LAD - Lithia Motors Inc.: Robust Revenue Growth Digital Dominance And Strategic Vision For LT Growth

2023-11-01 02:55:43 ET

Summary

- Lithia Motors showcased strong financial performance in Q3 2023, with increased revenues and impressive adjusted diluted EPS.

- The company's sales trends in the new vehicle and after-sales sectors are encouraging, despite challenges in gross profit per unit for new vehicles.

- LAD's focus on digital engagement and e-commerce, along with its strategic financial direction, sets it apart from its peers and indicates promising future growth.

Overview

My recommendation for Lithia Motors, Inc. ( LAD ) is a buy rating. In 2023's third quarter, LAD showcased remarkable financial strength, underscored by an uptick in revenues and a commendable adjusted diluted EPS. This strong result is further amplified by encouraging sales trends in both the new vehicle and after-sales sectors. Even amidst the challenges related to the gross profit per unit for new vehicles, LAD's unwavering commitment to maintaining a comprehensive inventory highlights its dedication to meeting customer needs. Their digital endeavors, characterized by a significant online footprint and an expanding focus on e-commerce, resonate with their ambition to emerge as a premier global omnichannel firm. Additionally, LAD's strategic financial direction, emphasizing long-term growth and value enhancement, coupled with their better financial metric benchmarks, distinguishes them in comparison to their peers. Considering these factors and the potential for double-digit returns, LAD's outlook looks promising.

Business

LAD is one of the largest automotive retailers in the United States, offering a wide range of new and used vehicles, vehicle financing services, and automotive repair and maintenance. Operating through various stores and online platforms, the company provides a comprehensive automotive shopping experience, catering to both individual consumers and commercial customers. With a focus on digital engagement and e-commerce, LAD has been expanding its online presence, aiming to establish itself as a leading omnichannel provider in the automotive industry. Their business model encompasses the entire vehicle ownership lifecycle, ensuring customers have access to services, parts, and educational insights, further solidifying their position in the market.

Over the last half-decade, LAD has exhibited sustained growth. The years 2019 and 2020 saw their revenue affected considerably by the COVID pandemic, resulting in growth rates of approximately 7% and 3% respectively, largely due to border closures and lockdowns. However, post the pandemic's initial impact, LAD witnessed a remarkable rebound in sales, registering high double-digit growth rates. While the growth has moderated recently due to challenging year-over-year comparisons, the company is still projected to maintain double-digit growth rates in the foreseeable future.

Recent results & updates

In the third quarter of 2023 , LAD reported strong revenue growth. The company's revenues grew to $8.3 billion, marking a 13% increase compared to the third quarter of the previous year. This growth in revenue was further complemented by an adjusted diluted EPS, which stood impressively at $9.25. Looking into the sales metrics, there was positive momentum in the new vehicle segment, with unit sales rising 5%. Additionally, the aftersales revenues, which encompass services and parts, also grew by over 4%. However, it's worth noting that the gross profit per unit [GPU] for new vehicles experienced a decline. By the end of the year, GPU for new vehicles had decreased by approximately $100 per month, which represents a 19% drop from the figures reported at the end of 2022. Despite this, the company remained well-stocked, ensuring they had an ample supply of new vehicles and parts to cater to customer demand, especially for domestic brands.

During the third quarter of 2023, LAD showcased a robust online presence , reflecting its commitment to digital engagement and e-commerce. The company's online channels attracted an average of 13.3 million unique visitors. This surge in online traffic was achieved even as advertising spending decreased by 10%, highlighting the effectiveness and reach of their digital platforms. Further emphasizing their digital prowess, total e-commerce sales began to play a more dominant role in the company's retail transactions, accounting for 22% of the total.

Building on its robust online presence, LAD has made significant progress in its digital expansion efforts. The company's online Monthly Unique Visitors [MUVs] grew by 34% across their digital platforms. This growth in the digital domain was further emphasized by an increase in digital transactions, which reached over 37,000 units in the quarter, marking a 21% rise compared to the previous year. A standout highlight was the contribution from sustainable vehicle sales, bolstered by educational insights provided by GreenCars. Sustainable vehicle sales accounted for 16% of the total new vehicle sales for the quarter, a notable increase from the 10% recorded in the third quarter of 2022. This digital evolution is in line with LAD's vision to establish itself as the preferred international omnichannel provider, catering to a diverse set of customer needs throughout the vehicle ownership life cycle and across various adjacencies. The company's strategies aim to enhance margins and reduce SG&A through a combination of growth efficiency, diversification, and scale.

During the earnings call, LAD outlined a clear financial strategy focused on sustainable growth and long-term value creation. Prioritizing growth and acquisitions, the company aims to drive its overarching long-term strategy. A cornerstone of this approach is ensuring that acquisitions are immediately accretive to cash flow from the outset. One of the distinctive elements of the LAD strategy is the resilient annual cash flow generated by its existing business operations. This cash flow, combined with the immediate positive impact of acquisitions, positions the company to effectively deploy capital towards strategic growth. By expanding its network, entering new markets, and investing in adjacencies that cater to the entire vehicle ownership life cycle, LAD seeks to provide comprehensive consumer-centric solutions. The company's team is diligently working towards achieving revenue goals and margin expansion. The ultimate aim is for LAD's EPS to revenue ratio to produce $1.10 to $1.20 in earnings per share for every $1 billion in revenue. In the longer term, the aspiration is to generate $2 in earnings per share, reflecting the company's commitment to delivering shareholder value.

