PARAA - Lions Gate Entertainment Stock: Too Cheap To Ignore At Current Price

2023-08-16 14:20:51 ET

Summary

- Lions Gate Entertainment Corp. has made the decision to divide its studio assets, its STARZ streaming business, and its content production, allowing investors to value each entity separately.

- The acquisition of eOne brings established content for kids into Lions Gate's library, with potential for increased earnings by 2025.

- Lions Gate recognizes the profitability of faith-based content aimed at a specific audience niche and sees it as a profitable moat.

Above: No matter how entertainment is delivered, it all comes down to the total eyeballs needed for a sustaining market share. Lions Gate can do it.

Real world takeaways from the company’s August 9 th earnings call—ex of the happy talk still moves us to call it a buy:

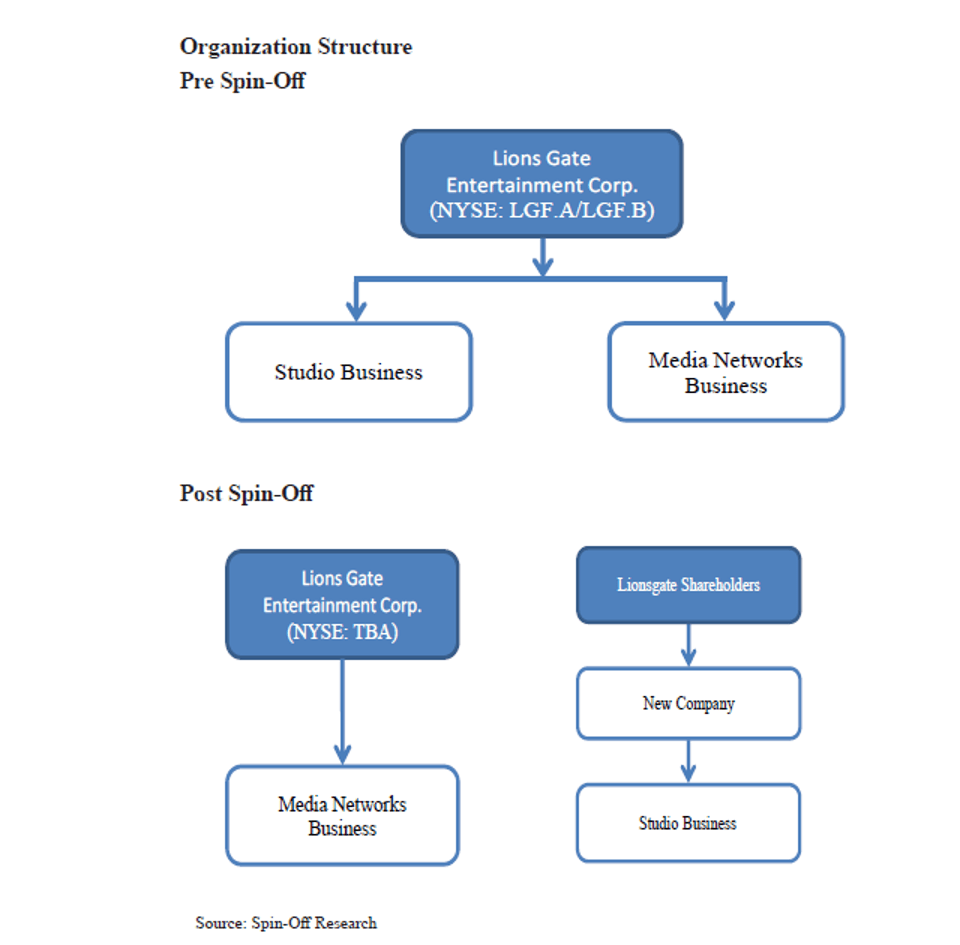

Lions Gate Entertainment Corp. (LGF.A) (LGF.B) has made a foundational decision that makes financial, marketing and the most elusive sense of all, common sense: Dividing its studio assets as pure producers of movies, TV shows as an emporium of content for itself and all comers, and its STARZ streaming business, is a logical solution. It recognizes the real media world we now live in. Investors can now value each entity on forward performance data relative to those vertical sectors alone.

