TWI - Lindsay Stock: Exceeds Q4 Expectations Still Maintaining My Hold Rating

2023-10-20 16:24:15 ET

Summary

- Lindsay Corporation stock soared 14.7% after reporting financial results for Q4 of its 2023 fiscal year that exceeded analysts' expectations.

- Lindsay's revenue for the quarter was down 12.1% YoY, but higher than anticipated, driven by strong performance in international irrigation and weak demand in North American irrigation and infrastructure.

- Despite the positive results, economic uncertainty and high stock prices resulted in the company remaining a "hold" prospect at this time.

It's always nice to see shares of a company skyrocket. Even if you aren't the one making money, it's good to know that others are. One firm that recently did shoot up rather significantly is Lindsay Corporation ( LNN ), an enterprise that produces and sells irrigation systems and various infrastructure products like crash cushions, railroad signs, and end terminals. On October 19th, the stock skyrocketed, closing up 14.7% after management announced financial results covering the final quarter of the firm's 2023 fiscal year.

This move higher came about even as revenue and some cash flow figures provided by the company worsened year over year. The big reason for the increase in price, then, was that management reported numbers that exceeded analysts’ forecasts . This was true on both the top and bottom lines.

While this is excellent to see, it doesn't change my own view on the company. Back in June of this year, I ended up upgrading the company from a "sell" to a "hold" to reflect improved financial performance on the bottom line. I couldn't be any more optimistic than that, however, because of how pricey shares were.

With this surge in price higher, the stock is still down about 4.1% since the publication of that article. But that's not terribly far away from the 2.5% drop seen by the S&P 500 (SP500). Although management remains cautiously optimistic about the near-term future, I still maintain my "hold" stance because, even though financials were better than expected, they still were challenged in some respects on a year over year basis. And when you add into this broader economic uncertainty, I do believe that there are better prospects to be had elsewhere.

