LMB - Limbach: FOMO Is Not Going To Get Me Profit-Taking Might Ensue

2023-12-21 03:19:28 ET

Summary

- Limbach Holdings' top-line growth is low; however, margins are improving.

- LMB has a strong financial position with low debt levels and no risk of insolvency.

- The management is improving profitability and efficiency, but sales growth is not impressive. Acquisitions and expansion opportunities are expected to continue.

Investment Thesis

After rallying almost 300% in the last year, I wanted to take a look at Limbach Holdings ( LMB ) to see if it would still be a good time to jump on the train for the long run. Unfortunately, with very low top-line growth and even with improving margins, the company is not an attractive buy at these prices, therefore I am assigning a hold rating for now until we see a pullback or an improved top-line growth.

Financials

As of Q3 '23, which is as of September 30th, the company had around $57.5m in cash and equivalents, against $19.5m in long-term debt. This is a great position to be in, because the debt levels are very low in my opinion, and can easily be covered by the outstanding cash pile. If we want to make sure it is not an issue, we can look at three main metrics that I like to use to determine this. All three solvency ratios below are flagged green in my model, which means the company is using leverage smartly and is easily manageable. Debt-to-Assets ratio is within the limits of 0.3 to 0.6. Debt-to-equity is well below the acceptable ratio of 1.5. Furthermore, the interest coverage ratio is over 6x, which means EBIT can easily cover annual interest expenses on debt. For reference, many analysts consider a ratio of 2x to be sufficient, while I think a 5x is much safer as it allows for more fluctuations in the business operations when the company's performance might be subpar. It is safe to say the company is at no risk of insolvency.

