BVH - Lindblad Expeditions Stock Plunges After A Mixed Quarter

Summary

- Lindblad Expeditions Holdings does continue to recover, but the bottom line results remain under pressure.

- It doesn't help that Lindblad has a great deal of debt on hand, but it is also true that the business is growing at a nice clip.

- All things considered, LIND stock could offer upside, but investors should approach the business with caution.

Before the market opened on February 28th, the management team at Lindblad Expeditions Holdings, Inc. ( LIND ) announced financial results covering the fourth quarter of the company's 2022 fiscal year. Unfortunately, the news reported by the company fell far short of what analysts expected. While revenue did come in higher than forecasted, earnings per share missed terribly.

In general, the company's bottom line looked rather depressing for the final quarter. Management did provide some interesting guidance for the 2023 fiscal year. Given the 20% drop in price that shares experienced in response to the fourth quarter earnings release, and how shares are priced on a forward basis if we assume that guidance comes to fruition, the stock may not be the worst prospect to be had. But, until we actually see something concrete come into play, I do still believe that a "hold" rating is the best that I can assign the business at present.

A wild ride

Back in September of 2022, I wrote my first article discussing the investment worthiness of Lindblad Expeditions. For those not familiar with the company, it focuses on providing its customers with expedition cruising and land-based adventure travel that centered around themes like exploration and discovery. Prior to the COVID-19 pandemic, the company had been doing quite well for itself. But then, the bottom fell out.

At the time that I wrote my article on the firm, I noticed that the picture for the business was improving. Even so, it wasn't exactly where it needed to be in order for the company to make for a solid investment prospect. But as a rule of thumb, I find it difficult to become bearish on a company that is showing significant improvements and that seems to be working its way toward a recovery. Because of this, I ended up rating the firm a "hold." Since then, Lindblad Expeditions Holdings, Inc. shares have fallen to about 8.9% compared to the 0.9% decline experienced by the S&P 500 (SP500).

