LMB - Limbach Holdings: One Of The Best Among Small Caps Today

2023-11-01 09:05:24 ET

Summary

- Limbach is a $330-million market cap firm that primarily focuses on the design, installation, and maintenance of mechanical, electrical, plumbing, and control systems, with a specific emphasis on HVAC services.

- The company's strategic acquisitions and strong cash flow have contributed to improved leverage and credit risk profile.

- Despite risks in the construction industry, LMB is seen as one of the strongest small-cap stocks in the U.S. with potential for long-term growth.

- I think LMB's overvaluation that appears at first glance may be easily explained by margin expansion, which I believe the market is still underestimating over the long term.

- I reaffirm my previuosly given 'Buy' rating.

Th e last time I wrote about Limbach Holdings ( LMB ) was June 28, 2023 , and since then my bullish call has held up well as far as I can see:

{kind=link}

In the meantime, the company has reported its Q2 results and will also submit its Q3 report in a few days, so I thought it necessary to update my coverage in advance.

The Company And Its Q2 Results

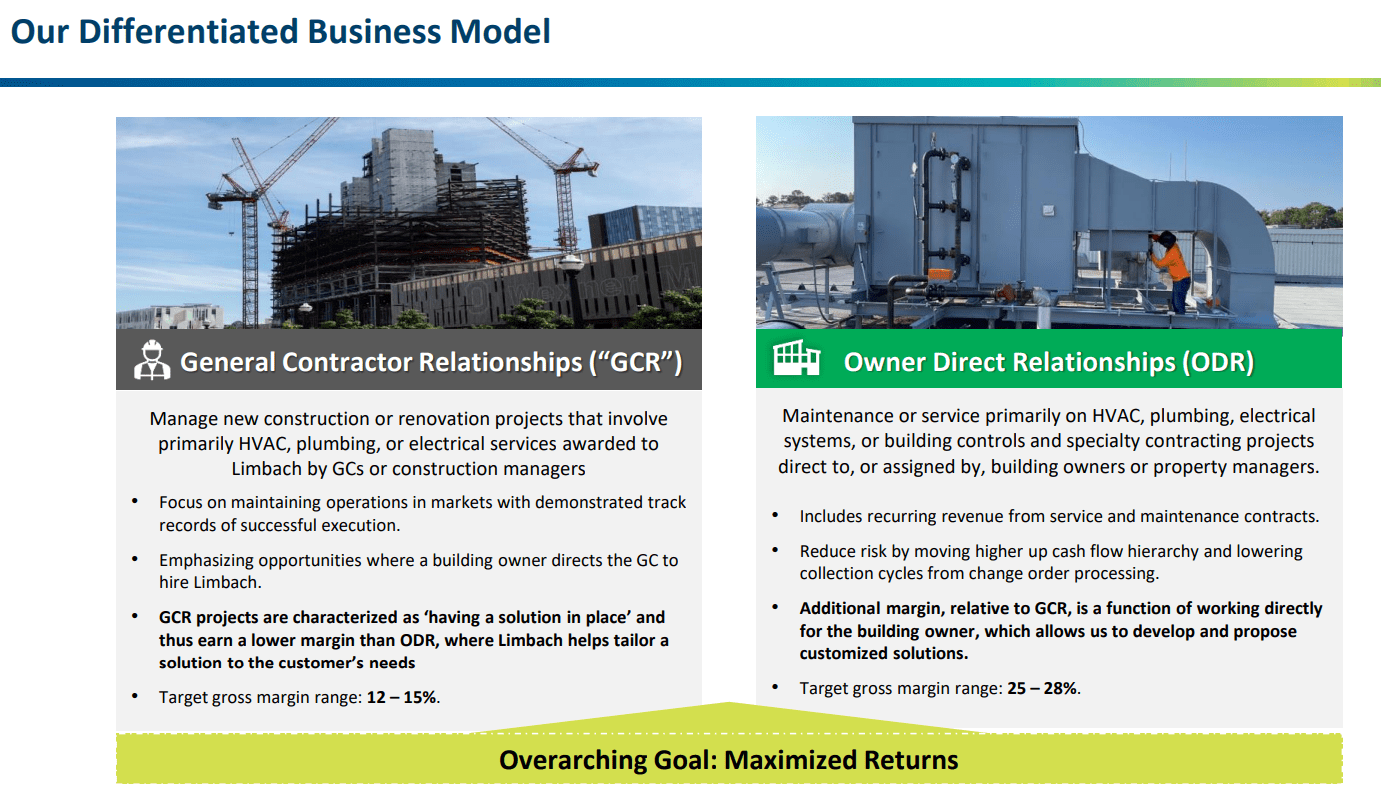

First off, Limbach is a $330-million market cap firm that primarily focuses on the design, installation, and maintenance of mechanical, electrical, plumbing, and control systems, with a specific emphasis on HVAC services. The company operates in two segments: General Contractor Relationships ("GCR", 52.9% of total sales in Q2 FY23 ) and Owner Direct Relationships ("ODR", 47.1%).

{kind=link}

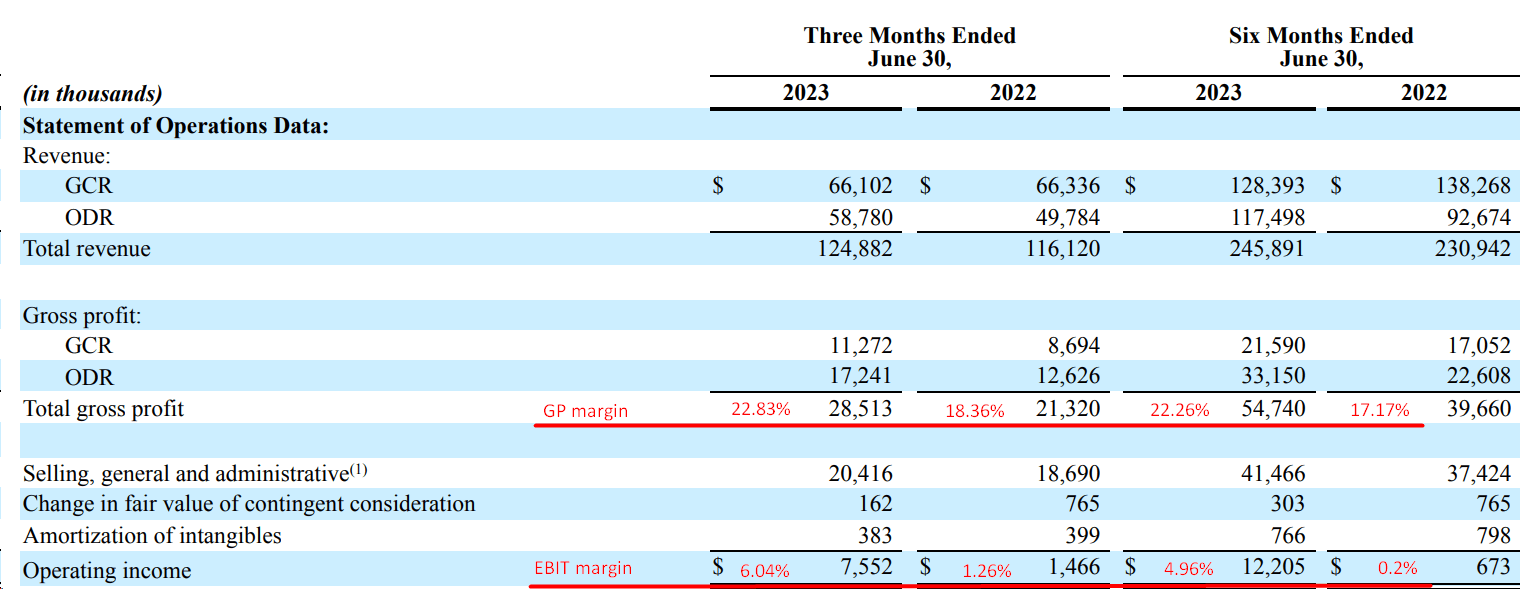

The company's total consolidated revenue experienced growth in Q2 FY2023, with the ODR segment accounting for 47.1% of the total consolidated revenue, up from 42.9% in the previous year. ODR revenues increased by 18.1% compared to the previous year, contributing to a 7.5% growth in consolidated revenue.