{kind=link}

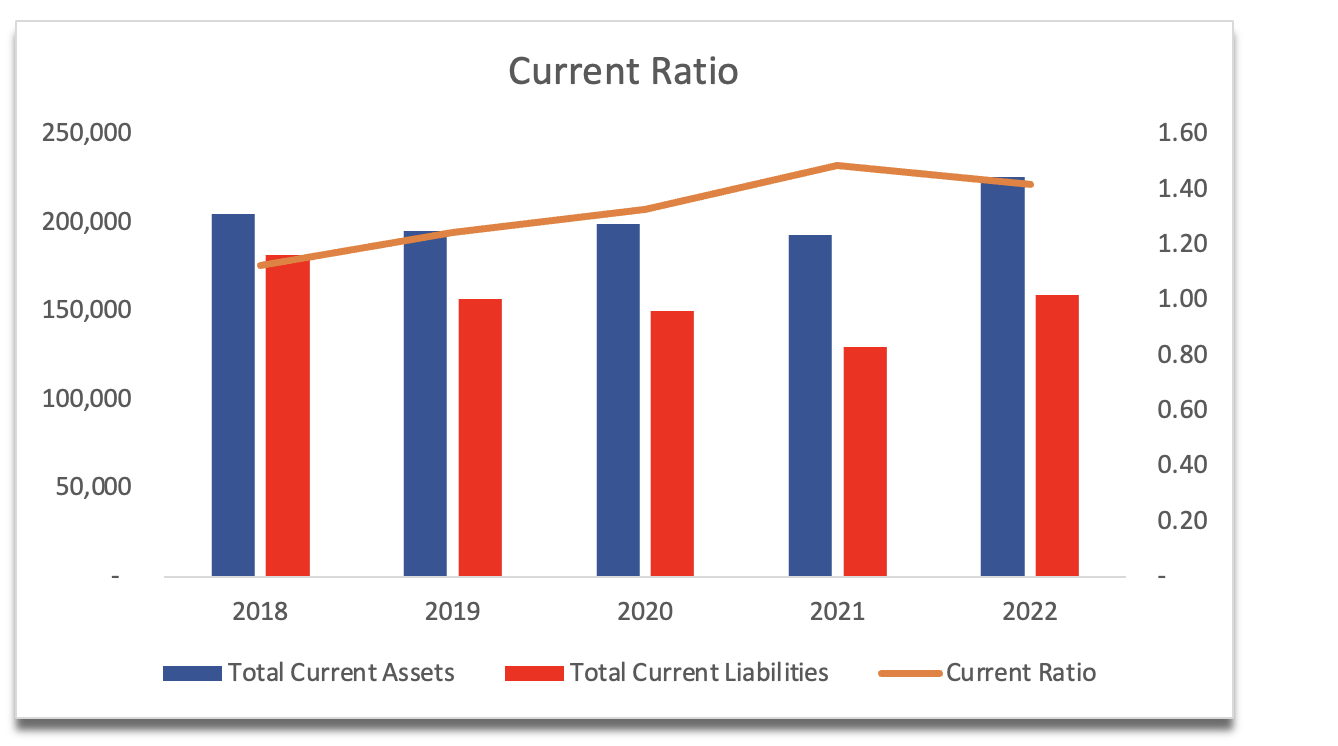

LMB's current ratio has been steadily improving and is well over 1, which means the company has no issues paying off its short-term obligations. In the latest quarter, the current ratio improved to around 1.5, which is right where I like it to be. LMB has no liquidity issues.

{kind=link}

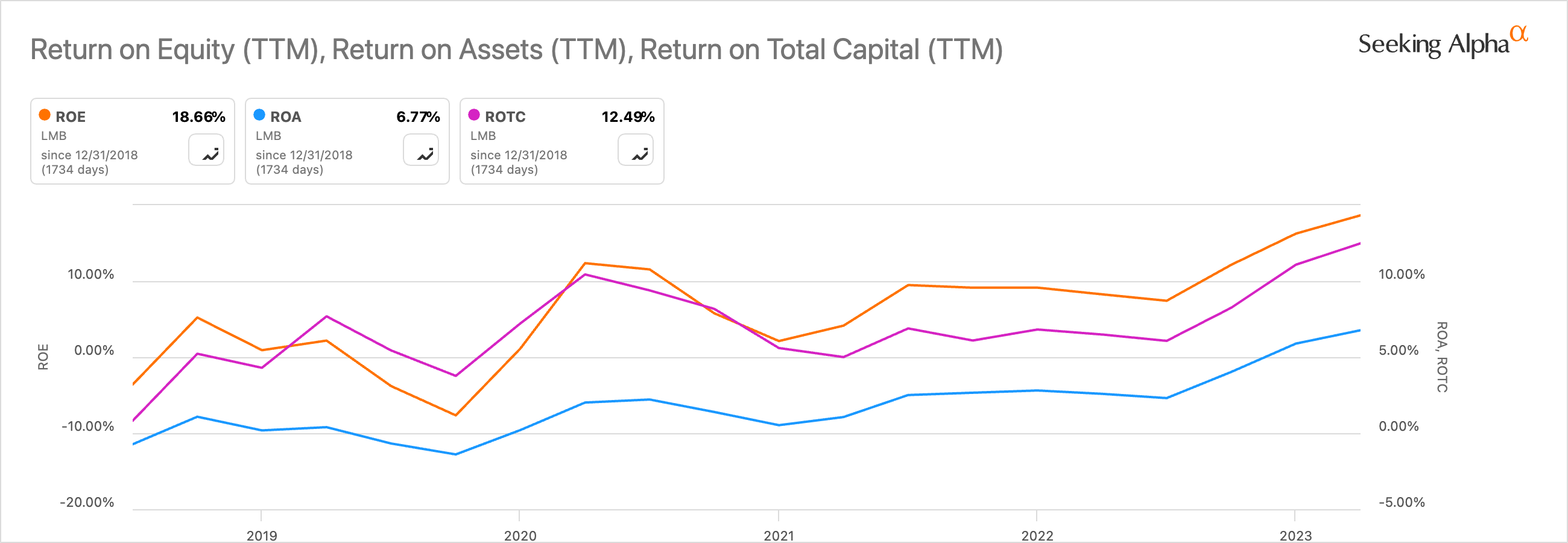

In terms of profitability and efficiency, the company has been steadily improving over the last 5 years, which is a good sign. The management is creating value for shareholders and is being efficient (somewhat efficient) with the company's assets. I would like to see ROA and ROE much higher than it was previously, which it looks like it will be for FY23.

The same can be said about the company's ROTC or return on total capital. It has been improving over the last while, which means that the company is gaining some competitive advantage. Furthermore, this tells us that the management can allocate capital towards profitable projects.

