LIMAF - Linamar: Strong Global Car Sales And Mobex Acquisition Should Strengthen Growth

2023-12-26 15:54:31 ET

Summary

- LNR:CA has shown strong revenue growth recovery and robust profitability margins over the years.

- Anticipated growth in the global car sales market and EV adoption will support LNR:CA's future growth outlook.

- The recent acquisition of Mobex will strengthen LNR:CA's business and drive long-term growth as it strengthens its offering range in all vehicle powertrain types.

- My valuation model shows that LNR:CA outperformed its competitors in all aspects. In addition, it also shows double-digit upside potential. Therefore, I am recommending a buy rating.

Synopsis

Linamar Corporation ( LNR:CA ) is a Canadian company that designs, manufactures, and distributes products for the mobility, agriculture, and MedTech sectors.

LNR:CA's historical financial performance has shown that revenue growth is on a recovery path, with net margins staying robust over the years. Its debt levels have improved over the years and pose no insolvency risk to them. Its 3Q23 results continue to show strong revenue growth momentum and margin robustness.

Moving ahead, the anticipated growth in the global car sales market and EV adoption will support its growth outlook as LNR:CA sells automotive parts and equipment to both traditional engine and EV segments. In order to further strengthen its offering range in all vehicle powertrain types, it recently completed the acquisition of Mobex. With all these tailwinds in mind, I am recommending a buy rating for LNR:CA.

Historical Financial Analysis

From 2019 to 2022 , LNR:CA's revenue growth showed a recovery trend. In 2019 and 2020, revenue year-over-year growth is negative, with 2020 reporting a larger decline. In its 2020 annual report, management attributed the decline to the impact of COVID-19. The pandemic resulted in a reduction in automotive production and sales volume due to shutdowns and work-from-home mandates.

However, since 2021, after COVID has subsided and economies around the world started to open up, revenue growth has recovered, and it is growing robustly at double-digit rates. In 2021, it reported revenue growth of ~12.4%, and in 2022, it was ~21.13%.

Author's Chart

Firstly, its gross profit margin started contracting in 2022, and this is attributed to the rising inflation experienced in that year. Although its gross profit margin contracted, its operating income margin and net income margin remained stable throughout the years.

Author's Chart

Looking at the following chart, LNR:CA is able to maintain its operating and net income due to its effective SG&A and interest expense management. Even though gross profit contracted, by reducing SG&A and net interest expense, it offset the impact of gross profit contraction, thus bolstering its bottom line.

Author's Chart

In terms of the debt-to-equity (D/E) ratio, it has improved significantly when compared against 2019's level of ~48%. Over the years, it has gradually decreased, and by 2022, its D/E ratio was ~27%. This represents an improvement of ~21%, which explains how it has been able to reduce its interest expense as a percentage of revenue over the years. With interest expense as a percentage of revenue less than 1%, it does not raise any concerns with me regarding its liquidity.

Author's Chart

Analysis of LNR:CA's 3Q23 Earnings Results

In my opinion, LNR:CA reported robust 3Q23 financial results. Revenue grew 16% year-over-year to $2.43 billion. For its industrial segment, revenue grew 26.8% year-over-year, and management attributed this growth to strong market share growth in its agricultural and access equipment. For its mobility segment, revenue grew 12.3% year-over-year, and it is mainly driven by consistent program launches and also from the revenue generated by its acquisition of Dura-Shiloh's Battery Enclosures facilities. Overall, top-line revenue is performing exceptionally well, continuing the strong revenue growth trend it has delivered since 2021.

Moving down its P&L, its operating income margin and net income margin remain largely stable for both its 3Q23 and nine months ended September 2023 (9M23). Its 3Q23's operating income margin is ~9%, and its net income margin is ~6%. Its 9M23 operating income margin is ~8%, and its net income margin is ~5%. When compared to 2022's result, it is in line, showing that margins are healthy and robust.

