LMB - Limbach: This Top-Rated Stock Still Has Some Room To Grow

2023-06-28 12:10:58 ET

Summary

- Limbach Holdings, Inc. is a $250M market cap company specializing in HVAC services and the design, installation, and maintenance of building systems.

- LMB's corporate approach should lead to higher EV/EBITDA multiples and a stronger gross margin at ~22% by FY2025 - almost double what we saw back in FY2017.

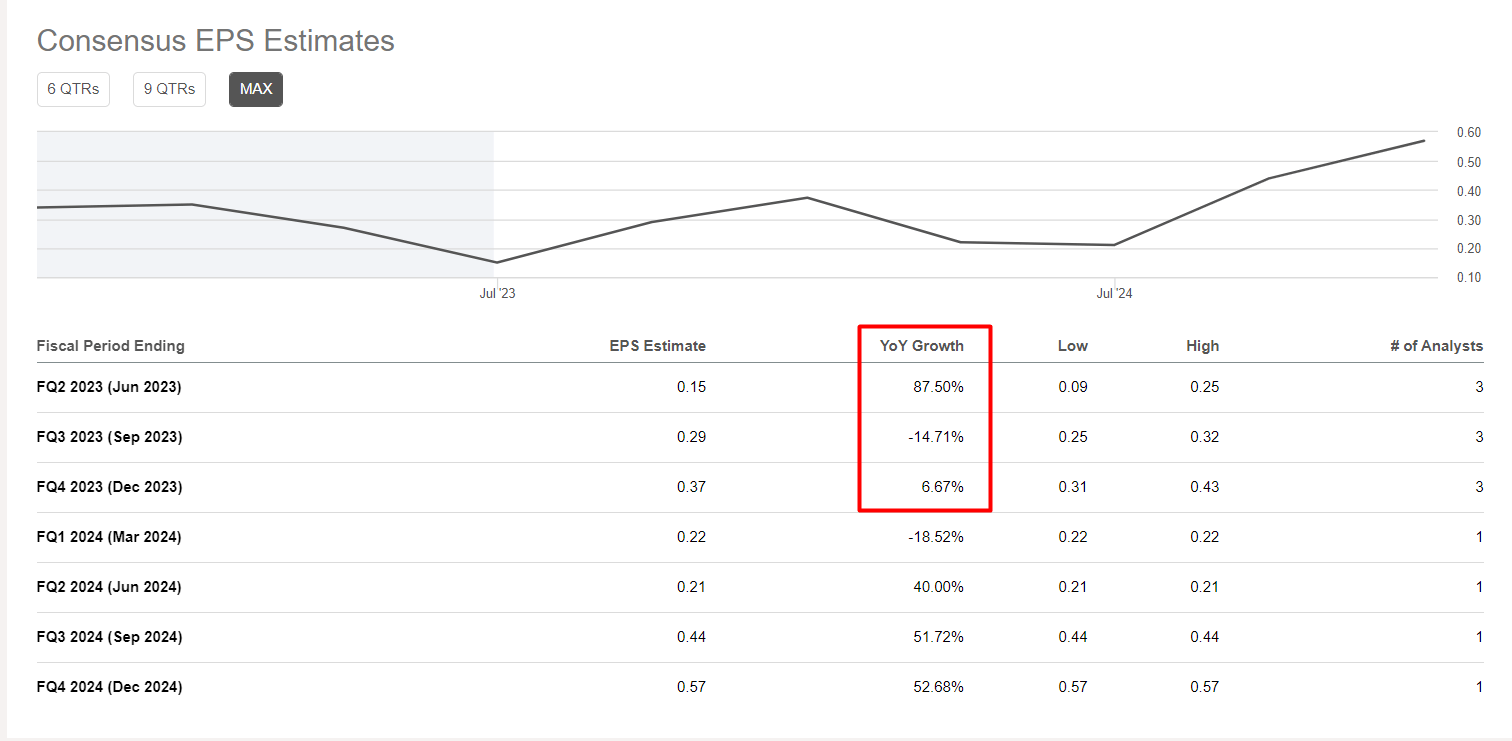

- The market expects LMB to increase EPS by 69.27% in FY23 and by another 32.31% YoY in FY24. I think it might be underestimated.

