DE - Lindsay Corporation: An Upgrade Is In Order

2023-06-20 15:30:39 ET

Summary

- Lindsay Corporation's financial performance has improved, leading to an upgrade from a "sell" to a "hold" rating.

- Despite a drop in revenue, profitability has increased, with net income growing from $22.5 million to $36.3 million.

- The company's stock is still relatively expensive compared to similar firms, but not as much as it was last year.

Very nearly one year ago, a company that I took a rather bearish stance on was Lindsay Corporation ( LNN ). If the business does not sound familiar to you, that's alright. With a market capitalization of $1.36 billion, it's a small enterprise. Furthermore, it operates a very specific line of products dedicated largely to the agricultural industry. Examples include irrigation systems and, to a lesser extent, infrastructure products like crash cushions, end terminals, road safety equipment, railroad signs, and more.

The 2022 fiscal year ended up being quite robust for the enterprise. But recently, we have seen some mixed results. However, between the improvement seen last year and how fundamentals are shaping up so far this year, I do believe that a slightly more optimistic outlook for the company is warranted. Because of this, I've decided to increase my rating on the company from a "sell" to a "hold."

The picture has improved

Back when I wrote my bearish article on Lindsay in late June of last year, I acknowledged how strong growth for the company had been up to that point. Even so, I was worried about a potential weakening of financial performance moving forward and I felt that shares of the company were far from being cheap. This led me to rate the business a "sell’ to reflect my view at the time that the stock should drastically underperform the broader market. And so far, that call has worked out reasonably well. While the S&P 500 (SP500) is up 17.3% since the publication of that article, shares of Lindsay have risen only 5.1%.