Assessing Lindsay's Q4 2023 quarter

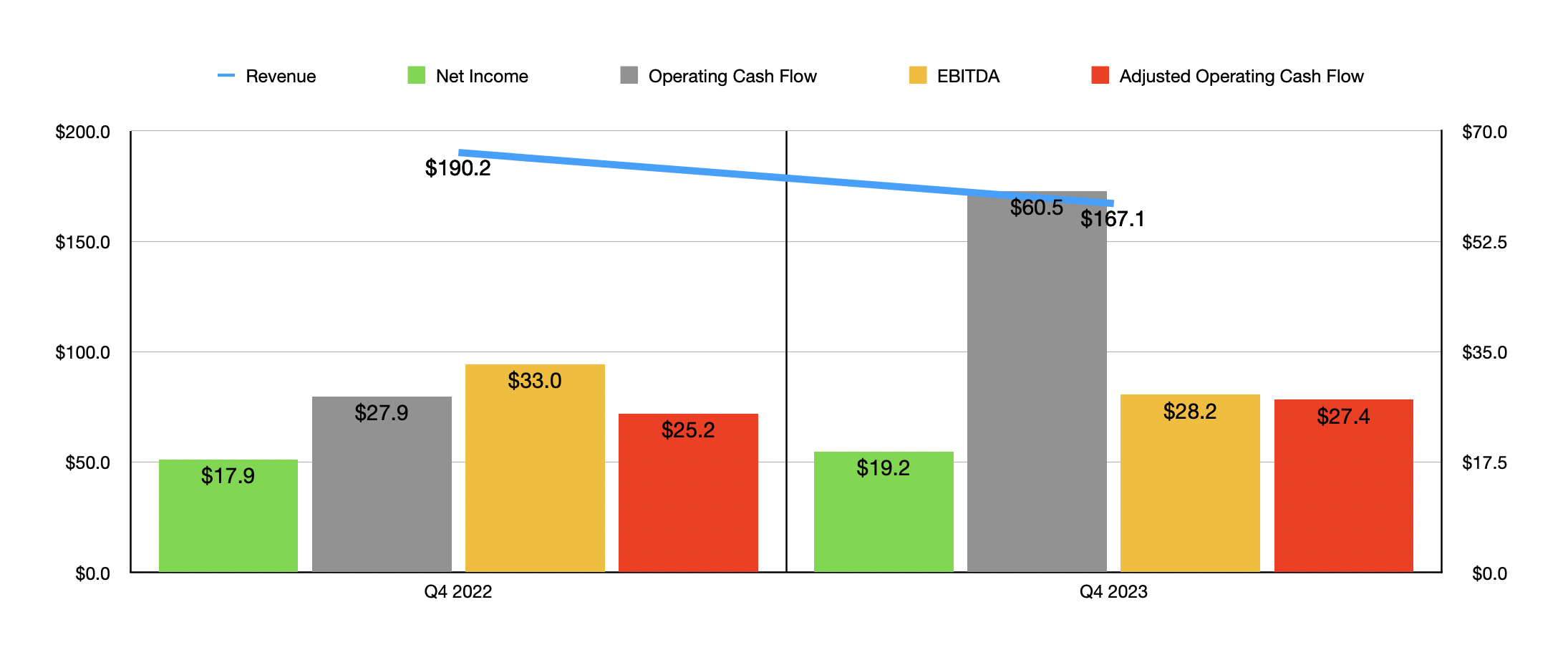

As I mentioned already, on October 19th, shares of Lindsay Corporation jumped 14.7% in response to management reporting financial results covering the final quarter of the company's 2023 fiscal year. During that quarter, revenue came in at $167.1 million. That's actually down 12.1% compared to the $190.2 million the company reported one year earlier. However, it was approximately $9.3 million higher than what analysts anticipated for the quarter.

{kind=link}

Management attributed these results to strong performance for its irrigation products. International irrigation revenue reported a robust growth on a year over year basis, jumping around 18% from $70.4 million to $83.4 million. However, this was more than offset by a 25% plunge in North American irrigation operations. Sales there plummeted from $80.1 million to $60.2 million. This is where context is important though. In the final quarter of last year, the company benefited from strong demand for irrigation products because bad storms caused what management considered to be an ‘exceptional level’ of damage that necessitated the ordering by many customers have replacement parts and systems.

The biggest weakness for the company from a revenue perspective involved its Infrastructure segment. Revenue dropped 41% from $39.7 million to $23.5 million. Management chalked this up to lower demand for the Road Zipper System that the company sells. Road safety product demand was also robust this year.

On the bottom line, the company reported profits per share of $1.74. In addition to beating out the $1.62 in earnings reported the same time last year, it also exceeded analysts’ forecasts by a whopping $0.63 per share. This allowed net profits to rise from $17.9 million in the final quarter of 2022 to $19.2 million the same time this year. Even though revenue took a beating, Lindsay Corporation benefited from a reduction in interest expense, significantly stronger interest income, and a big swing in other expenses to favor the current year. It is worth noting that other profitability metrics performed well for the most part. Operating cash flow, for instance, jumped from $27.9 million to $60.5 million. Even if we adjust for changes in working capital, we would get an increase from $25.2 million to $27.4 million. The only profitability metric to worsen during this time was EBITDA. It managed to tick down from $33 million to $28.2 million.

