LAD - Lithia Motors Driving More Strong Revenue Growth Through 2025

2023-06-23 11:00:46 ET

Summary

- Lithia Motors' share price has risen by 36% in the past six weeks, and the company expects to nearly double its revenue from $28.2 billion in 2022 to $50 billion in 2025.

- The company's growth is driven in large part by its acquisitions, and it has a history of delivering big revenue increases.

- Lithia Motors is considered a buy due to its growth targets for 2025, with 90% of its free cash flow allocated to growth.

The share price of Lithia Motors, Inc. ( LAD ) has risen dramatically in the past 6 weeks. From a low of $206.65 on May 4, 2023, it rose to $281.20 at the close on June 22. That’s a 36% jump.

That’s great if you already owned the stock. But what if you’re thinking about buying now? What do the fundamentals suggest for the future if we plan to keep the stock for several years?

About Lithia

The company is an automotive aggregator with 296 dealerships, representing 40 brands in the U.S., Canada, and the United Kingdom.

In the first quarter of 2023, it acquired 37 new locations while divesting one. Those purchased dealerships are expected to deliver more than $2 billion a year in new revenue.

The dealerships offer what’s called a full suite of financing, leasing, repair, and maintenance services.

In addition, Lithia has developed Driveway and Driveway Finance Corporation, its online ecommerce platform. Although the company does not break out online sales revenue, it reported an average of 2.4 million monthly unique visitors in the first quarter earnings release.

Finally, it offers GreenCars, an information, branding, and shopping portal for electric vehicles.

Revenue, EBITDA, and earnings

In the first quarter of this year, revenues grew by 4%, to $7 billion. That continued an accelerated uptrend that began in 2020:

During the quarter, new and used sales grew by 4% and 6%, respectively, while service, body, and parts revenue were up 17%. Driveway Finance also contributed, by originating almost $630 million in loans.

EBITDA declined in the first quarter, which it also did in the fourth quarter of 2022:

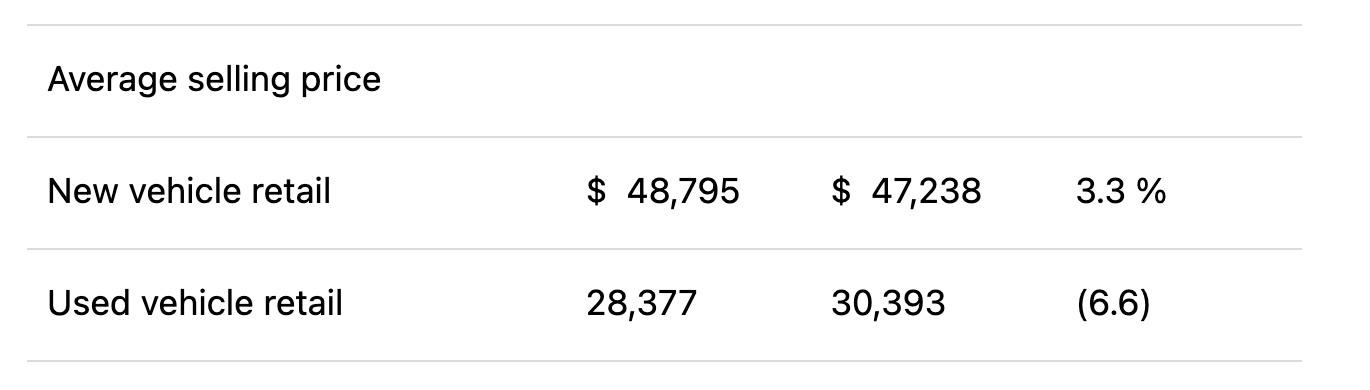

One reason for declining profitability in the past two quarters has been the depressed price of used vehicles. This excerpt from the Q1-2023 earnings release shows the modest gain on new vehicles and the proportionately bigger loss on used vehicles:

{kind=link}

But the prices of used vehicles may pick up in the second quarter and beyond, with the Bureau of Labor Statistics reporting that the used cars and trucks index was up 4.4% in April.