Its gross profit margin is looking really healthy. For 3Q23, gross profit margin is ~14%, while 9M23 is ~13.8%. In my earlier discussion under the 'historical financial analysis' section, I noticed that its gross profit margin contracted in 2022 to ~12.31%. As evidently shown, its gross profit margin has recovered to 2019-2021 level.

Overall, LNR:CA's top-line revenue growth continues to show strong momentum. In addition, bottom-line margins are consistent and show no signs of deterioration. As a result of these factors, LNR:CA's diluted EPS grew from $2.10 to $2.38 for 3Q23, which represents a year-over-year growth rate of ~13%. For its 9M23, diluted EPS grew from $5.17 to $6.47, which represents a year-over-year growth rate of ~25%. These EPS growth rates are looking really strong. As such, I believe its future EPS will continue to grow.

Author's Chart

{kind=link}

Growing Global Car Sales and EV Take-up Will Support LNR:CA Growth Outlook

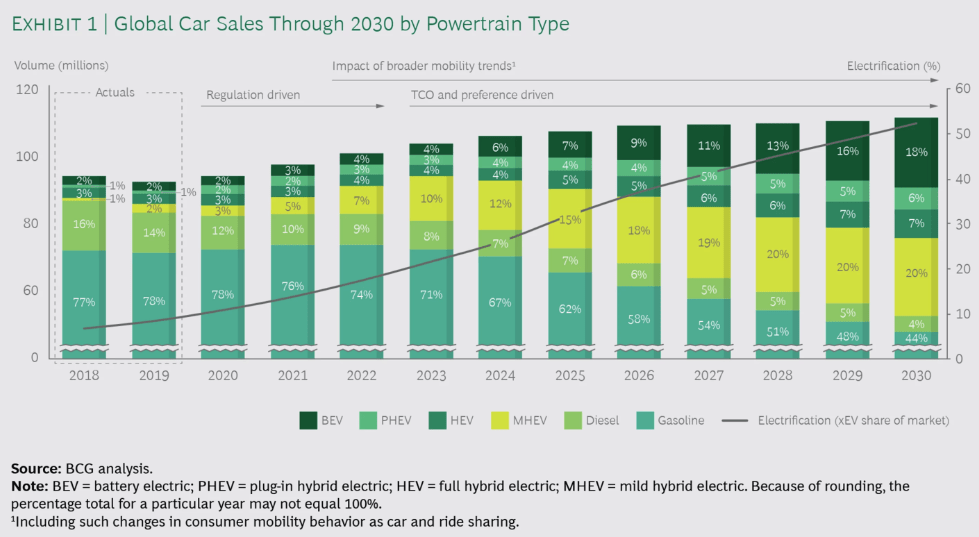

Based on the following chart , global car sales are expected to continue growing until 2030. As of 2022, the total volume is ~100 million, but by 2030, it is anticipated to reach ~110 million. Therefore, this anticipated growth in global car sales through 2030 will support LNR:CA's growth outlook for the next 7 years.

With more cars being sold, there will be more demand for car parts, and that is what LNR:CA is manufacturing and selling. Under its mobility products, it manufactures and sells products primarily for internal combustion engine ((ICE)) vehicles. For its eLIN product line, it caters mainly to electric vehicles ((EV)).

As you can see from the following chart, EVs are expected to account for ~56% of total car sales by 2030, and this represents an opportunity and also a threat for automotive parts and equipment manufacturers such as LNR:CA. If these manufacturers are unable to innovate and respond to this growing demand, they might become obsolete or face declining revenue in the near future.

In the case of LNR:CA, they have already developed their EV automotive parts and equipment capabilities, which is eLIN . Therefore, it is well prepared to not just capture growth in this EV sector but also prevent itself from becoming obsolete in this fast-changing automotive era.

