URCWF - Lithium Royalty: Crushed IPO With Macro Tailwinds

2023-12-13 18:00:21 ET

Summary

- Lithium Royalty Corp. generates royalty income from its portfolio of 34 mining properties worldwide.

- The company focuses on mining properties that produce lithium and other materials for automotive batteries.

- Its objective is to continually grow its portfolio and net asset value through investments in royalties, with an emphasis on lithium.

- We look at the setup the risk factors and the valuation.

All values are in USD unless noted otherwise.

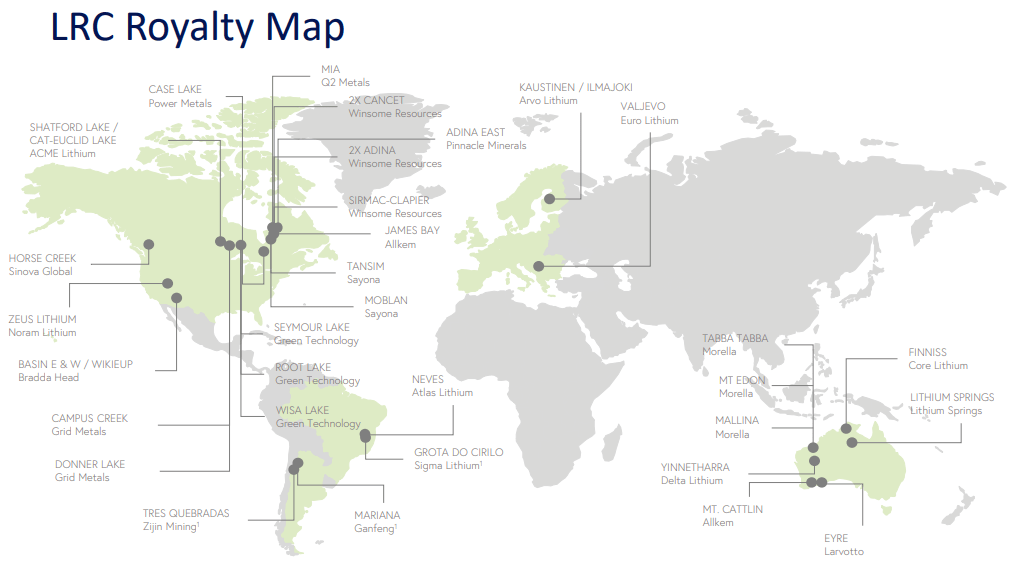

As its name suggests, the bread and butter of Lithium Royalty Corp. ( LITRF , LIRC:CA ) is royalty income. The LIRC portfolio comprises 34 royalty interests in 32 mining properties located in the Americas, Australia, and Europe.

{kind=link}

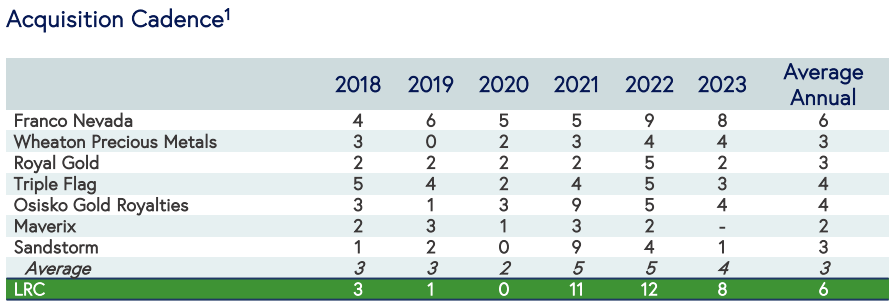

This Canadian business began operations in 2018 and has been adding to its portfolio at a steady rate over the last six years.

{kind=link}

While Lithium Royalty Corp. has been building its portfolio for over half a decade, it made its public debut only earlier this year, in March. LIRC IPO'd with an issuance of 8.8 million shares at a price of $12.35/share. The market has not shared in the company's belief vis-à-vis its value and has pulled it down more than a notch.