{kind=link}

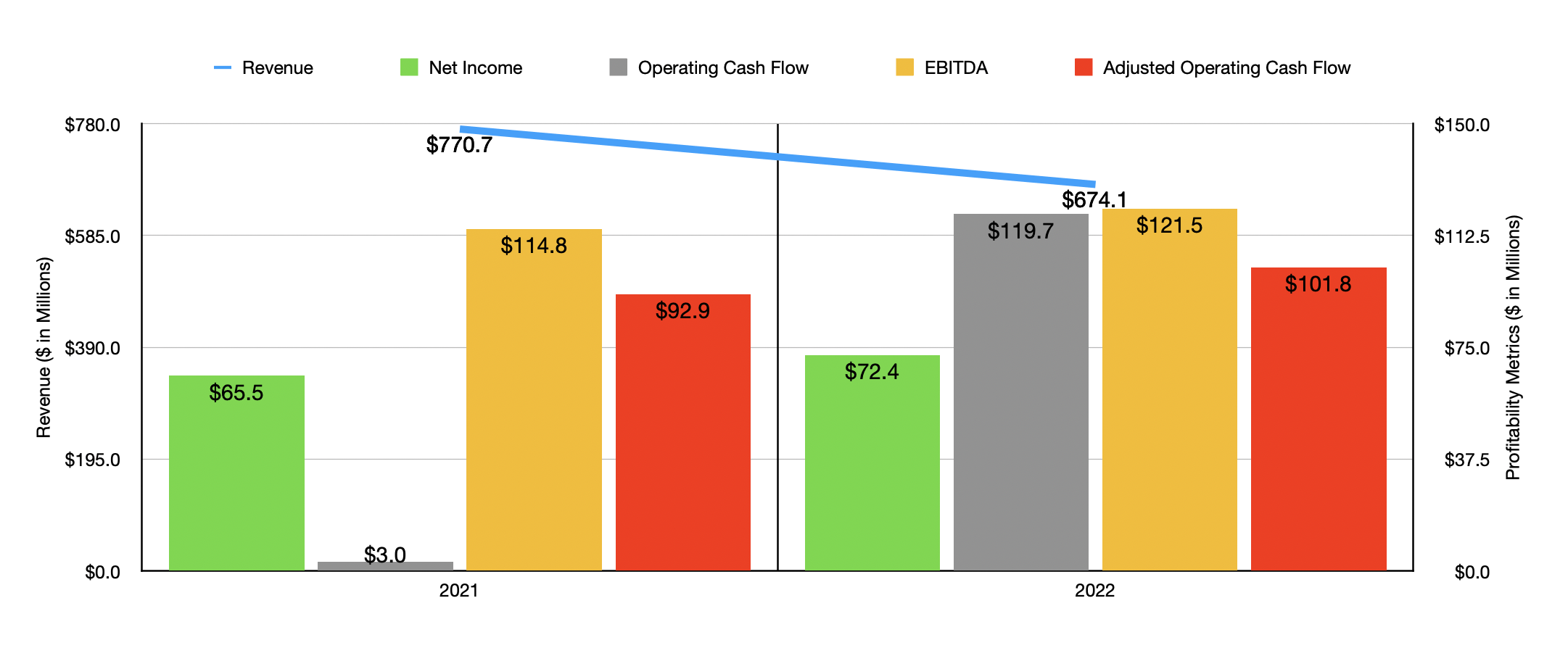

With this final quarter worth of data in, we now have a comprehensive look at 2023 in its entirety. And in many respects, it mirrored what the fourth quarter was. Revenue came in at $674.1 million. That's down 12.5% compared to the $770.7 million reported for 2022. But net profits managed to increase, climbing from $65.5 million to $72.4 million. As you can see in the chart above, operating cash flow and adjusted operating cash flow both increased year over year. The one difference between the fourth quarter and the year as a whole was that, for 2023 in its entirety, EBITDA was actually up, having risen from $114.8 million to $121.5 million.