- I think that the future upside potential of 40% is quite justified - LMB has quite a comfortable margin of safety in the medium and long term.

The Company

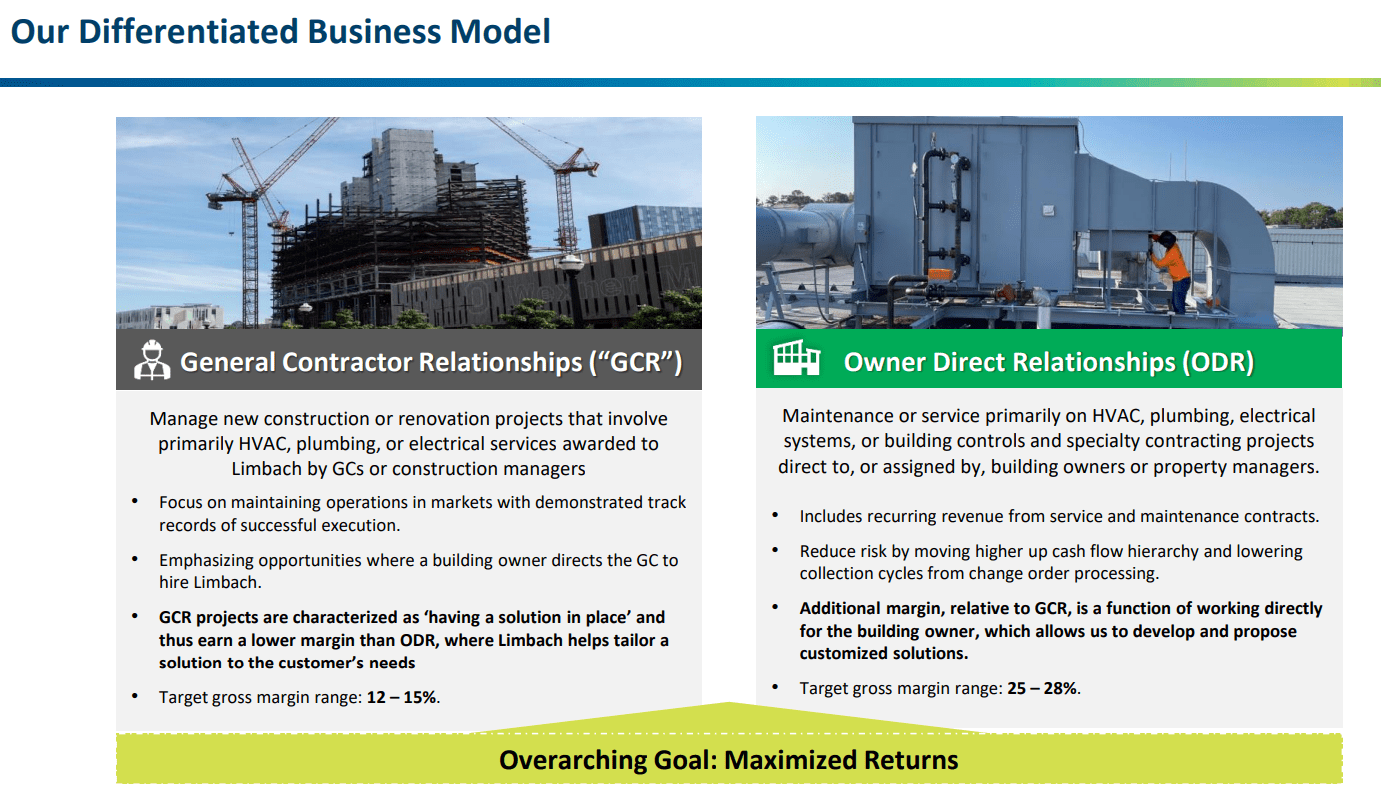

Limbach Holdings, Inc. ( LMB ) is a $250-million market cap firm that primarily focuses on the design, installation, and maintenance of mechanical, electrical, plumbing, and control systems, with a specific emphasis on HVAC services. The company operates in two segments: General Contractor Relationships (51.5% of total sales in Q1 FY23 ) and Owner Direct Relationships (48.5%).

