LCHTF - LiveChat Software: An Undiscovered Gem

2023-04-11 14:45:22 ET

Summary

- LiveChat Software is highly profitable, with a 55% profit margin.

- Revenue and income have grown at annualised rate of ~20% over the last 5 years, with no signs of slowing.

- Currently trading at ~24x earnings and ~13x sales, below its long-term average.

- Based in Poland, this company has little coverage which provides an exciting opportunity.

Growth, profitability, prospects - LiveChat Software ( LCHTF ) has it all, but without the hefty price tag. Owing partly to its listing location and lack of coverage, this extremely profitable company which has seen annual growth compound in excess of 20% is trading at a remarkably reasonable valuation. As such, I view LiveChat Software as somewhat of an undiscovered gem, with a major catalyst in the form of Artificial Intelligence ready to bring the company into the mainstream focus.

Business Summary

LiveChat Software is a developer and provider of software which allows businesses to communicate with visitors to their website in real-time - you will likely have come across those pop-up boxes on websites offering a live text message-style conversation with a customer service representative. Indeed, LiveChat counts the likes of MacDonalds, PayPal and Adobe as clients, so if you've ever visited the websites of these companies you may have seen their software in action.

LiveChat Software in action (Company Website)

{kind=link}

LiveChat then offers businesses a suite of supplementary tools to help manage their customer interactions, providing data analytics, chat transcripts etc. to allow them to hone their website experience. Their flagship software 'LiveChat', as described above, accounts for the vast majority of sales (~92% as of the most recent earnings report ). Alongside this, they offer two other services: a chatbot builder (~6%) which allows businesses to create an automated bot to offer customers support at all hours, and help desk software (~2%) which allows businesses to manage customer support requests.

LiveChat Software operates a subscription model with prices starting at $20 per agent per month for their most basic tier aimed at small businesses, rising up to $59 per agent per month and above for their most advanced offering which is aimed towards larger enterprises. It should be noted that LiveChat Software does not provide customer support agents, rather, the software is designed to be integrated into a business' pre-existing customer support framework, allowing the business' own customer support agents to communicate with visitors to their website. Hence, a small business might only require access for 1 agent while a large corporation might benefit from a subscription for multiple agents.

Their products are primarily targeted towards small and medium-sized enterprises (SMEs), think the small business owner to whom personal contact is an important way to engage customers. The software can be accessed by a business online from any phone or computer, meaning an operator can answer online customer queries while out and about.

The company is headquartered in Poland with its primary listing on the Warsaw stock exchange under the ticker LVC. However, this is very much a global business with revenues primarily from the United States (~35%) and the United Kingdom (~10%). In fact, only a very small portion of revenue comes from Poland - 1.4%. Poland is a country which I think is often overlooked, but it is in fact the world's 21st-biggest economy , larger than the likes of Ireland, Israel and Norway. The company seems to have minimal analyst coverage outside of its home country. Just take Seeking Alpha as an example, with no coverage in the last 18 months. While of course, this is likely mainly due to the stock's small-cap status, I do view LiveChat Software as somewhat of an undiscovered gem.

