LINC - Lincoln: A Great Investment Opportunity In 2023 And Beyond

2023-03-09 04:43:05 ET

Summary

- Strong FY2022 results and a turnaround in the last couple of years prompted me to look into the company further.

- The management is very optimistic about the future and sees a lot of growth in the next 5 years with many corporate partnerships in store to attract more students.

- The financials are solid and look much better than they did just a few years back.

- Even with conservative growth estimates, the company is a buy at these levels for the long-term investor.

Investment Thesis

The FY2022 results and optimism from the management about the future of Lincoln Educational Services ( LINC ) have prompted me to look into it further to see if what the management is saying about rewarding their shareholders, in the long run, is good enough to start a small position right now. A great path to further expansion and even my conservative estimates of the future growth of revenues shows me that the company is very well managed, can generate great cashflows after the aggressive expansion into a hybrid model, the company is a buy at these levels and would expect to be rewarded quite well in the next 5-10 years the management achieves their goals.

Briefly on FY2022 Results

The company managed to beat estimates even in this low unemployment rate environment. Revenues were 4.5% higher than last year. Not the highest increase, but it is still good considering the environment we're in. Net income came in at 12.6m, lower than last year due to a substantial increase in costs associated with higher staffing and transition into the hybrid model. The management expects this to keep up in the next year also until the hybrid model comes into full effect, and after that, the efficiencies will start to come through to increase profitability over the long run. The company managed to increase the graduation rate to 68.8% and the graduate placement rate to 81.6%.

Promising Growth Prospects

Forward guidance is what caught my attention. The management was very optimistic about what the future holds for them and is seeing a rapid expansion into more locations and further adoption of the hybrid model that will, in the long run, be more efficient and drive profit margins higher.

The school has many partnerships in place that can attract potential students to enroll in their training programs. The big one I see that has already started is the partnership with Tesla ( TSLA ) to train more EV Technicians . The school has an advantage here because it will only be 1 of 6 schools to offer this program in the western US. Tesla is one of the most popular companies in the world and has a lot of fans. I could see this being a very popular training program.

Besides that, they also have an intense program pathway with Johnson Controls ( JCI ). With 81.6% of graduates being employed, the school seems to have quite a desirable demographic for employment in all sorts of different industries.

The management also is trying to expand the nursing and allied health programs at the school, with a very smart decision to welcome on board a veteran of the industry Sylvia Chen who was the CEO and President of HCA Healthcare's Continental Division for over a decade. She will bring a lot of expertise which will no doubt help the segment grow organically and provide highly skilled workers to the economy.

The school is looking to expand to five more locations to accommodate an increase in demand over the next 5 years. I would say they assume a recession will come in the next 12-24 months and I believe the school would benefit from a recession as schools tend to see an uptick in enrollment during higher unemployment times because people want to become more skilled or re-train themselves so they wouldn't be in as much of a risk of getting fired the next time around. The programs that Lincoln Tech offers I believe are highly valuable to employers and the students will be able to become more resilient in the workforce after graduating.

Over the next couple of years, the aggressive expansion will affect their profitability, however, the management is very confident that the new hybrid model and all the partnerships with companies and new locations will eventually yield much more profit. The management is convinced that the new initiatives that will roll out at their full capacity are going to return $1m in profits annually after 3 years as per the earnings transcript.

The growth catalysts are quite impressive I have to say, and I do think that the school will be able to attain these numbers in the future. The hybrid work model will become more efficient as time goes by which will increase their margins, however, it is still early in the adoption stage of it and we will have to wait for the next couple of earnings seasons to see how well the management has implemented all these initiatives. It is also quite interesting to see that a recession might help the school in achieving better results, but I suppose a lot of educational institutions will benefit from that and Lincoln Tech could be a standout if the programs that they offer to people are desirable and manage to retain students in the long run.

Financials

While I was looking for a small cap company to cover, Lincoln popped up on my stock screeners presets and the reason I wanted to cover this company is that the books have been quite well kept and the metrics have turned positive after being deep in the negative territory for many years, signaling a potential turn around.

