LAD - Lithia Motors Is Crashing

Summary

- In this article, we start by discussing the increasingly depressing outlook for used and new car dealerships.

- Imploding affordability driven by high prices and high rates is causing sales to plummet and financing companies to become desperate.

- Lithia is suffering, too. However, I believe investors should use weakness in 2023 as the company is in a terrific position to generate high long-term returns for its owners.

Introduction

While I am very happy with the way things have gone since 2020 (we went massively overweight value stocks to not only beat the market but also generate high positive returns), I was wrong when it comes to being bullish on Lithia Motors ( LAD ) . In June 2021, I was bullish because of Lithia's fantastic business model and ability to expand in a highly fragmented industry. All of that is still valid. In 2021, I underestimated how bad the situation for consumers would get in 2022 - although I did highlight the risks in 2021. Now, inflation is high, rates are through the roof, and car prices are falling. It's a terrible environment for Lithia and all of its peers. In this article, I will walk you through these developments and explain how I'm dealing with Lithia. After all, I believe it's far from dead money. It's just important to get the timing right.

So, bear with me!

What's Happening?

Used cars were a hot commodity after the pandemic. Car manufacturers were lacking parts to produce enough to satisfy demand, while the pandemic fueled a housing boom and a rising desire for independent mobility (especially because of the pandemic).

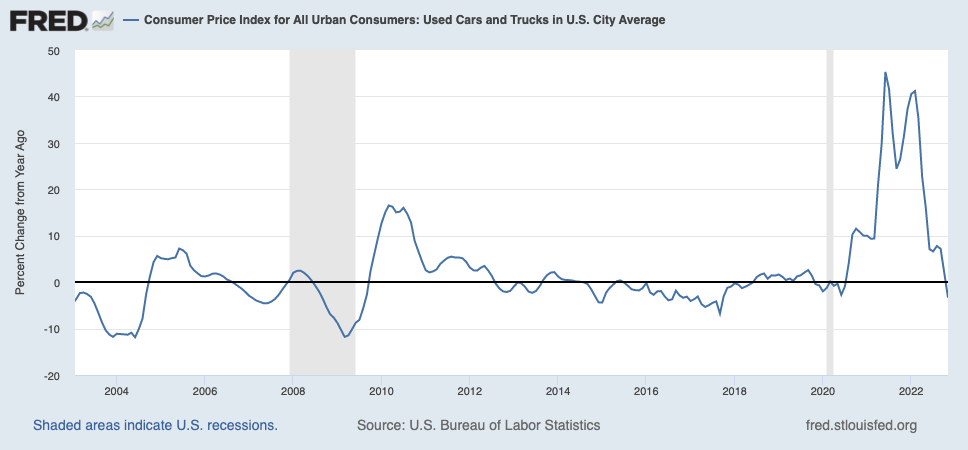

A lot of used cars suddenly appreciated , as there was simply not enough supply. The chart below shows that prices were rising more than 40% at some point. That is more than twice the growth rate after the Great Financial Crisis...

Federal Reserve Bank of St. Louis

{kind=link}

Now, everything is falling apart.

Year-to-date, auto dealers are in a tough position. Only AutoNation ( AN ) is currently outperforming the market on a total return basis. Lithia Motors is down 34%.

CarMax ( KMX ) shares are down more than 50% as this used car dealer and wholesaler has become somewhat of a ground-zero of automotive struggles.

The company reported horrible quarterly numbers, reflecting the ongoing struggles of the automotive industry (in this case, used cars).

Here are some of the things worth mentioning:

- Average contract rate (financing): 9.8%

- Average selling price: +1.9% year-on-year

- Unit sales: -20.8%

- Diluted EPS: -85%

- Halted buybacks

In other words, while pricing is still strong, rates have risen. According to the release:

We believe vehicle affordability challenges continued to impact our third-quarter unit sales performance, as headwinds remain due to widespread inflationary pressures, climbing interest rates, and low consumer confidence.

Moreover, as reported by Bloomberg :

"A gradual backslide in elevated used-vehicle values hasn't prevented consumers from heading for the exits, prompting a precipitous drop in unit volume for CarMax and motivating a shift toward older vehicles."

That's an interesting comment, as we have to consider the bigger picture.

On the one hand, used car prices have indeed come down. As measured by the Manheim used vehicle index, we see that prices are well off their peak. Unfortunately, prices are still elevated compared to pre-pandemic levels.