{kind=link}

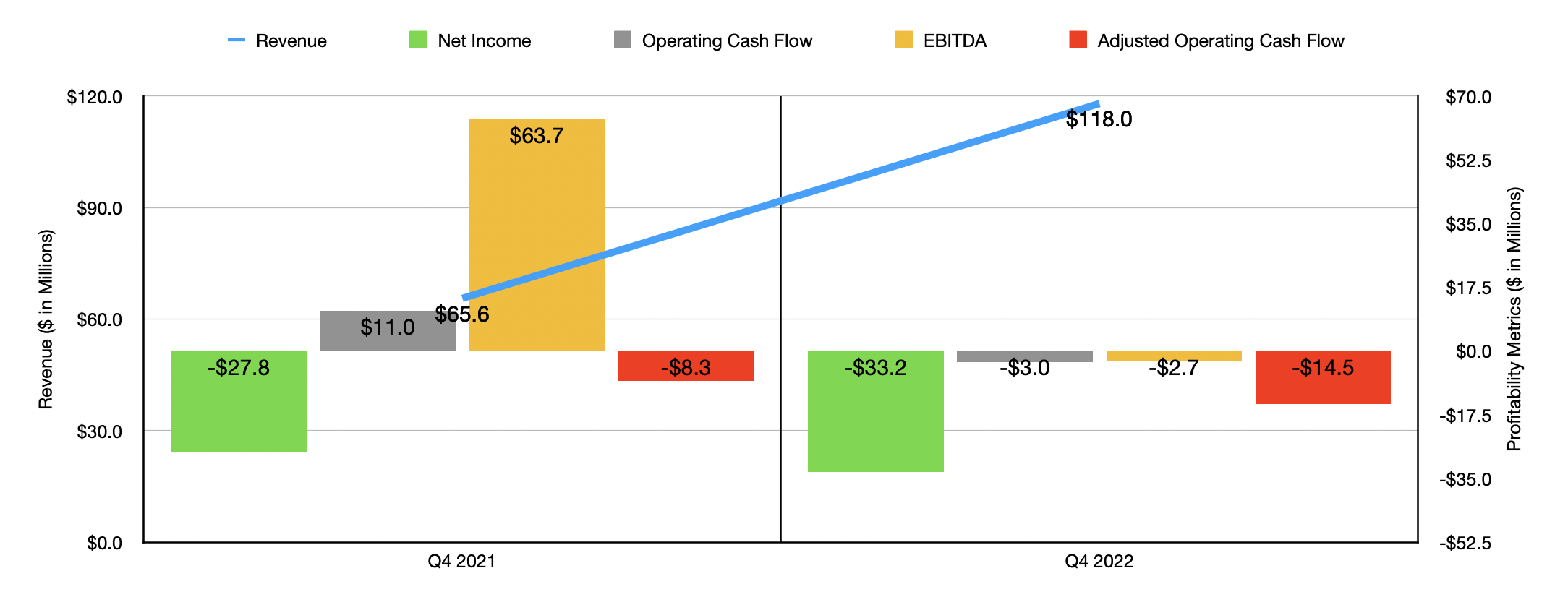

To start with, we probably should zero in on the earnings data reported by management for the final quarter of the 2022 fiscal year. During that time, revenue came in at $118 million. That's an impressive 79.9% increase over the $65.6 million the company reported only one year earlier. It's also higher than the $78.4 million in sales the company reported in the final quarter of 2019 before the pandemic took a significant bite out of the business. According to the data provided, these sales figures actually came in about $23.7 million higher than what analysts anticipated. Under the Lindblad operating segment, sales for the business spiked $37.8 million year over year, while revenue under the Land Experiences segment grew $14.6 million. These increases were driven by a combination of a ramping up in the number of expeditions and trips, as well as the result of higher pricing.

Although the company did incredibly well from a sales perspective, it suffered meaningfully on the bottom line. The net loss for the business totaled $33.2 million. That's worse than the $27.8 million net loss reported only one year earlier. On a per-share basis, the company's profits were negative to the tune of $0.63. That was $0.19 per share lower than what analysts were expecting. Sadly, other profitability metrics for the company followed a similar trajectory. Operating cash flow went from a positive $11 million to a negative $3 million. Even if we adjust for changes in working capital, the picture would have worsened, with the metric turning from negative $8.3 million to negative $14.5 million. And finally, EBITDA for the business plunged from $13.7 million to negative $2.7 million.

There were multiple factors that impacted sales negatively. It is true that, on a percentage of sales basis, the firm's bottom line did actually improve. But that doesn't change the fact that a 46.8% surge in the cost of tours, a 41.9% rise in general and administrative costs, and an 83.3% increase in selling and marketing expenses all pushed the company's bottom line lower.

