EBAY - Liquidity Services Stock Is Cheap But Isn't A Buy Yet

Summary

- Liquidity Services is an online marketplace for reselling surplus goods in the retail and capital goods markets, mostly under brands liquidation.com and allsurplus.com.

- While growth in its core business slowed in Q4, it appears to be short term in nature as a result of less used car inventory from government sellers.

- As businesses look to generate fresh working capital from excess/idle assets in 2023, Liquidity Services could benefit from growing supply coupled with its growing buyer base looking for value.

- While the stock trades at less than 0.5x run-rate GMV, the stock sits underneath technical moving averages and insiders aren't buying the stock.

- Gross Merchandise Volume (GMV) needs to re-accelerate for the stock to be actionable.

There is a lot to like about Liquidity Services ( LQDT ) as a business and investing theme as we enter 2023.

The most obvious reason is that the company runs a number of online marketplaces to resell used and excess inventory and assets for its customers, primarily in the retail segment under liquidation.com brand and for capital goods and other excess equipment under its allsurplus.com banner. For a view inside LQDT's reverse supply chain business, which manages returned and unwanted goods for retail partners, CNBC ran a segment last February to highlight this $644 billion end market.

LQDT's exposure to the "circular economy" sector seems timely given where we stand in the economic cycle and growing tailwinds of ESG and value-oriented consumer behavior as inflation remains high. Therefore, Liquidity Services could be setting up to asymmetrically benefit from countercyclical forces should the economy slow and financial distress heighten.

But that doesn't mean the stock is a buy yet, given LQDT stubbornly trades underneath its moving averages, coupled with non-company specific risks in the equity markets. The company also guided to lackluster growth in its current Q1 FY2023 quarter, suggesting flat to slightly higher gross merchandise volumes (GMV) compared to the year-ago quarter.

Part of the problem appears to be a lack of supply in key segments, such as used vehicles available on its marketplaces, and a delay in ramping up its real estate businesses where it is helping municipalities sell seized real estate online (from failure to pay property taxes). I expect real estate sales to be a large growth vector for LQDT over time in an immense addressable market. The company disclosed on the December earnings call that it has a growing backlog of agreements in place with municipalities across the country, but the inventory hasn't shown up on the marketplaces yet as a result of various residual government policies around forbearance.

To that end, I recommend monitoring LQDT in case any material catalysts appear as a result of economic dislocations during this cycle whereby LQDT could pick up significant supply for its marketplaces or if the stock gets washed out in a market-wide panic.

The company is also run by savvy owner-operator CEO Bill Angrick who has significant skin in the game, owning 23-24% of the company, and he manages the balance sheet conservatively and allocates capital prudently. He has proven to be a timely buyer of LQDT shares in the open market in the past, although he currently is a net seller of LQDT shares given a 10b5-1 plan established in August 2022. If Mr. Angrick begins to buy stock aggressively again, as he did in 2020, that would indicate a very strong buy signal, in my opinion.

Importantly, Liquidity Services also benefits from network effects of an online marketplace designed to connect buyers and sellers in highly fragmented markets.

Moreover, the business model has transitioned over time from first-party sales where LQDT took on inventory risk to largely a third-party self-service consignment model which has created a higher quality revenue stream from recurring, high-margin commission revenue while reducing working capital requirements of taking possession of inventory.

This evolution to a 3P model also creates an incentive for sellers to use Liquidity Services marketplace because it can lead to higher recovery rates after backing out LQDT's take-rate coupled with a growing base of quality buyers, currently sitting at 4.9 million active buyers.