Manheim, Cox Automotive

Now, add to this that discretionary spending is under tremendous pressure. Inflation and rates are high, which more than offsets this decline in used car prices.

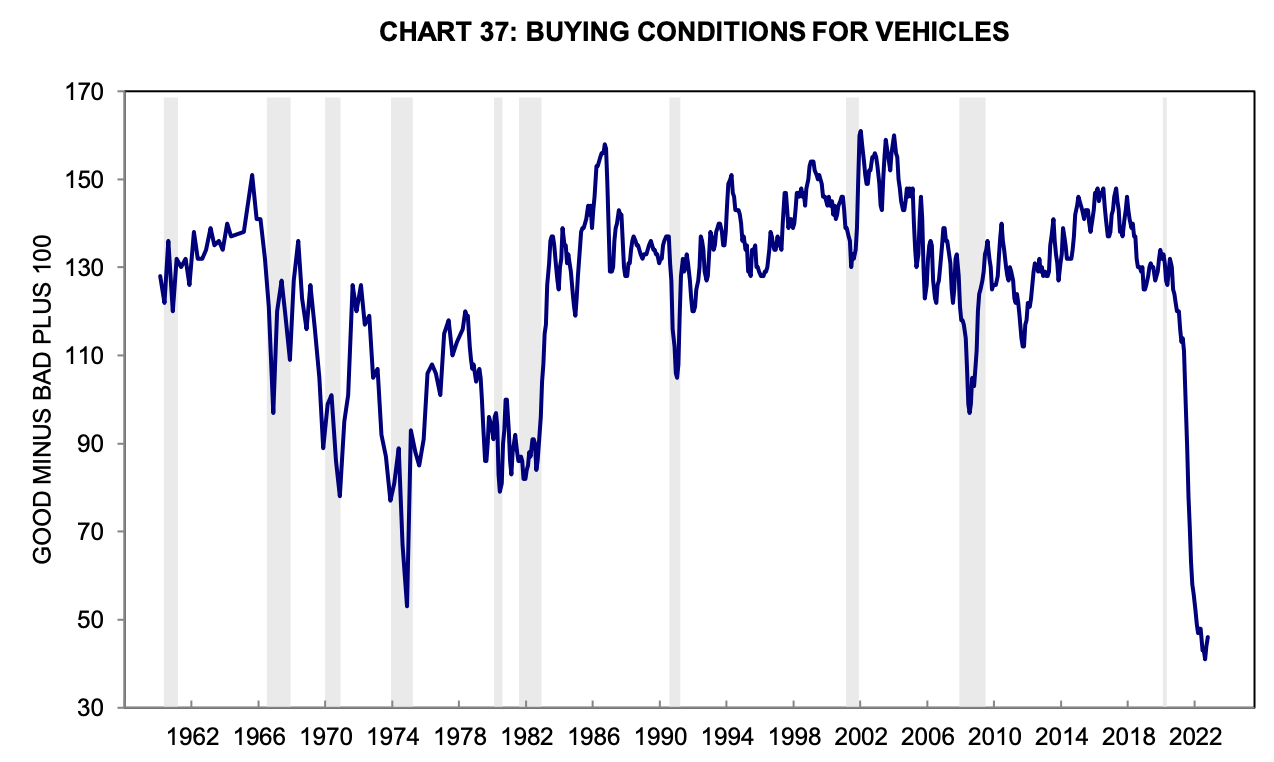

This is what the University of Michigan buying conditions for vehicles chart looks like:

{kind=link}

It's a horrible environment for car companies. According to an industry insider on Twitter named CarDealershipGuy with more than 180 thousand followers, there's more bad news on the horizon as he explained in a recent thread.

Essentially, he explains that the house of cards that was built over the past two years is now coming down. People bought expensive new and used cars with often high loans. Now, prices of some cars have declined as much as 30%, meaning some borrowers are now underwater, owing the bank more than the value of their car.

He noticed that auto lenders have started waiving open auto stipulations.

This is a response to the problem where people who are financially underwater cannot trade their cars. Dealers can't trade the car because consumers owe way too much money on it. This means dealers cannot sell cars, consumers cannot buy cars, and lenders cannot finance cars.

Because some lenders are waiving the open auto stipulation, they let consumers borrow anyway, knowing consumers will default on the loan.

It's what CarDealershipGuy calls a "dog-eat-dog style". Yet, it's the only way to maintain sales volumes.

I've been a doubter, but after what I saw this morning, I'm now FULLY convinced that a wave of car repossessions will hit in early/mid-2023. If lenders are willing to backstab each other in order to put more loans on the road, we're in trouble.