The first thing that stood out to me is that the company has no debt on its hands. They paid off the debt completely in the last 2 years, which shows the management's priorities for keeping the books clean and efficient. They are looking to add a new credit facility to fund their future growth prospects, but we don't have any more information on that. I believe this is a smart move and the management seems very competent seeing how clean the balance sheet looks. They are also in the process of selling their Nashville Campus which will get them around $35m in gross proceeds.

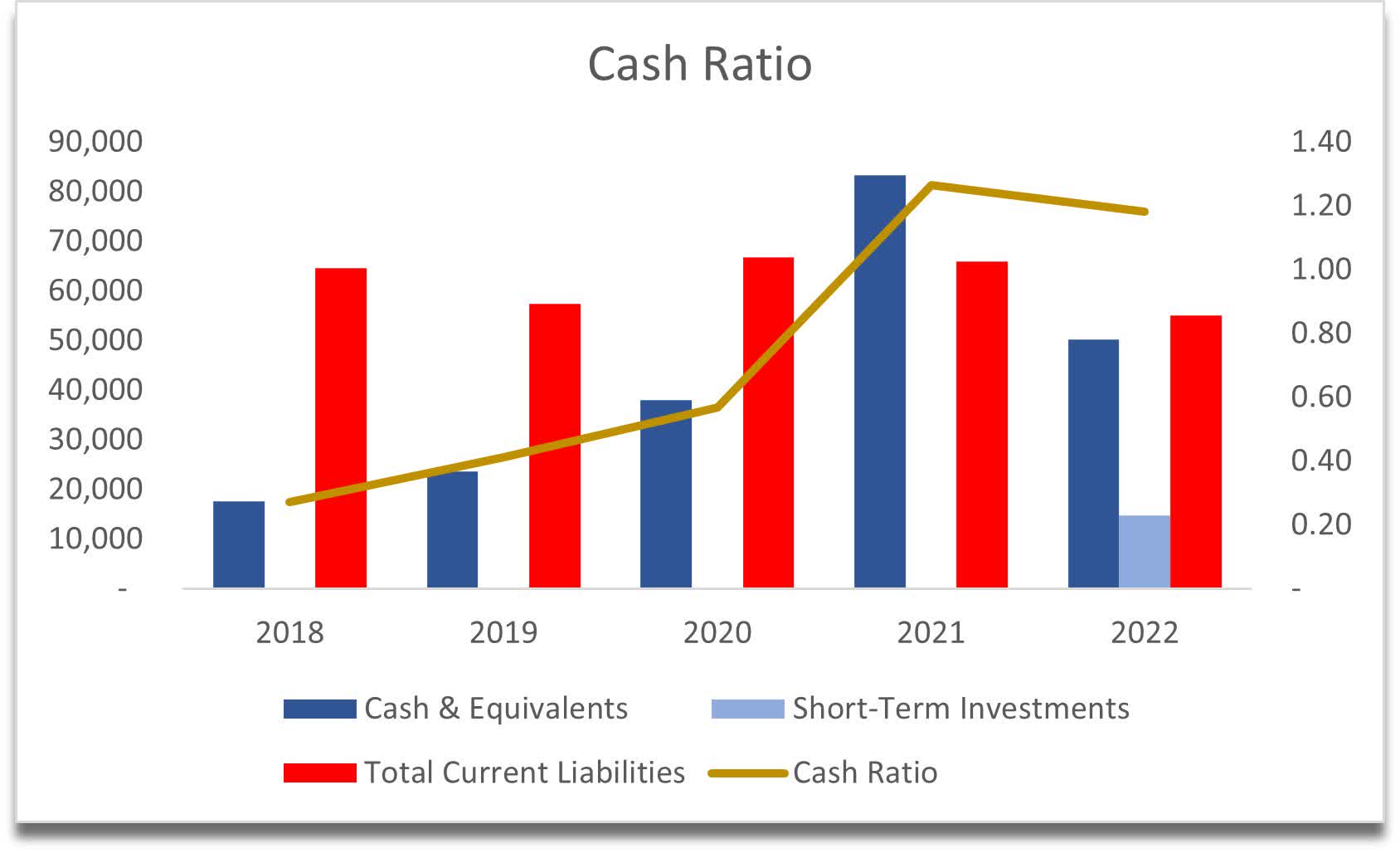

The company is also very liquid. The cash ratio: the stricter way of measuring liquidity which looks at the cash available and short-term investments to see if the company can pay off its short-term obligations, Lincoln is currently sitting at 1.18 meaning it can pay off all its current liabilities with ease. This was not the case before and I would be happy if this trend continued.

