LNC - Lincoln National: Oversold Due For A Big Bounce 6.2% Dividend

Summary

- 5.8% Dividend Yield. Stock pullback is an attractive entry at E23 PE of 3.3.

- COVID-19 claims are decreasing, and earnings hit now behind the company.

- Record of steady growth in earnings and dividends. Secure $1.80 dividend payment is easily covered by E23 EPS of $9.10.

- Portfolio yield increases will have a positive impact on earned interest and allow for more favorable product pricing.

- New CEO, renewed management direction.

Investment Thesis

Lincoln National Corporation (LNC) is a provider of retirement, insurance, and wealth protection products with approximately 16 million customers.

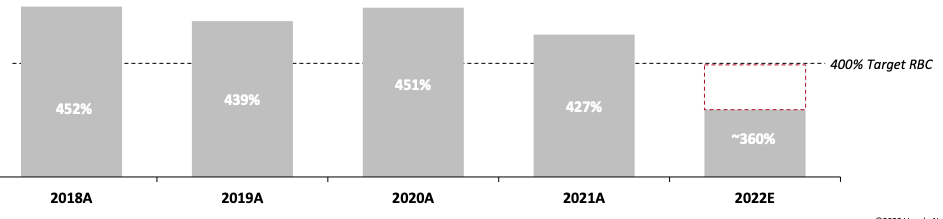

LNC expects RBC (Risk Based Capital) Ratio of 360% for end of year 2022. The strategic and long-term target for this ratio is 400%. RBC Ratio is a measure of total capital, cash and investments on the company's books, divided by the Required RBC minimum to meet regulatory statutes. This means that LNC has approximately 3.6x the capital on hand required to be considered solvent by regulators.

LNC stock has collapsed from its $74 per share high as the company took large, $2.3 billion, impairments to the life-insurance portfolio. However now, COVID-related claims are down, and the top line is still expanding. With a new CEO that took control in May, LNC has renewed its focus on increasing the margin of operations and streamlining costs to contribute to higher cashflows. We expect EPS to regain its growth form in 2023.

We believe that this temporary impairment to a single segment of the company has caused a significant overselling of LNC's shares compared to a long-term outlook for a high-quality business. We believe that we will see a significant price recovery in 2023 as LNC's normalized earnings power reasserts itself.

Estimated Fair Value EFV

P/E 8.0x times 9.20 E23 EPS = $73.60

Our PE number errs toward the lower end of the financial sector for peers in a similar financial situation, of which the current sector median is roughly 10x with a range of 7-13x.

Capital Targets and Impairment

In FY22 RBC fell below the 400% target, dropping to an estimated 360% for the end of year. It began the year at 427% . As a result, LNC will be taking certain actions to accelerate the return to capital targets.

LNC Investor Presentation November 2022

{kind=link}

The updated 3Q22 actuarial update estimates a $2.3 billion net income impairment from life insurance. $550 million in capital impact related to this is to be expected to be realized for 4Q22 with an ongoing $180 million run rate impact. The largest impairment at $1.8 billion is to policyholder behavior. Typically, as individuals get older, they allow their life insurance policies to expire without renewal. However, with COVID-19 proving to be far more persistently fatal amongst the older segment of the population, many policyholders have opted to extend their term plan or opt for whole life. LNC estimates that consumer behavior in renewing whole life has put a 22-point impact to RBC numbers but stresses that there is no cash flow impact.

However, a new industry study has changed the assumption that LNC's life insurance division was operating on. The 2020 and 2021 revisions for policy count for 75+, the typical age group at which policies lapse, were increased. Of the 128,000 total policies on the books in this category, LNC estimates roughly 10,000, 8%, additional policies are on the books that would have otherwise lapsed. These additional policies in the assumption make up the lion's share of the ongoing run-rate impacts, as LNC will need to keep additional reserves on hand.