{kind=link}

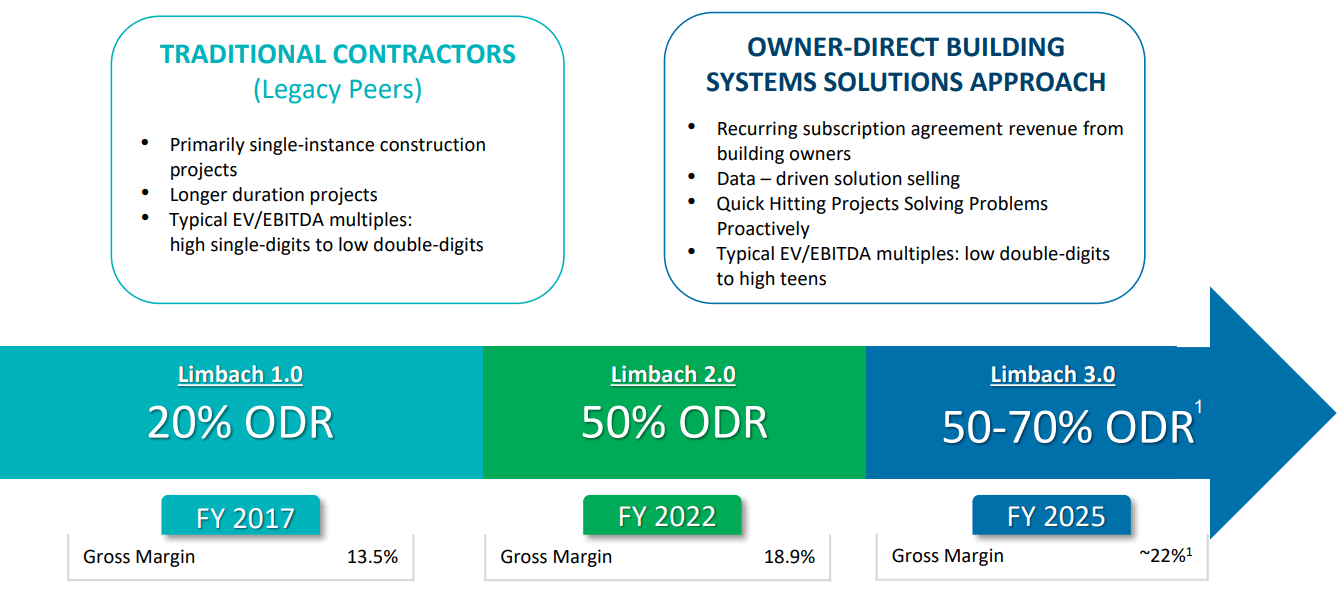

Limbach had a solid start to the year, with adjusted EBITDA outpacing the 1st quarter of the previous 2 years. Revenue saw modest year-over-year growth, while gross margin continued to expand, driving bottom-line growth. In its most recent IR presentation [ May 9, 2023 ], Limbach's management wrote that its legacy peers in the construction industry primarily focus on single-instance construction projects with longer durations. They are valued at moderate EV/EBITDA multiples. In contrast, Limbach's owner-direct building systems solutions approach emphasizes recurring subscription agreement revenue, data-driven solution selling, and quick-hitting projects. This approach leads to higher EV/EBITDA multiples and a stronger gross margin, that should reach ~22% by FY2025 - almost double what we saw back in FY2017:

{kind=link}

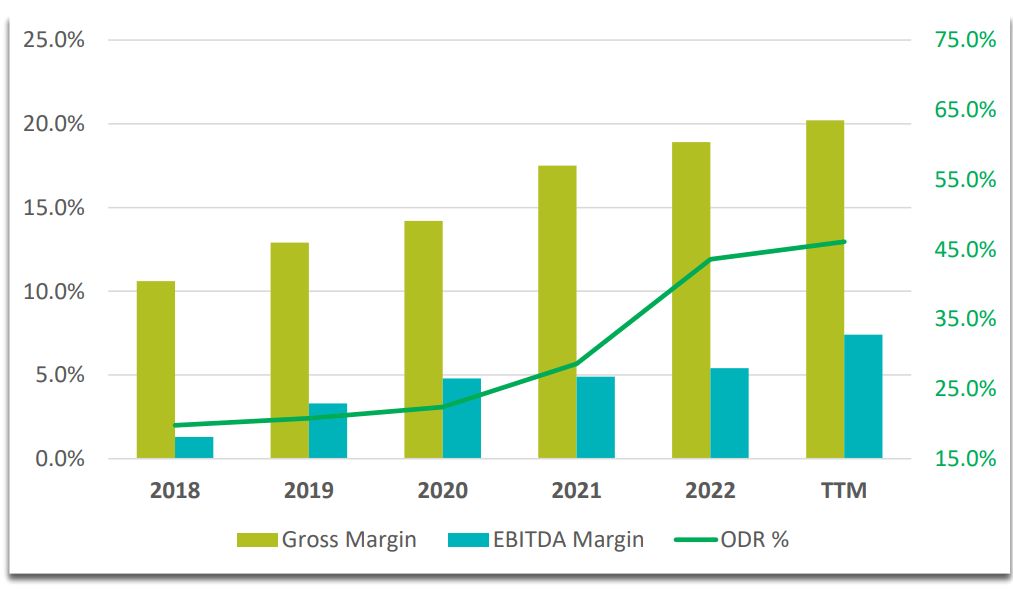

From FY2018 to FY2022, Limbach experienced significant growth in gross margin, which reached 18.9% last year. This improvement in gross margin has played a pivotal role in driving the EBITDA margin up by more than 5 times, increasing it from 1.3% to 7.4% over the same period.

As it goes from the latest earnings call transcript , the firm aims to grow the top line as the higher growth ODR segment outpaces the contraction in the General Contractor Relationships [GCR] segment. At the same time, the firm expects its SG&A expense as a percentage of total revenue to have a similar run rate as FY2022 this year. I, therefore, expect the operating margin to increase even further in the next 2 quarters.

{kind=link}

LMB generated a net income of nearly $3 million and cash flow from operating activities of more than $9.3 million in the 1st quarter, thanks largely to changes in working capital (receivables on the balance sheet declined significantly). The company used the generated cash to pay down term debt and had a cash balance of $41.4 million [+14.9% QoQ]. They negotiated an amendment to the credit agreement, expanding the revolver to $50 million, and providing capital for acquisitions without requiring equity financing. From what I see, Limbach has had a strong liquidity and solvency position over the past few years at least:

