PNR - Lincoln Electric Holdings: Getting Better But Not There Quite Yet

Summary

- Lincoln Electric Holdings has done really well in recent months, both fundamentally and from a share price perspective.

- Long term, the company should continue to fare well, and shares have gotten cheaper from a valuation perspective.

- But it's not an ideal prospect quite yet and needs to either pull back or see stronger fundamental growth to warrant a bullish rating.

In order for such a massive economy to exist and for such a large global population to thrive, there must be infrastructure, tools, and other physical items to make everything come together and work for the greater good. At the end of the day, all of this requires a great deal of physical 'stuff', much of which needs to be created from or assembled with various parts. One company dedicated to helping make this a reality is Lincoln Electric Holdings ( LECO ), an enterprise that provides its customers with a large line of welding, cutting, and other related products. From a purely fundamental perspective, the firm has done quite well as of late. In response to that, shareholders have benefited nicely. But this does not mean that shares deserve meaningful upside relative to what the broader market deserves. Considering how shares are priced, I would make the case that the company is a solid 'hold' candidate at this time, but it wouldn't take much more for it to be upgraded to a 'buy'.

Great performance

Back in the middle of September 2022, I wrote an article that took a rather neutral stance on Lincoln Electric Holdings. In that article, I talked about the strong growth the company had been exhibiting on both its top and bottom lines. For the most part, I felt as though the company's health was impressive and I believed that it had a bright future ahead for it. But because of how shares were priced, I felt as though there were better prospects for investors to consider. This ultimately led me to rate the company a 'hold' to reflect my view that shares should generate returns that would more or less match the broader market over an extended period of time. So far, the market hasn't exactly agreed with my thoughts. While the S&P 500 has dropped by 4.9%, shares of Lincoln Electric Holdings have generated upside of 4.8%.

