LAC:CC - Lithium Americas: Beware Chronic Lithium Glut And Thacker Pass Project Uncertainty

2024-01-15 00:10:51 ET

Summary

- Lithium prices have collapsed by 85% from their peak due to a glut in the market, which seems to be a chronic issue.

- The Earth has abundant lithium resources, pointing towards a potential long-term glut rather than a shortage, as output estimates may be above demand through 2030.

- The valuation of Lithium Americas depends on the success of its Thacker Pass lithium mine project, which faces uncertainties and risks.

- I estimate LAC is currently trading at a 5-7x "EV/EBIT" range if we account for its project estimates, typical lithium prices in recent years (excluding 2022), and financing considerations.

- I believe LAC's valuation today is only justified if the company can demonstrate it should complete its project on time and on budget throughout 2024.

The long-term potential of vehicle electrification depends significantly on the supply and price of lithium. Lithium is a critical component for battery manufacturing and is one of the highest commodity segment costs within EV production. Historically, an electric vehicle battery might cost $10K to $20K , accounting for a considerable portion of the overall vehicle price. That said, the cost of lithium batteries has collapsed in recent years as lithium supply has risen extremely rapidly . Lithium production has risen faster than demand, creating a glut that has recently caused many miners to avoid the sector.

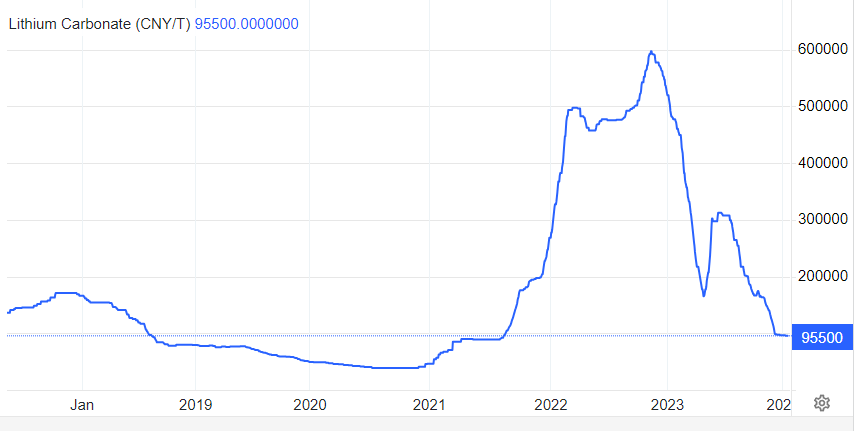

Lithium was in a significant shortage after production cuts and higher demand around 2021. However, EV demand has attenuated since lithium production soared, leading to a massive price collapse. See below:

{kind=link}

These lithium prices are in Chinese Yuan, given that China is the primary battery manufacturer and, therefore, the most excellent lithium price driver. Lithium prices have collapsed by a staggering ~85% from its late 2022 peak to today, leaving lithium prices back near the "glut" pricing range that existed during the temporary 2020 declines in EV demand.

This situation has had terrible consequences for many lithium miners, such as Lithium Americas Corp. ( LAC ). LAC remains far above its 2020 price range but has rapidly erased much of those gains over recent months. See below:

Crucially, at the end of 2023, LAC split into two companies, with Lithium Americas Argentina ( LAAC ) splitting. LAAC has outperformed LAC by a wide margin since the split, likely because LAAC owns key mines currently operating and produced in developed areas with lower breakeven prices. On the other hand, LAC is a 100% owner in Nevada's Thacker Pass lithium mine. With this change, LAC needs close analysis to determine its potential value and risks going forward, particularly given the glut in the lithium market.

The Earth Has Far Too Much Lithium

The company estimates that the mine can produce 40K tons of lithium in its first production phase, with a total potential capacity of 80K tons per year and a 40-year life expectancy. The company has given General Motors ( GM ) exclusive rights to its Phase 1 production for ten years. In perspective, total annual lithium production in 2023 was likely around 170K tons, meaning LAC's mine could theoretically substantially increase global lithium production.

Considering the many lithium mining projects today, analysts expect lithium output to rise to around 500K tons annually by 2030. By then, demand is expected to be around 245K tons per year, pointing toward a sizeable potential glut. Of course, other projections, which may not be based on mine projects but instead on extrapolation , point toward an expected lithium shortage. In my view, the risks of a glut remain higher than the probability of a shortage, given the lithium market has generally been in a chronic glut since the EV market began to grow, leading to historical stagnation for the lithium miner ETF ( LIT ) and its constituents.