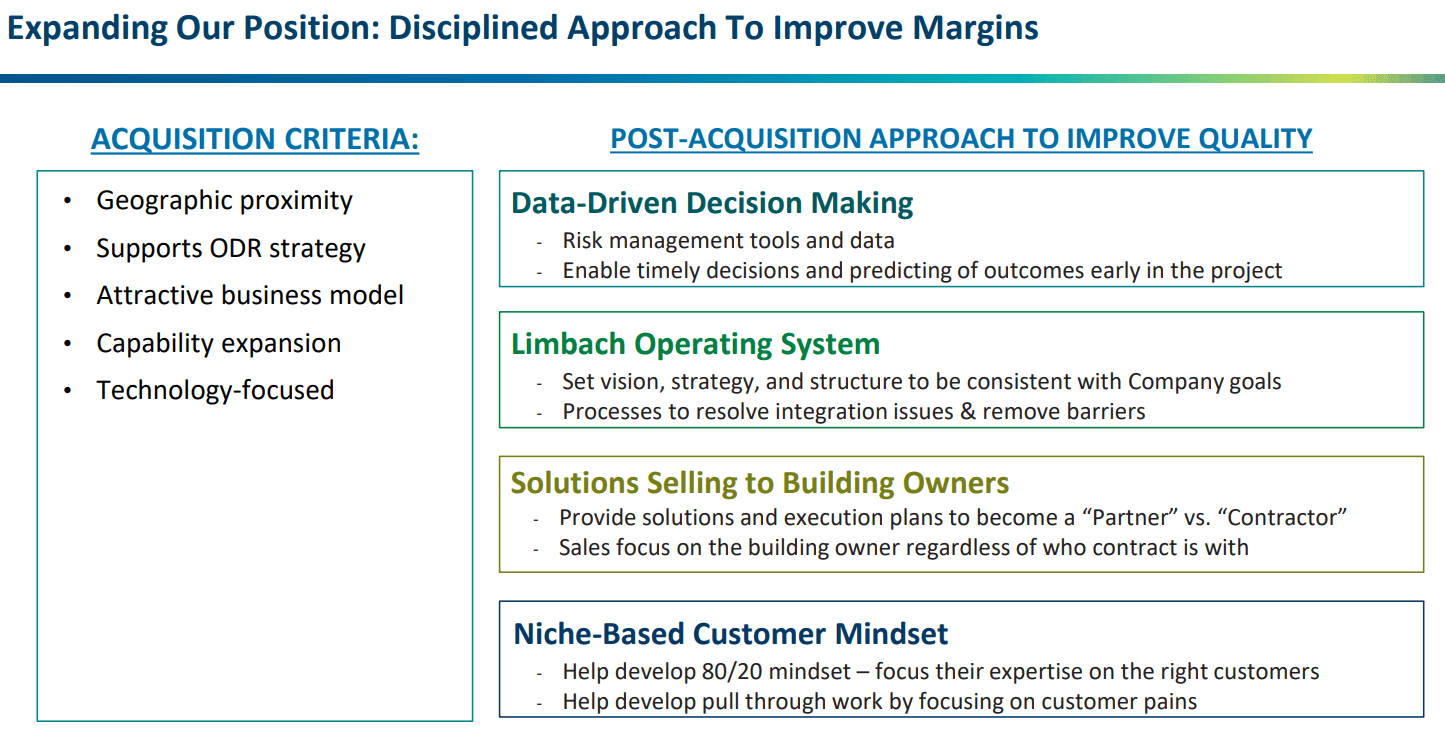

The company has a robust pipeline of potential acquisitions, targeting new geographies and tuck-in locations. Limbach emphasizes cultural fit and strategic alignment when considering acquisitions. I like their criteria for M&As in general:

{kind=link}

Limbach's management reiterated their financial guidance for 2023, expecting total revenue between $490 million to $520 million and adjusted EBITDA between $33 million to $37 million. They anticipate stronger results in 2H FY23, aiming for the upper end of the guidance range.

But how much has the market priced LMB's success in?

Valuation & Expectations

The market expects LMB to increase EPS by 69.27% in FY23 and by another 32.31% YoY in FY24. At the same time, revenue growth in the corresponding years is expected to be 0.31% and 6.25%, respectively [both YoY].

It's difficult to say how justified this forecast is. However, if we take into account the management's guidance that the sales volume will be higher in the second half of the year than in the first, then I believe that LMB has every chance of surprising everyone again - in a positive sense. And why?

In Q1 FY22, LMB's gross margin was 15.97% and gradually increased to 18.36%, 20.31%, and 20.37% in Q2, Q3, and Q4 respectively [for the reasons outlined above]. In Q1 of FY23, this number reached 21.67%, and if we see at least a slight margin expansion in Q2, Q3, and Q4 of FY23, then I believe the full year 2023 projected growth rates will appear underestimated given a lower debt burden compared to FY22:

{kind=link}

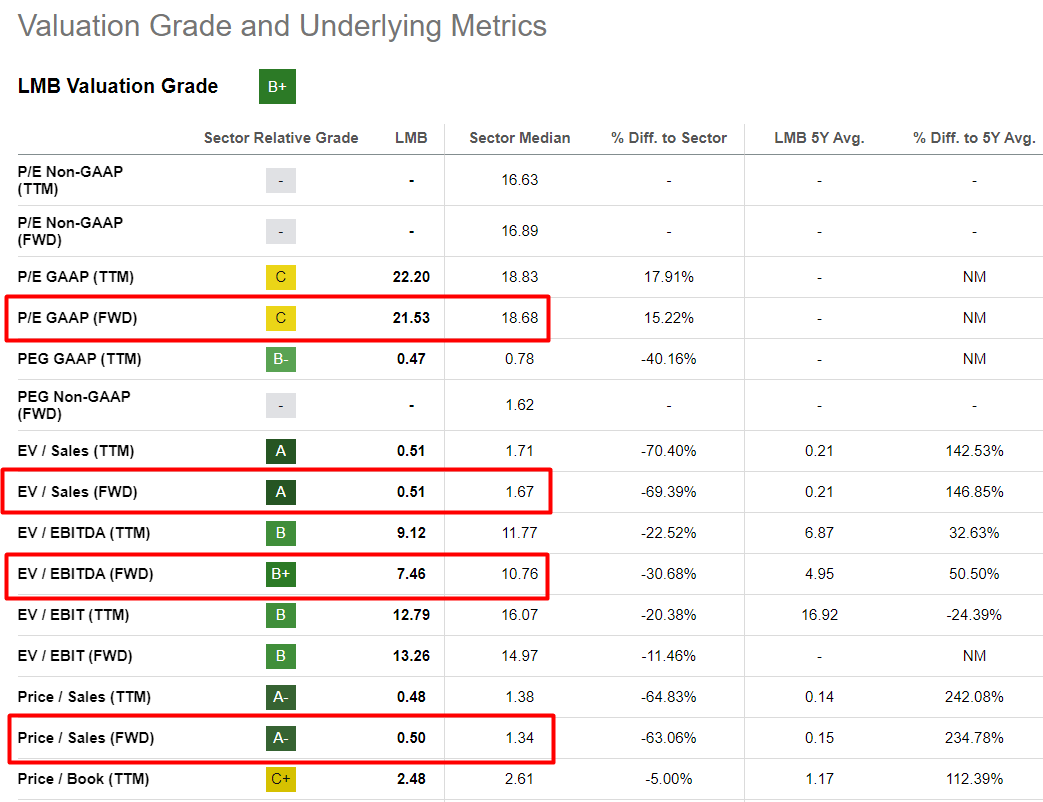

I am not very concerned about the absolute valuation of the company. Yes, the P/E ratios may seem high, but LMB stock trades at an EV/EBITDA of just over 7x, and its forward EV/Sales ratio of 0.51x is ~70% lower than the sector's median.