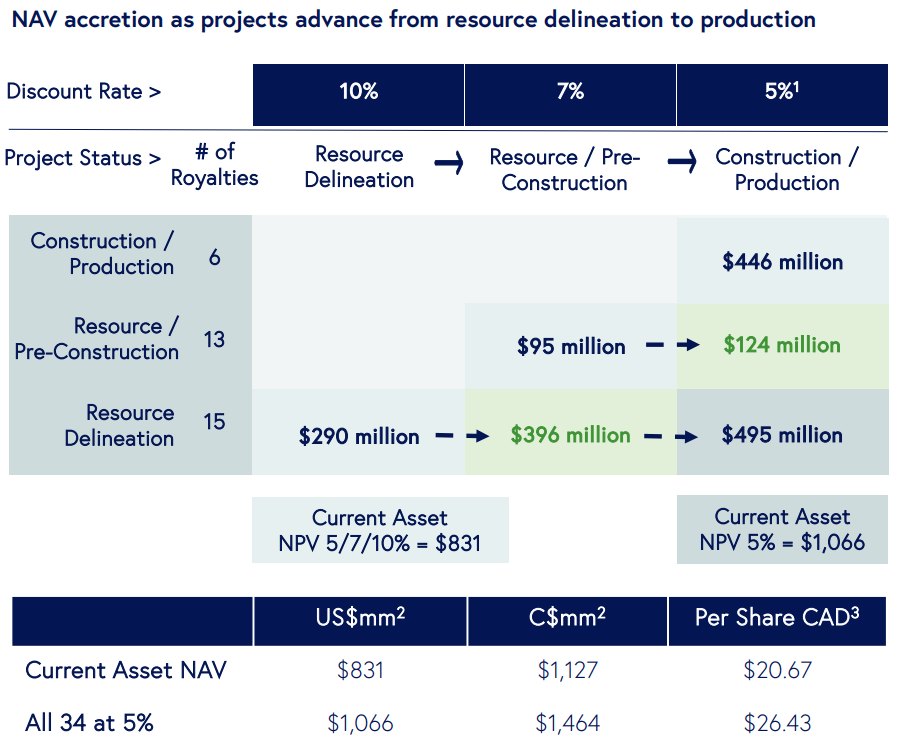

LIRC, however, remains undeterred by the market pricing, and the Q3 results have it estimating the net asset value, or NAV, to be around $15/share ($831 million / 55 million shares outstanding).

{kind=link}

Speaking about the company's portfolio (which forms the predominant portion of its NAV), LIRC targets mining properties that produce lithium and other raw materials for automotive batteries. The "overarching objective" as noted in the MD&A is:

to grow our portfolio and net asset value through ongoing investments in royalties within an electrification and decarbonization macroeconomic theme, with an emphasis on lithium.

The company's current portfolio base shows their commitment to the lithium cause.

Dec 2023 Presentation

Three of the 32 properties in the LIRC portfolio are currently producing the goods, with an equal number in the construction stage. The balance of 26 are in various stages of development and exploration, where no decision has been made to begin construction. In terms of the amount invested by LIRC in these properties, 20% of its asset base is yielding royalties at this time, with the best yet to come.

Dec 2023 Presentation

LIRC expects the construction phase assets to commence production in 2024. On the other hand, the company does not anticipate the 45% to produce until 2025. The LIRC earnings are a mix of Gross Overriding Royalties [GOR], Net Smelter Return [NSR] and royalties based on tonnage. Unlike the tonnage-based rate, the former two are impacted by the realized revenues of the miner.

In all cases, the market price of lithium dictates not only the revenues, but also the rate at which the mining projects move along from development to production. Another all-pervasive factor impacting LIRC bottom line is foreign exchange, since the company conducts its business using the USD, and it does not necessarily receive royalties in the same currency.

Q3 2023 Results

LIRC has 3 out of 32 projects that are producing currently, 2 of which only began production in 2023. This is reflected in the sixfold increase in year-over-year royalty income. On the expense side, the company was hit with expenses related to its public debut, resulting in significantly higher general and administrative outlays compared to the prior year.

{kind=link}

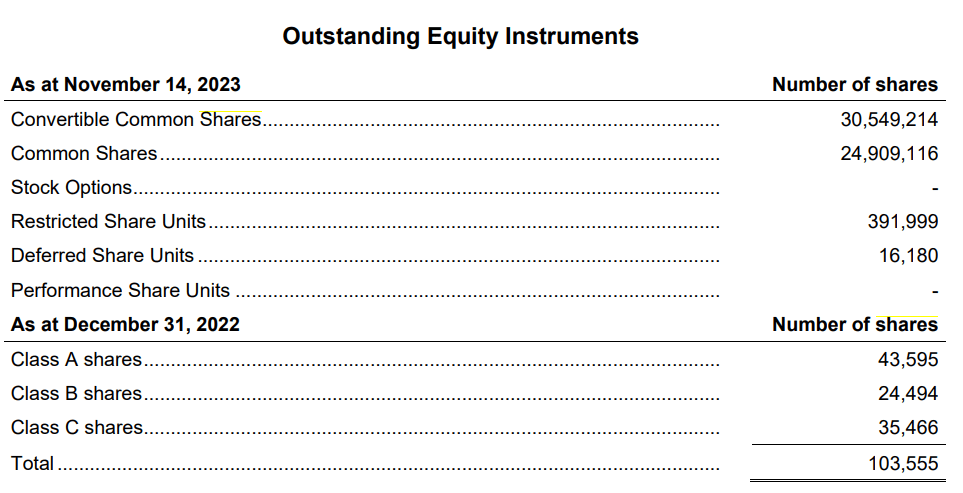

The 103,555 common shares pre-IPO were converted into 46,358,131 common shares during the process. Hence the difference in the respective period ending shares is not as steep as the below comparison would suggest.