{kind=link}

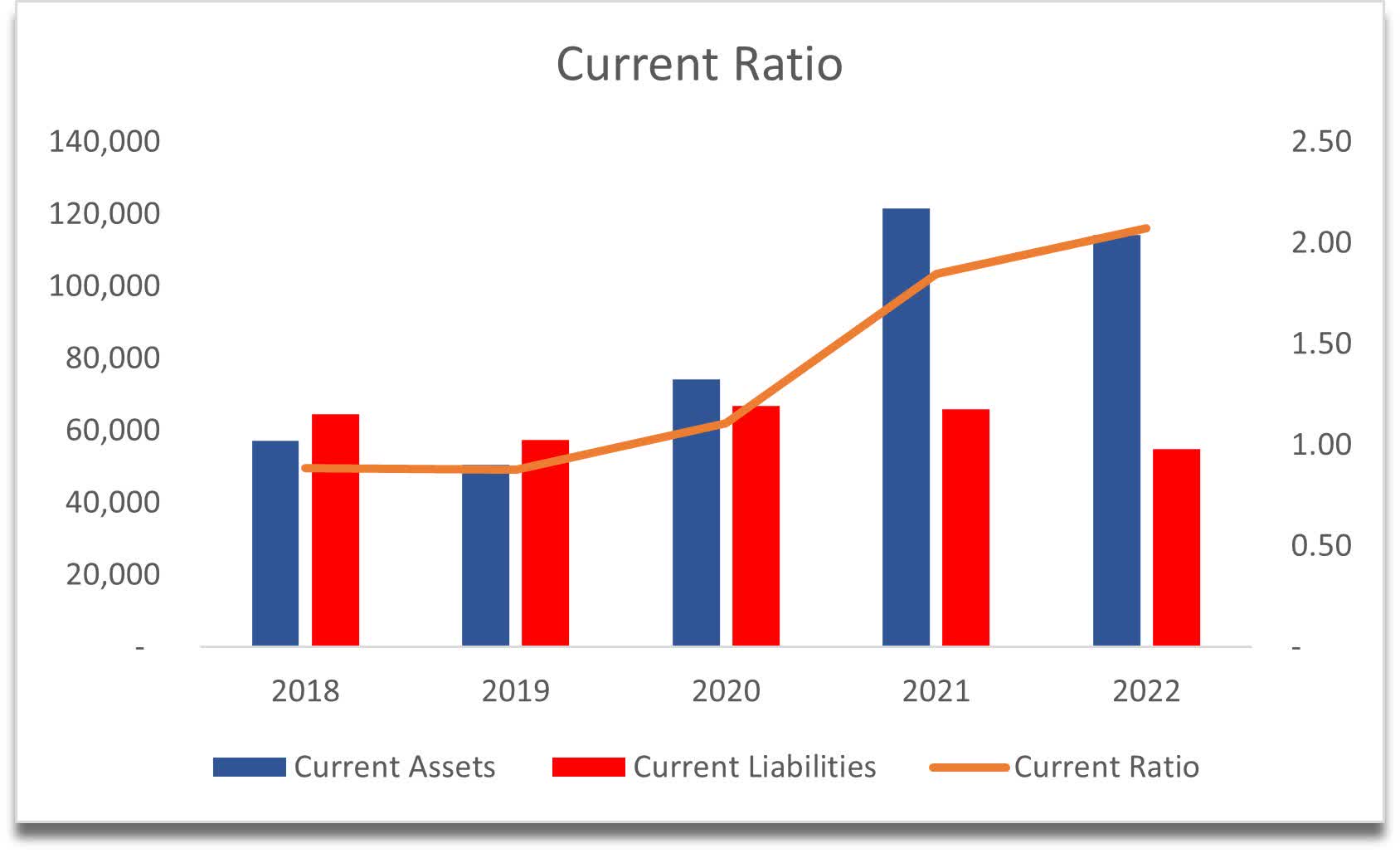

In the same fashion, the current ratio has become acceptable in the last couple of years, and would like for the ratio to increase or at least stay stable above 2 as that is my desired liquidity threshold.

Current Ratio (Own Calculations)