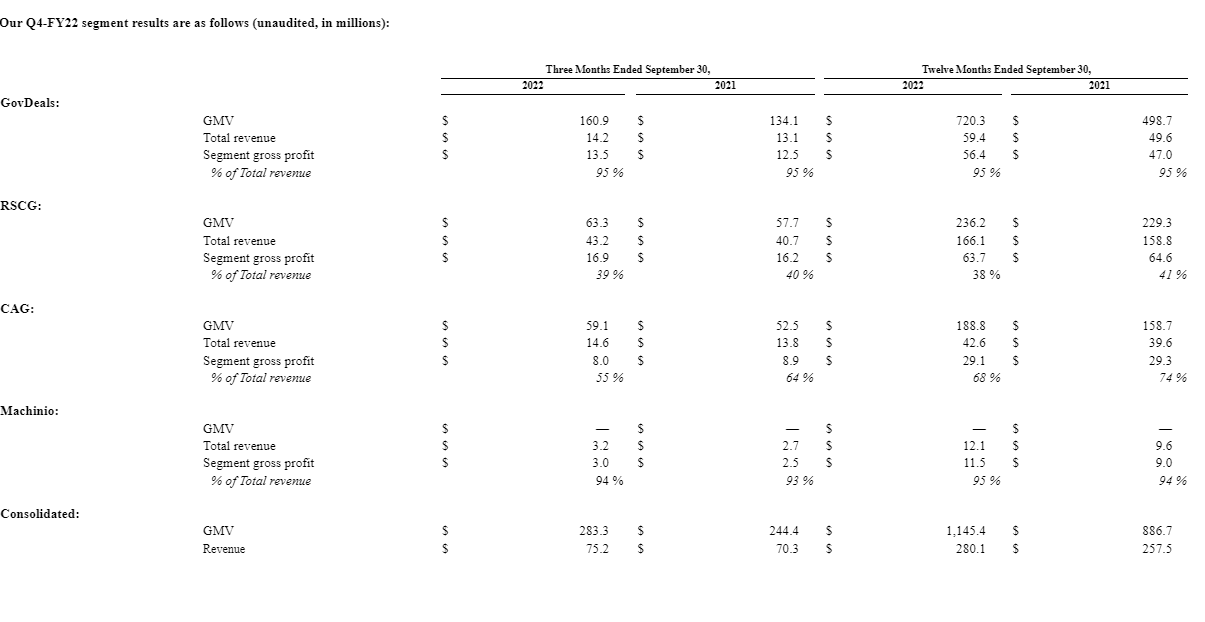

Q4 Results and Outlook

The company reported the following headline results for Q4:

Gross Merchandise Volume (GMV) of $283.3 million, up 16%, and Revenue of $75.2 million, up 7%, from higher consignment activity.

Non-GAAP Adjusted EBITDA of $12.3 million, up $0.9 million, and Non-GAAP Adjusted Diluted EPS of $0.19, down $0.08 reflecting our higher effective tax rate.

Cash balances of $97.9 million with zero financial debt and trailing 12-month operating cash flow of $44.8 million.

{kind=link}

The company also provided the following guidance for Q1 FY2023:

GMV to range from $265 million to $295 million.

GAAP Net Income to range from $1.0 million to $4.0 million.

Non-GAAP Adjusted EBITDA to range from $7.0 million to $10.0 million.

Given LQDT reported $260 million GMV in the Q1 FY2022 quarter, the growth rate year-over-year is stagnating while sequential growth will likely decline, due in part to seasonality. Liquidity Services' marketplaces generally benefit from higher levels of supply and demand in the post-Christmas quarter ending March 31 in its reverse supply chain business, and in the spring and summer months in its All Surplus business, which focuses on capital equipment.

Competition Grows

While LQDT has carved out a powerful and sticky customer base in the government sector, and it enjoys a pole position in being the primary source for providing local, state, and federal government agencies surplus programs across the country, it does appear that competition in its used equipment market is growing considerably which could impair its non-government supplier base.

To that end, given the immense size of the equipment resale market, other players such as eBay ( EBAY ) and Ritchie Bros. ( RBA ) are investing considerable capital in the sector to increase the size, scale, and reach of their platforms.

In September 2021, eBay announced it "doubled down" on the used equipment market with its strategic investment in Bidaroo as a result of a rapid movement of used equipment auctions to purely online auctions. This is precisely where LQDT plays as an online native auction platform for used goods.

And Ritchie Bros. announced in November 2022 its planned acquisition of IAA ( IAA ) for $7.3 billion versus $14.5 billion in gross transaction volume (GTV), about a 0.5x multiple of GTV. The acquisition was motivated by access to a greater supply of used and salvage vehicles, a growing network of buyers, and increased scale in the industry.

Given the rapid consolidation in this sector, and because LQDT would be immediately earnings accretive to an acquirer, one has to wonder if LQDT would itself become a takeover candidate at the right price. That decision would be made by Mr. Angrick, and I don't see any desire on his end to sell the business he founded, especially considering the growth opportunity still ahead of him.

Conclusion

Liquidity Services is a well-run company with multiple levers to drive growth going forward in its large and growing end markets. But it does face significant competition from larger players and the macroeconomic backdrop remains uncertain, although it does appear favorable for the countercyclical nature of Liquidity Services' collection of businesses.

But there are significant stresses on other players in the end markets Liquidity Services serves, particularly for used cars, as platforms such as Carvana ( CVNA ) face considerable going concern risk. To that end, it is hard to know how it shakes out given the competitive nature of this market, but LQDT could be in line to pick up share if other competitors fail. Given the strong balance sheet, asset-light model, and large buyer base, LQDT has the type of operating model that can provide leveraged EPS growth if it sees a step-up in its gross merchandise volumes.

At this point, a significant reacceleration of growth remains unclear. Absent a significant catalyst against the backdrop of increasing competition in the used goods space, while LQDT does appear like a decent value investment, there might be a better time to invest as this market unfolds if investors are looking for exposure to the circular economy theme.

For further details see:

Liquidity Services Stock Is Cheap But Isn't A Buy Yet