{kind=link}

LIRC's cash reserves declined from around $36 million at December 31, 2022, to $13.5 million at the end of September. The 2023 acquisition activity consumed most of this cash. The management indicated that remaining net proceeds from the IPO and the three producing mines were sufficient to meet its operating and working capital requirements for now. In addition, LIRC also has a $25 million credit facility with National Bank of Canada, the funds of which can be utilized for operating and investment purposes. The terms of the arrangement are laid out in the MD&A.

- Base rate loan with interest payable monthly at the National Bank base rate, plus between 2.00% and 3.25% per annum depending upon the Company's leverage ratio; or

- Term loans for periods of 1, 3 or 6 months with interest payable at the rate of term-based Secured Overnight Financing Rate ("SOFR"), plus between 3.1% and 4.5% per annum, depending on the Company's leverage ratio.

As of September 30, 2023, no amounts had been drawn on the facility.

The Macro

The lithium story has been getting a lot of attention over the last 3 years. Just look at some of the comments being made by McKinsey, IEA, and Albemarle Corporation ( ALB ).

{kind=link}

Estimates are that demand will go up 42-fold relative to the 2020 base by the year 2040. It is interesting that we see several stories that copper will be in short supply by 2040, but lithium, which is supposed to outpace that by 14-fold, gets less attention.

Dec 2023 Presentation

Of course, if demand grows as expected, you can expect some severe shortfalls by the time you get anywhere close to that timeframe.

Dec 2023 Presentation

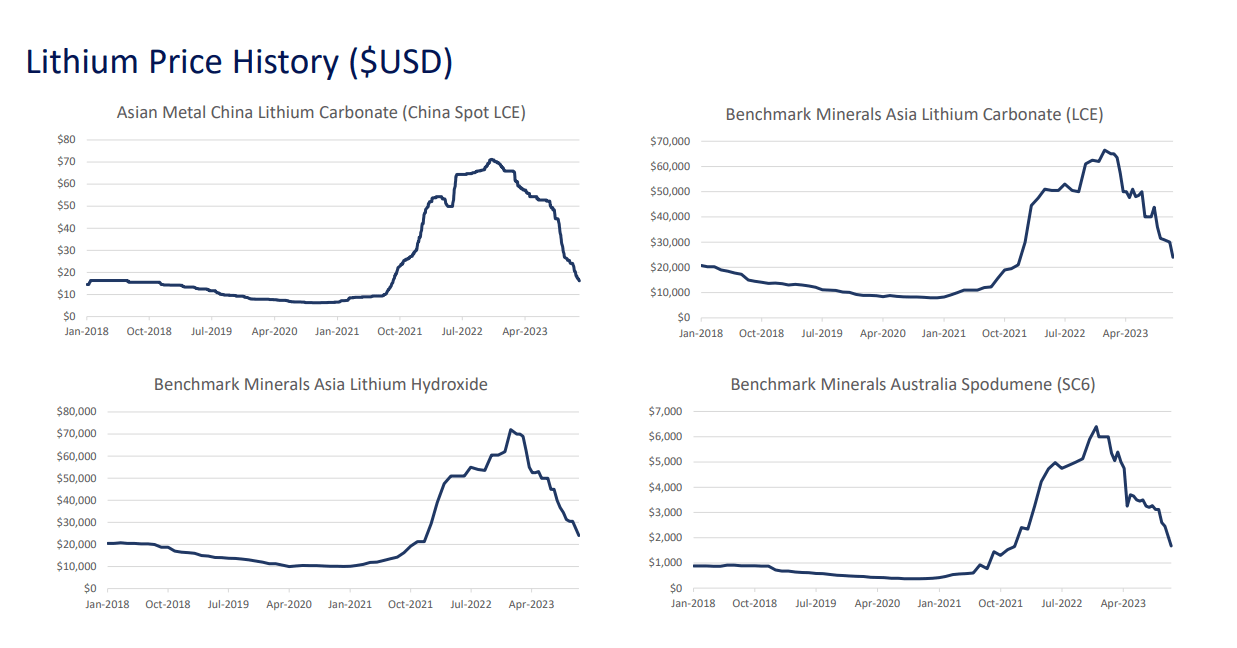

Nobody told the lithium price that story, it appears. The price peaked in early 2023, and has been dropping like a stone since then.

