LFUS - Littelfuse Remains Under Appreciated By The Market

Summary

- Littelfuse reported Q4 and FY2022 results that are showing the impact from economic headwinds in its markets. Guidance was particularly weak.

- We believe headwinds will eventually dissipate, and there are several reasons why the company should eventually return to healthy growth.

- Shares remain under appreciated by the market, despite the company outperforming the S&P 500 index over the past ten years. At current prices the valuation looks very attractive.

We continue to believe that Littelfuse ( LFUS ) is under appreciated by the market. Probably because of its relatively small size, and that it does not operate in a particularly sexy industry, it appears to fly under most investors' radars. The company is not perfect either, as it operates with a high degree of cyclicality. Despite of this, Littelfuse has managed to deliver double-digit revenue and earnings growth for years, and has provided long-term investors with very attractive returns. It has outperformed the S&P 500 index ( SPY ) by a wide margin over the last ten years.

The company just published its Q4 and full-year 2022 results , and it is clear that the company is facing increasing headwinds from a weakening economy, a relatively soft automotive market, and inflationary pressures. As a result of these headwinds the company posted lower earnings in the quarter, and gave relatively soft guidance for next quarter. On the positive side, the secular tailwinds benefiting the company continue to be present. For example, the industrial end markets which include applications such as solar, wind, energy storage, HVAC systems, and factory automation, reported that the rate of new business wins is accelerating. In the transportation end markets the transition to electrified transportation continues to benefit the company. The company shared that it has had more than $550 million in passenger vehicle design wins, and over half are for electrified platforms. This is helping increase the average content across vehicles by double digits. In addition to the EVs themselves, the company is also seeing increased design wins for off-board charging infrastructure. The electronics end markets continue to be healthy as well, with the company securing design wins in several categories including hand tools & appliances, building technologies & automation, and security systems & medical devices.

Q4 and FY 2022 Results

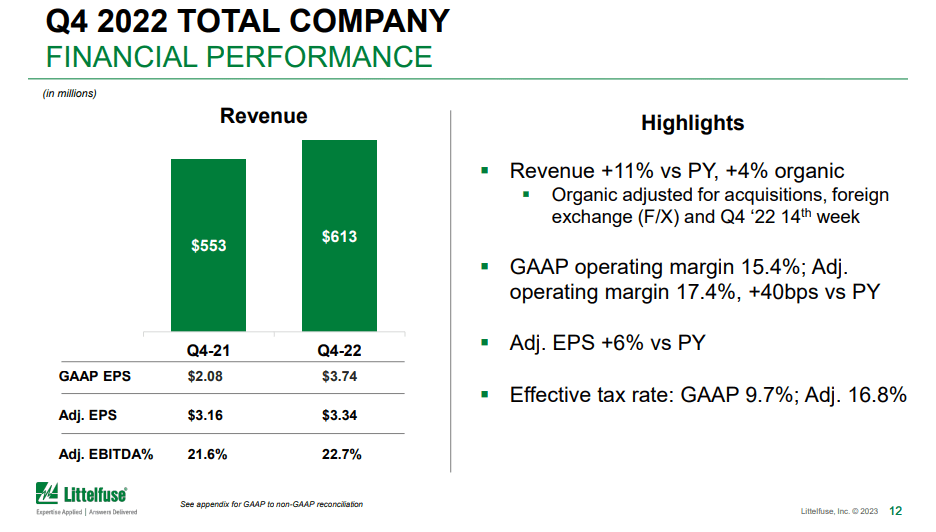

Results for the quarter were certainly a little disappointing, but given the headwinds the company is facing it is understandable that there would be some weakness. Organic revenue growth decelerated to 4%, and adjusted earnings per share increased only by 6% compared to the previous year. What this means for investors is that growth will be below what the company usually delivers while the short-term headwinds continue.

Littelfuse Investor Presentation

{kind=link}

Looking at the results for the entire year, organic revenue growth looks better at 11%, and adjusted earnings per share increased by 28% compared to the previous year. Comparing full year results to Q4 performance, it is clear that there was significant economic weakening in the markets in which Littelfuse operates in the last few months of 2022. Some of the highlights for the year include two acquisitions adding over $200m in sales, and significant progress integrating the Carling and C&K businesses.