While I'm using what I believe is a very credible source without a motive to lie, I have to say that it also makes sense given the bigger picture. Auto loans are extremely high. Some people are paying double-digit rates on models that have depreciated more than 25% in value.

It's a terrible situation that likely won't end until we get some kind of reset, which comes with high default rates, plummeting car values, and a Fed being forced to pivot.

I hope I'm wrong, but that seems to be what we're dealing with for now.

What It Means For Lithia Motors

As I already briefly explained in the intro, there are three reasons I'm writing this article.

- To discuss developments in the car industry

- To discuss one of my worst calls (a.k.a. eating crow)

- To discuss why I am looking to buy Lithia

A few years ago, I would have looked for opportunities to go short weak players in the industry as part of (for example) a spread trade.

However, as I have increasingly moved towards buying value, I am now looking for the best players that I want to buy at distressed prices.

Lithia is my favorite in this industry. The company has a well-diversified business consisting of new (45% of total sales) and used (34%) cars, wholesale, finance/insurance, and services. Moreover, the Oregon-based dealership company has a well-diversified portfolio of import, export, and luxury vehicles, which is a bonus over any company sticking to a certain brand or niche.

However, that's not even the best thing. Lithia excels at one thing more than its competition. It is able to rapidly grow in an extremely fragmented industry.

