LNC - Lincoln National: Returning 14% And Worth A Look

2023-07-28 17:04:53 ET

Summary

- Lincoln National is trading at an attractive historical valuation due to concerns about bond losses and profitability.

- The pessimism is priced into the shares, making it a reasonable time to enter the market.

- Selling put options on Lincoln National is I think the best way to play the stock into earnings.

- By doing so, traders can generate returns from event-based volatility. High-probability trades in the market right now are yielding close to 14% annualized.

- If assigned, put sellers will be assigned a durable insurance company at a great price.

Lincoln National ( LNC ), a leading player in the insurance and retirement solutions industry, is currently trading at an attractive historical valuation due to investor concerns about bond losses and plummeting profitability. Despite these concerns, we think that the pessimism is sufficiently priced into the shares, and now could actually be a good time to think about entering the story.

As we expect that profits and sentiment have bottomed, and with earnings around the corner, Lincoln National seems like a perfect platform for shrewd investors to sell put options on, in order to generate returns from event-based volatility. In the case that these put options are assigned, buying into this well priced, durable insurance company at the current multiple seems like a win-win opportunity.

Financial Results

As we just mentioned, Lincoln National has had some issues recently with its financial results.

At this point, these issues have been well covered elsewhere, but they're still important to mention because they affect the stability of the company into the future.

In short, Lincoln National has experienced a similar problem to Silicon Valley Bank, where the rapid rise in interest rates in 2022 and 2023 has led to large losses in the firm's Available for Sale, or "AFS" book. These losses have totaled nearly $10 billion. Lincoln national doesn't face a significant duration mismatch, which means that this move likely won't lead to insolvency.

However, it should have an impact on earnings, as fellow Seeking Alpha contributor Harrison Schwartz explains in his recent article :

Unlike banks, most insurance companies cannot place securities in the "held to maturity" category, where they do not need to realize bond devaluations. Most insurance company assets are "available for sale" because insurance providers are expected to sell many of their holdings as benefits.

One interesting example is Lincoln National Corporation, which has seen a ~$10B asset devaluation due to declines in the value of its fixed securities assets. Most of those securities are corporate bonds ($80.5B today), with most due after ten years - giving them exceptionally high duration price risk exposures.

Over time, LNC's cash flow will be impacted by these losses as it is generally likely to sell those assets at a loss unless long-term Treasury yields fall back to extreme lows over the coming years.

In other words, Lincoln National will need to sell a good chunk of its holdings over time. On these bonds, the firm will likely lock in a loss.

Sure, this drop in value has led to a precipitous decrease in tangible book value, but the real concern has to do with future earnings.

In effect, LNC took in premiums and bought fixed income securities. The value of those securities went down, and now they will need to slowly sell them at a loss in order to pay out liabilities.

The good news is that LNC will be able to stagger sales depending on market conditions, and liabilities seem spread out well into the future.

That said, it's a massive opportunity cost, and will likely impact buybacks, dividends, and returns to shareholders.