{kind=link}

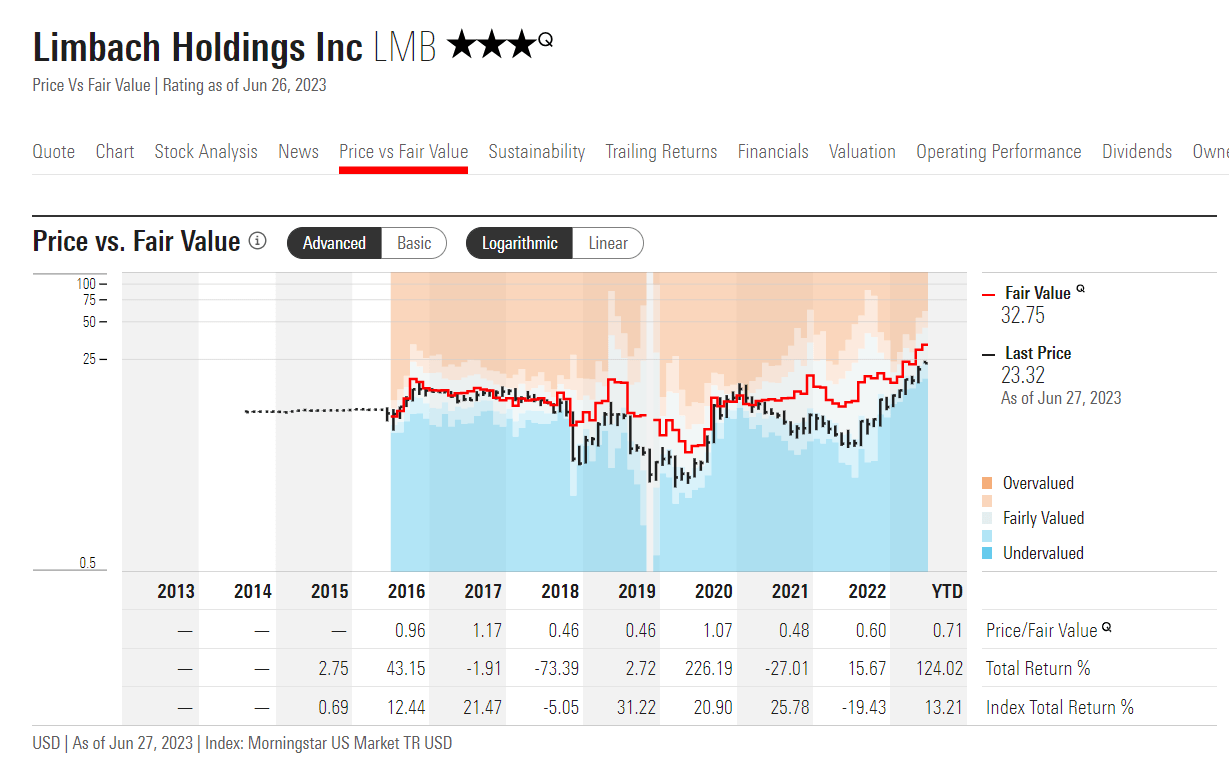

Given the margin expansion, this can only mean one thing - if management's targets for the company's growth continue to hold, then we are now in a zone of severe undervaluation.

Despite the explosive growth of the stock over the past year [over 300%], Morningstar's valuation system gives a fair value estimate of $32.75/share, which is >40% above the last closing price:

Morningstar Premium [proprietary source]

{kind=link}

The Bottom Line

Of course, buying a stock with a market cap of $250 million is anything but risk-free.

First, the margin we are seeing now may have peaked - we have never seen such a high margin for LMB before, and we do not know exactly when it will reach its limit. Based on management's target of ~22% for FY25, we are already there today - in the coming years, LMB's EPS will most likely have to grow due to higher sales volumes, not margin expansion. To some extent, this reduces the attractiveness of LMB's stock, as it introduces an unloved uncertainty for all shareholders.

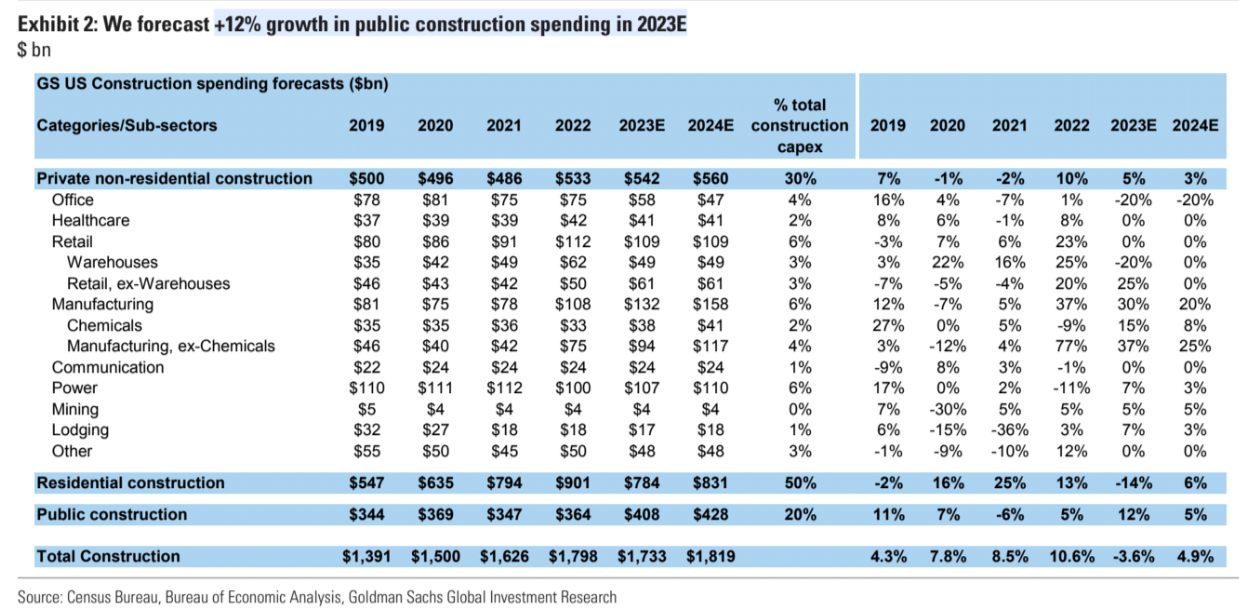

Second, LMB's business is heavily dependent on the construction sector. So far, the growth prospects for this sector are relatively good. Goldman Sachs recently published a forecast that public construction spending should grow +12% in FY2023 and another 5% in FY2024, which is not bad:

Goldman Sachs [June 27, 2023 - proprietary source]

{kind=link}

But the slowdown may not be fully priced in yet, which makes buying LMB shares near their multi-year highs risky.

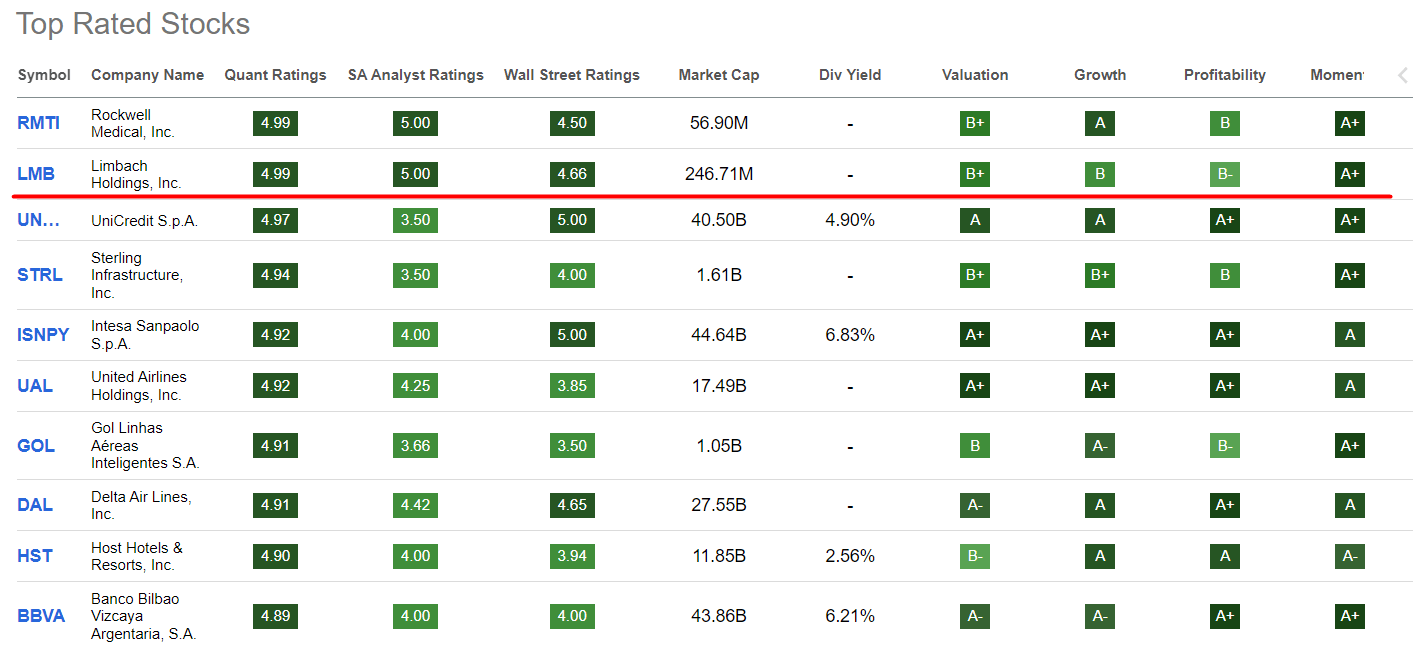

Despite the risks involved, I think LMB has some of Seeking Alpha Quant's strongest grades for a reason and has made it into the top stocks:

{kind=link}

I think that the future upside potential of 40% is quite justified - LMB has quite a comfortable margin of safety in the medium and long term.

Thanks for reading!

For further details see:

Limbach: This Top-Rated Stock Still Has Some Room To Grow