{kind=link}

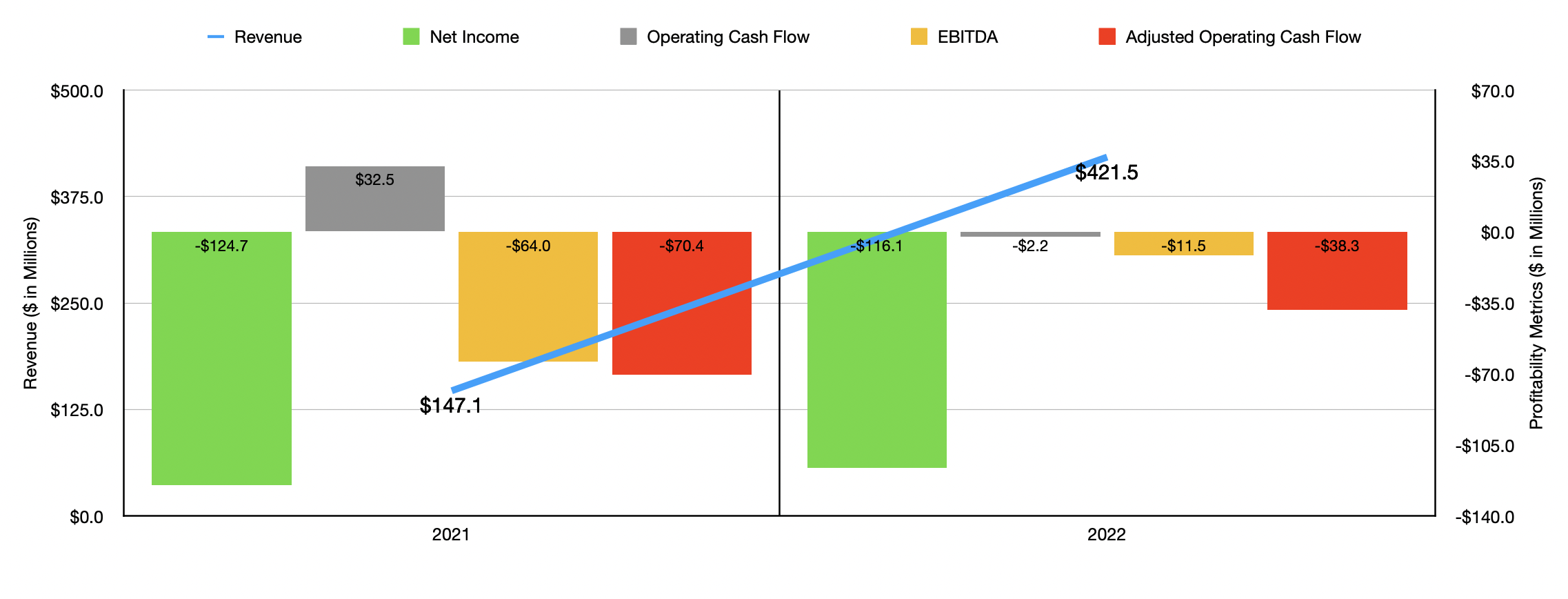

The results Lindblad Expeditions Holdings, Inc. reported in the final quarter of 2022 were instrumental in determining how the company fared during its 2022 fiscal year relative to how it performed in 2021. Revenue spiked from $147.1 million in 2021 to $421.5 million in 2022. Despite the rough final quarter of the year, the company did still see its bottom line improve, with its net loss dropping from $124.7 million to $116.1 million. Operating cash flow, on the other hand, went from $32.5 million to negative $2.2 million. Fortunately, once we adjust for changes in working capital, we can see that the metric actually improved, turning from negative $70.4 million to negative $38.3 million. And finally, EBITDA turned from negative $64 million to negative $11.5 million.

Those who are bullish about the company will also point out some other interesting pieces of information. For starters, management is forecasting adjusted EBITDA for 2023 of between $70 million and $80 million. Management has not provided an official operating cash flow estimate. But if we take the current interest rates applied to the debt on its books and factor in a 21% corporate tax rate, we would get operating cash flow of about $35 million for the year. Given the years of losses on its books, it's highly unlikely that the company will have any tax expenses. If not, that will make the bottom line look even better.

Although the company did not reveal what revenue should look like for the year, it's all but certain that such a massive improvement in EBITDA that's what management has forecasted would have to be driven in large part by a surge in revenue. The good news for investors is that the company already has seen strong reservations for future travel, with bookings for 2023 already coming in 47% higher than in 2019 for the same point in 2019. In addition to the world opening up following the end of the COVID-19 pandemic, the company is also benefiting from the fact that it launched the 48-passenger National Geographic Islander II vessel to replace the original National Geographic Islander vessel.