{kind=link}

{kind=link}

{kind=link}

Acquisition of Mobex Will Strengthen LNR:CA's Business and Drive Long-Term Growth

On 1st November 2023, LNR:CA announced the completion of the acquisition of Mobex, a recognized Tier 1 supplier of automotive components. Tier 1 suppliers refer to companies that supply their products directly to original equipment manufacturers ((OEM)). Tier 1 suppliers work closely with OEMs to design and manufacture parts that meet specific requirements. Therefore, I believe this acquisition will greatly improve LNR:CA's access to and relations with OEMs, therefore allowing them to leverage this relationship for future business expansion. Therefore, I believe this acquisition will bolster its growth outlook.

In this acquisition, the assets LNR:CA will buy over from Mobex include Mobex's manufacturing operations, which specialize in the production of chassis, suspension modules, and components that are able to adapt to a variety of propulsion systems, such as ICE or EV. The strategic purpose of this acquisition is to improve LNR:CA's product offering range in all vehicle powertrain types, and there is a sound reason why it is doing so.

In my above discussion, I stated that EVs are anticipated to account for ~56% of total global car sales by 2030, which provides automotive parts and equipment manufacturers with both opportunities and threats. Through this acquisition, it will further strengthen LNR:CA's EV capabilities (existing is eLIN) and really position them well for the future market shift towards EVs in my view.

Relative Valuation Model

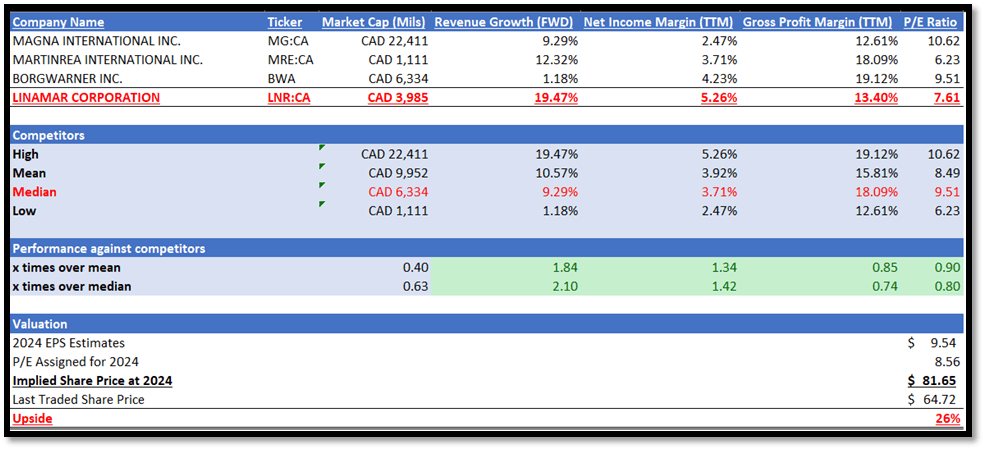

Based on LNR:CA's profile, it operates in the automotive parts and equipment industry; the list of competitors I used in my relative valuation model below also operates in the same industry. Therefore, it forms a good comparison basis.

Before I begin, please take note that all of the competitors listed are trading in Canada except for BorgWarner ( BWA ), which is listed in the US. I have converted its market capitalization into CAD to ensure an accurate comparison.

In terms of market size, LNR:CA is significantly smaller than its competitors. LNR:CA has a market capitalization of ~$3.9 billion vs. its competitors' median of ~$6.3 billion, which means that it is 37% smaller than them.

Despite its smaller size, it outperforms its competitors in terms of its forward revenue growth outlook and net income margin TTM. LNR:CA's forward revenue growth outlook is ~19.47%, while its competitors' median is ~9.29%. This means that LNR:CA's growth outlook is 2.10x larger than that of its competitors.

In addition to revenue growth outlook outperformance, LNR:CA's net income margin TTM of 5.26% also beat its competitors' median of ~3.71%, which is 1.42x over competitors' median. The impressive part is that LNR:CA did that with a lower gross profit margin TTM of 13.40%, while competitors' median is ~18.09%.