LNC Supplemental Presentation (Nov 22)

Market volatility, persistent COVID-based mortality, and heavy losses in the fixed-income portfolio have significantly impaired the portfolio over the latter half of 2022. Share buybacks are paused, but management stated that the common dividend would be maintained at its present level. Further actions including consumer-sided pricing actions, usage of reinsurance, and restructuring the debt-equity mix to more hybrid or preferred shares rather than senior debt and common shares are actions management is taking.

Products

LNC's strategy maintains a level of fluidity to create adequate risk-adjusted returns. This is done through the "reprice, shift, new" framework published by management. It is best boiled down as repricing underselling products, shift sales toward products that have the best demand-weighted returns, and adding new products that may fit a niche.

The weighted average duration of assets in the portfolio is 8.5 years, 13 years for life insurance, and 5.0 years for annuities.

Despite unfavorable markets, the annuity lines have performed as expected, with a return on equity (ROE) of 18% reported in 3Q22 and a 0.68% return on assets (ROA).

LNC Investor Presentation November 2022

Overall, risk levels for annuities of all types are consistently below peers in net amount at risk (NAR) divided by account value ((AV)). As of the end of 1H22 LNC had 4.1% for guaranteed minimum at-death policies and 5.3% for guaranteed living benefits policies. In these percentages, the lower number is better, as they represent the difference between the face value of the plan that LNC would have to pay out versus the amount that the insured has paid into the plan plus accumulated earnings on the accounts invested premiums.

Favorable interest rates amongst annuities have also increased earnings expectations by $217 million.

Life insurance was hit hard by COVID-19 with mortality rates being 115% (calculated by actual deaths to expected) for 2020 and 2021. 2022's mortality rate remained higher than expected at 109%. As previously discussed, LNC had to resets their expectations for lapses and cashouts for life insurance. LNC estimates that 75% of impairment to the RBC was related to life insurance. Despite this adjustment, higher interest rates, decreasing pandemic claims, and a revamped portfolio have created an environment conducive to a robust in-force business. 3Q22 sales have grown 3% year over year and are still expected to achieve the targeted 12% return profile.

Retirement planning services have been relatively unaffected by COVID and have seen solid results despite poor market performance and high fixed-income losses. Sales have grown by 34% year over year with a 7% increase in recurring deposits into accounts.

Group protection is the smallest market but is well positioned to be strong through periods of volatility with contracts tending to be variable and renegotiated every 1-3 years. Premiums have gone up 8% year over year, with LNC increasing new sales on group protection products by 83% year over year.

"Spark" Cost-Streamlining and repositioning

The name of the company-wide efficiency initiative is "Spark", which is projected to have $300 million in savings by 2024. Around 45% of this saving has been realized to date . The program seeks to reposition toward a more remote workforce and cut down on operating costs through automation and digitization of services.

Group protection and retirement services are taking a more forward role in the long-term strategy. LNC is targeting a 5-7% margin which if realized would significantly aid in capital generation. Most of the margin expansion can be attained through optimizing a sales mix that leans toward higher-margin products, and pricing actions to counter any additional COVID-19-related claims.

Additional savings can be realized by shifting sales mix across the company toward shorter-term products which are far less sensitive to interest rate swings. The weighted average duration of assets has fallen by half a year since 1H22 to 13 years. The decrease in asset duration helps create capital efficiencies without sacrificing consumer satisfaction.

Risk Profile and Financial Health

97% of investments are in NAIC-declared investment-grade assets, 60% being rated A or higher. Solid credit quality combined with sector diversification produces a strong portfolio. There have been significant losses to the fixed-income portfolio which accounts for almost 80% of total assets. Most of the losses experienced are because of interest rate impacts, and LNC states that ratings movements of assets within the portfolio are trending upward. Though it is important to note, insurance companies are almost exclusive buyers to maturity, not traders. While there is a significant effort for insurers trying to find better yields in alternate investment classes , it is unlikely that any of the unrealized losses on the portfolio will actually be realized before maturity.

LNC purchases reinsurance for some of its policies in the form of both block and flow. Flow reinsurance being a percentage of future sales being reinsured and block being a pool of policies that already exist being sold to a reinsurer. The most recent deal is the Talcott VA flow agreement , which is up to $1.5 billion in sales from 2Q21-2Q23.