{kind=link}

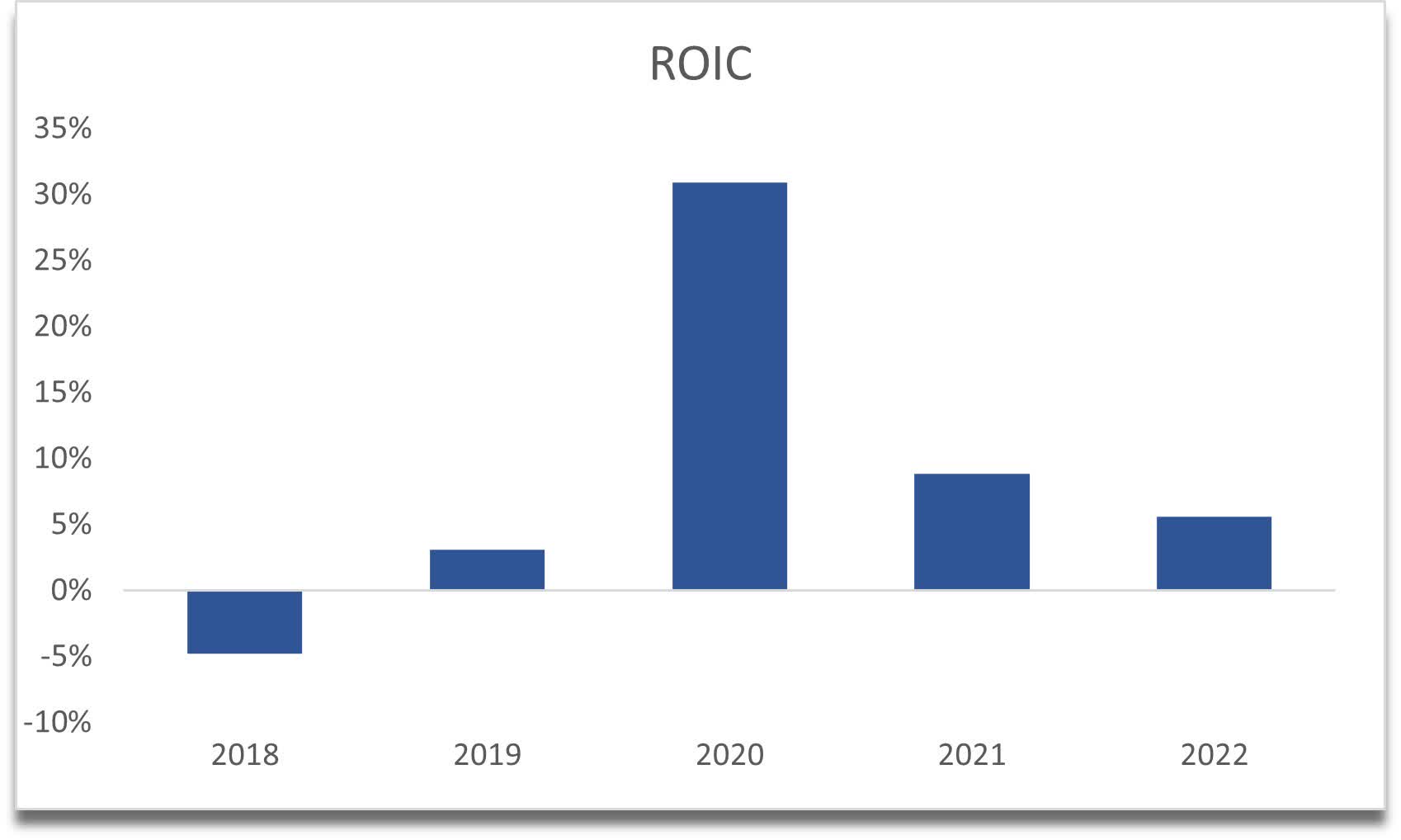

The return on invested capital is nothing to brag about, however, it is positive, and I would expect it to increase after all the expansions and efficiencies take place in the next few years. The outlier here is the 2020 figure where the company had a huge tax benefit.

{kind=link}

Overall the management has improved the company's books quite considerably and it became a profitable business in the last few years which will continue to be so in my opinion. Now the next thing to look at is how much an investor should be paying for the growth the company will see in the next 5 years.

DCF Valuation

As I mentioned earlier the management is very optimistic about the growth of the school, however, I am more of a conservative when it comes to valuations. I will present 3 different cases, a conservative case, a base case, and an optimistic case. The figures for the conservative and optimistic cases will be derived from the base case.

The management is very confident that EBITDA will double from 2022 to 2025. I won't be that confident and make my estimates more conservative. In my base case, I have a 42% increase from 2022 to 2025. I just could not be as optimistic as they are mainly because I'm a pessimist and cannot take the word of the executives at face value, they would be biased obviously as it is their company. It would be great to be proved wrong, however, I will stick to my conservative growth estimates and if the company is still a buy then we are getting a good deal.

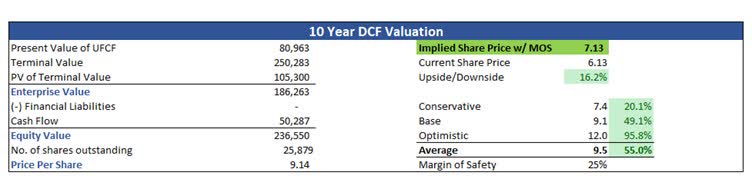