Profitability and Efficiency improving (Seeking Alpha)

{kind=link}

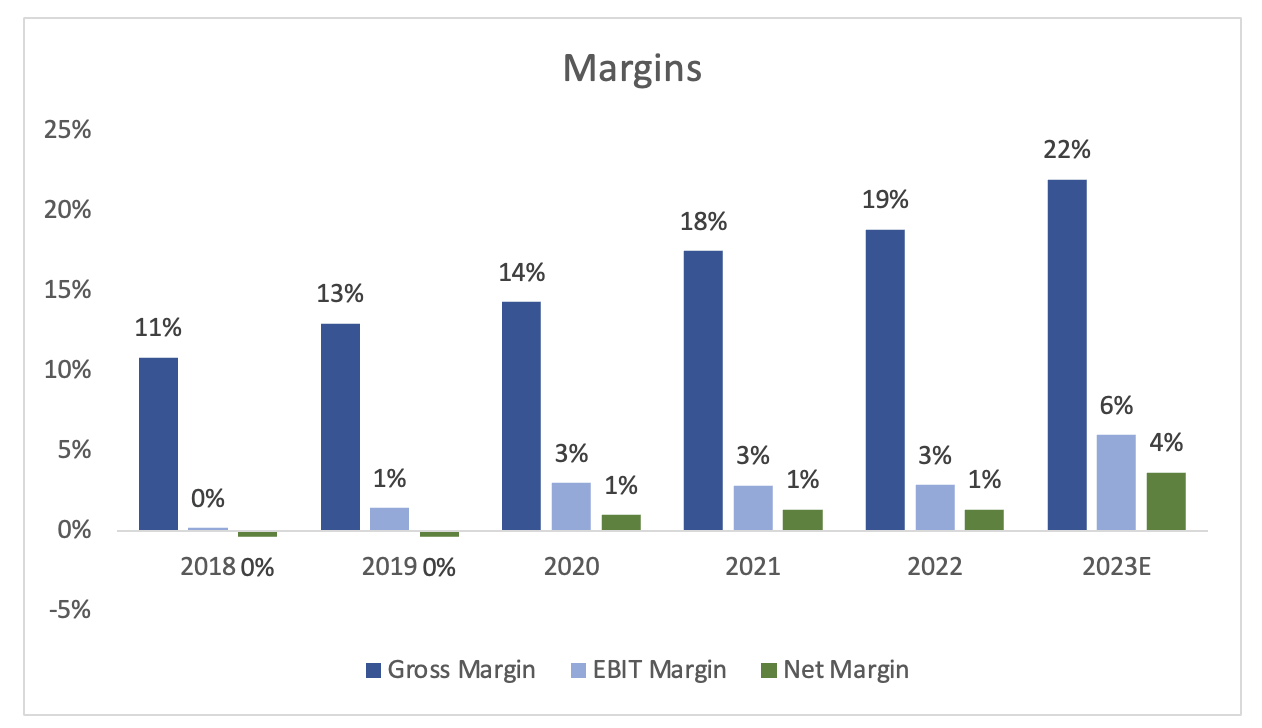

Speaking of efficiency and profitability, the company's margins have been steadily increasing over the last 5 years; however, they were very tight. In the latest quarter, gross margins have improved even more, as the company becomes more efficient. Comparing y/y COGS, we can see the costs reduced slightly while revenues went up. The company is becoming much more efficient and very rapidly. The management seems to know what they're doing and knows their company well to find where to cut costs and execute improvements.

Margins continue to improve (Author)

