LIVN - LivaNova: Struggling To Eye Value At Current Multiples Reiterate Hold

2023-08-02 02:19:06 ET

Summary

- LivaNova PLC posted mixed Q2 FY'23 results, with growth observed in the P&L and balance sheet.

- The company's Q2 earnings showed top-line growth and margin decompression on an adjusted basis.

- Despite this, I'm yet to be convinced based on the economic characteristics of the business over the long-term.

- Net-net, reiterate hold.

Investment Briefing

LivaNova PLC (LIVN) posted Q2 FY'23 results last week with a mixed set of numbers. Growth was observed throughout the P&L and balance sheet, yet, the firm's economic characteristics languish on my examination. Following my May publication on LIVN, its equity stock has nudged ~24% into the money, surpassing previous valuation estimates in doing so.

In the May publication, I noted the following market expectations based on a 12% discount rate:

- Adjusted for R&D investment, LIVN could produce $300-$320mm in post-tax earnings this year [I've adjusted this down following this latest profiling].

- Taking $300mm, the market had correctly priced LIVN at $2.5Bn market value [in May] with the 12% hurdle rate ($300 / 0.12 = $2,500).

- Investors were selling LIVN at 47x forward earnings at the time of the last publication.

Collectively, these points had me resting at a neutral position on the company.

Rolling forward to the present day, and I've yet to observe a catalyst worth buying into LIVN, now trading at an eye-watering 80x forward GAAP earnings. Granted, this adjusts to ~22x forward on non-GAAP, but the point is, this premium better be justified to advocate a buy.

My analysis opines the premium is unjustified, and that LIVN is trading above a fair value when factoring all economic characteristics of the business. Net-net, reiterate hold.

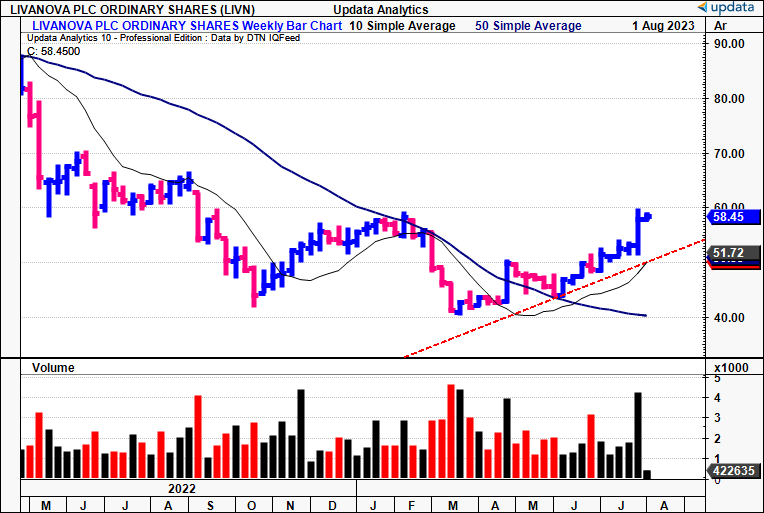

Figure 1. LIVN price evolution, FY'22—FY'23 to date

{kind=link}

Q2 earnings breakdown

As mentioned earlier, unpacking the firm's Q2 numbers gives me mixed opinions about LIVN as an investment grade company. On the one hand, you've got top-line growth and gross margin decompression, that feeds vertically down the P&L. Segmentally, the company did well too. The praise isn't shared via the firm's economic characteristics, however. It has ~$1.4Bn of capital committed to its maintenance and growth operations [including R&D capitalized], yet, the corresponding profitability hasn't surged to a level where I'd expect it to be. A full breakdown of the quarter follows.

(1). Top-line growth

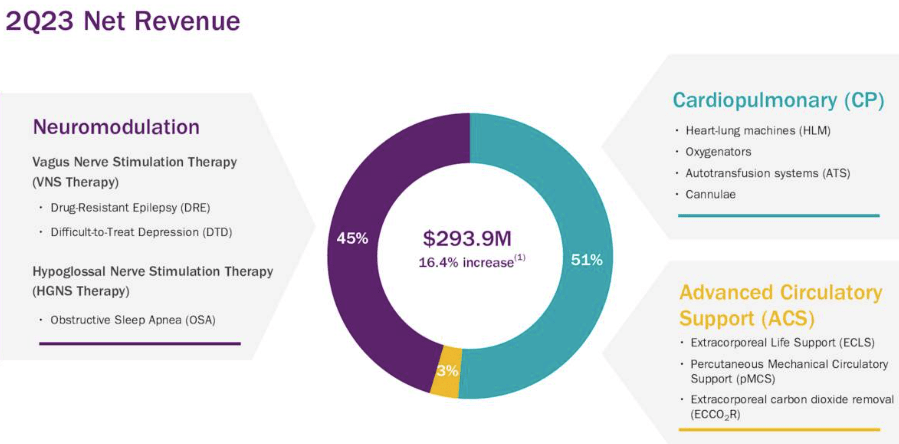

LIVN booked Q2 revenue of $294mm, up 16% YoY. The breakdown on this is quite interesting:

- Management stated that ~600bps of growth stemmed from the combination of price, end-of-service revenues, and oxygenators.

- This tells me the remaining 1,000bps was likely a function of demand [volumes] across its product lines.

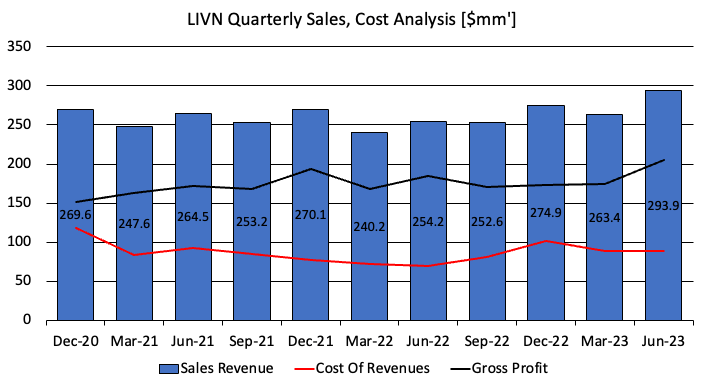

Figure 2. Note the divergence in COGS to gross from Q1 FY'23

{kind=link}

In this inflationary environment, one of the key measures I've been benchmarking company growth against is pricing vs. volumes. It's easy for companies to simply pass through costs [pricing] and book these as revenue increases. Much harder to actually increase the volume [demand] side of the equation: Revenue = units sold x price per unit. It is a little more complex than that—especially in LIVN's case—but the basic premise remains the same. Hence, the demand contribution is certainly noted here.

(2). Margin decompression—mixed opinions

Another potential takeout from Q2—adjusted gross margin loosening up. I would urge this with a word of caution, however, which I'll discuss in a bit. LIVN clipped 72% adj. gross, in what I would say is a significant improvement from the 69% reported same time last year. Again, the decompression came as a result of positive pricing and higher volumes. The benefit of this is the leverage over fixed overhead—ultimately adding to the profitability factor. As mentioned previously, as a collective, LIVN—in my opinion anyway—absorbed a large component of cost inflation quite well as a result of this.

Moving down the P&L, the firm clipped adj. EBIT of $49mm, up from $33mm last year. Operating margins were up 400bps to 17% for the quarter as a result. The same thematic is present—higher revenues, higher gross, equalling leverage over expenditures. It pulled this to adj. quarterly earnings of $0.78, well ahead of consensus estimates.

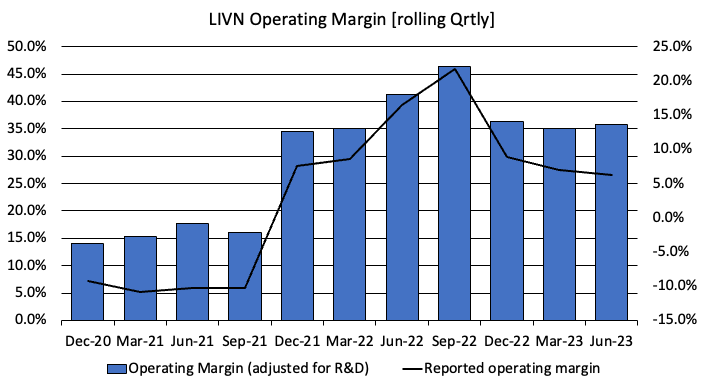

This is all well and good. But the point is, they are all adjusted numbers. It makes me wonder why LIVN even bothered to report GAAP earnings in the first place, because its entire language on the earnings call and in the investor presentation were non-GAAP figures. Some adjustments from GAAP accounting conventions are essential in healthcare companies—lines like R&D and sizing up the salesforce headcount are often expensed on the income statement, rather than capitalized on the balance sheet as intangible assets, and amortized over their useful life. As a reminder, the firm is running a multitude of clinical trials, including the OSPREY study, the ANTHEM trial, and the RECOVER trial. Hence, the R&D investment is of statistical relevance here. Whilst there is discretion over what should be expensed or not, R&D is quite obvious. Thus, performing the same calculus for LIVN's operating margins, albeit adjusted for R&D only, the picture is strikingly different to the firm's language.

