LMB - Limbach Holdings: We Might See A Fall In The Share Price

2023-03-13 15:18:59 ET

Summary

- LMB recently posted its FY22 and Q4 FY22 results. Their revenue and income growth were flat compared to FY21.

- The share price is near its all-time high and showing bearish signs.

- The management is expecting stagnant revenue growth in FY23.

- I assign a hold rating on LMB.

In the US, Limbach Holdings (LMB) provides comprehensive building systems solutions. It engages in the design, installation, and maintenance of mechanical and control systems and HVAC systems. Their facility services comprise HVAC service and maintenance, engineering and design, equipment and materials selection, and mechanical construction. They serve research and inpatient hospitals, universities, the sports arena, and life sciences. They operate in two segments owner direct relationships ((OCD)) and general contractor relationships ((GCR)). They recently announced their Q4 FY22 and FY22 results. In this report, I will analyze its financial performance. They saw stagnant revenue growth in FY22, and the management expects the same growth rate in FY23. As a result, I believe we might see a fall in the share price soon. Hence I assign a hold rating on LMB.

Financial Analysis

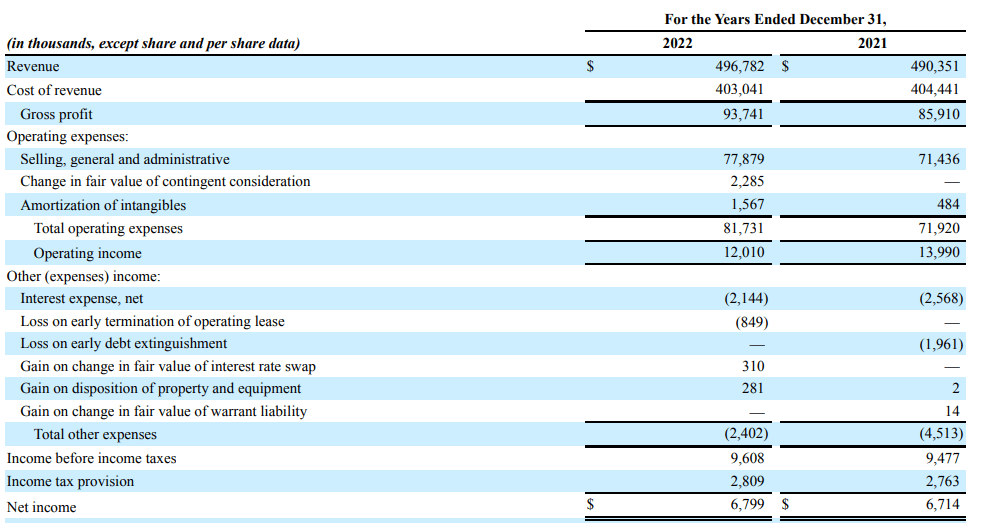

LMB recently posted its FY22 and Q4 FY22 results . Compared to FY21, the revenue and net income increase was pretty much unchanged in FY22. The revenue for FY22 was $496.7 million, a mere rise of 1.3% compared to FY21. I believe the main reason behind the rise was an increase in revenue from the ODR segment. The revenue from the ODR segment rose by 54.2% in FY22 compared to FY21. The net income for FY22 was $6.8 million, a rise of 1.2% compared to FY21. In my opinion, the annual financial performance was not particularly remarkable, and the growth of revenue and net income was relatively flat. In my opinion, the GCR segment's poor performance was the primary cause of the stagnant growth of revenue and net income. In comparison to FY21, the GCR segment's sales fell by 19.9% in FY22.

{kind=link}

The revenue for Q4 FY22 was $143.4 million, a rise of 13.1% compared to Q4 FY21. I think the company's emphasis on growing the ODR segment and improved project execution were factors in the Q4 FY22 revenue rise. When compared to Q4 of FY21, the ODR segment's revenue grew by 63.7% in Q4 of FY22. The net income for Q4 FY22 was $3.8 million, a decline of 11% compared to Q4 FY21. I think the decline in net income was primarily caused by a decline in the revenue of the GCR segment and a rise in expenses. I believe LMB's financial performance in FY22 was fairly average; revenue growth was flat, and Q4 FY22 net income decreased compared to Q4 FY21.