Littelfuse Investor Presentation

{kind=link}

Financials

Despite having a high degree of cyclicality in its financials, revenue growth has been averaging solid double digit growth. This can also be appreciated looking at the graph for the trailing twelve months revenue over the past ten years.

Adjusted earnings per share have been growing even faster, with a roughly 17% CAGR. Given the secular tailwinds in many of its markets, and the effectiveness of Littelfuse's M&A bolt-on acquisitions strategy, we believe the company is well positioned to continue growing revenue and earnings at a healthy rate.

Littelfuse Investor Presentation

{kind=link}

Guidance

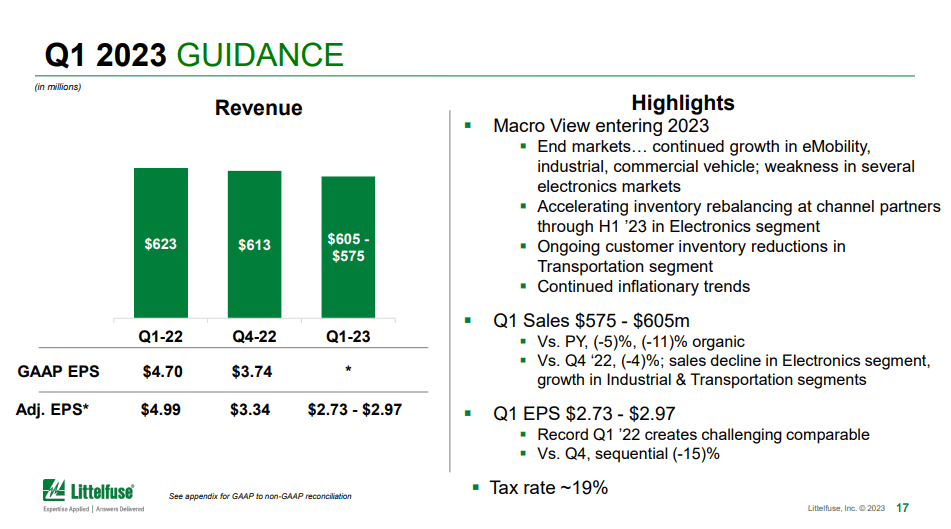

There is no doubt that guidance for Q1 of fiscal 2023 was weak. The company is guiding revenue below that of Q1 2022, and earnings are expected to significantly contract. The company is expecting weakness in several electronics markets, and inventory reductions in the transportation segment. We believe these headwinds will prove temporary, and that the secular tailwinds the company enjoys will eventually help the company return to healthy growth.

Littelfuse Investor Presentation

{kind=link}

Valuation

Based on current prices around $252, and adj. diluted EPS of $16.87 in 2022, shares are trading with a price/earnings ratio of ~14.9x. We believe this is a very attractive multiple to pay for a company that has been growing earnings at a ~17% CAGR. Shares look a little more expensive based on analyst estimates for 2023. Still, earnings should mostly recover by 2024, and are expected to be posting records again in fiscal 2025. Investors should also consider that this is a company with a very solid balance sheet, ending the year with net debt to EBITDA leverage of ~1.2x. We therefore believe that investors willing to wait for the short-term headwinds to dissipate will eventually be rewarded.

Seeking Alpha

Shares are trading a couple of turns below the ten year average EV/EBITDA. The historical discount is even more apparent when looking at the price/earnings ratio.

The ten year average p/e ratio for Littelfuse has been ~30x, and currently they are trading at more than a third cheaper.

Risks

The main risk we see for Littelfuse investors is that of a weakening economy. Its results are already reflecting the impact of the economic headwinds in the markets it serves. That said, the risks are mitigated by the company's strong profit margins and solid balance sheet. The company also sports an excellent Altman Z-score of ~4.3x, comfortably above the 3.0 threshold.

Seeking Alpha

Conclusion

We understand that investors probably have mixed feelings from Littelfuse's earnings results. The impact of economic headwinds is resulting in slower revenue growth and lower earnings. Still, the company continues to report design wins and has strong secular tailwinds that should eventually allow it to return to healthy growth. We believe shares remain under appreciated by the market, and find the current valuation attractive. We are therefore maintaining our 'Strong Buy' rating.

For further details see:

Littelfuse Remains Under Appreciated By The Market