LGF.A’s acquisition of eOne brings lots of ground rooting established content for kids into the corporate library. That list does not contain some of eOne’s gems. But if anything, LGF.A is good at the game of creating and marketing B level moving wallpaper—cheap to produce, able to find audiences. The $400m deal brings 6,500 titles of LGF.A. Some investors think LGF.A has overpaid. But at its birth, eOne represented a $4b investment by Hasbro (HAS). The haircut has been taken by them, the value for LGF.A will be seen in forward earnings by 2025.

LGF.A maintains a sleeper vertical in its Kingdom Story shows, which are faith-based content aimed at a very specific audience niche—mostly bypassed by competitors. No, unto itself it’s not a game changer. But it recognizes a moat, be it small, that can be very profitable and understandable: you make a product that fits the needs of the spiritual audience it is aimed at. Unlike the woke mandarins of Disney (DIS), Netflix (NFLX), and Paramount Global (PARA), LGF.A sees a niche presumably too narrow to pursue.

80% of the LGF.A library revenue comes from IP driven out of its own studios vs. 60% ten years ago, which was either acquired or managed for a third party.

{kind=link}

Source: Equity Clock. A reasonably balanced historic flow-through should continue once the STARZ spinoff is complete by year's end.

STARZ’s production output will move to 28 features a year to 2023, and advance to 40 in 2025, which will include its flagship moneymaker, John Wick . (Chapter 4 will debut in ’25). Awaiting release imminently are three biggies: Hunger Games , a Michael Jackson film, and Ballerina — all aimed at built-in audiences. Add the potential of a MONOPOLY movie, already in progress

STARZ has 29.4m subscribers, down 300,000.

OTT subscriptions sit at 19.9m globally, YOY growth 9%. Valuing the vertical for clearer appraisal can’t really bring insight for investors until the spinoff is complete by the end of this year. Yet what looms as a positive is the spinoff itself as a way to really build value as STARZ. It won’t have to keep in the rat race with big streamers being fed by its own content source in the LGF.A entity. (The SEC Form 10 is filed for the spinoff, but the closing of the eOne deal comes first and delays the separation.)

STARZ has bundle deals with MGM+, Pluto, and other small supported operators that represent cheap marketing that makes sense going forward.

LGF.A exited Latin America. The reasons alluded to may or may not be just concerns about its problematical partners, but probably in poor results. Nobody walks away from a productive, profitable business unless it’s time to sell and take cash off the table. But what supports our case for management here is the gut check that said: it’s a loser—your first loss is your best loss. However, in the earnings call , management noted that cash still owed to LGF.A from LatAm during the wind-up against exit costs will offset, and no actual loss will be shown.

{kind=link}

Above: The proposed spinoff produces two well-balanced entrants into the media sector that clarifies valuation for both.

Feltheimer’s focus is rooted in his resume

CEO Jon Feltheimer is a product of the world of movie/ TV content during its glory days. He was a key guy in the development of TriStar Pictures, then supervised a series of mega-hits for TV under Sony. You can trace that evolution down through to 2000, when he took on LGF.A as CEO. His strength lies in developing genre content at budgets that hold promise of profitability with as little standard Hollywood crap-shooting as possible. That is evident in the steps the company has now taken to save itself from the current maelstrom in media and entertainment.

LGF.A

Above: The next chapter of Hunger Games should have a built-in audience showing the tentpole has legs ahead.

Why Lions Gate--too cheap to ignore--- is being ignored

Price at writing: $7.40

52 week range: $5/46---$12.09

Market Cap: $1.7b

Stock is down 29% since beginning of this year.

Book value: $3.14—stock is trading at ~35% above book.

Our sense here is that a company selling so near to book value, having taken viable steps to address its weaknesses and challenges in what is really a chaotic market at the moment has built value not yet baked into its trade. Clearly, earnings release happy talk is not execution. In this case however, I am betting that the moves are correct and will result in higher valuations.