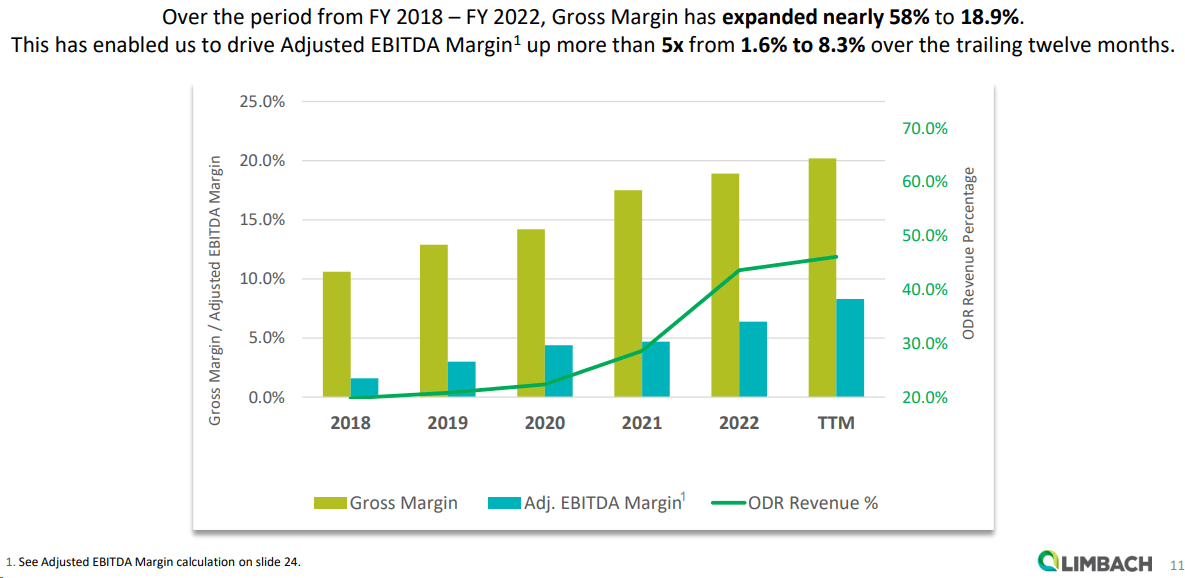

LMB's Q2 2023 results revealed its strategic focus on improving margin profiles by actively shifting its revenue mix towards the ODR segment. This shift has contributed to an increase in consolidated gross and EBIT margins in Q2 and 1H FY2023:

{kind=link}

{kind=link}

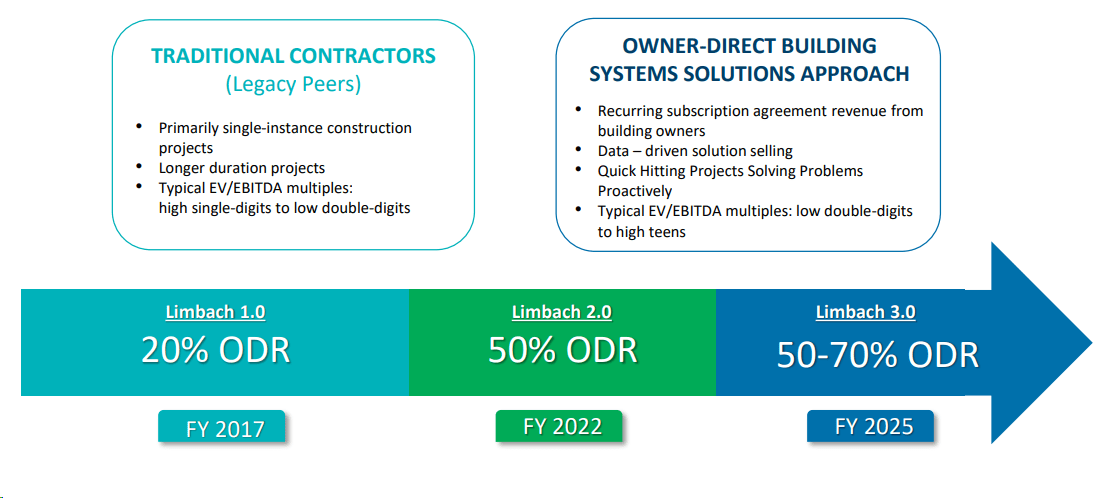

I particularly like the fact that LMB's margin expansion is not a one-time event: over many quarters, management has worked hard to achieve today's levels, which can only inspire respect:

{kind=link}

According to LMB's management commentary, the firm is also trying to achieve higher margins by making proactive recommendations that maximize returns on customers' physical asset investments.