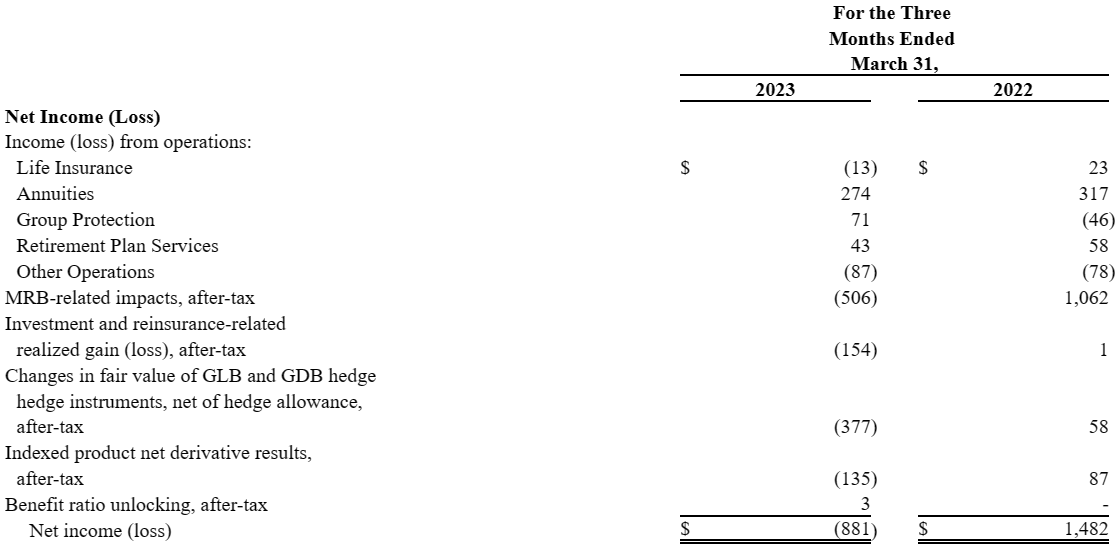

This earnings overhang has also been exacerbated by increased mortality costs post-Covid.

Check out the increase in MRB related costs YoY:

{kind=link}

10Q

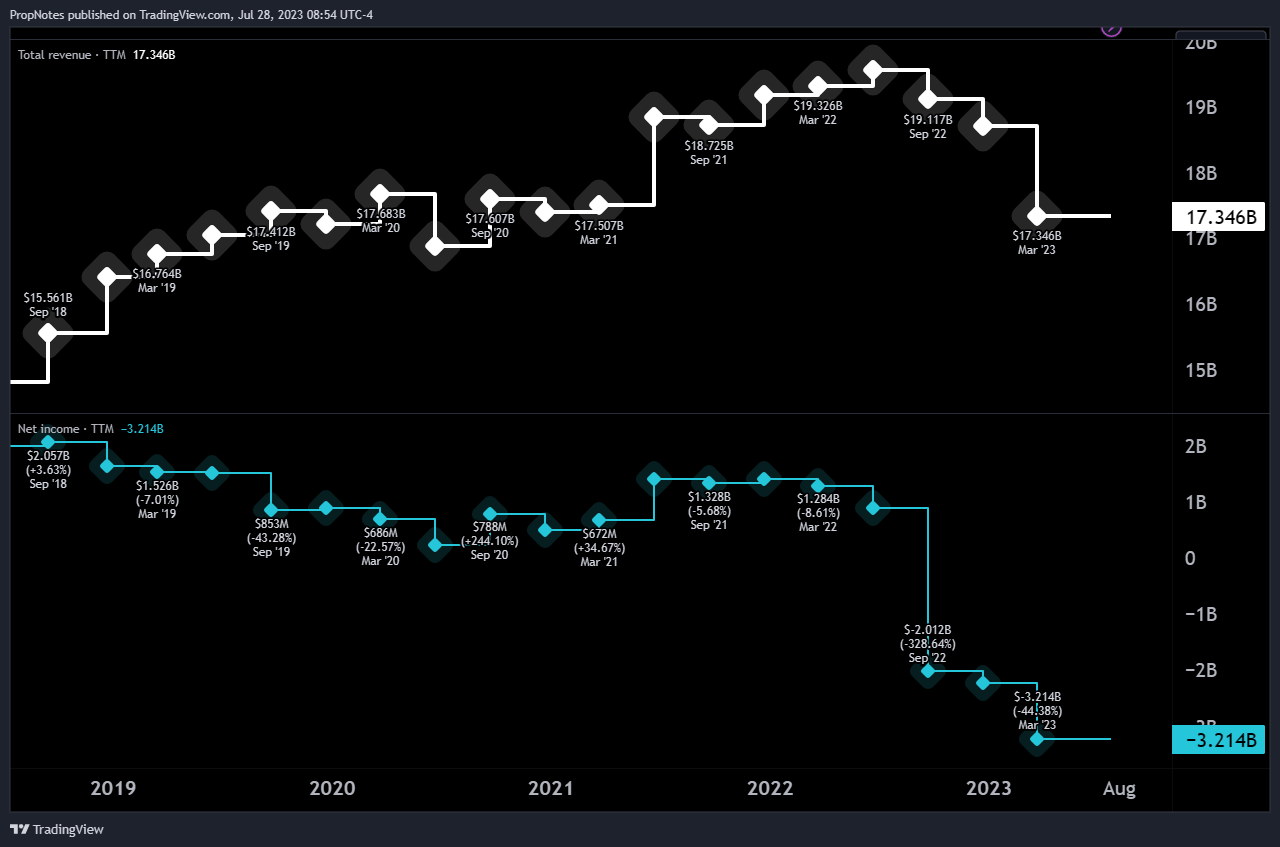

This increase in policy costs has overflowed above top line sales, causing huge TTM net income losses:

{kind=link}

TradingView

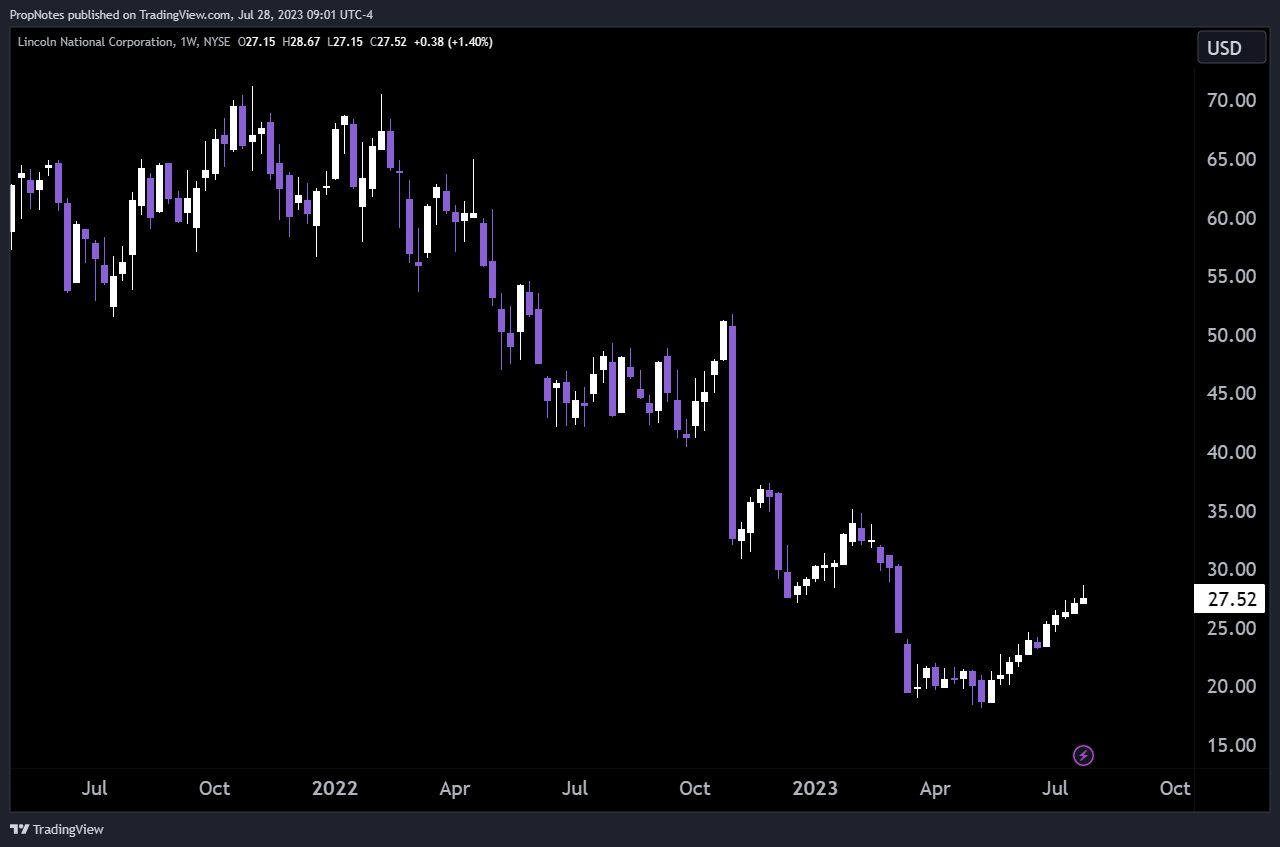

This, in combination with the hit to book value, has caused the stock to sink:

{kind=link}

TradingView

However, not all is lost.

Zooming out somewhat, I think it's clear that the company has a track record of strong operating profits, which we expect will continue into the future as things normalize, even if they settle at a lower point:

{kind=link}

Seeking Alpha

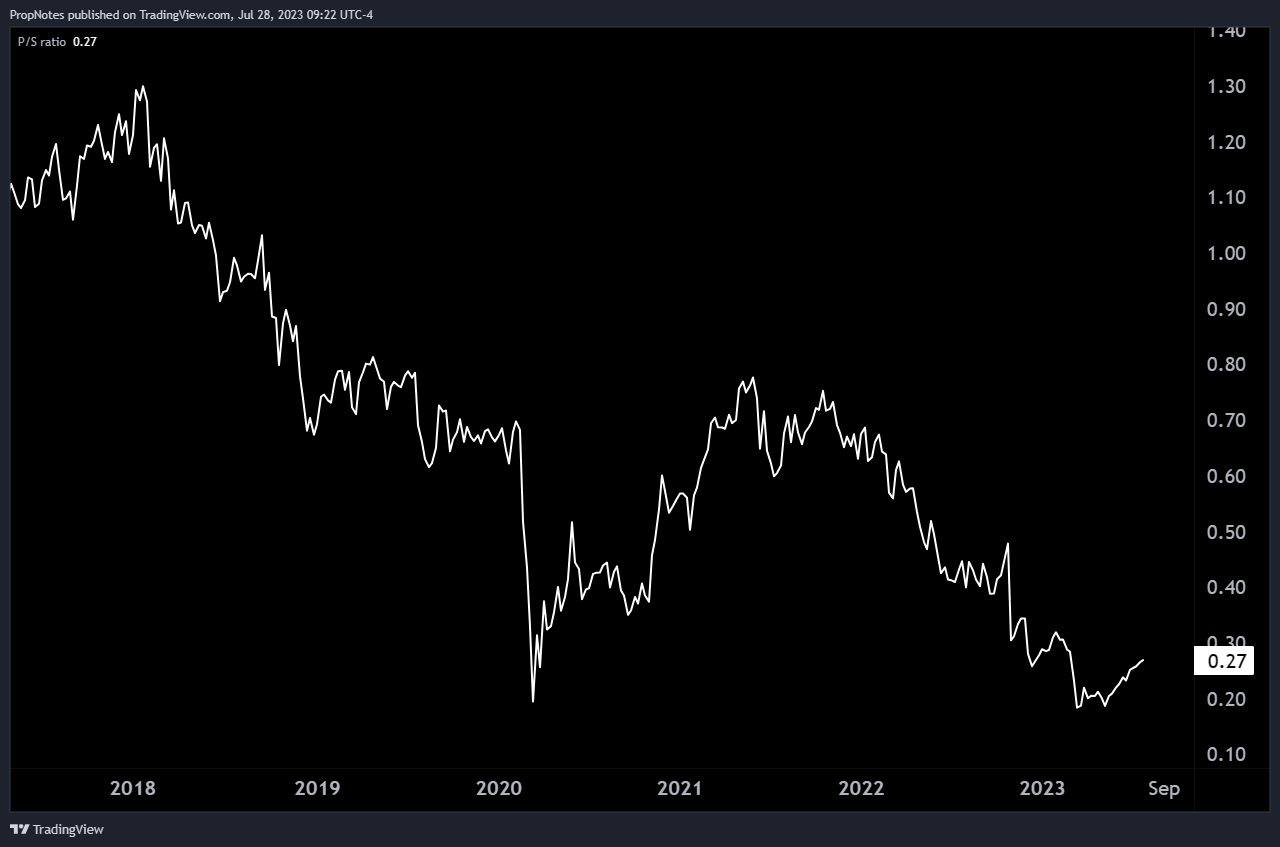

Additionally, a historically cheap revenue multiple makes an entry at the current price seem highly attractive, and suggests that the market is already aware of the risks and has priced them accordingly:

{kind=link}

TradingView

So, while the recent negative catalysts will likely put pressure on margins going forward, we think the strong track record and cheap valuation counteract this somewhat. Getting long now likely means sitting through some bumps, but it could lead to gains depending on how quickly rates normalize.

In short, fundamentally, we rate LNC as a "Hold", as there are balanced risks and rewards at the present moment in time.

Past Earnings

That said, we're looking to make a trade that benefits off of the upcoming earnings report. Thus, it makes sense to take a look at how the stock has reacted in the past to previous reports.

Here’s the data:

| Date |

| Move |

| 5/9/2023 |

| -3.9% |

| 2/8/2023 |

| -2.9% |

| 11/2/2022 |

| -33.1% |

| 8/3/2022 |

| -9.2% |

| 5/4/2023 |

| -9.3% |

| 2/2/2022 |

| -6.2% |

If you add up the recent absolute moves and average them out, you’ll end up with an average move following earnings of 10.76% .

There are two things to keep in mind tactically based on this data.

First, we should look create a trade that has a breakeven point below this average move. That way, in most cases, we'll be shielded from volatility and should quickly be in profit.

Second, after the market digested the $10 billion loss in late 2022, earnings reactions have been more stable. This makes sense fundamentally and should also play to our favor as the option markets may end up mispricing these contracts.

The Trade

As we mentioned, this setup seems like a great opportunity for shrewd investors to sell put options, due to LNC's balanced set of potential risks and rewards.

For those who may not be familiar with a short put strategy, when you sell a put option, you're committing to buying the stock at a predetermined price before the contract expires.

If the stock finishes below the strike price by the expiration date, then you may be obliged to purchase the stock.

In return for assuming this risk, the put seller collects a premium.

In this example, we're ok buying the LNC stock it if it goes lower and becomes even more discounted, but we're also happy if the option expires worthless and we get to keep our option premium free and clear.