{kind=link}

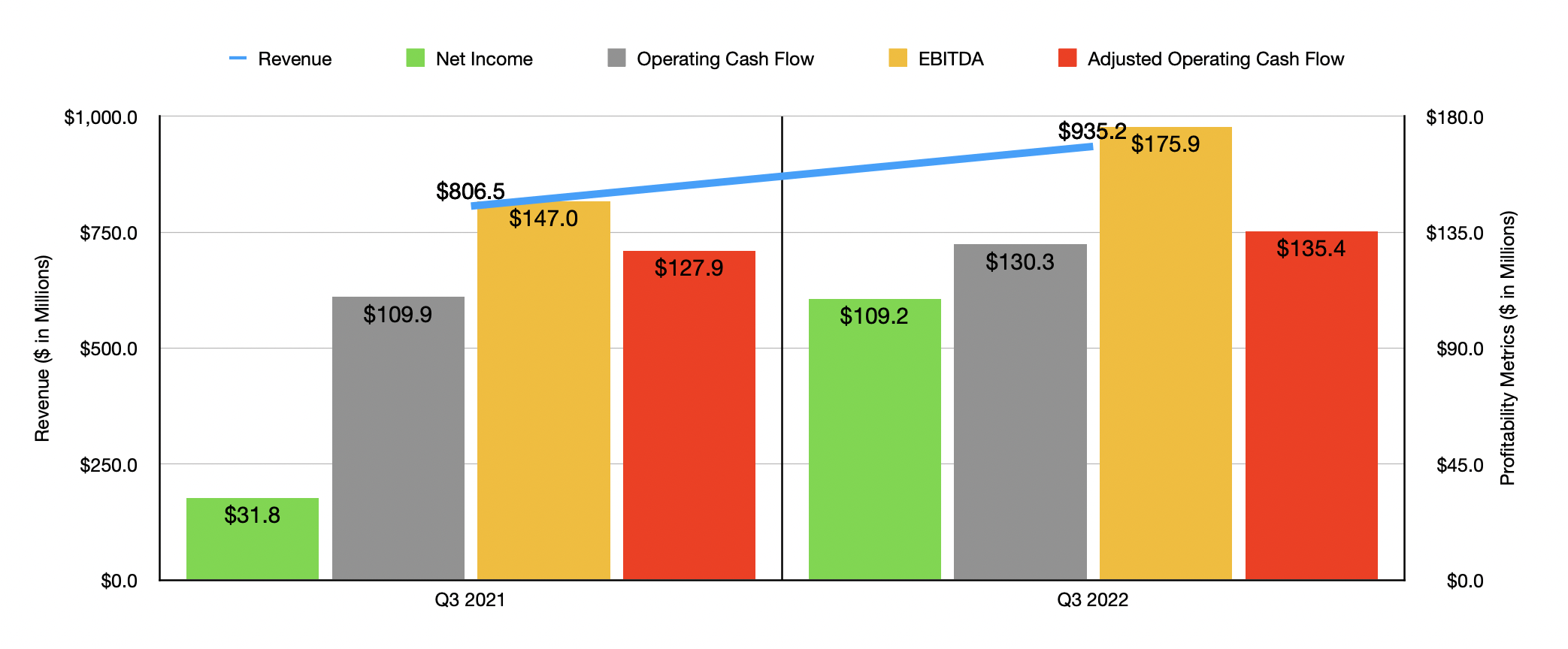

The key driver behind this upside is the robust growth the company has been demonstrating. To see what I mean, I would like to point out financial results covering the third quarter of its 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about the firm. During that time, revenue came in at $935.2 million. That's 16% higher than the $806.5 million reported one year earlier. During that three-month window, the largest contributor to the sales increase was increased pricing. This added $100.7 million to the company's top line. Higher volume added another $71.1 million, while acquisitions contributed $10.3 million. Unfortunately, some of this was offset by a $53.4 million impact associated with foreign currency fluctuations.