{kind=link}

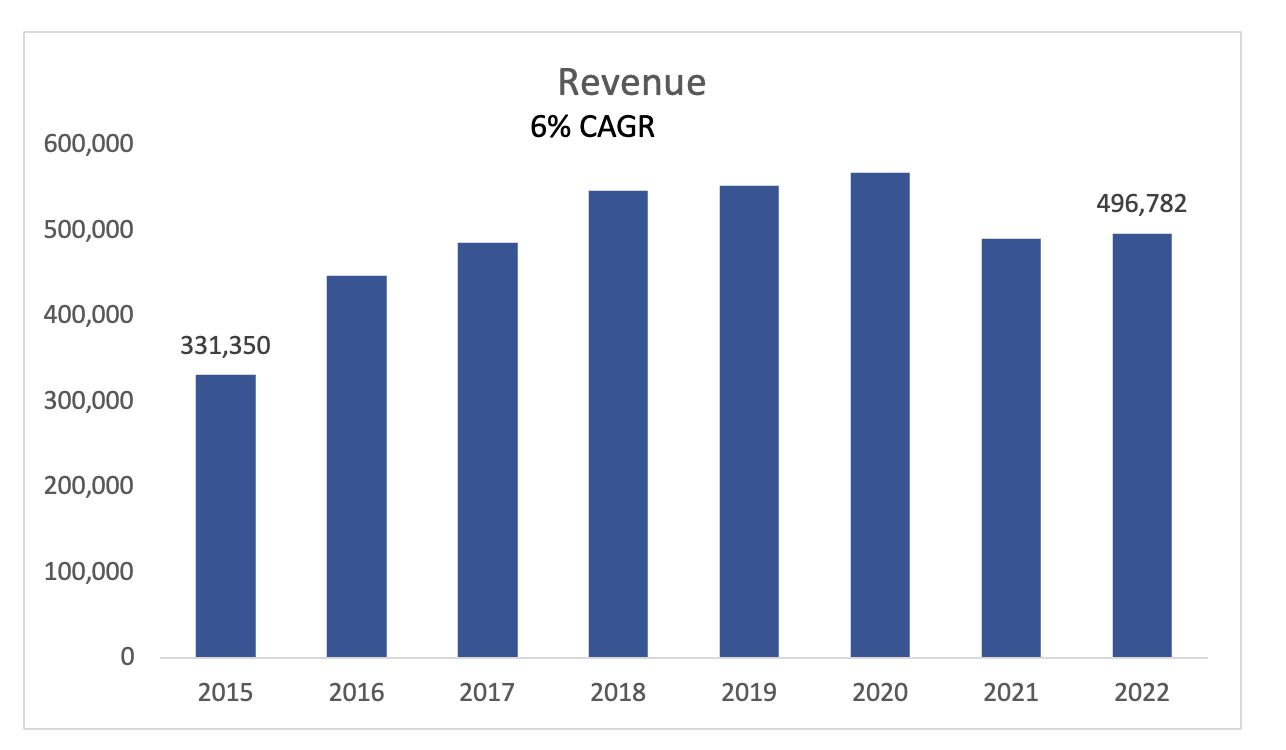

Over the last while, the company managed around 6% CAGR of top-line growth, which is not an outstanding pace, but as long as the company can improve efficiency, sales growth is not the most important thing, however, it may deter many investors who are looking for exciting opportunities and judge a company by its top-line growth.

{kind=link}

Overall, I am very impressed with the company's rapidly improving profitability and efficiency, even if sales are not as impressive as some other companies. The company has a decent balance sheet with very little risk, and the management seems to know what they're doing. If the company continues on this trajectory going forward, I could see the share price continue to climb up with justification.

