LMB - Limbach Holdings: Compelling Opportunity In A Defensive Name

2023-10-03 05:17:54 ET

Summary

- Limbach Holdings is a small-cap business that is underfollowed by Wall Street, capitalizes on vital infrastructure, has a resilient customer base, and has returned 344% in one year.

- In the face of slowing revenues, the company has turned to improving its bottom line and has been met with great success.

- Limbach presents an undervalued investment opportunity as a resilient business, and its future looks primed for more acquisitions with a prime balance sheet.

- Evidence of multiple insider buys adds to further confidence in this company as an investment, and I rate this as a Buy.

What businesses underpin our world? What businesses make a compelling case for investment? Depending on who you ask, everyone has a different answer. The popular narrative would have you believe in whatever grabs the most eyeballs (Let me tell you about this AI company..!) But great returns need not always come from big narratives. Sometimes they even can be hiding in plain sight.

Simply said, it goes back to a philosophy of investing where you buy "what you know" and "what you understand". It is part of a Peter Lynch approach where you focus on companies and industries you understand well from your own experiences and daily life. This is where an average retail investor can get their edge (In other words "beat the street")

Getting the story on a company is a lot easier if you understand the basic business... That’s why I’d rather invest in pantyhose than in communications satellites, or in motel chains than in fiber optics. The simpler it is, the better I like it.

- Peter Lynch

Recently, a small-cap business Limbach Holdings popped up in my filter that took me by surprise in a lot of aspects. Three big things of note -

1. This business is hardly followed by Wall Street (Only 2 analyst ratings)

2. Business capitalizes on the vital infrastructure that underpins our world (which means resilience)

3. Has returned 344% in one year (Again not being in a "hot" industry)

Limbach Holdings and its operations

Limbach Holdings ( LMB ) operates in the industrial sector and is a leading commercial specialty contractor. Segment-wise they break down their business in terms of managing new construction or renovation awarded by contractors (General Contractor Relationship) and managing maintenance or service directly(Owner Direct Relationship). These are the main components of their business -

Mechanical Services : Limbach offers a wide range of mechanical services, including the installation, repair, and maintenance of HVAC systems.

Plumbing Services : The company provides plumbing services, which involve the installation, maintenance, and repair of plumbing systems.

Electrical Services : Limbach offers electrical services that encompass installing, maintaining, and repairing electrical systems.

The resiliency of their operations comes from the fact that most of the repair and maintenance-related projects have customer bases with mission-critical systems.

Core Areas of Business (Company Investor Materials)