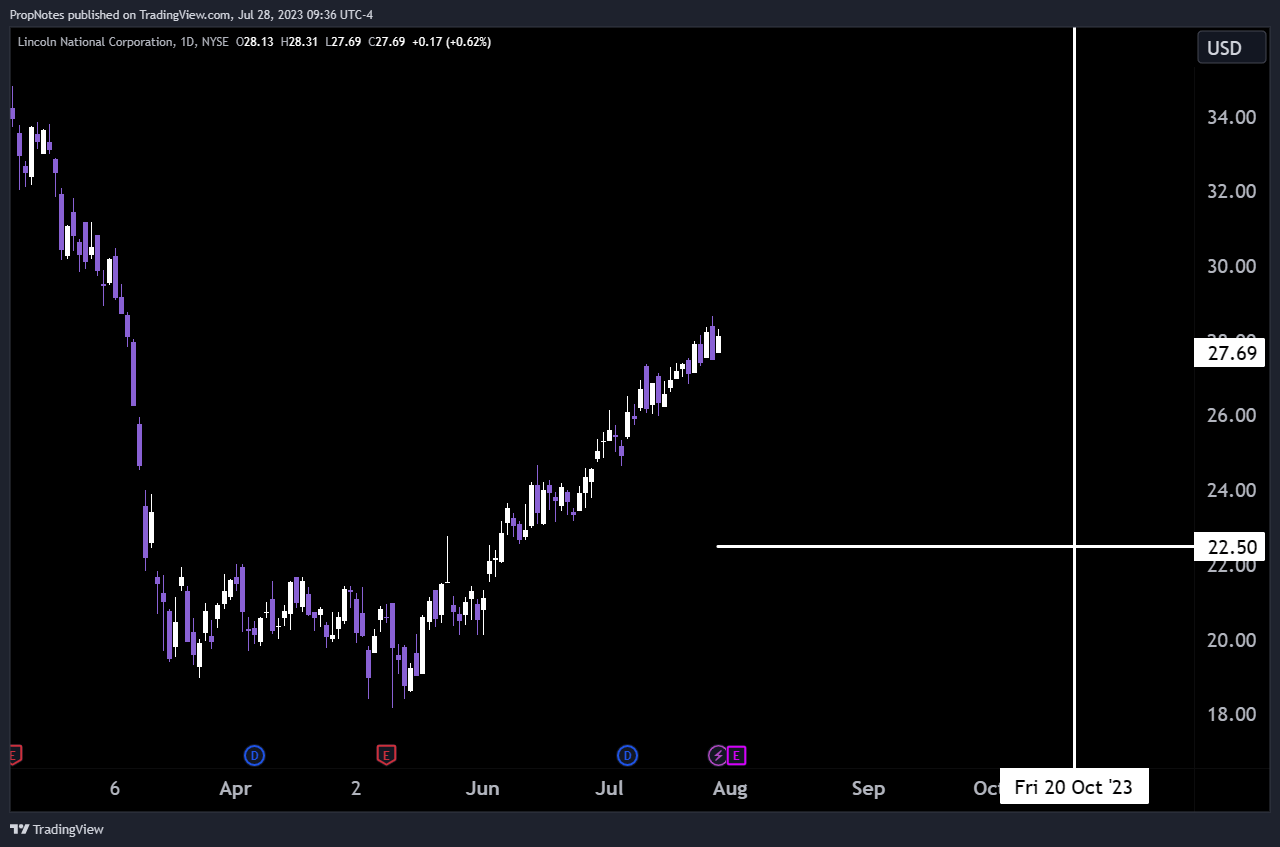

Currently, we like the October 20th, $22.5 strike contracts:

{kind=link}

TradingView

This trade provides a breakeven of -21% , which is bigger than the average earnings move of 10.76% . This seems "cheap" in our view and is perhaps mispriced vs. expectations. Options markets are also anticipating the probability of max profit by expiry at 83%. Not bad!

In return, sellers of this contract can collect 0.70c per share, or $70 per contract. Given that each contract sold will burden $2,250 of cash in your brokerage account, the cash-on-cash return stands at 3.21%. This annualizes to 14%, which is very healthy in our view.

If the position gets assigned, then you’re left with a company that has some flaws, but that also has a solid track record. Plus, its trading at a dirt-cheap valuation.

Risks

There are some risks here.

The main one in our mind is inflation and interest rates. Given that LNC's assets and future cash flows are driven by the Fed Funds rate (the bond complex LNC owns is driven from this single point of data), it appears that any changes here of an adverse nature could significantly impact earnings in the years to come.

