me that the gap between the current stock price and the fair value will not close fast.

For further details see:

Limbach: Brace For Weakness