I went for quite a simple growth outlook for the base case, where average growth is only 2% per year for the next 10 years. The optimistic case goes up to 4% a year and the conservative case is flat. This will give me a range of possible outcomes for the company. It seems like the company can generate quite a good FCF and even at such low growth estimates, it will reward its shareholders in the future. To be even more on the safe side of the valuation, I added a 25% margin of safety to the implied share price, which shows that the intrinsic value of the company is $7.13 implying around 16% upside from the current valuation.

10-year DCF Valuation (Own Calculations)

{kind=link}

Conclusion

Solid growth potential, great FCF generation, competent management, and even my conservative estimates tell us that this is a good time to invest, and I do believe that this educational company has quite good prospects in the future, if partnerships with the companies like Tesla, Johnson Controls and other corporations bear fruit then this institution will be at the forefront of desirable skilled workers in the US that will be more resilient to downturns in the economy.

If we do see a recession coming in the next 12-24 months, where the unemployment rate ticks up slightly, I see Lincoln benefiting from this as more people will want to become more skilled and therefore more employable in the future once the recessionary period has ended. I will monitor what the Fed will do in the upcoming months and will think about opening a small position to start with as I do believe the company will reward its shareholders in the long run.

Of course, there is also the risk that all these growth prospects that the management mentioned do not come to fruition and they are not able to attract and retain more students in the future, which could throw all the modeling out the window. So far, we do not know what will happen and we will have to wait and see how it all develops in the future.

For further details see:

Lincoln: A Great Investment Opportunity In 2023 And Beyond