{kind=link}

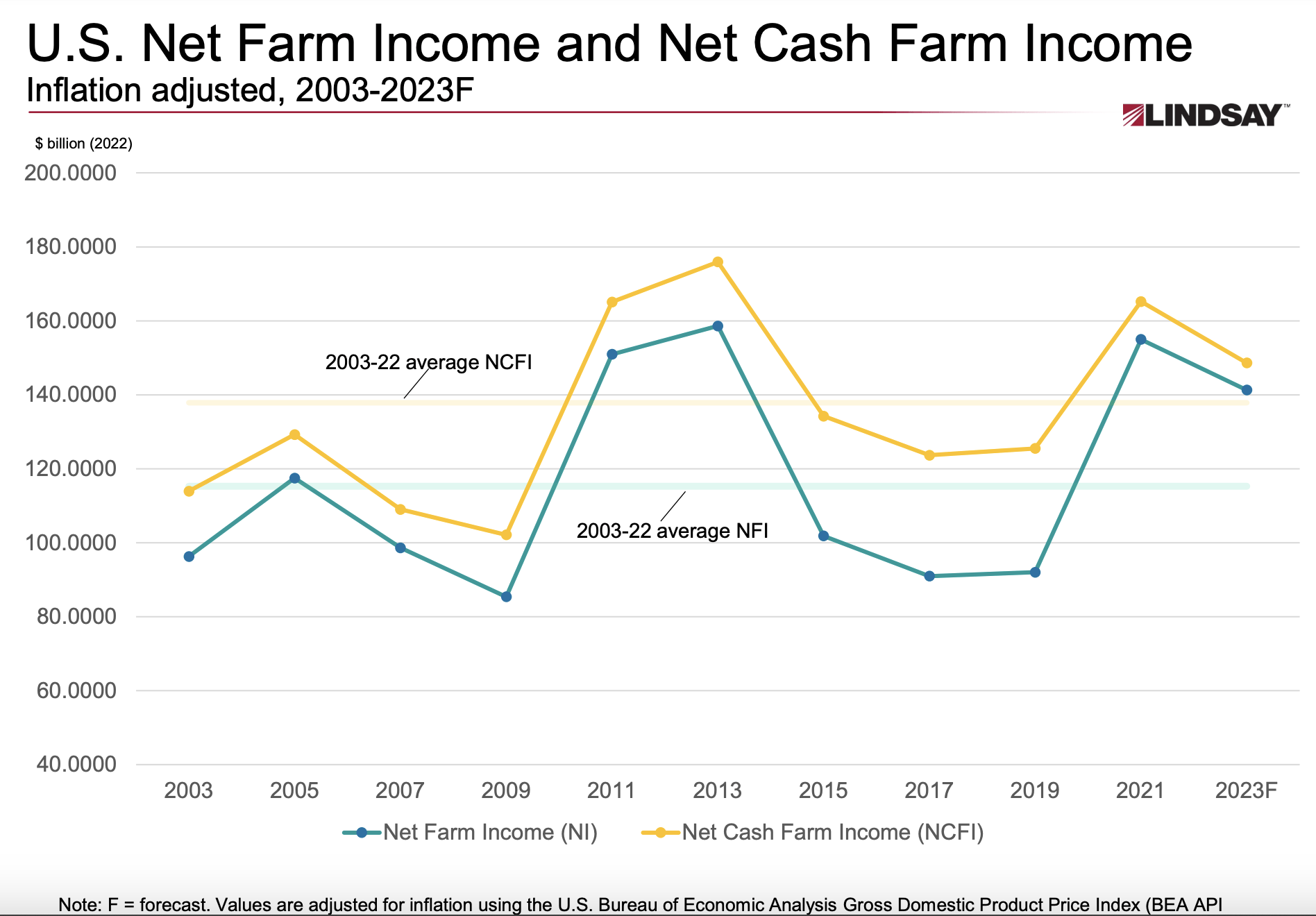

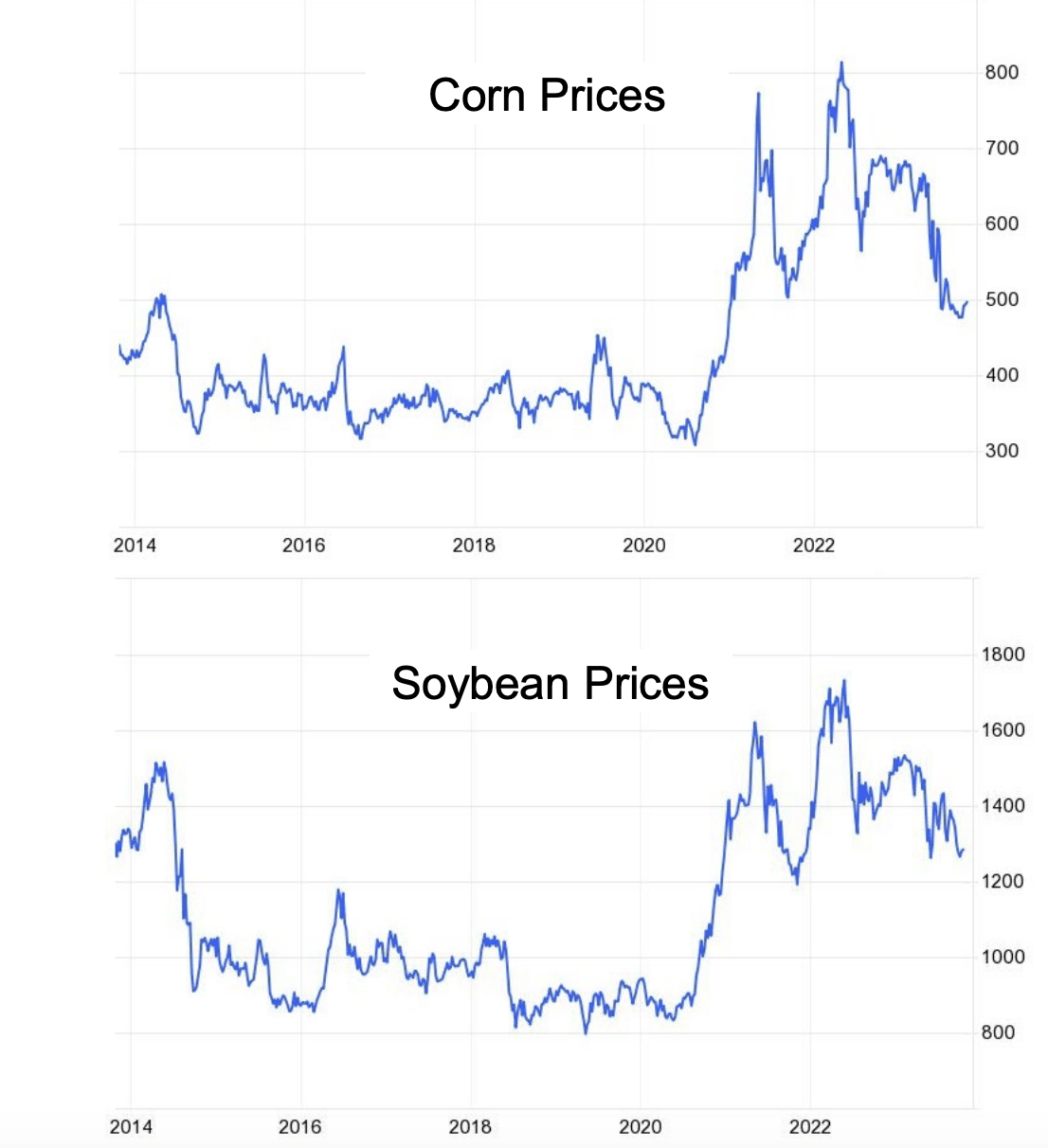

Management was fairly straightforward when it came to their own outlook for 2024. They recognized that both commodity prices and US net farm income projections are lower than they were last year. This does come with a bit of a caveat. The actual decline projected for net farm income for 2023 was approximately 23% compared to the year prior. This does indicate some contraction in demand moving forward.

Having said that, the level in income is still fairly high compared to what it has been historically. And that's what management is optimistic about. They said that they continue to expect demand for irrigation equipment to be supported in the North American market because of this. They also expect sales volume levels in key international markets, particularly in Brazil, to remain robust as well as in certain developing markets because of food security issues and challenged global grain supplies. The latter of these has been a major problem because of the conflict between Russia and Ukraine.

{kind=link}

Unfortunately, management has not provided any guidance for the year. But they have said that their goal is to continue to average annual revenue growth that is in excess of 7% per year and earnings per share growth that is more than 10% per year. It remains to be seen whether this is feasible based on the year over year weakening that's anticipated. But with commodity prices still well above historical averages, there could be some hope. Even so, it might be better to assume that management will not deliver on growth. It might be best to value the company based on data from 2022 and 2023.