Earnings were also hit on the other side of the ledger in the first quarter. The cost of new vehicle sales was up 10.7%, leading the way to a gross profit decline of 5.2%. SG&A expenses also climbed, by 3.3%.

All of that added up to a 29% decrease in adjusted net income per diluted share, from $11.96 in Q1-2022 to $8.44 per share in Q1-2023.

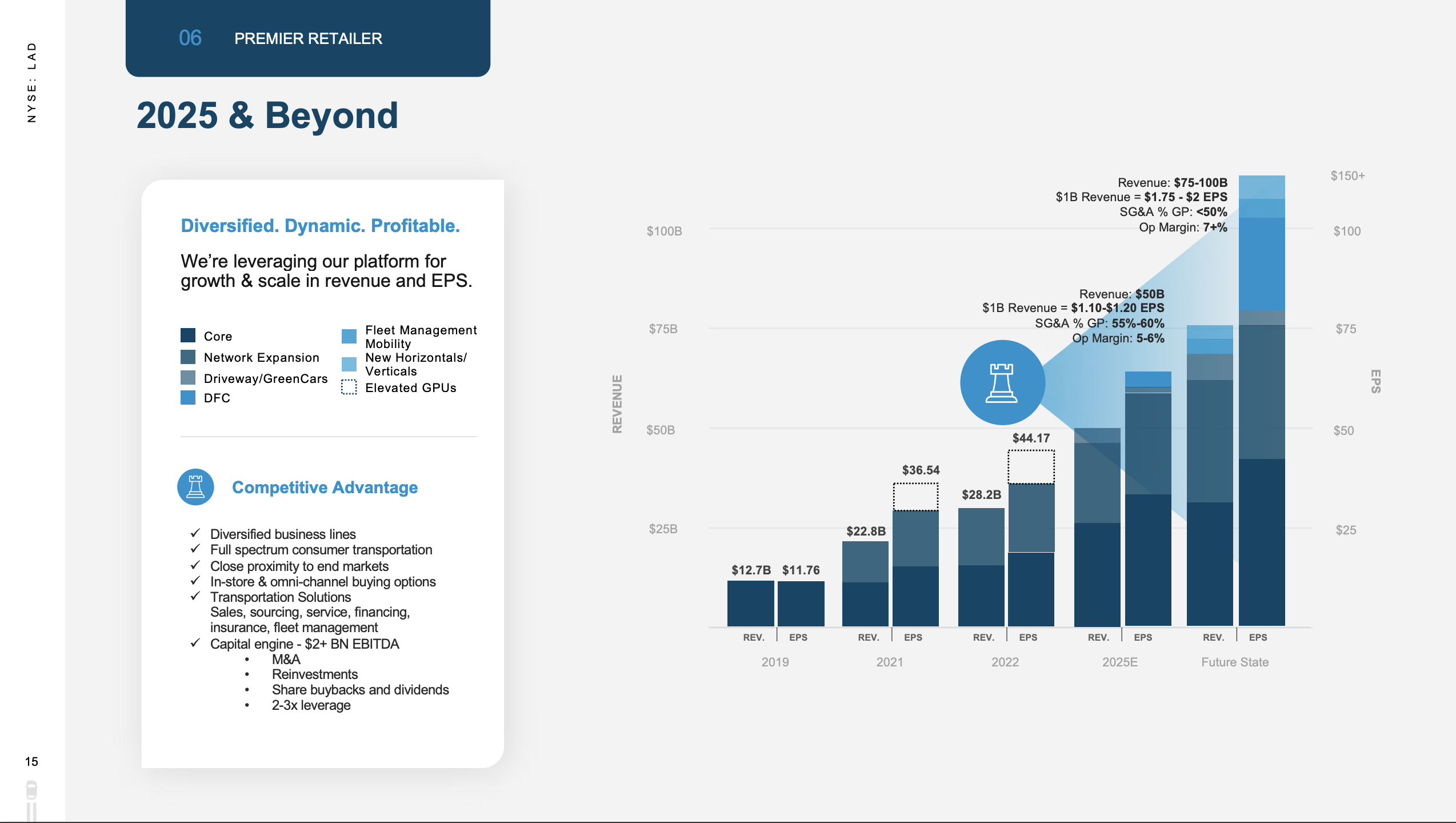

Longer term growth

Lithia expects to nearly double its revenue over the next two and half years, from $28.2 billion in 2022 to $50 billion in 2025. This slide from the Q1 earnings presentation provides details:

{kind=link}

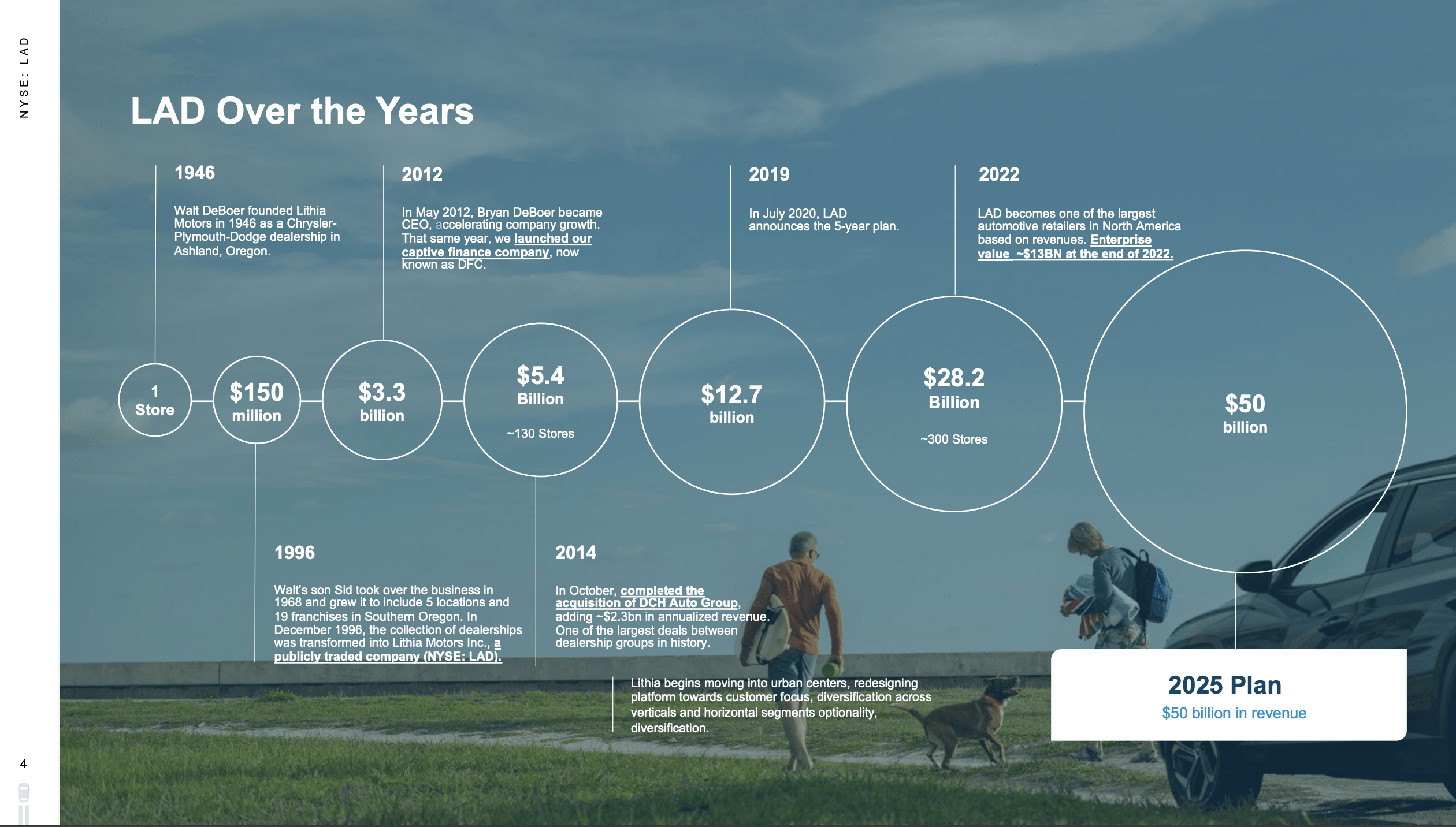

Can it deliver on such an ambitious goal? It probably can, given how quickly it has grown in the past, as shown on this slide:

LAD historic growth chart (LAD Q1-2023 earnings presentation)

{kind=link}

Behind that growth is a business model that features acquisitions. As the company wrote in its 10-K for 2022:

Our disciplined approach focuses on acquiring new vehicle franchises, which operate in markets ranging from mid-sized regional markets to metropolitan markets. Acquisition of these businesses increases our proximity to consumers throughout North America. While we target annual after tax return of more than 15% for our acquisitions, we have averaged over a 25% return by the third year of ownership due to a disciplined approach focusing on accretive, cash flow positive targets at reasonable valuations.

The company has delivered significant growth in the past and I see no reason to think it won’t do the same in the next three years.

Dividends and repurchases

In the first quarter, Lithia increased its dividend to $0.50 quarterly and $2.00 annually. With the share price at $281.80 on June 22, that worked out to a 0.71% yield.

The company has increased its dividend by an average of 9.86% per year over the past five years. Dividend growth has increased every year for the past 11 years, and the payout ratio is low, just 4.32%.

The dividend gets poor ratings from the Seeking Alpha quant system; however, we must recognize Lithia is still a growth stock.

Shareholders also get a modest boost, in theory at least, from share repurchases. In the first quarter, the count was reduced by 7.1%, from 29.6 million in Q1-2022 to 27.5 million in Q1-2023.

Capital allocation

Lithia articulated its capital allocation plan in its 10-K for 2022.