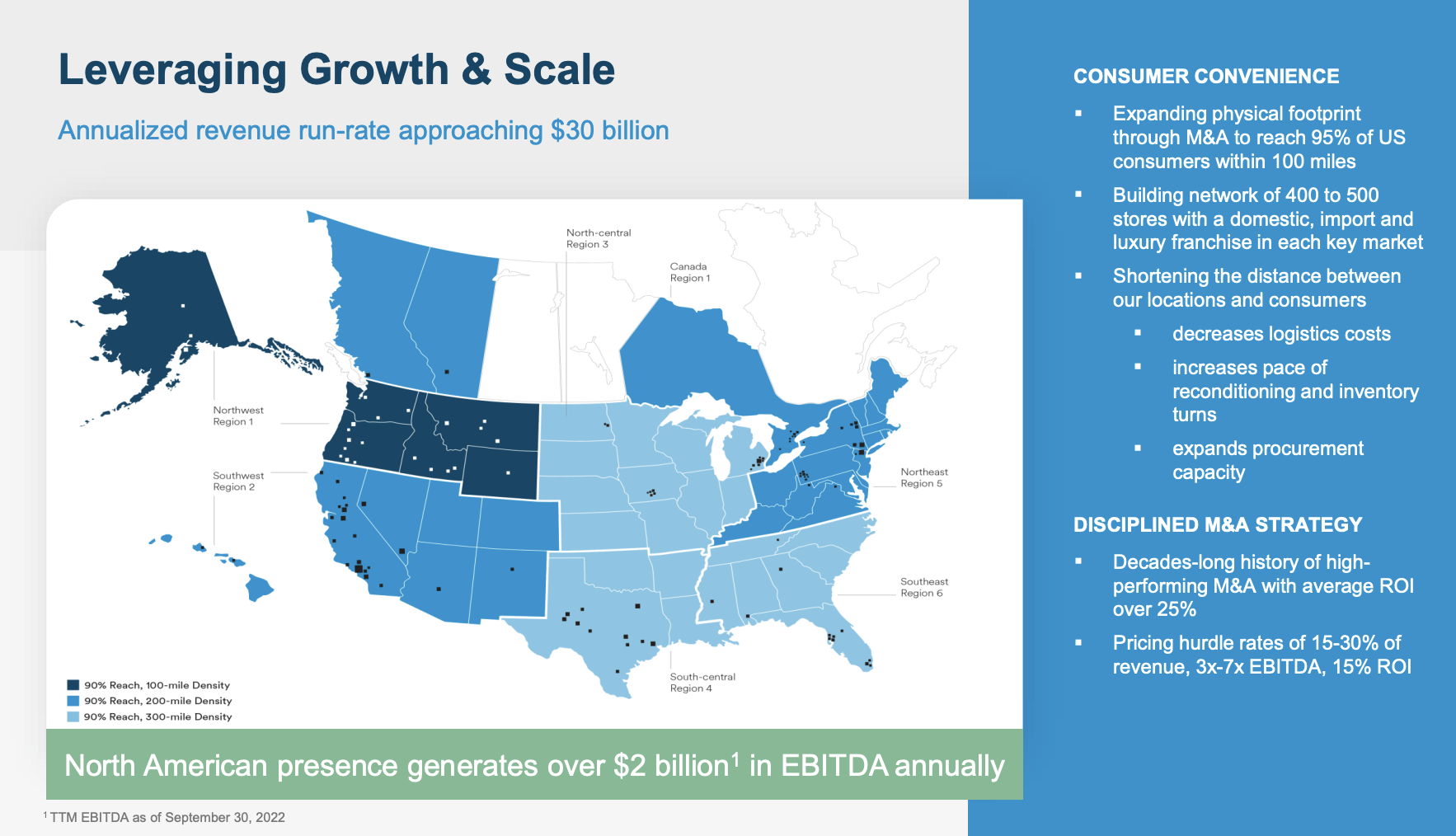

{kind=link}

Through M&A and organic growth, the company is now reaching 95% of US consumers within 100 miles. The company has a market share of roughly 0.5%, with a goal to boost this number to 2.0% in 2025.

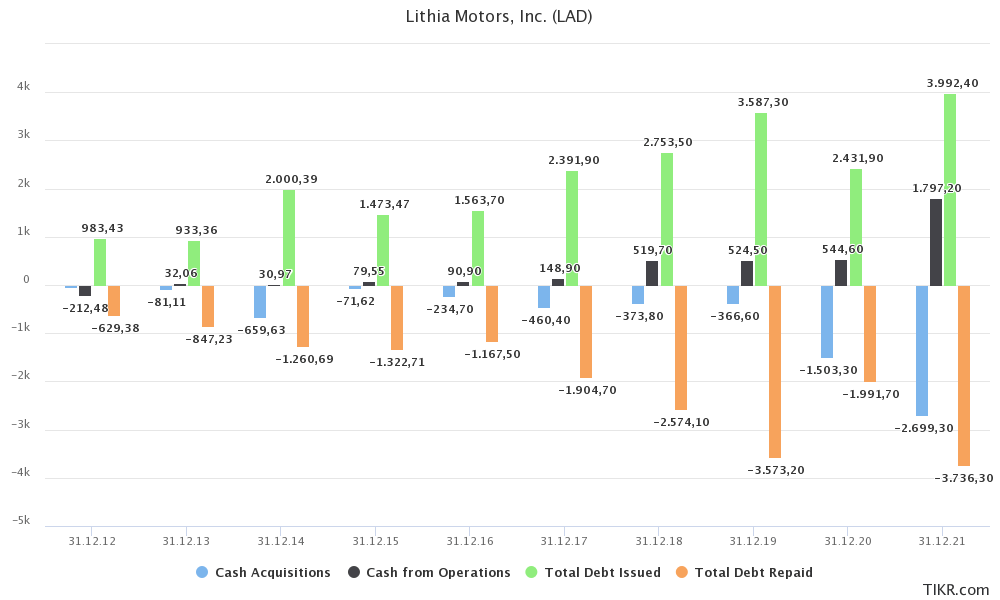

The graph below might seem confusing, but it shows why LAD was able to expand so quickly. The blue line shows cash acquisitions. In 2021 alone, the company spent $2.7 billion on new dealership assets.

The black line shows the operating cash flow. While the company is spending more on M&A than it generates in OCF, we do see that the gap is not wide. While the company is issuing new debt at a faster pace than debt repayments (it has to fill a funding gap), there is not a big gap. The company aims to spend 65% of its capital on M&A. Dividends are just 5% of capital. The dividend yield is currently 0.9%, which is bad news for income-seeking investors, but a great reward for investors with low entry prices, who now enjoy a decent yield on cost.