Taken alone, the decision to split off STARZ recognizes that streaming services freed of the complexities of living within companies with related or barely related units have had their day. The vast media emporiums resemble the department stores of yesteryear. Pots and pans, shirts and socks, appliances, cookware. Shoes. Kid departments. Restaurants on premises. Sunglasses, t-shirts, jewelry and fine China. Amazon (AMZN) and pandemics changed all that.

Yet what we have seen thus far from the major media operators is little more than a tweak here and a nudge there. Not exactly arranging the deck chairs on the Titanic, but believing that mass layoffs and organization charts revised, price hikes and all will do the trick. Maybe, maybe not. In LDF.A, reality bit, and they apparently have acted.

Whenever STARZ begins life as a standalone entrant into the streaming sector, it will be easy for investors to understand. Its advances or losses of subscribers will be clearly linked to its revenue stream and earnings. Its ability to crapshoot at an economically sound level will inevitably hit a blockbuster or two, build subs, lose a few, but overall prove it can go head-to-head in the great crap game of streaming.

Meanwhile, it will have a load of everyday genre content no better nor worse than peers in the moving wallpaper category. Produced with tight budgets, reaching payback faster, dumped faster if they fail. That prompts us to believe that buyers of LGF.A at $7.54 in the parlance of crap games,. Betting the line and backing up with odds. They’’ be leaving the wild prop bets to their bigger peeks. And that’s the best way to play the game. The financial structure, it must be said, is another matter. It clearly is part of the reason LGF.A is trading at such a low range these days. Investors can’t really see their way clear to the company liberating itself in a reasonable time from the heavy burdens of its balance sheet .

TTM

Cash on hand: $323m

Revolver available: $1.5b How much will be tapped post spin off is not really clear yet.

But they have bought back $85m of their bonds for $60m.

They have repurchased $285m of their bonds for $200m. This moves have reduced net debt by $90m. It’s a start.

Total debt: $4.62b (mrq). Like their peers, this feels heavy in terms of the overall outlook on the FCF on the way as the fodder with which to service the debt.

Current ratio: 0.38. This is a little flag, but a red one. LGF.A will need to continue its aggressive program of buying back its debt and its equity to get its long term debt down to a more comfortable level that will begin—we believe—to spark new interest in the stock and move it smartly north.

Levered FCF: $1.07b. This is a good start toward what we believe will be significant improvements once the separation with STARZ is complete by year’s end.

Operating cash flow: --(84.9m). This of course is not pretty but a turn to black is built into the key decisions noted above at the top of this article.

TTM operation quick snaps

Revenues: $3.971b EBITDA: $345M

Net income AVI to common ---(1.90b)

Book value: $3.14

Conclusion

We like the logic expressed by LGF.A management in splitting its studio production and corporate business from its STARZ streaming vertical. We believe it materially increases investor clarity on the stock and its potential. In comparing it with all other streamers, from the giants, would-be giants, and mass pure plays like Netflix, we believe that the stock has been beaten down below its real world forward prospects.

Its CEO is at heart a savvy evaluator of content given his background in overseeing a floodtide of hits both at his TriStar film tenure and especially his Sony TV track record. Investor focus as rightly been on the biggies as they struggle to lift themselves out of the mud piles created by the pandemic, its aftermath and their own excessive poor decisions. LGF.A has hardly been immune to these headwinds. Yet in their most recent policy shifts and decisions we are beginning to discern a pattern of not only survival, but one which could set a robust new parameter as to how to make money in this crazy-quilt world of streaming video.

So there it sits at $7.40 a share in a kind of afterthought limbo beaten down by a not very pretty debt profile, not fully understood content strategy that engenders little conviction. Clearly, price alone is never a good rationale to buy or pass on a given stock. But when that price does not in our view realistically appraise a possible upside sneak attack on vulnerable targets resulting in higher valuations, it’s time for another look.

We like LGF. A to move higher as their moves clarify ahead and reach close to if not meet its 52 week high, ~$12.

For further details see:

Lions Gate Entertainment Stock: Too Cheap To Ignore At Current Price