{kind=link}

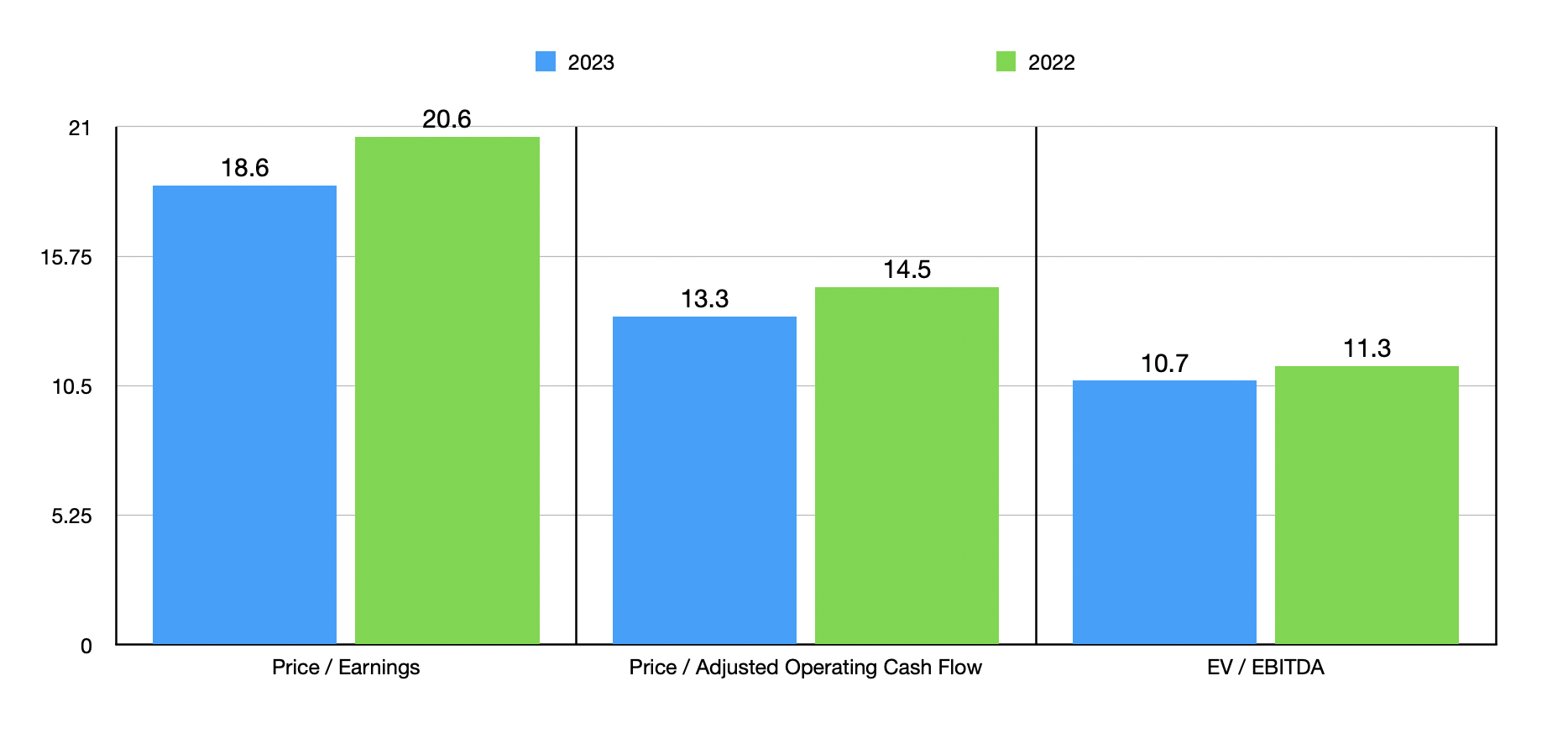

Following in that approach, I was able to value the company as shown in the chart above. The stock does look a bit cheaper using data from 2023 as opposed to last year. The stock isn't exactly cheap, but I wouldn't describe it as expensive either. I then compared it to five similar firms as shown in the table below. Using both the price to earnings approach and the EV to EBITDA approach, I found that four of the five companies ended up being cheaper than it. This number drops to two if we use the price to operating cash flow approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lindsay Corporation |

| 18.6 |

| 13.3 |

| 10.7 |

| Titan International ( TWI ) |

| 5.3 |

| 3.9 |

| 4.2 |

| The Toro Company ( TTC ) |

| 23.4 |

| 29.6 |

| 15.5 |

| CNH Industrial ( CNHI ) |

| 6.7 |

| 17.8 |

| 8.3 |

| Deere & Company ( DE ) |

| 11.3 |

| 15.8 |

| 9.8 |

| AGCO Corporation ( AGCO ) |

| 7.8 |

| 8.4 |

| 6.0 |

Takeaway

Based on all the data provided, I would argue that Lindsay Corporation is doing quite well for itself, even though revenue has pulled back some. In the long run, I suspect the company would do just fine. But there is a good amount of economic uncertainty and shares are a bit pricey compared to similar firms. Given this combination of factors, I am not yet comfortable upgrading the company to something more bullish. And because of that, I have decided to keep it rated a ‘hold’ for now.

For further details see:

Lindsay Stock: Exceeds Q4 Expectations, Still Maintaining My Hold Rating