{kind=link}

Tightening its belt

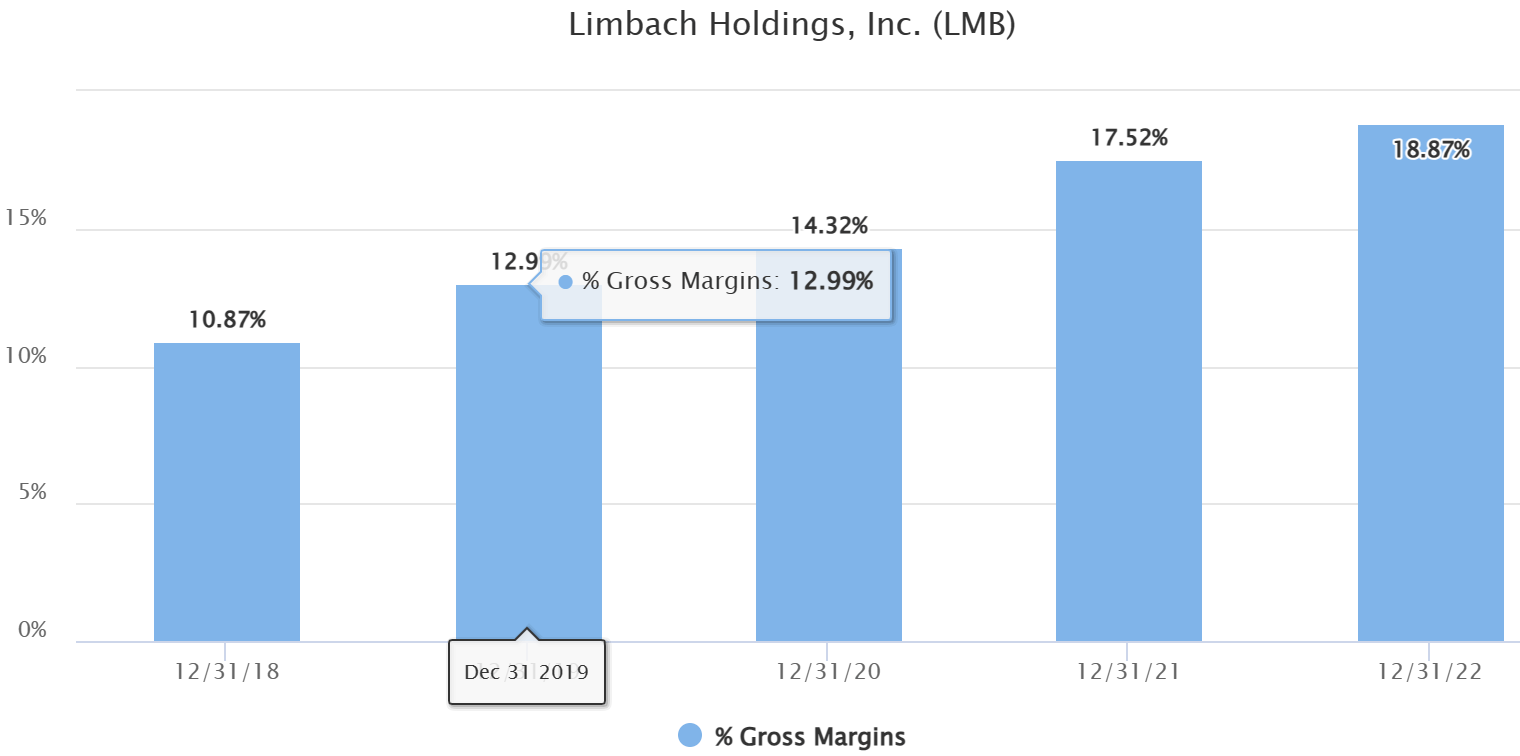

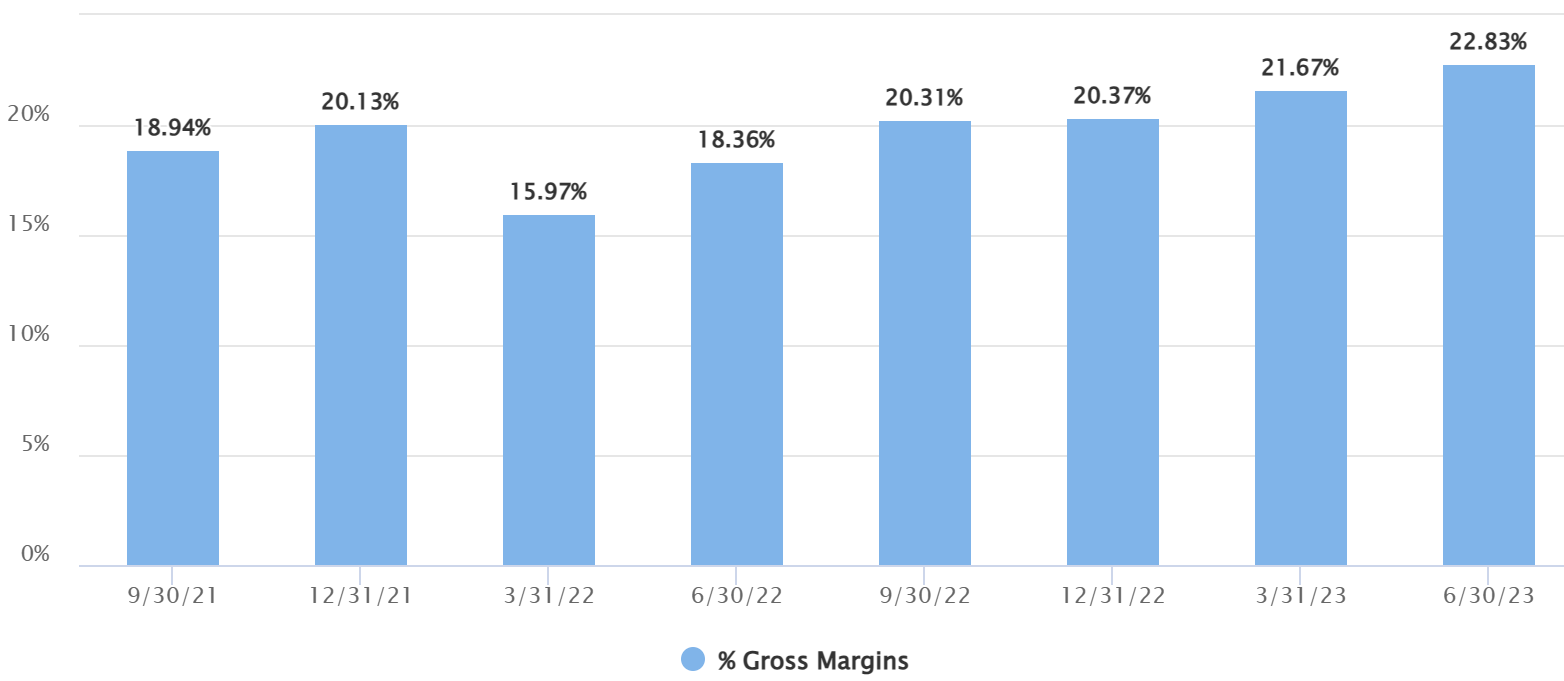

In the face of slowing revenues, I like what the company was able to achieve through the bottom line. After growing steadily for a few years, the last two years were a disappointment after the revenue dropped by more than 10% from the 2020 high.

However, the company saw opportunities to improve its gross margins and was able to execute it well. Comparing 2019 which had its best year in terms of revenues, gross margins have improved by almost 7%, and when you look at the latest quarters this is still trending up! If you look at LTM, Gross profits are at 21.2% and Operating margins are close to 5% at the highest levels ever. This has resulted in the company having the highest diluted EPS in its history.

Gross Margins Annually (Tikr) Gross Margins Quarterly (Tikr)

{kind=link}

{kind=link}

Their focus on improving costs in the face of slowing revenues means key metrics have been trending up for the company. ROE, ROA, and ROIC are all at the highest levels they have ever been.

All of this has translated to excellent health in their balance sheet. Its cash position of $46M is more than its total debt. Its debt-to-equity ratio has been in big decline and has moved from being close to 1 from three years ago to 0.2 as of the latest quarter. This is why I think the company is remarkable as it has been able to tighten its belt and come out stronger in the face of slowing revenues.

