LMB - Limbach Holdings Can Thrive In A Recession

2023-04-25 09:33:25 ET

Summary

- Limbach is achieving its goals; owner-direct revenue is growing, margins are improving, and the company is generating ample cash flow.

- At its current pace, the company is on track to be a multi-bagger in the next three to five years.

- Will a recession in 2023 or 2024 derail Limbach's growth trajectory? I think the answer is no; a recession might even act as a tailwind for the company.

- In this article, I revisit the LMB investment thesis and highlight why I think the company will thrive, even in a recessionary environment.

[Limbach Holdings] doesn't have to hit consecutive home runs to reach a $30 share price; 12% revenue growth in the ODR segment, declining GCR revenue, no margin expansion, and modest multiples are enough to make the company a multibagger over the next five years " - Me, in my last Limbach article

Limbach Holdings ( LMB ) remains a multibagger in the making. The company's stock price is up 130% since my last article was published and I think it is likely to double again in the next 3-5 years. LMB is growing its owner-direct relationships (ODR) at an accelerated rate, improving its general-contractor (GCR) margins, and shoring up its balance sheet for future acquisitions. In this article I will update my LMB investment thesis and highlight why I think the company will thrive in the years ahead, even in a recessionary environment.

Company Updates

I am going to assume that readers are already familiar with LMB and the investment thesis I laid out in my previous articles. With that in mind, there are a pair of important updates to highlight. First, LMB has a new CEO. Longtime CEO Charlie Bacon has stepped down from the role and passed it on to Michael McCann, the company's Chief Operating Officer. McCann has worked closely with Bacon to focus the company on growing ODR revenue, and I expect the long-term plans for LMB to remain the same after the transition.

Second, LMB adjusted their 2023 (and beyond) projections on the last company conference call. Revenue expectations were increased to between $490mm and $520mm, with revenue evenly split between the ODR and GCR segments. This increase implies 16% growth in ODR revenue. I was also pleased to see that management was comfortable raising GCR segment margin expectations to a range of 12%-15% (up from 12%-13%). As promised, LMB is growing ODR revenue, improving GCR margins, and generating positive EBITDA and cash flow.

Progress Towards the Investment Thesis

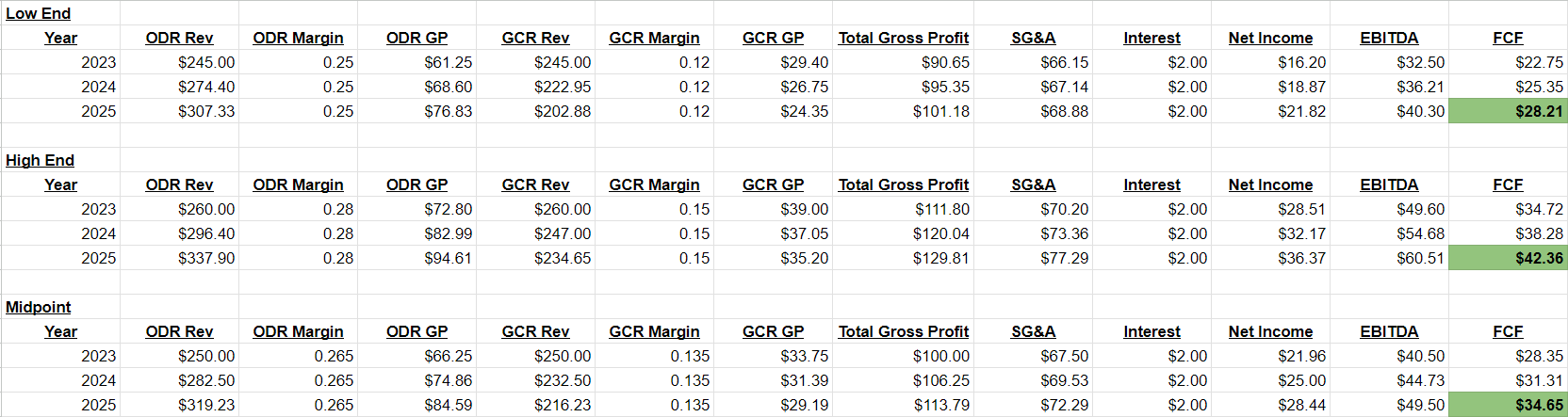

I have updated and expanded upon the model I presented in my previous article. I incorporated management's 2023 guidance ( source ), added a free cash flow estimate, and outlined three different scenarios: the low-end of management's estimates, the high-end of their estimates, and the midpoint of their estimate ranges. All dollar values are in millions.