Comments on the Outlook

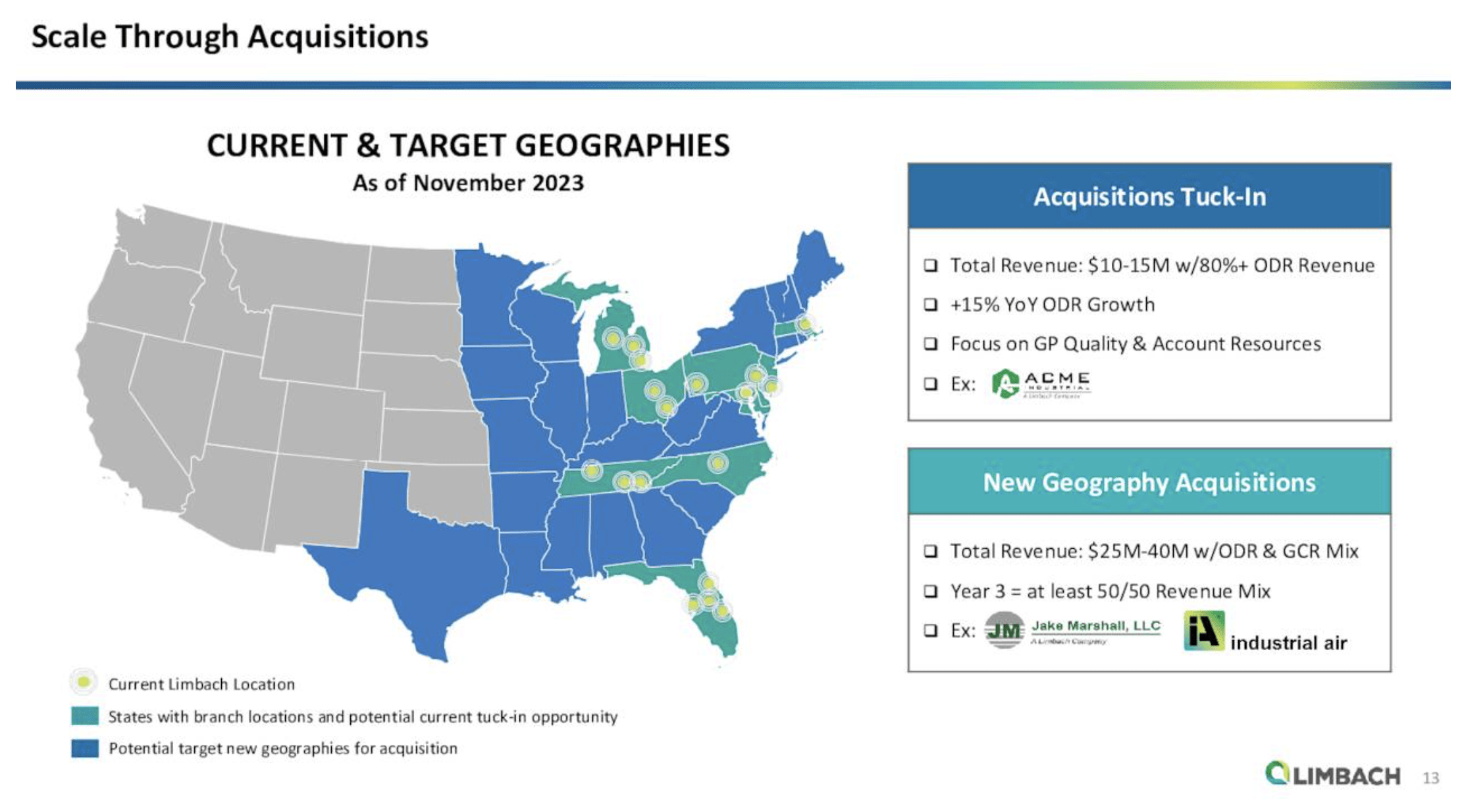

LMB has been on a tear recently with acquisitions, which seem to be working quite well. I believe the company should continue on the same path and acquire more companies to expand its footprint across the US. I believe the management is very capable of finding the right fit that will integrate with the company spectacularly. Furthermore, the company has a lot of opportunities to expand across the US, so I would expect the acquisitions to continue, and we'll see the company continue to scale.

Potential of acquisitions (LMB Investor Presentation)

{kind=link}

The management is doing a great job at improving the company's efficiency and profitability over the years as seen in the metrics above. As I mentioned before, the company doesn't necessarily need to grow its top line like a tech company. As long as it has steady growth while making improvements on the bottom line, the company will continue to create value for its shareholders going forward.

There are macroeconomic risks to consider here too. The company is very well diversified in its core markets, so I would expect the demand for its products to be quite resilient.

Valuation

I approach valuation with a conservative mindset just to give myself that little bit of extra margin of safety. For revenues, I went with around 4% CAGR over the next decade, which can be easily beat, however, seeing that the company grew very little in the last 3 years, a 4% CAGR is justified in my opinion. To cover all my bases, I also included a conservative and an optimistic case. Below are those assumptions with their respective CAGRs.

{kind=link}

For margins and EPS, I decided to improve gross margins but a little less than what we saw in the latest quarter just to give myself even more room for error. Below are those assumptions. Note the continual improvement over time, which I think is very reasonable.

Margins and EPS Assumptions (Author)