{kind=link}

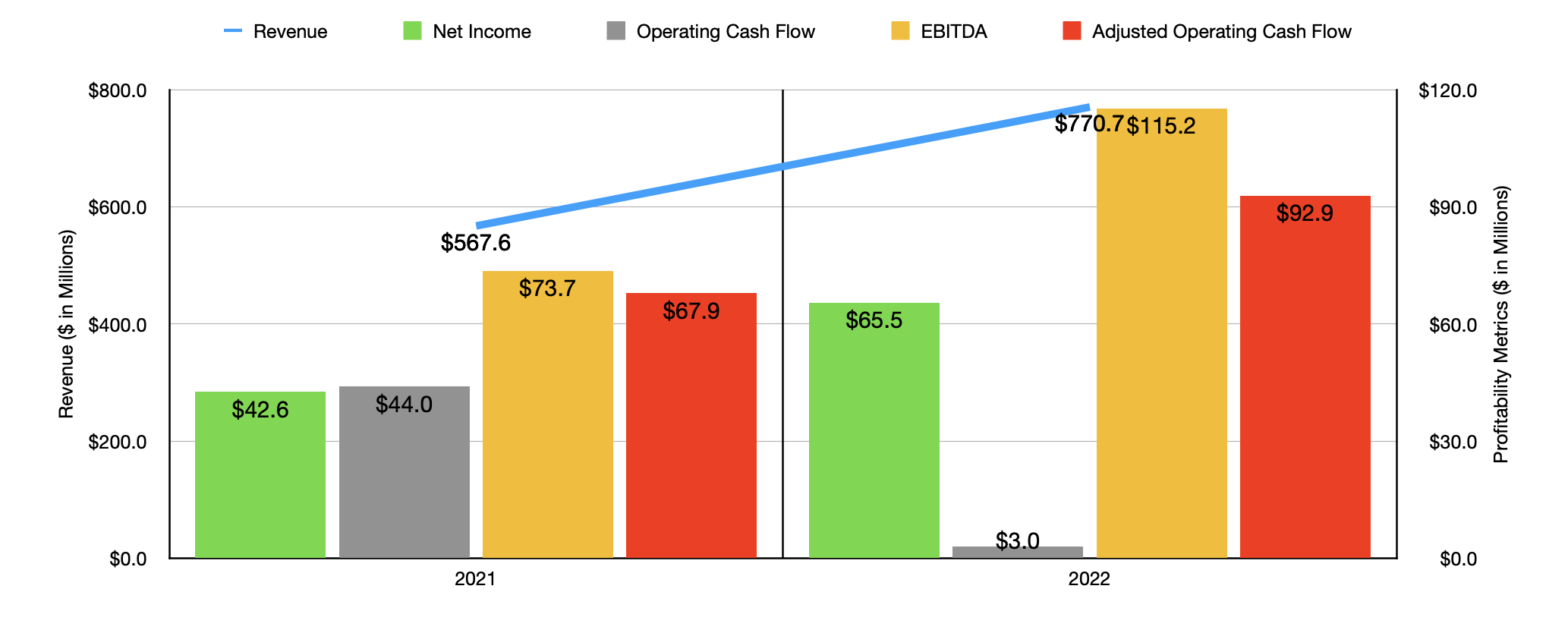

Almost no matter how you stack it, 2022 was a fantastic year for the company. Revenue came in at $770.7 million. That's a 35.8% above the $567.6 million the company reported one year earlier. This increase, management said, was driven by a roughly 41% surge in revenue associated with the company's irrigation operations. Revenue in this category was driven higher in North America as the company benefited from higher average selling prices and a small increase in irrigation equipment unit sales. Internationally, these factors were also at play. In particular, the firm demonstrated its strength throughout Brazil and Europe.

Thanks to this surge in revenue, profits for the company jumped from $42.6 million to $65.5 million. It is true that operating cash flow worsened from $44 million to only $3 million. But if we adjust for changes in working capital, we would see this number grow from $67.9 million to $92.9 million. And finally, EBITDA for the enterprise expanded from $73.7 million to $115.2 million.