Limbach 3-Year Financial Estimates (Author's Spreadsheet)

{kind=link}

If management can meet the midpoint of its guidance over the next three years, the company will be generating roughly $50mm in EBITDA and $35mm in consistent free cash flow in 2025. LMB generated nearly $35mm in FCF this past year, but the value was inflated due to the timing of shifts in working capital. Applying my usual baseline target of a 10x FCF valuation, this would give LMB a projected market cap of $350mm, exactly double today's current market cap of $175mm. This translates to a target share price of $32.50.

Will LMB's Progress be Derailed by a Recession?

The market is concerned about an imminent recession, but I think a recession will help LMB more than it will hurt it. I think this for two reasons. First, LMB's customers rely on the company to support mission-critical systems. To quote new CEO Michael McCann from last quarter's conference call:

Limbach is also very focused on being disciplined in working with customers where their systems are mission-critical and have needs regardless of the macroeconomic environment. In these types of buildings, the owners can defer large capital expenditures, but they can't avoid immediate repairs. " ( source )

When you operate a data center or a hospital, you can't afford to have your air conditioning go down for an extended period of time, so maintenance and emergency fixes remain a priority even a recession. Because LMB has focused on growing direct relationships with building owners, they will remain the first call that the building owners make when they need assistance. If companies are forced to delay new construction or major upgrade work due to capital constraints caused by a recession, it means they may need to unexpectedly invest more into maintenance and repairs on their existing systems. This makes them potential new customers for LMB's services.

Second, a difficult macroeconomic environment may present LMB with accreditive acquisition opportunities. The company had a net cash position at the start of 2023 ($36mm in cash against $32mm in total debt) and is already looking for takeover candidates. If other businesses in adjacent industries (particularly those focused on new construction) begin to struggle in an economic downturn, they may be more open to a buyout and have less leverage in negotiating a sale price. LMB has already demonstrated its M&A skills with its acquisition of Jake Marshall at the end of 2021. LMB paid $19mm net of cash received for Jake Marshall, and in 2022 the division generated $63mm in revenue, $9.7mm in gross profit, and $3.7mm in net income. I'm very happy to get a business with growth prospects at a price that is only five times earnings. If additional acquisition opportunities present themselves in a recession, LMB will have the financial flexibility and acumen to take advantage of the situation.

Risks

While a recession would likely help LMB grow its service and maintenance revenue, it is also possible that it would cut down on the number of new-construction projects they are awarded. If LMB's customers put capital expenditures and expansion plans on hold, that lost revenue will only be partially offset by an increase in service revenue. That being said, I don't expect new construction to completely fall off a cliff. Federal and state government spending programs tied to 2021's bipartisan infrastructure legislation are just beginning in earnest, and the passage of the CHIPs bill and Inflation Reduction Act will provide further support to many of LMB's existing and potential customers.

I don't see there being liquidity risk for LMB in a recession. The company has gotten to a net-cash position on their balance sheet and has over $20mm in available liquidity on their credit facility. I don't expect this to be an issue anyway, as the company has convincingly moved to generating positive free cash flow and shouldn't need additional credit unless an acquisition takes place.

Conclusion

If the US economy manages to avoid falling into a recession, then I expect LMB to continue its steady and consistent growth. The company is on track to generate meaningful and consistent cash flow, which I expect to translate into a share price north of $30. If a recession materializes, I expect LMB to be able to grow its customer base even faster and potentially be able to get a great deal on an acquisition. LMB is the third largest position in my portfolio and I am comfortable keeping it a highly weighted, even in the face of a potential recession.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Limbach Holdings Can Thrive In A Recession