{kind=link}

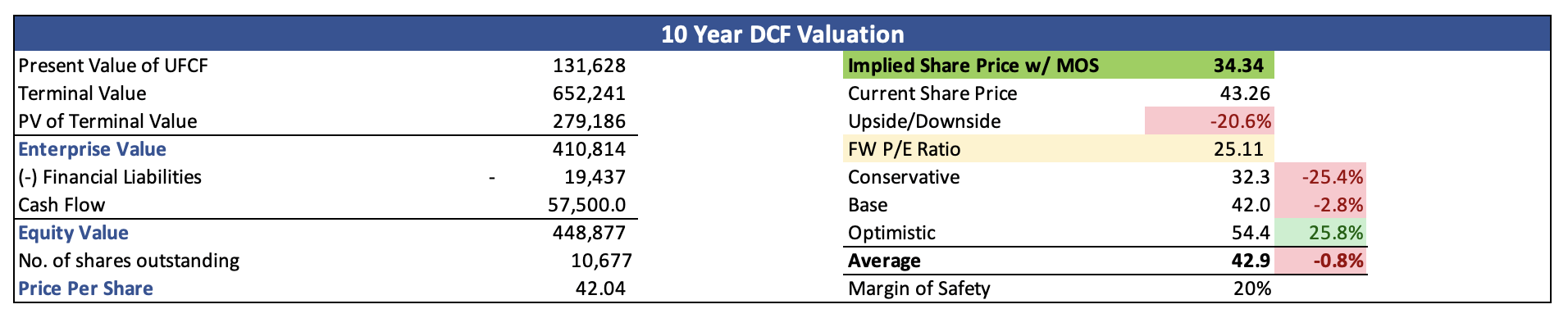

On top of these assumptions, I decided to go with the company's WACC of 8.8% as I think this is a high enough discount for the DCF analysis. Furthermore, I went with a 2.5% terminal growth rate. Lastly, just so I could get a good night's sleep knowing that I bought a company at a discount or at least a fair price, I am adding another 20% margin of safety to the intrinsic value calculation. With that said, LMB's intrinsic value and what I would be willing to pay for it is around $34 a share, which means the company has passed my PT and it is not an ideal time to start a position right now.

{kind=link}

The company's valuation grade on Seeking Alpha is currently sitting at a C+, which ties in with my hold rating as I believe the company is slightly overvalued and it would not be a good time to jump on board right now.

Valuation Grade (Seeking Alpha)

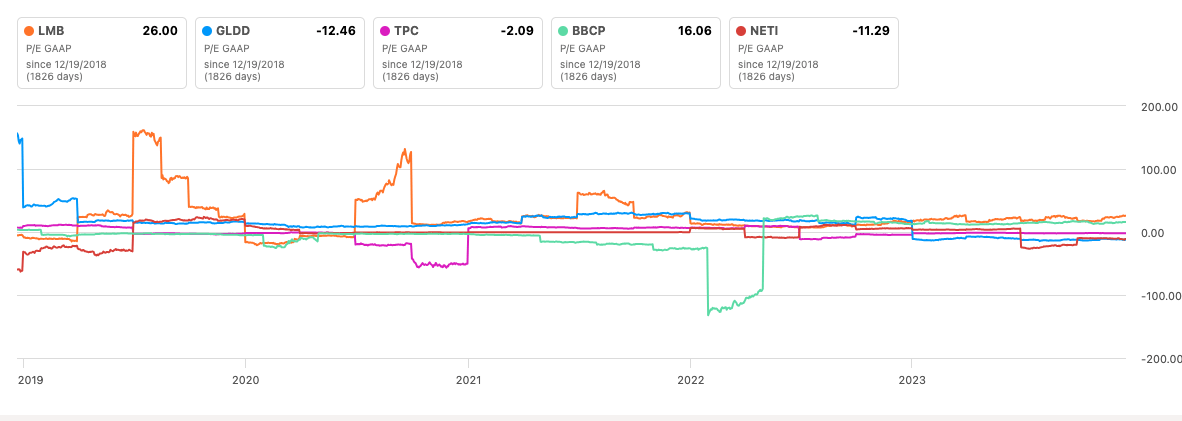

The company's GAAP PE is also above the sector median, which makes me even more cautious.

PE Comparison to sector (Seeking Alpha)

The company doesn't mention specific competitors but if we look at the companies that Seeking Alpha suggests, we can see that over time, LMB has seen its PE ratio fluctuate quite a bit, while the rest of the peers (except for BBCP are still GAAP unprofitable). It looks like the spikes have normalized, however, the company was trading below a 20 PE ratio for most of the FY22 and FY23 so far, which may be hard to see from the image below because of those large spikes.

{kind=link}

Closing Comments

I will not be giving into FOMO and will avoid the company until it comes down closer to my PT, or the company manages to improve its earnings dramatically. Both are very likely, however, after a 300% increase in stock price in the last year, I can't help but wonder if there will be some people who will take some profits on any negatively perceived news, for example, a miss on the next earnings. I feel there will be some investors who will be looking for any reason to take profits off the table.

I am going to wait until something changes, either the share price comes down or earnings improve further because right now it feels like a gamble and giving into the fear of missing out and that is not the way to invest. I missed the run-up before, but I will have the company on my watchlist with a price alert closer to my PT and see how the company's story develops going forward.

For further details see:

Limbach: FOMO Is Not Going To Get Me, Profit-Taking Might Ensue