Undervalued but the future needs work

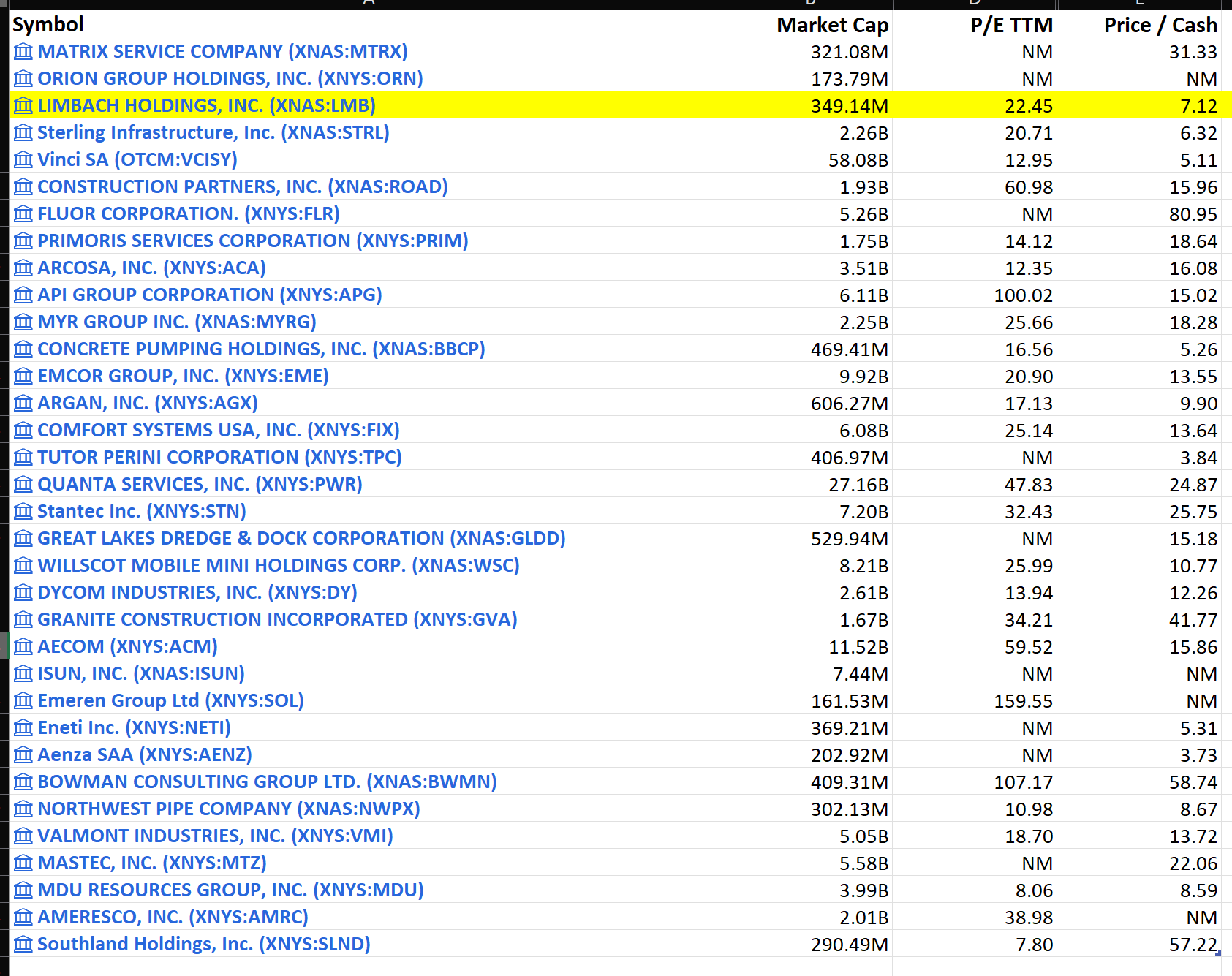

With a rising stock price, the earnings multiple has been expanding as well and it currently stands at 22.4x. When you crunch the multiples for all the stocks in the "Construction and Engineering industry", the average comes out to be 36x. I believe this highlights the challenge across the industry. The margins are generally lower which squeezes most companies. In light of this fact alone, the company's moves in this direction to improve profitability make it a compelling case for investment. They have also been able to improve their cashflows which presents us with another valuable P/CF ratio at 7.1x (industry average 19.5x).

Valuation Industry Comparables (Seeking Alpha)