{kind=link}

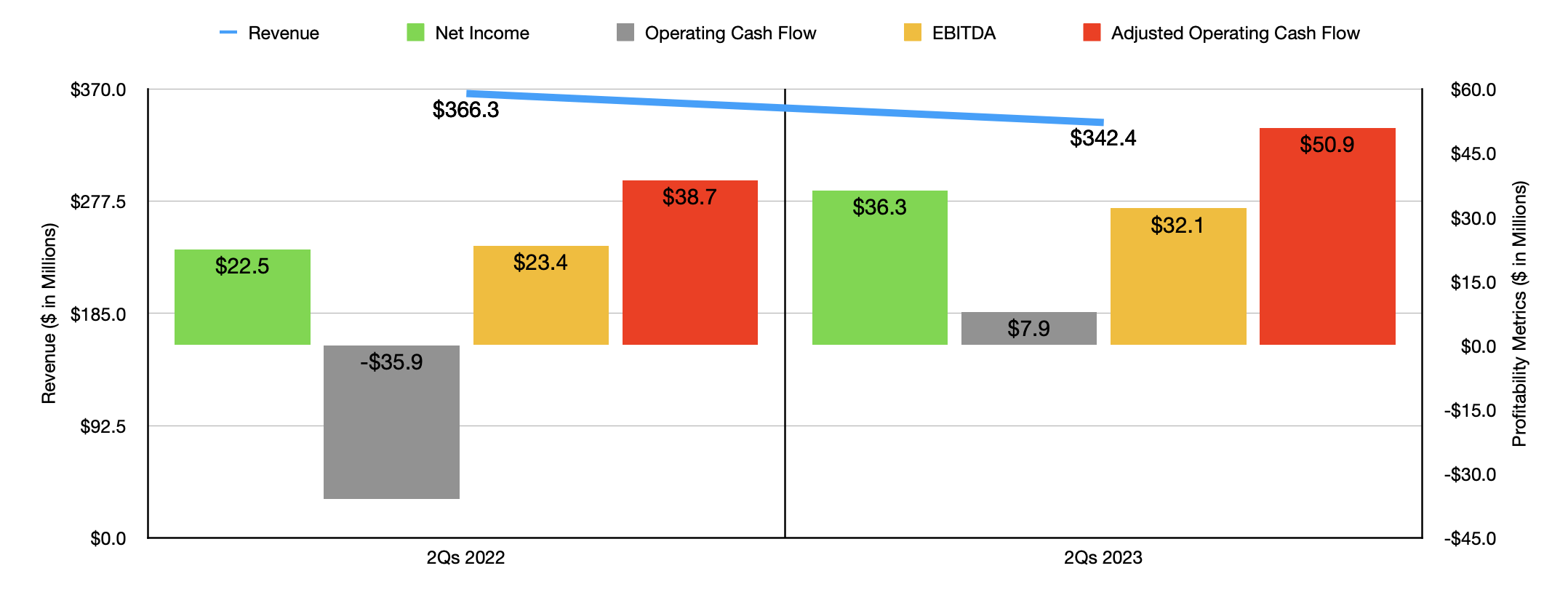

After the stellar 2022 fiscal year, you might think that the company would continue strong performance in 2023. But things have not been that simple. Revenue, for instance, actually fell from $366.3 million in the first two quarters of 2022 to $342.4 million the same time this year. Even though the company benefited from a 7% increase in sales associated with its infrastructure operations, its irrigation operations reported an 8% decline in sales. According to management, a reduction in volume more than offset price increases. The company also said that it experienced some pain because of lower sales volumes in both Ukraine and Russia. However, it did not provide an estimate on how much pain was associated with those two nations.

Even though revenue dropped, profitability for the company improved markedly. Net income of $36.3 million dwarfed the $22.5 million reported one year earlier. Both of the company’s operating segments showed improvements in their operating profit margins. For the irrigation business, the profit margin grew from 12.8% to 20.5%, while for infrastructure it expanded from 7.8% to 12.7%. These improvements seem to be largely the result of an easing of inflationary pressures, combined with certain one-time events such as A $1.8 million charge that was incurred last year that was related to non-recurring factory maintenance and outside consulting services. Other profitability metrics for the company followed suit. Operating cash flow, for instance, went from negative $35.9 million to $7.9 million. On an adjusted basis, it expanded from $38.7 million to $50.9 million. And finally, EBITDA for the company grew from $23.4 million to $32.1 million.

For the current fiscal year, management has not provided any detailed guidance. But they did paint an interesting picture for the industry. They said, for instance, that agricultural commodity prices are still high. Corn prices, for instance, were up 35% in February of this year compared to the same time last year, while soybean prices have jumped 8% year-over-year. At the same time, however, net farm income in the U.S. is down 15.9% thanks to a reduction in government support payments as stimulus has trailed off and as cash receipts for crops is forecasted to fall by 3.1%. So we do seem to be at a point where, even though prices are elevated, investment activity into the kinds of products Lindsay manufactures, should weaken.