Strategic acquisitions also play a pivotal role in LMB's growth strategy, with a recent acquisition of ACME Industrial expanding its customer base and market presence in the hydroelectric end market. The global hydropower generation market is expected to grow at a CAGR of 5.60% from 2023 to 2032, according to Prudence Research data , so I think LMB's purchase has a good chance of becoming a successful addition to the firm's portfolio.

The company's operating cash flow amounted to ~$26.3 million for 1H FY2023, which is about twice bigger than YoY. This cash is actively used to reduce debt and fund LMB's acquisition program, the management noted. And the effort is really paying off, considering how LMB's leverage profile has improved recently:

At the end of Q2 LMB had a cash and cash equivalents balance of $45.9 million, indicating strong collections during the quarter and effective management of working capital accounts. Therefore, I believe that LMB's credit risk profile has improved in Q2 when we consider the combination of the above factors (strong cash balance and declining leverage ratio).

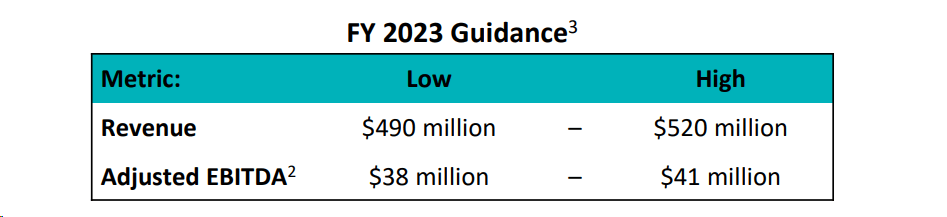

Despite supply chain challenges, the company remains focused on meeting strong demand in mission-critical vertical markets, with a dedicated approach to delivering value and maintaining strong customer relationships. That's why the management revised its adjusted EBITDA guidance for FY2023 to a range of $38 million to $41 million, up from the previous range of $33 million to $37 million.

{kind=link}

From an operational perspective, I like what I see in LMB's financials: The company continues to grow and improve its margins while improving the quality of its balance sheet.

But what about the stock's valuation?