{kind=link}

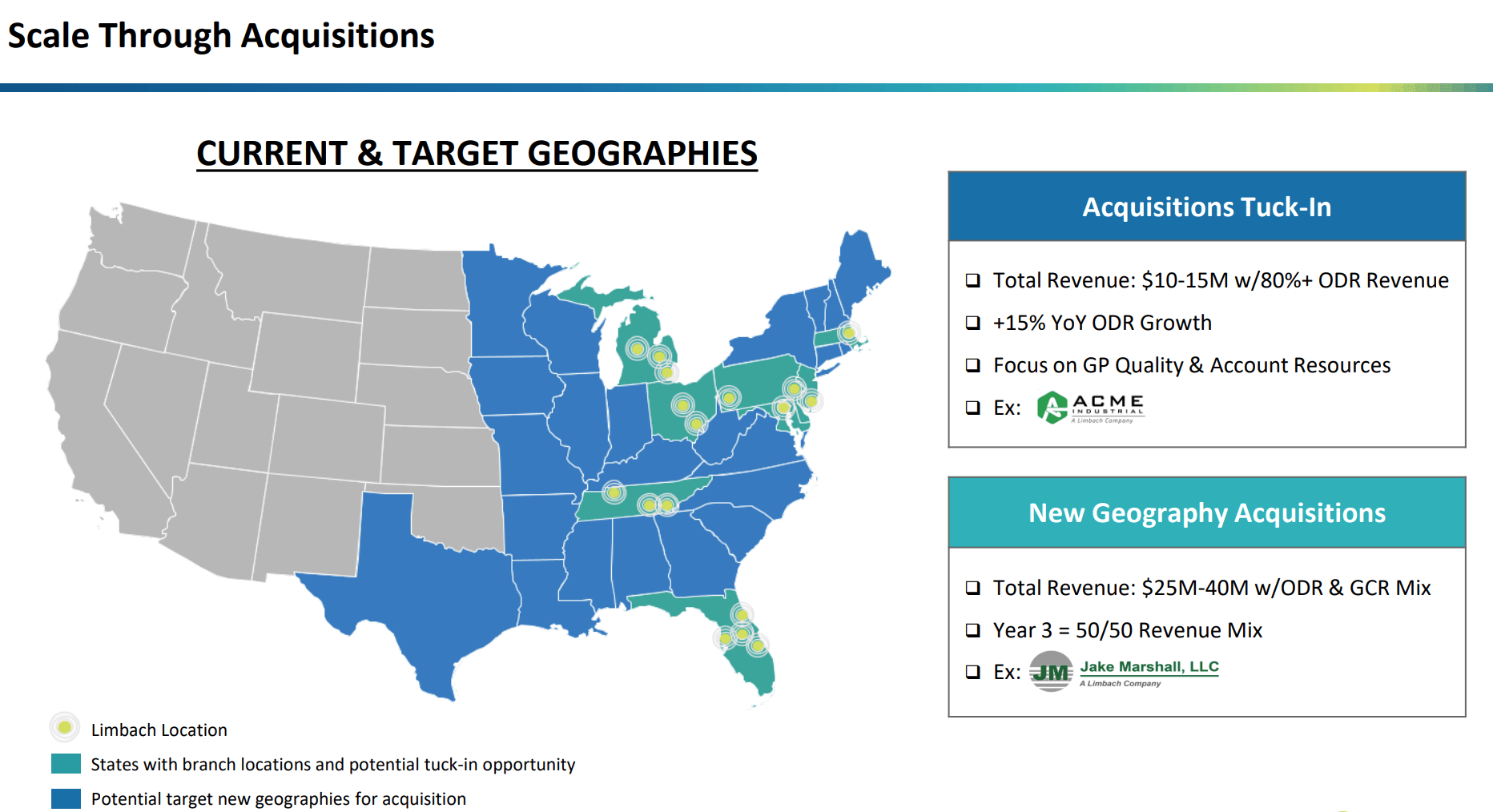

Can this continue? I believe at some point we would hit a limit in terms of how much costs can be saved (which is a reason I haven't used the PEG ratio regardless of how attractive it looks right now at 0.24). There are only so many tricks the company can pull here which is why I believe it is important to see what its outlook looks like. In its latest investor presentation, the company guided to $490 - $520M of revenue. This means it will be around what we saw in 2022 ($497M). On one hand, it is experiencing a saturated market and on the other, it can hit the ceiling in terms of saving costs which is why I believe the company is increasingly looking at acquisitions for growth. It is looking at both expanding within areas it already operates and also expanding to new areas.

{kind=link}

It will be interesting to see how this plays out in the next few years.