{kind=link}

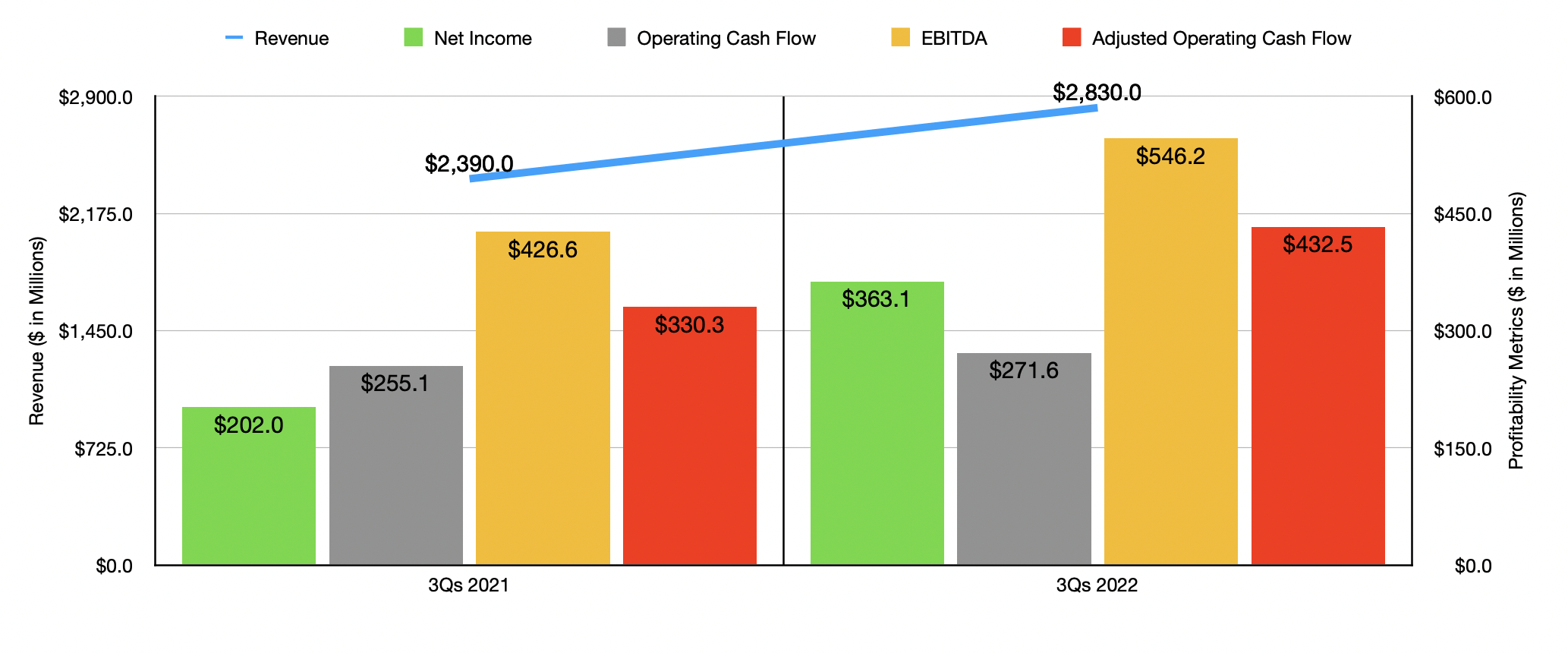

Profits for the company also managed to rise nicely. Net income soared from $31.8 million to $109.2 million. Operating cash flow rose more modestly from $109.9 million to $130.3 million. If we adjust for changes in working capital, the increase was even smaller, with the metric rising from $127.9 million to $135.4 million. Over that same window of time, we also saw EBITDA improve, climbing from $147 million to $175.9 million. When it comes to the first nine months of 2022 as a whole, sales of $2.83 billion beat out the $2.39 billion reported one year earlier. Once again, higher pricing was the biggest driver here, accounting for $385.4 million worth of the sales increase. Profits almost doubled from $202 million to $363.1 million. Operating cash flow rose from $255.1 million to $271.6 million, while the adjusted figure increased from $330.3 million to $432.5 million. And over this same window of time, EBITDA for the company expanded from $426.6 million to $546.2 million.