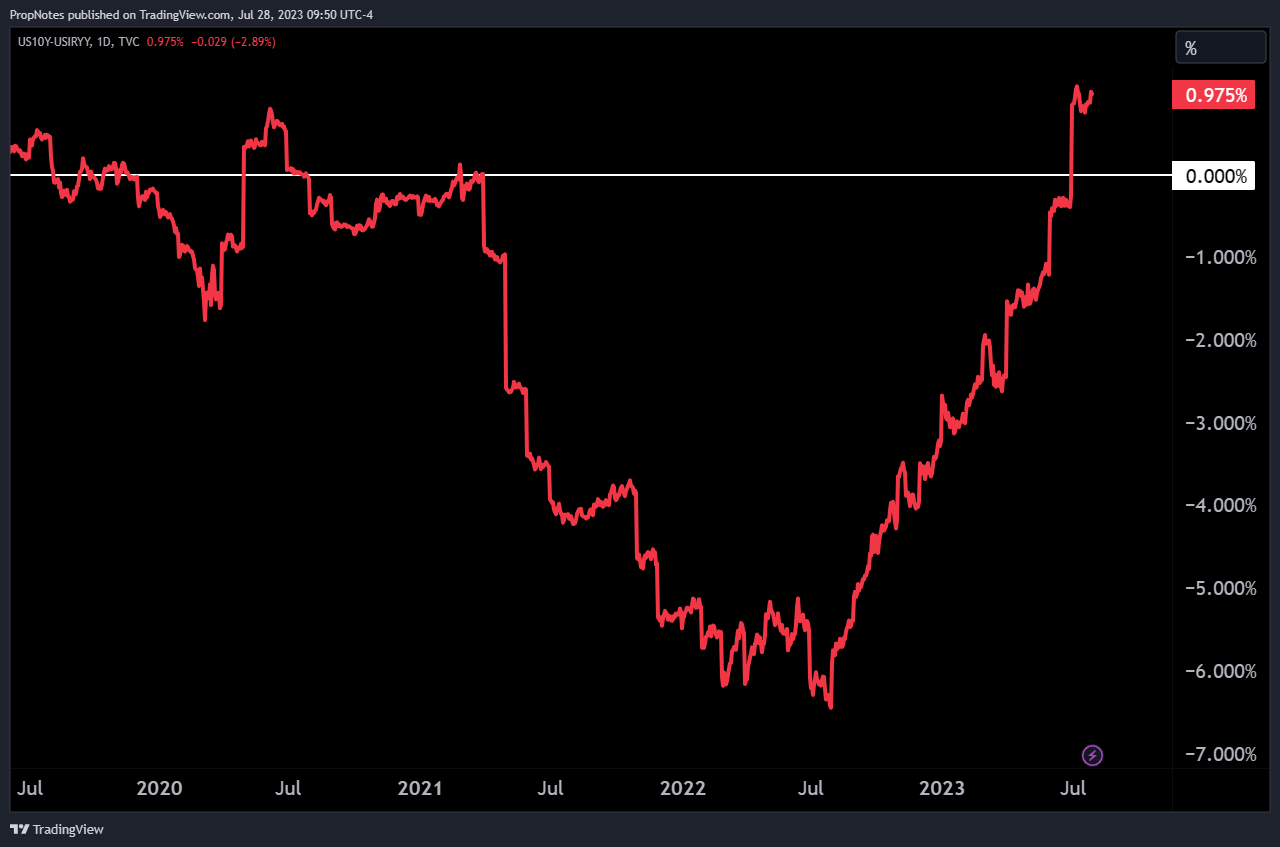

Thankfully, we appear to be on the "other side" of the inflation monster, as real rates have become to come back into positive territory:

{kind=link}

TradingView

Additionally, while we've tried to construct a trade that should mitigate volatility around earnings, it's anyone's guess how the market will react to an earnings report. Put sellers risk that things may go farther or faster than expected to the downside, which could leave them forced to buy the stock above market come option expiration.

This isn't a worse outcome than simply holding the stock outright, but it's worth mentioning.

Summary

In conclusion, LNC's strong historical performance and cheap valuation make it a great potential stock to sell puts on going into earnings.

By selling put options with a strike price of $22.5 and a several-month expiration, investors can generate income, capitalize on earnings volatility, and benefit from a large price cushion in the underlying shares. Additionally, we think that assignment at that price would also be favorable for a long-term hold.

While there are some risks around inflation picking back up, we think that the opportunity, on balance, is a win-win scenario.

For further details see:

Lincoln National: Returning 14% And Worth A Look