Figure 3.

{kind=link}

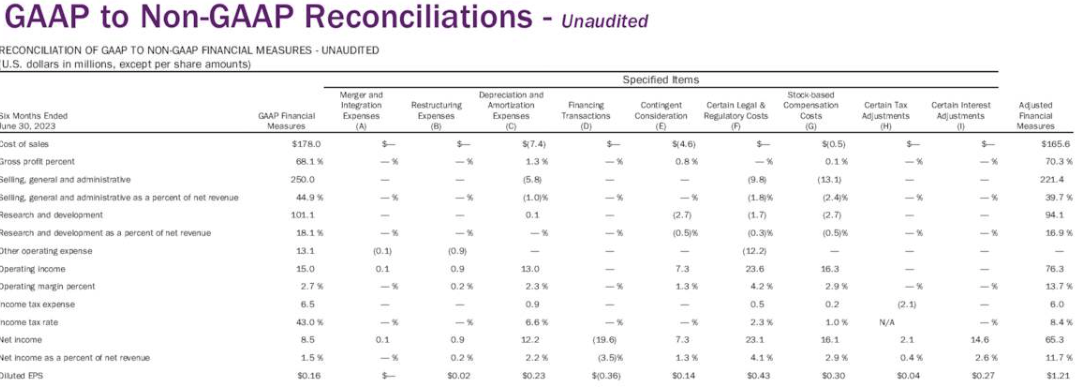

Figure 4. This is one of many "GAAP to non-GAAP reconciliations" shown in the investor presentation .

{kind=link}

(3). Divisional breakdown

The company's divisional highlights from Q2 are as follows:

- The cardiopulmonary segment was 21% YoY with quarterly revenues of $151mm. Underlining this growth were oxygenator volumes, driven by the higher demand function outlined earlier. Additionally, heart-lung machine revenue was over 30% above last year. I noted S5 placements and the first Essenz installations in the EU and the U.S. as key underlings for this.

- Most important to my interest in LIVN is the company's epilepsy business. It saw a 14% increase in sales during the quarter. Critically, the breakdown on this was constructive:

- LIVN booked 838 new patient implants, a 13% growth YoY, and 1,947 replacements of devices, up 8% YoY.

- The point on replacements is interesting. The key product in question here is the SenTiva device —a pulse generator that's used to treat/manage refractory epilepsy. It has a function called "scheduled programming", designed to get patients to an optimal regime of treatment.

- What's been happening is patients are reaching their "optimal therapy" in 6 months, versus the originally projected 12 months. The 50% optimization period is one key factor that is driving the rate of replacements. As a result, the firm is "starting to see the first wave of replacement from those patients who were initially treated with SenTiva" . This is something to be taken heavily into consideration for the epilepsy business in my view.

- Management projects ~7% growth in its epilepsy business for FY'23.

Figure 5.

{kind=link}

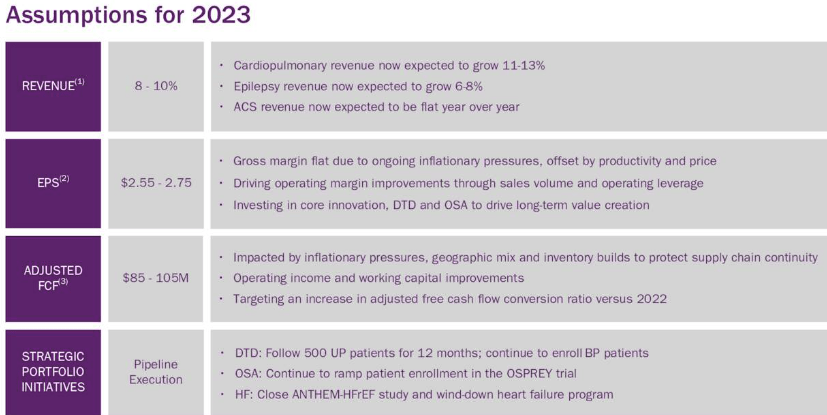

(4). FY'23 projections back to 10% top-line growth

The company revised its full-year guidance based on the momentum shown in H1 FY'23. It now anticipates revenue growth between 8%—10%, calling for $1.13Bn at the top. A 100bps FX tailwind is baked into this.