Despite a better forward revenue growth outlook and net income margin, LNR:CA's P/E ratio of 7.61x is trading below competitors' median of 9.51x, representing a discount of ~20%. When I looked at its 1-year historical P/E average, it was ~8.5x. Given these factors, LNR:CA deserves a higher P/E ratio. In order to remain conservative in my model, I am going to apply a 10% discount to competitors' median P/E ratio, which gives me 8.56x P/E.

The market revenue estimate for LNR:CA is expected to reach $9.64 billion in 2023 and $11.15 billion in 2024, and for EPS, the market estimate for 2024 EPS is $9.54. Given LNR:CA's strengths and growth drivers, which I have discussed in depth above, it supports these market growth estimates. In addition, these estimates are also in line with management's revenue guidance for 2023 and 2024. In the slides, management anticipates double-digit growth in revenue for both years.

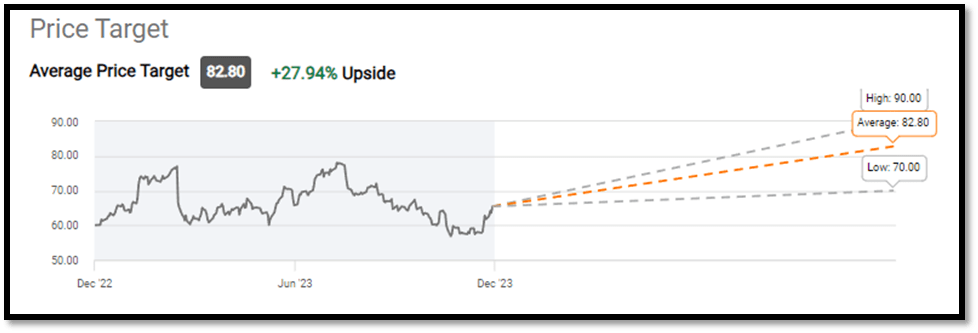

By applying my adjusted P/E ratio for LNR:CA of 8.56x to its 2024 EPS estimates, my 2024 price target is $81.65, and this represents an upside potential of ~26%. My price target is also in line with Wall Street estimates, thus giving me confidence in my model, as this provides a form of sanity check for my valuation model. Overall, I recommend a buy rating for LNR:CA.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Downside Risk

One downside risk of buying LNR:CA's stock is in regard to its SG&A expense management. As mentioned, management is managing these expenses to mitigate the effects of gross profit margin contraction. Managing SG&A effectively requires experience and foresight, as it requires striking a delicate balance between cost containment and sales support. Overly aggressive reductions in SG&A could potentially hamper top-line revenue growth. Furthermore, consistently reducing SG&A and interest expenses may not be a sustainable strategy in the long term. In my valuation model, my target price is driven by LNR:CA's superior forward revenue growth outlook. Should LNR:CA fail to meet market revenue growth expectations, there is a possibility that its share price could stagnate or even decline.

Conclusion

In conclusion, its past financial performance has shown strong revenue growth recovery after being impacted by the COVID pandemic. For the last 2 years, revenue has been growing in the double-digit range. Although its revenue growth trend fluctuated, its profitability margins have stayed robust throughout the years. In addition, its D/E ratio has also improved over the years, resulting in net interest expense reduction, which helps with its margin.

For the next few years, the global car sales market is anticipated to continue growing robustly. EVs are expected to gain more market share annually, and by 2030, they are estimated to account for more than half of total car sales. I believe LNR:CA is well prepared for this market transition, as it is already providing automotive parts for both traditional powertrains and EVs. In addition, it acquired Mobex to further strengthen its offering range in all vehicle powertrain types.

In my conservative relative valuation model, I revealed that LNR:CA is trading at a lower P/E despite outperforming its competitors in terms of growth outlook and profitability. With double-digit upside potential, I am recommending a buy rating for LNR:CA.

For further details see:

Linamar: Strong Global Car Sales And Mobex Acquisition Should Strengthen Growth