Rating it as a Buy

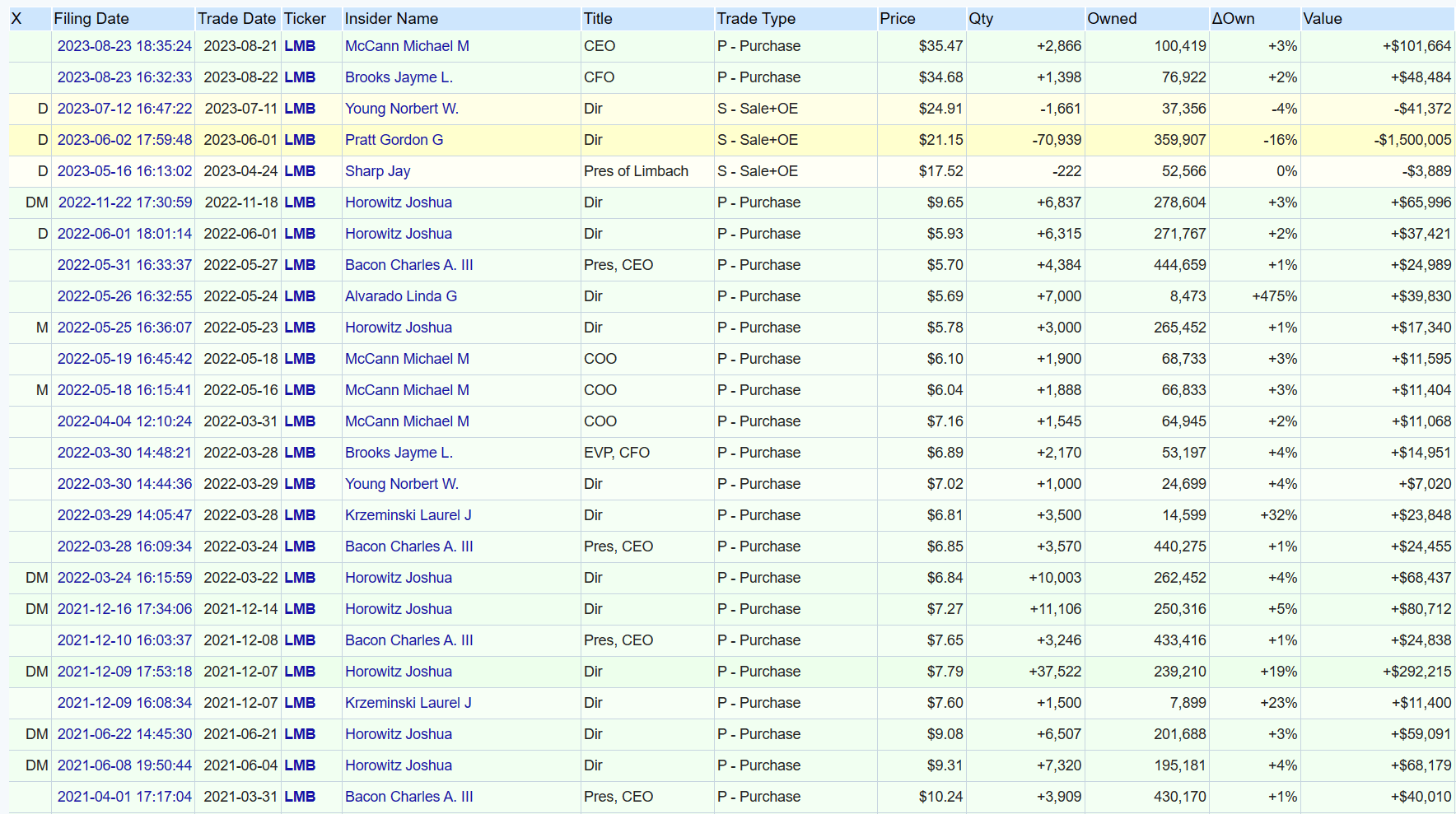

I am rating the company as a Buy and believe that the management is confident of further propelling the company's fortunes through a combination of acquisitions and then bringing efficiency to the acquired operations. This would enable it to grow its top line and also put it ahead in the industry in terms of margins. My confidence in their fortunes gets a further boost when I see the number of insider buys.

Insider Transactions (Open Insider)

{kind=link}

It is well known that insider sales could happen for any number of reasons, but insider buys happen for only one reason – insiders believe the stock price will rise (In the last 3 years, there have been close to 25 transactions by the company insiders in terms of buying the stock).

A key risk worth mentioning

While I believe a big portion of the company's earnings are resilient and are in the realm of services that cannot be pushed or postponed, it is also important to note that the company gets its business from new construction projects as well. In the face of a recession, this may see a slowdown (although there are some core areas that may not be affected at all e.g. Healthcare). This would bring down the top line, and relying on the bottom line again would not be as fruitful as we saw previously (Could hit the ceiling in terms of cost efficiency). For now, I am not in the business of forecasting a recession and an investor can only act with the information that is available now. All indicators point to this being a wonderful business and their vision is something I agree with. I would be a buyer of the company at this price.

For further details see:

Limbach Holdings: Compelling Opportunity In A Defensive Name