Reinsurance block transactions may increase to reduce the capital required for the life insurance business. Block reinsurance on more of its life insurance policies would move the risk for these policies to the reinsurance entity thus reducing the RBC minimums and increasing the RBC ratio. Moreover, this increases the credit quality of LNC but lowers future expected profits. Lower future profits make LNC reluctant to increase its reinsurance. Fortunately, if LNC shows a strong recovery in earnings in 2023, additional reinsurance will most likely not be necessary.

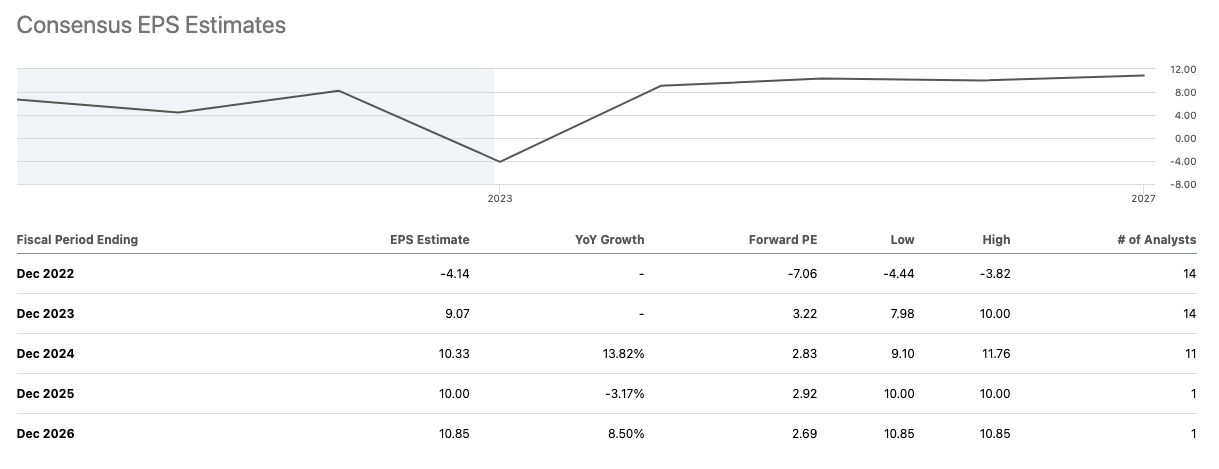

Management is assuming that if interest rates stay in their present neighborhood of around 3.5%, roughly $225 million will be recovered from the $550 million impairment by the end of 2023 . The LNC holding company has $750 million in cash on hand, with $300 million marked for debt repayment in FY2023 with an additional $200 million maturing in FY23. The dividend payments are running at $300 million per year. LNC does not want the holding company to have less than $450 million in cash on hand and would likely draw from the credit facilities if earnings prove to be persistently weak. However, management states that they will continue to maintain cashflow-focused transactions and pricing actions, rather than a more aggressive form of RBC ratio recovery. Increased cash flow is a positive development and will contribute to stronger earnings in the future. We do not believe that LNC will have to draw from the credit facility, with earnings expectations returning to the mean or higher for FY23. Current estimates on Seeking Alpha are sitting at $9.10 for FY23.

{kind=link}

Risk

In our last article , we stated that the most pressing risk to LNC was persistent COVID-19 morbidity. While morbidity remains high at 900bps above the pre-pandemic baseline, the most major risk is long-term assumption risk. As shown in 3Q22, consumer behavior in regard to long-term life insurance products has shifted drastically because of COVID-19, and it is difficult to gauge the persistence of this shift.

Fixed income losses jumped higher with interest rates increases, and LNC has incurred $9 Billion in unrealized losses on the portfolio related to this. As previously discussed, insurance companies are buy-to-maturity debt holders and will generally not recognize losses and will hold to maturity when they are paid back at par.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Lincoln National: Oversold, Due For A Big Bounce, 6.2% Dividend