LIN - Linde: Defensiveness At A Discount

Summary

- After our APD and L'Air Liquide analysis, Linde is the most defensive company within the industry.

- Supportive macro to micro reasons to buy and hold the company.

- Compelling valuation with an ongoing buyback and an interesting backlog with double-digit IRR expectations.

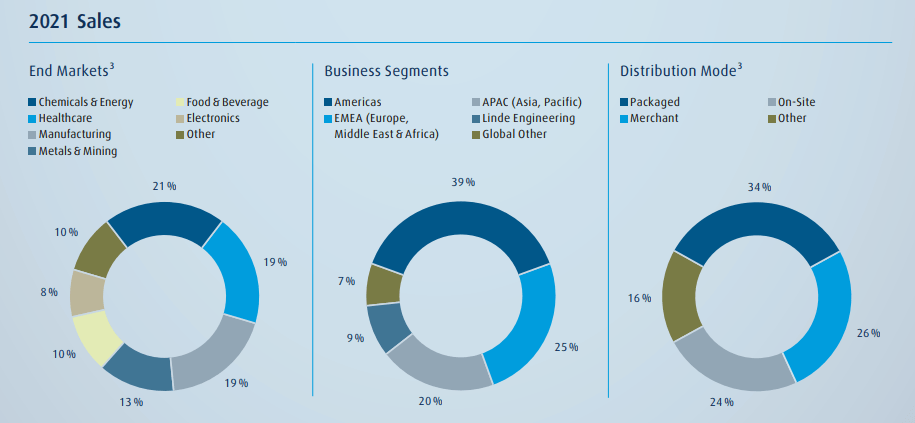

After our comment about the Q2 performance of L'Air Liquide ([[AIQUF]], [[AIQUY]]) and Air Products and Chemicals (NYSE: APD ), here at the Lab, we have decided to deep-dive into Linde plc ( LIN ) - the largest global manufacturer of industrial gases. In short, the company provides all the atmospheric and process gases. In addition, Linde is an engineering company engaging its activities in designing and building turnkey processes and gas plants for the third-party players - this segment provides 9% of the company's total sales based on 2021 numbers. Linde was incorporated in 1879 and is based in the United Kingdom.

{kind=link}

Why are we positive?

Our buy case recap is based on MACRO and MICRO reasons, some of our main key takeaways are taken from our sector publications, while others are company-specific. Starting with the former:

- (macro) - The European Union is supportive of CO2, hydrogen and green opportunities, thanks to Linde's exposure, we believe that the company is set for a sustainable growth rate;

- (macro) - Again, related to point 1) coupled with the ongoing Ukraine/Russia war, energy transition and independence has become one of the key topics for the European Parliament, this will further accelerate the company's development;

- (macro) - As already emphasized in our Infineon recent publication , Linde might take advantage of the EU's Chips Act : " the European Commission plans to allocate €11 billion in public funds for the research, design and manufacturing of semiconductors, with the goal of mobilizing a total of €43 billion of public and private investment until 2030 ". Recent news shows that Intel is planning to open a new chip lab facility in Italy for a total investment of more than $4 billion. There are rumors of new chip labs in Germany. APD has recently disclosed a new investment fully dedicated to the semiconductor industry.

- (macro) As already disclosed in our L'Air Liquide analysis , compared to the Internal Combustion Engine Vehicle, EV and BEV cars " are almost 50% more gas-intensive" - this certainly will be an upside for the whole sector;

- (micro) - Linde has the greatest diversity in gases and applications compared to APD and AL;

- (micro) - Again, looking at Linde's revenue exposure, we can clearly see that is a truly diversified operator whereas AL is more focused on EU countries and APD is more exposed to the North American region. This is also true in terms of costumer sector exposure;

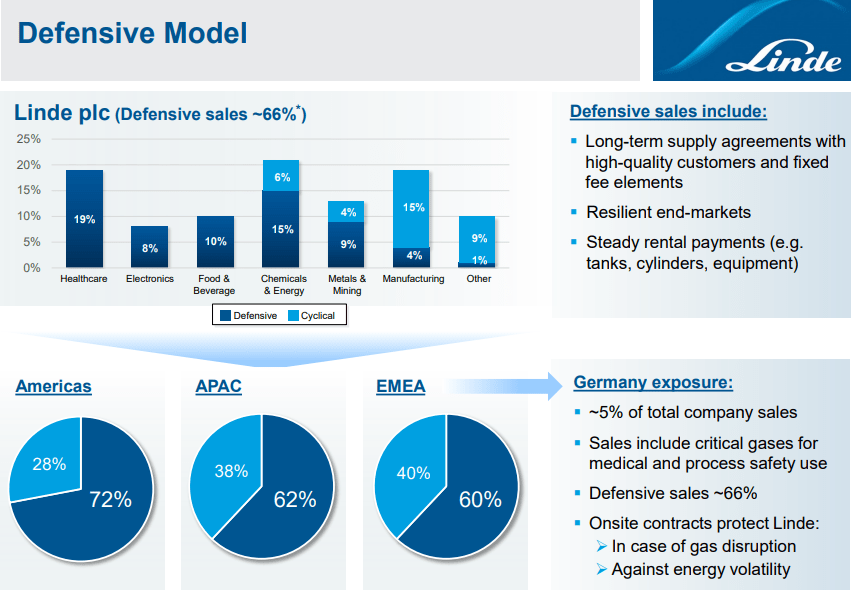

- (micro) In addition, the company sells different solutions starting from cylinders (for small clients' needs) to bulk liquid. This latest practice consists in liquifying and delivering the gas via trucks. These customers (usually hospitals and chemical facilities) have contract agreements with fixed volume and guaranteed margin with an average duration of four years. Lastly, the most important point, Linde's end customers are the ones receiving gas by connected pipeline, onsite, or close to the company's gas plant. Those clients have contracts with a duration of more than ten years, with margin and volume guarantees (with a full pass through of raw material inflationary pressure). This makes Linde the most defensive company within the industry.

{kind=link}

Conclusion and Valuation

Linde has a high-quality order backlog with a supportive double-digit IRR. Macro to Micro reasons make Linde a clear buy. Moreover, during the Q2 presentation and despite the macroeconomic challenges, the company has just raised its EPS guidance. The dividend will follow EPS growth, and according to our numbers, it is set for a 10% increase year-on-year. Going to the financials, our model indicates a 2024 forecasted EBITDA of almost €12 billion and valuing the company with its three-year average of EV/EBITDA multiple of 15.0x (adjusting for net debt consideration); hence, we derive a target price of $330 per share versus the current market price of $260. We do not add anything more, since we consider it to be a clear buy.

The main risks to our target price include wage inflation, raw material cost pressure, execution risk in the engineering arm, and macroeconomic slowdown with a consequent decrease in industrial activities.

For further details see:

Linde: Defensiveness At A Discount