Total lithium reserves on the earth are estimated at 88 million tons, a quarter of which is economically viable to mine. That points toward around 40 years of the 2030 projected supply. Of course, just a decade ago, the USGS estimated there were only 13 million tons of lithium, indicating that there could be far more lithium than is estimated today, subject to technological improvements in mining and exploration. With current technology, 22 million tons of lithium should be enough to produce 2.8 billion EVs, twice as many as the 1.4 billion cars on the road today. If we consider technological improvements, it appears very likely that the earth has vast lithium resources. Further, because lithium is produced through brine-water evaporation, mining companies can often scale production comparatively fast, and that scale may improve faster with the newest technologies.

Overall, this points toward a situation where it is likely that lithium miners will generally face a glut compared to a shortage. Of course, as seen in 2021 to 2022, shortages can lead to immense temporary profits but are almost always followed by gluts due to lithium's high supply elasticity. That is to say, the cost of producing a new mine has huge upfront CapEx costs, but the cost of increasing output in an existing mine is relatively small. For the same reason, low lithium prices hardly result in lower production since brine operations rely on continuous output.

What is LAC Worth Today?

Based on data from its estimates , LAC expects to start production at Thacker Pass around the end of 2026 once its current phase is completed, having begun at the end of 2023. The company expects that the capital cost of this will be around $2.27B. The second phase, with construction from 2026 to 2030, is expected to cost an additional $1.73B, ideally doubling production to 80K tons. The company projects that total operating costs will be ~$6.75K per ton of lithium carbonate.

The current USD price of lithium (converted from CNY) is ~$13.4K per ton of lithium carbonate. Historically, lithium fluctuates between around $10K per ton to $25K per ton, though it has gone much higher, as seen in 2022. For our purposes, I will use a $17.5K per ton projection as a long-term average, higher than the current price but within its typical range. If the company's projects pan out (which is not guaranteed), I will project a marginal operating profit of around $10.75K per ton. That equates to an estimated operating profit of around $430M, given its estimated 40K tons per year, or around $325M after estimated taxes.

That makes LAC potentially worth around $3.25B if we assume a 10X "P/E" ratio (given mining firms are more cyclical and, therefore, have lower valuations.) Theoretically, an output doubling from its phase two completion may double its fair value to $6.5B, given it can indeed produce as much lithium as it estimates, which remains unclear.

Based on its last quarterly report , it had a net positive working capital of about $197M. Its total CapEx was $46M, indicating that it has around $2.22B in additional investing needs or around $2.02B in additional financing needs for the first phase of its project. Thus, LAC must sell substantial equity or use other external financing to raise sufficient capital for its project. That figure would be around $3.75B if we account for its projected phase two needs.

Adding these needs to its current $896M market capitalization gives us a "phase one" EV projection of ~$2.92B, ideally delivering a $430M EBIT or an "EV/EBIT" of ~6.8X. If its phase two projections stand true, and my price projections, its EV would be around $4.65B, for a $860M EBIT, or an "EV/EBIT" projection of ~5.4X. Of course, these projections have a high level of potential issues, as lithium may not be priced at $17.5K in the long run as I expect, given that prices still vary depending on geography. Additionally, the company's CapEx, operating cost, project timeline, and output capacity projections may all be off, as is often the case in mining companies.

The Bottom Line

If we consider all the company's estimates accurate and a relatively typical lithium price, then LAC appears to be roughly fairly valued today. While the "EV/EBIT" targets of 5.4 to 6.8X may seem low depending on the project phase, most miners trade in that valuation range. Further, there is an extremely high risk that the company's estimates and projections do not pan out, particularly considering it is looking to produce in the US, which has inflationary issues in high capital cost items and regulatory burdens. The Thacker project has faced regulatory problems but may have an advantage because lithium is a crucial commodity for the transition to clean energy.

I would not buy LAC at its current price. While its valuation is justifiable, mainly if we assume a rise in lithium prices, I feel lithium likely remains "lower for longer" due to its chronic glut. Further, I do not believe its current valuation accounts for the many risks involved in the project, mainly that it takes longer and costs more than estimated or does not have as low overhead costs as projected. Thus, I am neutral on LAC today but could become bullish if the company can sufficiently develop the project in 2024, proving that its estimates will pan out.

For further details see:

Lithium Americas: Beware Chronic Lithium Glut And Thacker Pass Project Uncertainty