Valuation and risk

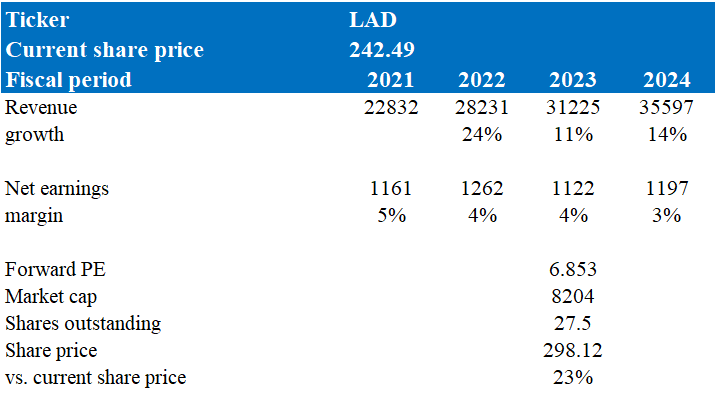

According to my model, LAD’s target price is $298, representing a 23% increase. This target price is based on my growth forecast of a double-digit growth rate over the next two years. This projection aligns with prevailing market sentiments and is underpinned by several key factors. LAD's commendable financial performance in the third quarter of 2023, characterized by revenue growth and a robust adjusted diluted EPS, supported this outlook. The company's positive sales trends, especially the momentum in the new vehicle sector and the uptick in after-sales, further corroborate this growth narrative.

LAD's dedication to digital transformation is evident through its expansive e-commerce endeavors. Their digital platforms have attracted a significant number of unique users, solidifying e-commerce's pivotal role in their business framework. The notable increase in online user engagement, increased digital transactions, and the focus on sustainable vehicle sales accentuate their digital expertise. Moreover, LAD has charted out a blueprint emphasizing sustained and holistic growth. Their strategic pivot towards expansion, underpinned by acquisitions and a consistent annual cash inflow, promises a positive outlook.

{kind=link}

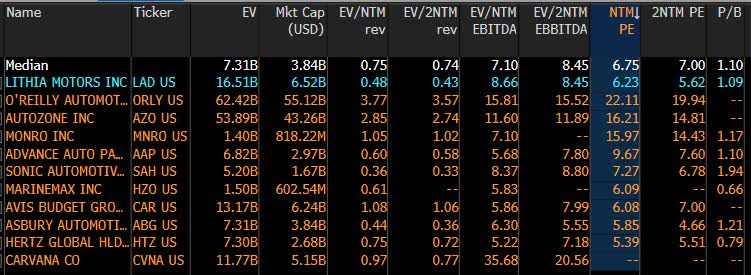

Currently, LAD's forward Price-to-Earnings [P/E] ratio is 6.23x, which is closely aligned with its peers that have a median P/E of 6.75x. While LAD's net margin mirrors the peer median at around 4%, its growth outlook is notably higher. Specifically, LAD boasts a one-year revenue growth rate of 11%, which is significantly higher than the peer median of 3%—nearly four times greater. Given these metrics, there's a strong case to be made that LAD's forward P/E should surpass the median of its peers. Adopting a conservative approach, I've adjusted LAD's forward P/E upwards by 10%, arriving at a 6.85x forward P/E. Based on this new P/E, my target price for LAD is $298. Given the potential for a 23% return, I recommend a buy rating for LAD.

{kind=link}

One potential downside risk to my buy rating for LAD is the cyclical nature of the automotive industry. Economic downturns, supply chain disruptions, or global events can lead to decreased consumer spending on vehicles. Additionally, with the rapid transition towards electric vehicles [EV] and the challenges associated with sourcing EV components like batteries, there's a risk that traditional automotive retailers like LAD might face supply constraints or increased competition from dedicated EV manufacturers. If LAD doesn't adapt quickly to these industry shifts or if there are significant disruptions in their supply chain, it could impact their revenue growth and profitability, potentially affecting their stock performance.

Summary

LAD showcased a commendable third quarter 2023 result, marked by an uptick in revenues and a strong adjusted diluted EPS. The firm's sales indicators point towards an encouraging outlook, with the new vehicle sector being a highlight and the after-sales sector also registering growth. While there was a dip in the GPU for new vehicles, LAD has ensured they're equipped to cater to consumer needs. Their dedication to digital innovation is evident, underscored by their pronounced online footprint and a growing emphasis on e-commerce. This digital initiative resonates with their ambition to emerge as a top tier omnichannel entity. Moreover, LAD's strategic financial plans, which underscore long-term growth, lean heavily on acquisitions that amplify cash inflow. The consistent annual cash inflow, combined with strategic acquisitions, sketches a promising outlook for LAD. Given their financial metrics and growth prospects, I recommend a buy rating.

For further details see:

Lithia Motors, Inc.: Robust Revenue Growth, Digital Dominance, And Strategic Vision For LT Growth