{kind=link}

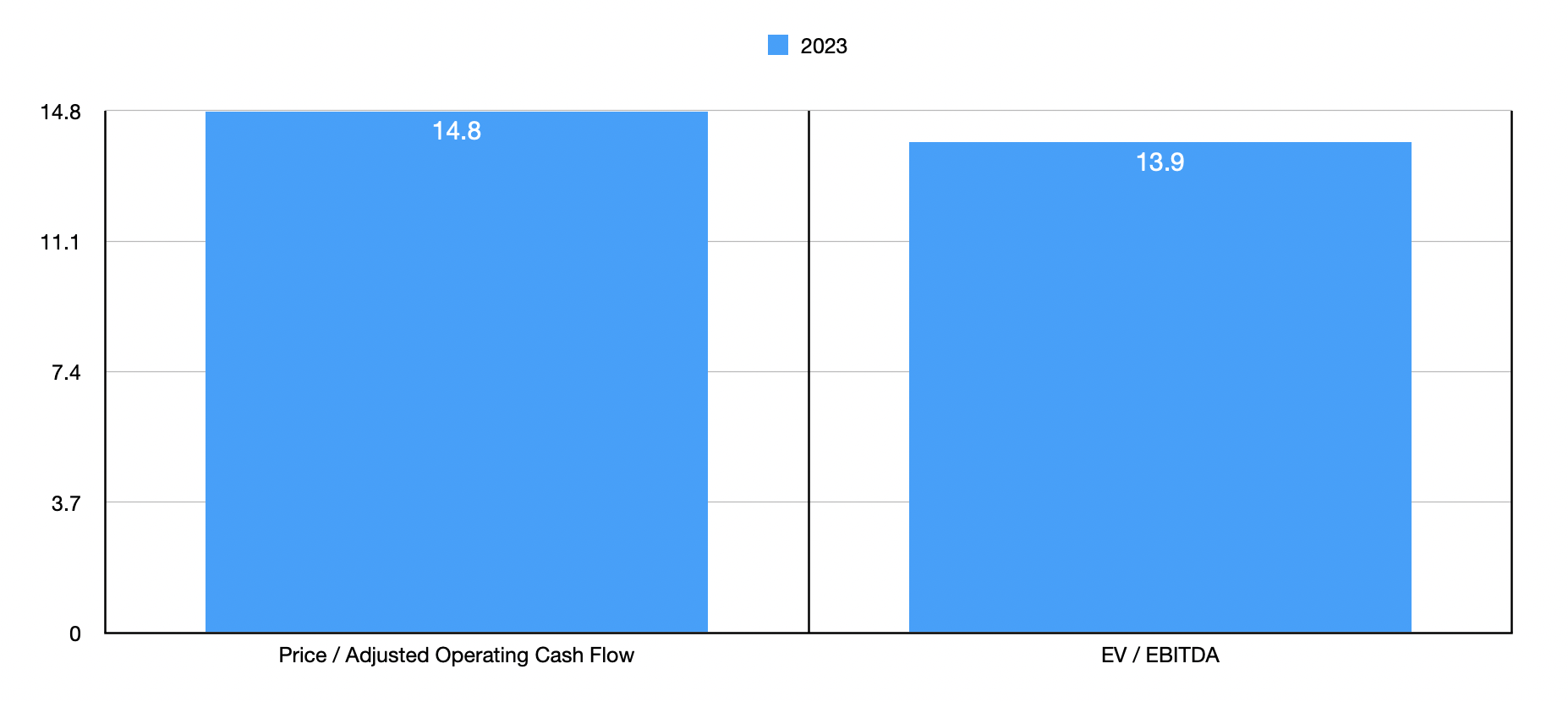

Because both 2021 and 2022 saw significantly negative cash flow data, we can't really value the company on that basis. What we can do, however, is value the company based on these forward estimates for 2023. Based on my math, Lindblad Expeditions seems to be trading at a forward price to adjusted operating cash flow multiple of 14.8 and at a forward EV to EBITDA multiple of 13.9. For context, the price to adjusted operating cash flow multiple assumes that the company was to pay its preferred distributions of nearly $4.2 million annually in cash instead of in-kind like it has the option, but not the obligation, to do.

Truth be told, valuing Lindblad Expeditions Holdings, Inc. relative to similar firms is difficult because of how unique this firm is and because of its size. I made a good-faith effort, however, to put together a list of five companies that have some similarities to it from an operational perspective. On a price to operating cash flow basis, these firms ranged from a low of 6.1 to a high of 37.4. Using our forecasted results, I calculated that only two of the five companies are cheaper than our target. Meanwhile, using the EV to EBITDA approach, we end up with a range of between 0.4 and 64.8, with three of the four companies that had positive results trading lower than our prospect.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Lindblad Expeditions Holdings |

| 14.8 |

| 13.9 |

| Bluegreen Vacations Holding Corporation ( BVH ) |

| 11.4 |

| 7.3 |

| Royal Caribbean Cruises ( RCL ) |

| 37.4 |

| 64.8 |

| Vacasa, Inc. ( VCSA ) |

| 6.1 |

| N/A |

| Marriott Vacations Worldwide Corporation ( VAC ) |

| 33.2 |

| 12.1 |

| Sonder Holdings ( SOND ) |

| 22.9 |

| 0.4 |

Takeaway

Fundamentally speaking, Lindblad Expeditions Holdings, Inc. is showing some signs of improvement. However, the bottom line clearly missed analysts' expectations materially, and that caused a tremendous amount of pessimism for the business. It's also possible that the market was hoping for a more robust forecast for 2023.

To be clear, I don't believe Lindblad Expeditions Holdings, Inc. is a high-quality prospect by any means. I also think that it likely deserved to take the plunge that it did. Until we see bottom line results actually materialize in a way that looks along the lines of what management is forecasting, I do think it makes for nothing better than a "hold" prospect at this time. And for those who don't like the risk that comes with a firm like this and that has a significant amount of debt, totaling $423.2 million in all on a net basis, I would say that it might just be best to stay away from Lindblad Expeditions Holdings, Inc.

For further details see:

Lindblad Expeditions Stock Plunges After A Mixed Quarter