{kind=link}

Our take here is that the story is, of course, as real as it gets. But one must not completely dismiss the counterarguments. From our perspective there are 3 major ones.

1) Lithium may be ruling the roost today, but alternative technologies could displace at least a portion of the total demand. Here is one that investors should watch.

Toyota says it has made a technological breakthrough that will allow it to halve the weight, size and cost of batteries, in what could herald a major advance for electric vehicles.

The world's second-largest carmaker was already pursuing a plan to roll out cars with advanced solid-state batteries, which offer benefits compared with liquid-based batteries, by 2025.

Kaita said the company had developed ways to make batteries more durable and believed it could now make a solid-state battery with a range of 1,200km (745 miles) that could charge in 10 minutes or less.

The company expects to be able to manufacture solid-state batteries for use in electric vehicles as soon as 2027, according to the Financial Times, which first reported on Toyota's claimed breakthrough.

Solid-state batteries have been widely seen as a potential game-changer for electric vehicles, promising to reduce charging times, increase capacity and reduce the fire risk associated with lithium-ion batteries, which use a liquid electrolyte.

However, solid-state batteries have typically been harder and costlier to make, limiting their commercial application.

Source: The Guardian .

2) The second argument is that many of those other elements shown above (like rare earths, cobalt, etc.) could become a limiting factor for total lithium usage. If the car cannot be manufactured due to a shortage of any of those elements, then, well, you won't use the lithium either.

3) The final one is that one should not underestimate the supply response. Supply has been blistering and is poised to increase dramatically in 2024 and 2025. Eventually, the overhang will pass, but it will take some painful years in the interim.

Verdict

Chalk it up to really poor timing. The IPO came right near the price peak for Lithium.

Lithium Royalty Corp. slipped 0.6 percent in its Toronto Stock Exchange trading debut after raising $150 million (US$109 million) in Canada's biggest initial public offering in 10 months.

Shares of the Toronto-based company fell to $16.90 at 9:30 a.m. start of trading Thursday on an "if, as and when issued basis," slightly below its IPO price. The stock was down 1.8 percent as of 9:45 a.m.

Lithium Royalty sold 8.82 million shares for $17 apiece in its IPO, within its targeted range of $16 to $19. That makes it the biggest IPO on a Canadian exchange since last May, when Bausch + Lomb Corp. was spun off in a dual listing and Dream Residential Real Estate Investment Trust went public.

The sale, which confirms an earlier report by Bloomberg, brings another lithium-based company to the Toronto Stock Exchange when the appetite for battery metals is soaring on strong prospects for electric vehicles. The company, which was founded by Waratah Capital Advisors Ltd. in 2018, trades under the stock symbol LIRC.

Source: BNN Bloomberg .

We would have actually liked it more at this point, if the company had raised even more cash at that $16.90 price point. That would have boosted the tangible book value per share (the obvious side effect of raising capital well above tangible book value per share). As it turns out, it was a bit low. Today, despite the near 50% drop, LIRC is not resoundingly cheap on this metric when you run against established royalty companies like Franco-Nevada Corporation ( FNV ), or Royal Gold, Inc. ( RGLD ), or even ones that are not showing any revenues like Uranium Royalty Corp. ( UROY ).

But price to tangible book value does not always capture the potential in royalty plays. This is particularly true here, as the company has been around since 2018 and a lot of the deals were struck during the last famine in this sector. The logic here is that if LIRC strikes deals when the lithium price $10,000 per ton, it will make more money in the long run versus if they do it when lithium price is $60,000 per ton. Analysts have also established this in their models and have tried to figure what the real value of those royalty assets is. In other words, figuring out a NAV.

Dec 2023 Presentation

Everyone concurs that LIRC is radically undervalued based on modeling that, and the numbers are similar to what LIRC uses in its own models. Those NAV numbers above are from November 30, 2023, and LIRC is another 10% lower. So, it is fair to say, you are not buying it with the FOMO crowd at this point. Management is well-aligned here, and Riverstone, which sold Hammerhead Energy Inc. ( HHRS ) to Crescent Point Energy Corp. ( CPG ), also owns a big chunk.

Dec 2023 Presentation

We think Lithium Royalty Corp. stock is a reasonable bet here for the long haul, but tax loss selling likely provides big headwinds for the next 2 weeks.

For further details see:

Lithium Royalty: Crushed IPO With Macro Tailwinds