{kind=link}

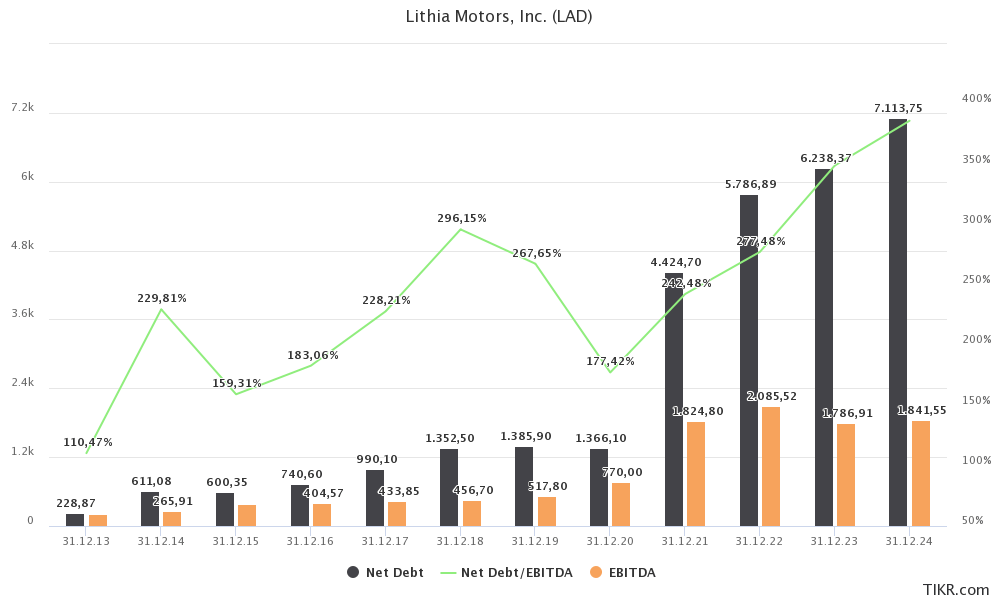

In other words, the company is buying new businesses, improving them, and using accelerating cash flow to buy even more new businesses. As a result, Lithia has kept its balance sheet in check. While net debt (gross debt minus cash) is rising consistently, the net debt ratio has remained below 3.0x. Next year, that is about to change as analysts expect lower EBITDA. I believe that is very reasonable. It may even be a bit optimistic given the headwinds facing the industry. But when it comes to the balance sheet, I'm not worried. The credit rating is BB+.

{kind=link}

According to the company :

Overall, we remain comfortable with current strategy and allocations across M&A, internal investments and balance toward shareholder return. Given the shifting macro environment, we have adjusted some of our focus towards improving our operational efficiency to offset some of the near-term headwinds facing our sector, namely higher interest rates and normalizing vehicle gross profit levels.

So, what about the valuation?

Valuation

Thanks to its qualities, LAD is a huge outperformer in the consumer discretionary sector. Over the past ten years, the stock has returned 480%. That's a fantastic number. Even more impressive is that it includes a steep decline. Prior to the decline, the stock was up close to 1,000% on a ten-year basis.

In my prior article, I wrote two important things. The first part is still valid, the second point turned out to be right - I guess that's one thing I got absolutely right.

1. Lithia Motors is one of the best cyclical stocks on the market. I have little doubt that the company will gain significant market share over the next few years and use this to generate strong EBITDA and free cash flow. As a result, I am long-term bullish and believe that the company will almost certainly achieve a $20+ billion market cap over the next 5-7 years. This assumption is based on the company's ability to achieve its 5Y growth targets and a reasonable valuation.

2. Right now, consumer cyclical stocks are under pressure due to macroeconomic developments. (Potential) investors need to keep this in mind as it could lead to further (unrealized) capital losses. If we encounter a situation where the Fed is forced to hike rates next year to combat inflation, we could see significant short-term stock price declines in the consumer cyclical industry. That could, technically, delay the bull case discussed in this article by 1-2 years depending on the severity of potential economic weakness.