Technical Analysis

{kind=link}

LMB is trading at the level of $14.7. The price is currently close to its record high of $16. There is a barrier area at $16 that has been attempted to be broken twice in the past, once in 2016 and again in 2021, but both attempts were unsuccessful. The stock dropped more than 65% after hitting the resistance zone both times, indicating that sellers are aggressive at $16. The stock recently attempted to break through the resistance mark, but after touching it, it dropped 6%. The weekly candle has an enormous wick, indicating weakness, as seen by looking at it. Therefore, in my view, one should avoid the stock because it is at a critical level, exhibiting weakness, and it can fall from current levels.

Should One Invest In LMB?

{kind=link}

The price has increased by more than 90% since March 2022. It is currently very close to its peak. If we look at the FY22 figures, net income, and revenue growth were both flat. Therefore, in my view, the company's share price is not justified by its financial performance. In the near future, I believe the share price might fall.

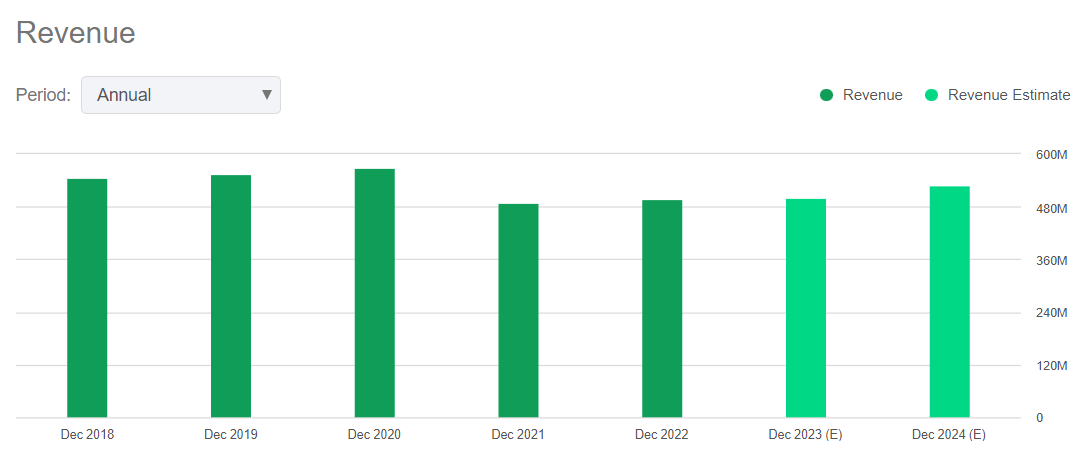

The estimated revenue for FY23 is $499.8 million, which is on par with the revenue for FY22. In FY23, the management anticipates stagnant revenue development. In the GCR segment, the business is having trouble. In FY22, the GCR segment's revenues decreased considerably. Additionally, there are a number of challenges that could affect the business, including weaker markets, high inflation, and delays in the supply chain. In light of all these obstacles, I think they may have trouble reaching their revenue goals, which could have an impact on the stock price of the company.

Now talking about the valuation. I will use two ratios to judge its valuation. The first ratio is the Price / Sales ratio which is calculated by dividing a firm's market capitalization by its revenue over the past twelve months. They have a Price / Sales ((FWD)) ratio of 0.31x compared to the sector ratio of 1.34x. The second ratio is the EV / EBIT ratio which compares a company's enterprise value to its EBIT. They have an EV / EBIT ((FWD)) ratio of 9.34x compared to the sector ratio of 14.66x. After looking at both ratios, I think they are undervalued. But apart from the valuation, I can't see any positives in the company for now.

Risk

Customers who participate in design/build projects have a singular point of contact for both the design and the construction. They generally handle the engineering and design work themselves when they are given these projects. On other tasks, they serve as a direct resource for the project design team rather than acting as the designer. There is a chance that they, their subcontractors, or the appropriate professional liability or errors and omissions insurance would not be able to shoulder the responsibility in the event that a design error or omission by them results in damage. Any liability coming from a claimed design flaw with regard to their projects could seriously harm their financial position.

Bottom Line

Their revenue and net income growth were stagnant in FY22. The management’s guidance suggests that they are expecting stagnant revenue growth in FY23. There are several challenges that I believe will affect its revenue growth. In addition, its share price is near an all-time high, so I believe we might see a fall in the share price due to underperformance in FY22; hence after analyzing all the parameters, I give LMB a hold rating.

For further details see:

Limbach Holdings: We Might See A Fall In The Share Price