{kind=link}

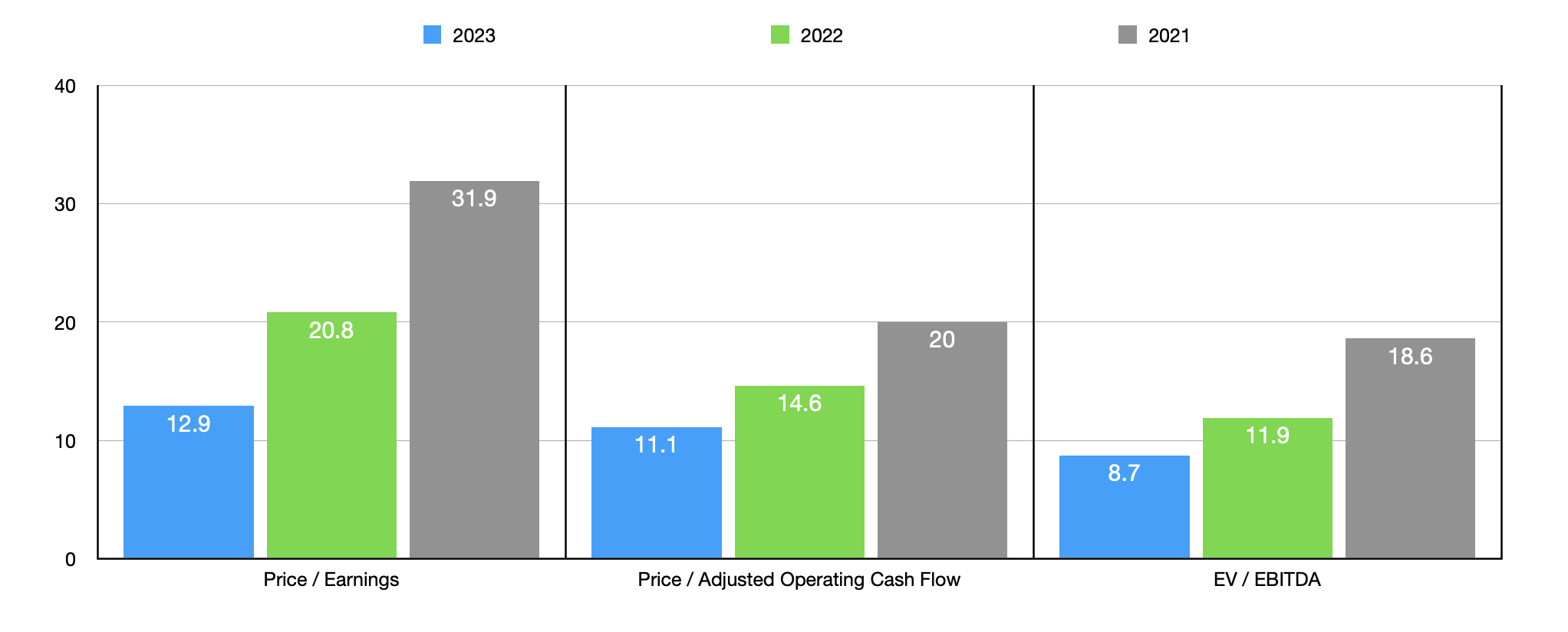

In terms of the overall picture for the company, I would say that the situation has improved to some degree. As you can see in the chart above, I used financial data from both 2021 and 2022 to value the company. If we are heading in the direction of further weakening, it's not unthinkable that financial performance could revert back to what it was in 2021 as opposed to what it was last year. In this case, the stock does look pricey. But it's not so expensive that I would be overly bearish. Relative to similar firms, shares are rather expensive still.

As you can see in the table below, Lindsay is more expensive than any of the five companies I compared it to on a price to earnings basis. On a price to operating cash flow basis, only two of the five companies ended up being cheaper than our target, while that number increases to four if we utilize the EV to EBITDA approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lindsay |

| 20.8 |

| 14.6 |

| 11.9 |

| Titan International ( TWI ) |

| 3.9 |

| 3.5 |

| 3.4 |

| The Toro Company ( TTC ) |

| 19.9 |

| 32.6 |

| 13.6 |

| CNH Industrial ( CNHI ) |

| 9.2 |

| 26.7 |

| 9.4 |

| Deere & Company ( DE ) |

| 13.6 |

| 19.4 |

| 11.3 |

| AGCO Corporation ( AGCO ) |

| 10.2 |

| 11.5 |

| 7.1 |

Takeaway

The past year has not been particularly kind for Lindsay or its investors. While it's great that the company experienced some share price appreciation, it has significantly trailed the broader market. For now, I believe that we will see some weakening occur in the space that could hurt its fundamentals. But it's also true that the stock is not as expensive as it was when I last wrote about it. Because of this, I've decided that an upgrade from a "sell" to a soft "hold" is appropriate at this time.

For further details see:

Lindsay Corporation: An Upgrade Is In Order