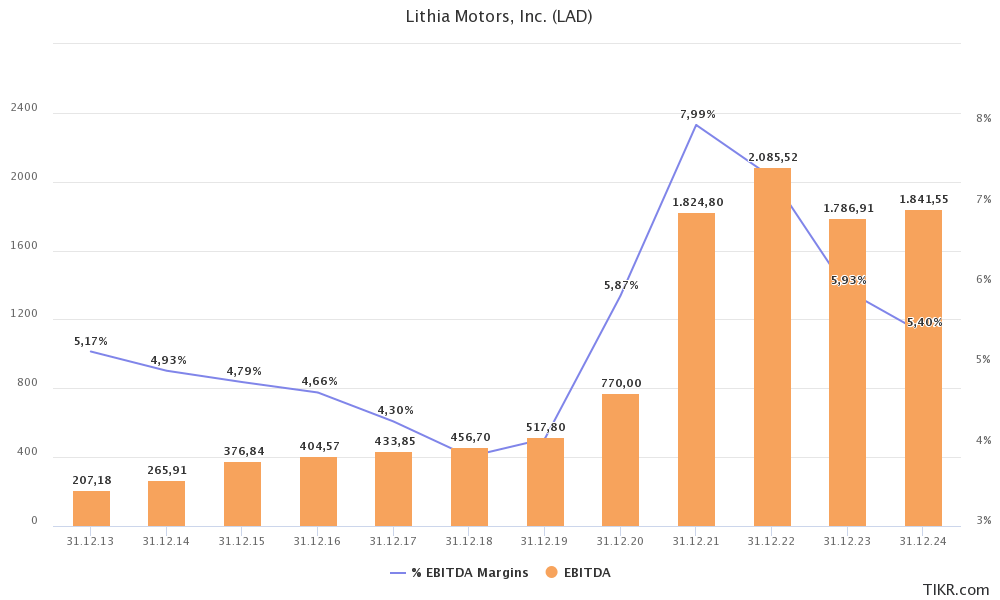

The problem is estimating a shorter-term price target. After all, I believe we could see significant analyst downgrades in the months ahead. For now, it looks like the company will maintain longer-term EBITDA results close to $1.8 billion as acquired growth offsets cyclical weaknesses like lower prices. This will likely push EBITDA margins down to 5.4% by 2024, which is still above pre-pandemic levels.

{kind=link}

We'll also have to wait for weakness to hit LAD's financials. In its most recent quarter, the company grew unit sales by 5.4% with average price growth close to 10%. The fourth quarter will look different.

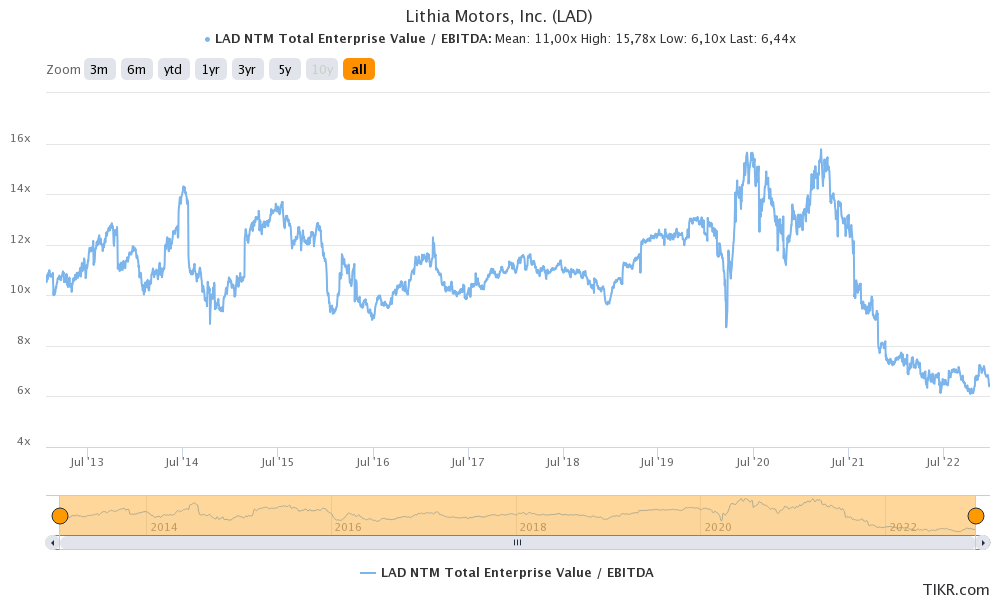

Currently, LAD is trading at 6.4x 2023E EBITDA of $1.8 billion, based on its $11.5 billion enterprise value ($5.3 billion market cap plus $6.2 billion in net debt).

This valuation is well below the long-term average of 11x NMT EBITDA (painting with a broad brush).

{kind=link}

Now, there are two options:

- The market is dead wrong. LAD's market cap should be at least $10 billion.

- The market is way more bearish than analysts as risks are accelerating.

I believe the answer is a combination. LAD is too cheap. If someone were to make a takeover offer, it would have to be at least $10 billion - excluding debt. However, I do not disagree with the market. While there is no certainty in life, I think the odds are high that the industry will run into more trouble.

Hence, I think that there's a high chance of buying the LAD ticker at a better price in 2023.

I'm looking to buy some shares between $140-$150 for my trading account if I get the chance. That's a mile below the current $309 analyst target, which will likely come down a lot in the months ahead.

FINVIZ

Once the bull market returns, I think we're dealing with a stock capable of working its way to a $20 billion market cap.

(Dis)agree? Let me know in the comments!

For further details see:

Lithia Motors Is Crashing