My numbers have the company to hit $1.3Bn at the top this year, stretching up to $1.18Bn in FY'25. I'd call for LIVN to do ~$57mm in post-tax earnings on that, ~$260mm adjusted for R&D investment. I have revised this number down from my previous estimates of ~$300–$320mm. This is from a reduction in my estimates for the company's R&D spend this year and higher OpEx requirements. Still, it could spin off ~$150mm to $180mm in free cash to its shareholders on these adjusted numbers based on my modelling. This is above management's view of $105mm in free cash flow for the year, a potentially bullish signal.

To get there I would estimate LIVN to invest ~$30mm in growth CapEx, and free up an additional $37mm from NWC. One of the issues I see regarding these projections is that I've got LIV only investing ~2% of earnings back into the business to fund its growth operations. Hence, whilst it could be generating reasonably attractive returns on existing capital [discussed later], the actual deployment of capital at these rates would appear to be sub-standard on my benchmarking, thus limiting the growth of its intrinsic valuation in my opinion. Full FY'23–'26 estimates are observed in Appendix 1.

Figure 6.

{kind=link}

Valuation

One of the challenging points I find here with LIVN is on how to price the company's equity stock. On the one hand, investors are selling the company at 22x forward earnings—more than 80x on GAAP numbers (perhaps this is why LIVN chose to use adj. earnings?)—and they are getting a bid at these prices. The stock is trading above all respective moving averages as evidence of this. To pay $22 for every $1 in future earnings you'd expect two things, 1) profitability i.e. high returns on capital employed, and 2) reasonable earnings growth.

For LIVN, you've hardly got either in my opinion, at least at the moment anyway. For starters I've got the company hitting $47mm in post-tax earnings this year, <1% YoY growth. Into FY'24 and FY'25, I've got similar projections. Hence, you're paying $22 for every $1 in future earnings with no growth on these estimates. Using a 12% discount rate, this doesn't give you any value over the coming 2 years (57/33.3 shares outstanding = 1.71; 1.71/0.12 = $14.20. This is way off the current share price of $59 as I write).

Secondly, even when adjusting for R&D, LIVN has delivered ~2-3% economic profits this year (defined as ROIC less 12% hurdle rate). The value-added on this is therefore thin, and reflected in the company's equity price. I often rhapsodise about the importance of high economic profits. I look to cash + 5% as a major benchmark, and that would be a benchmark of 10.4% at the time of writing, using the yield on the 3-month Treasury bill as a proxy for cash.

Figure 7.

Data: Author

Critically, therefore, my projections lead me to the following conclusions:

- Discounting my forecasts for owner earnings (NOPAT less investments) out to FY'28 at 12%, the base case gets me to a corporate value of $2.12Bn for LIVN's equity stock. In the upside case, I get near the current market value of ~$3.1Bn.

- This equates to an equity value of $40—$57 per share, well below what's currently changing hands in the market as I write.

- Using the FY'23 estimates I've outlined earlier, this gets me to a fair forward P/E of just 8.2x, or 12.2x using the current market value.

- You would be obtaining an FCF yield of 3.3% based on the same stipulations.

- Therefore, I do not believe LIVN is undervalued, and is trading above the estimate of fair value in this case. This does not support a buy rating.

Subsequently, I remain neutral on LIVN's equity stock based on these factors of valuation.

Figure 8. LIVN valuation estimates

Data: Author

Discussion

Based on the culmination of factors discussed in this report, my stance remains neutral on LIVN as an investment grade company for the long-term. There are certainly positive developments in its epilepsy business, coupled with the evidenced demand hikes in its product offerings. The talk on margin decompression is, pardon the pun, marginal in my opinion, given the company's reliance on adjusted numbers in its reporting.

Then we move to the valuation calculus. I just can't get to LIVN's current market value with my modelling, even in the upside case. I've got the company at ~$40–$57 per share, using a firm 12% hurdle rate in all discounting. Further, I made plenty of adjustments for R&D in this analysis, but you've got to also remember why R&D was chosen to be expensed on the income statement in the first place, all the way back in the 70's—because there is an uncertainty element, and, the length of time of conversion. So whilst I do capitalize the R&D investment here, it's worthwhile remembering the profits generated on this may not be realized for many, many years to come. Net-net, reiterate hold.

Appendix 1. LIVN forward estimates [note: all figures are presented in a rolling TTM format].

{kind=link}

For further details see:

LivaNova: Struggling To Eye Value At Current Multiples, Reiterate Hold