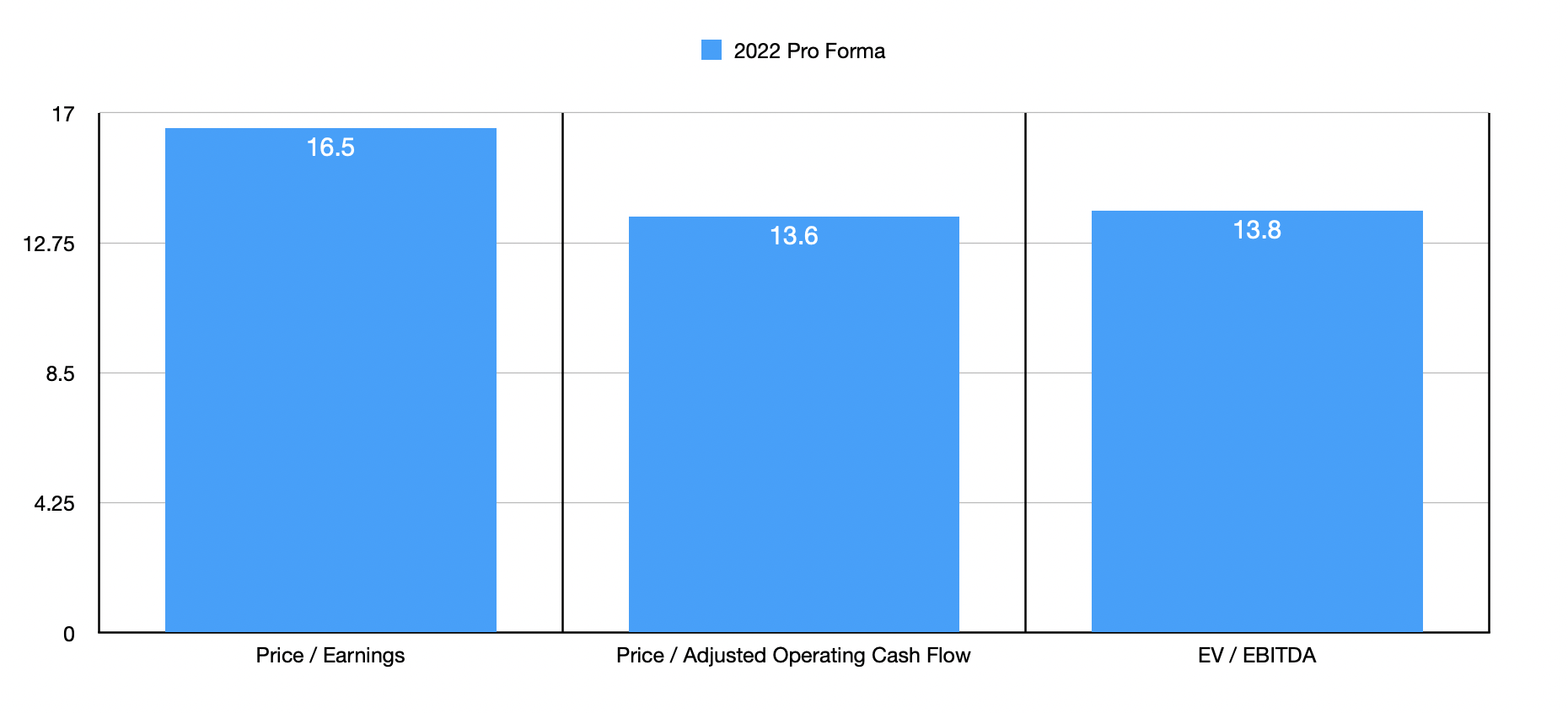

We don't really know what to anticipate for the 2022 fiscal year in its entirety, since management has not provided any real guidance. But we do know that the picture has been made more complicated by the fact that the company recently made an acquisition in the amount of $427 million. That purchase alone should increase sales by $225 million and benefit earnings per share in 2023 by between $0.12 and $0.15. At the midpoint, this would imply additional net profits of $7.8 million. $400 million worth of the purchase price was made using a term loan with an estimated interest rate of around 5%. The actual number was just under that, but I rounded up to be safe. Taking all of this into consideration and annualizing results experienced in the first nine months of the year, we should anticipate net income for 2022 on a pro forma basis that accounts for the purchase as though it had been completed at the beginning of the year, of $504.8 million. Adjusted operating cash flow should be $611.3 million, and EBITDA should come in at around $683.2 million.

{kind=link}

Based on these figures, the company is trading at a forward pro forma price-to-earnings multiple of 16.5. The price to adjusted operating cash flow multiple would be 13.6, while the EV to EBITDA multiple would come in at 13.8. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 14 to a high of 63. In this case, only one of the five companies was cheaper than our prospect. Using the price to operating cash flow approach, the range was from 21.7 to 67.6. In this case, our prospect was the cheapest of the group. And finally, using the EV to EBITDA approach, the range was from 12.2 to 31.9. In this case, three of the five companies were cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Lincoln Electric Holdings |

| 16.5 |

| 13.6 |

| 13.8 |

| The Middleby Corporation ( MIDD ) |

| 18.3 |

| 29.7 |

| 13.0 |

| Pentair ( PNR ) |

| 14.0 |

| 21.7 |

| 13.4 |

| RBC Bearings ( ROLL ) |

| 52.2 |

| 40.4 |

| 31.9 |

| Chart Industries ( GTLS ) |

| 63.0 |

| 67.6 |

| 26.9 |

| Dover Corporation ( DOV ) |

| 16.8 |

| 24.7 |

| 12.2 |

Takeaway

All things considered, I will say that I remain impressed by the fundamental performance achieved by Lincoln Electric Holdings. The company has demonstrated impressive pricing power and has managed to grow sales, profits, and cash flows all nicely in what is admittedly a difficult market. Long term, I suspect the company will do quite well. But shares are not quite cheap enough at this moment to warrant a 'buy' rating just yet. If the stock falls a bit from here or if fundamentals improve further, that opinion could easily change. But for now, I feel more comfortable with a 'hold' rating.

For further details see:

Lincoln Electric Holdings: Getting Better But Not There Quite Yet