The Valuation And Expectations

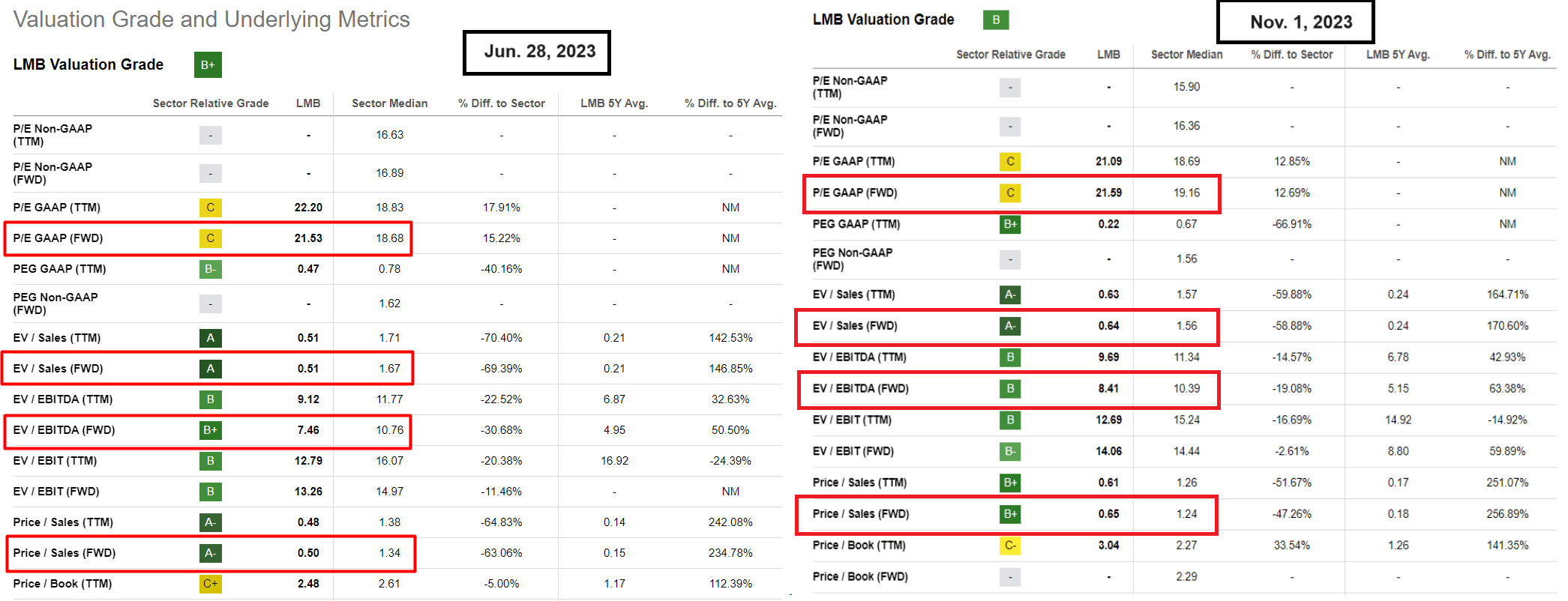

I am still not very concerned about the absolute valuation of the company.

{kind=link}

LMB stock trades at 8.41x of next-year EV/EBITDA , which is 13.2% lower than its TTM figure. The last time I looked at this metric, it was 11.3% lower. Because of this difference, LMB has grown to some extent during the period indicated (i.e. multiple expansion). However, the current value of 8.41x is still 19% lower than the median value for the Industrials sector . As we remember, LMB is still in the process of increasing its margins - therefore, the growing EV/EBITDA multiple seems justified to me.

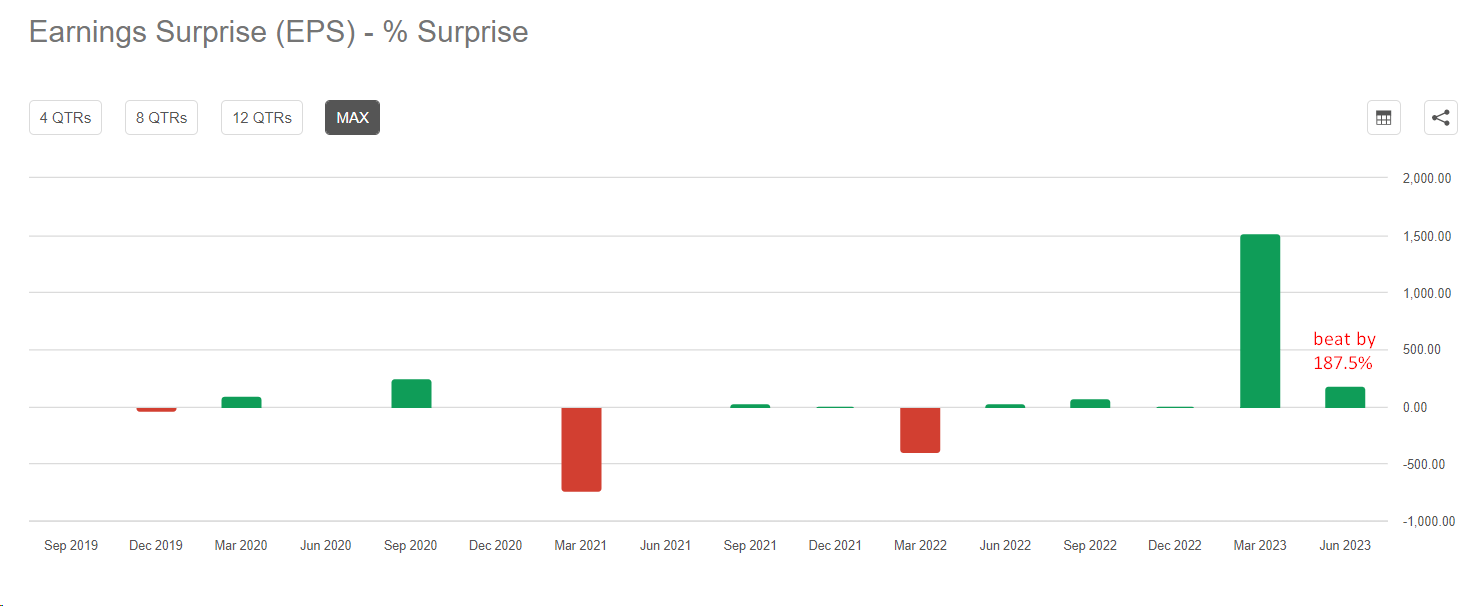

As you can see above, LMB's EBITDA margin is expected to be lower in two years (FY2025) than a year earlier (i.e., in FY2024), according to consensus [YCharts data]. This assumption seems too pessimistic to me given the speed at which LMB is adding new assets and reducing debt. Therefore, I expect new surprises in earnings per share going forward ( as was the case recently ).