It puts 65% of free cash flow toward acquisitions, 25% toward capital expenditures, innovation and diversification. The final 10% goes to shareholder returns in the form of dividends and share buybacks.

Valuation

Curiously, the Seeking Alpha quant system gives Lithia an overall valuation grade of D. That’s despite the fact that only one of 16 metrics is substandard: the dividend yield grade is D-minus.

Otherwise, we see a lot of A and B grades. The P/E non-GAAP, on a TTM basis, is A-minus. On a GAAP basis, it receives an A.

The price-to-sales ratio is graded A-minus, and the price-to-book ratio checks in with a B-plus.

However, the overall grade makes some sense when we look at a five-year price chart and that increase over the past six weeks:

As noted above, that’s a jump of more than 36%. While I’m not a technical analyst, I do note that the price is getting close to the $300 mark. That’s where the price stalled out in February this year.

Other perspectives

Seeking Alpha analysts and the Quant system give Lithia a Hold rating, while Wall Street analysts rate the stock a Buy.

In the first quarter, insiders bought 6,427 shares and sold 2,251. Over the past twelve months, they bought 77,845 and sold 41,554 shares. CEO Bryan DeBoer has a sizable commitment to the company’s success, with 257,487 shares as of February 22.

Winding up

I give Lithia Motors a Buy rating, not because of any short-term possibilities, but because of its growth targets for 2025. That's backed by the allocating 90% of its free cash flow to growth.

We’re talking about a near doubling of revenue, and the company’s history suggests earnings could grow that much as well. Even if it only grows 25% or 50%, it would still provide a reasonable return to shareholders.

For further details see:

Lithia Motors Driving More Strong Revenue Growth Through 2025