{kind=link}

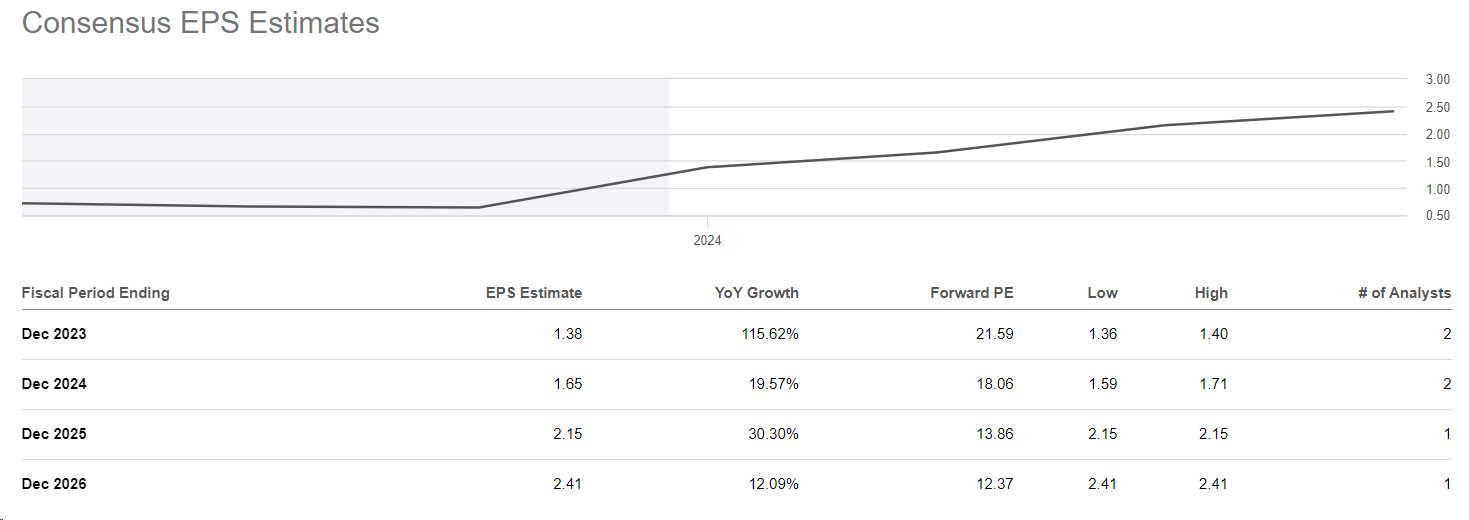

I understand that many are concerned about LMB's relatively high P/E ratio, but I don't think there is any reason to panic about it: EPS expectations have improved dramatically in recent months, and judging by the implied P/E ratios beyond this year, LMB is trading very attractively today.

{kind=link}

The Verdict

As always in the stock market, investing in small caps like Limbach Holdings carries many risks that should be carefully considered. First off, LMB operates in the cyclical construction industry, making it susceptible to economic downturns and fluctuations in demand for its services. Secondly, market conditions and competition may affect the company's contract acquisition and margin maintenance. Thirdly, supply chain disruptions, economic factors, and interest rate fluctuations can impact project costs and financing, while dependence on key customers and project execution quality are pivotal to LMB's success. Additionally, macroeconomic factors and external events can disrupt construction projects and affect the company's financial stability. So potential investors should assess these risks alongside their investment strategy and risk tolerance.

But despite all the risks, I think LMB is one of the strongest small-cap stocks in the U.S. right now. I think the overvaluation that appears at first glance may be easily explained by margin expansion, which I believe the market is still underestimating over the long term. I cannot say with certainty whether LMB will be able to beat Q3 FY2024 consensus estimates - we should find out on November 8, 2023 (according to Seeking Alpha). But I am quite optimistic about LMB's long-term future.

Thanks for reading!

For further details see:

Limbach Holdings: One Of The Best Among Small Caps Today