The Bull Case

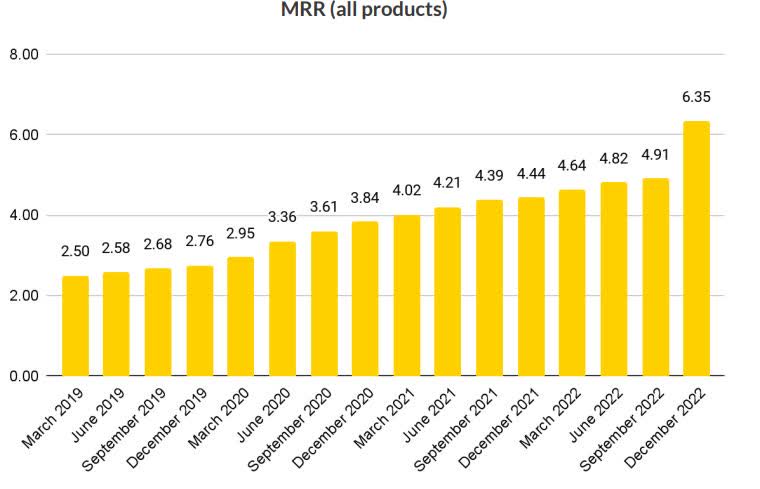

LiveChat Software has thus far shown a strong growth story, revenue has increased at a CAGR of ~20% over the past 5 years with net income growing at the same rate. A commonly used metric for business with a subscription model is monthly recurring revenue (MRR), which is a good indicator of the stability of the business - they report this figure in USD since the majority of sales are made in the dollar - in the most recent quarter ending December 31st 2022, it was $6.35m (27.5m PLN), and has been steadily growing quarter on quarter as seen below. The jump in the most recent figure can be explained due to price increases. If we exclude the most recent quarter, MRR has compounded at an annualised rate of about 21%.

{kind=link}

Company accounts

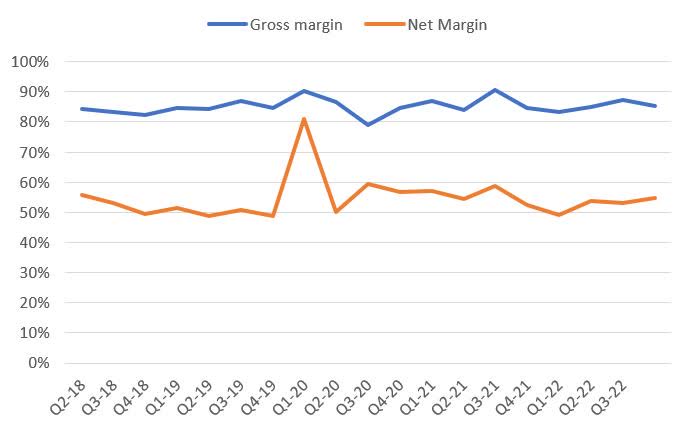

Additionally, LiveChat Software is a very profitable company. As of the most recent filing, gross/net margins were 85.4%/54.9% respectively, and have historically hovered around that region (this is best-in-class). As a result of the high margins and low capital requirements, this business generates cash very well. Free cash flow generated in the 12 months ending Dec 31st 2022 was 130m PLN ($30m) over profits of 153m PLN ($36m) and revenues of 289m PLN ($68m) - that's a margin of 45%, which is excellent for a company still in its growth phase.

{kind=link}

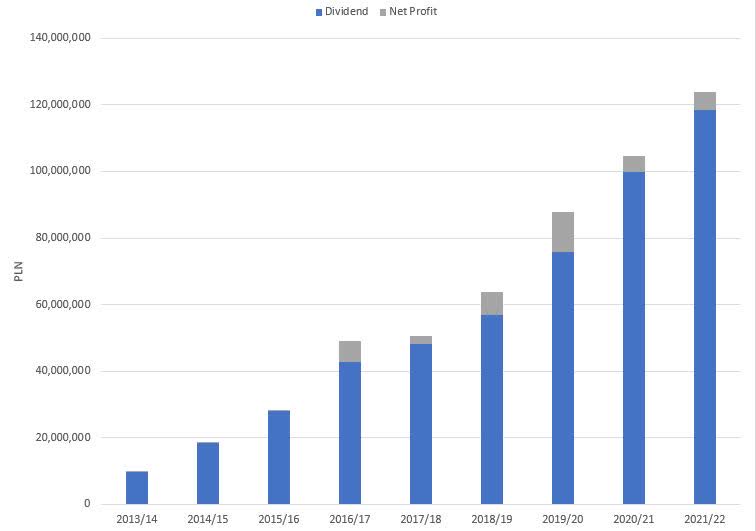

Management has stated that it will return any excess cash to shareholders, and has certainly kept its word in this regard; the dividend payout ratio has been consistently in the high 90s - 96% in FY 21/22. Dividends have thus been compounding at the same rate as net income at about ~20% per year over the last 5 years and the current dividend yield is about 3.3% . Owing to the extremely high payout ratio, one can't expect to necessarily maintain/exceed the level of the current dividend. Future dividend amounts are directly correlated with earnings and are thus susceptible to major fluctuations.

{kind=link}

The company is very financially secure. As of Dec 31st, they had no debt and a sufficient 91m PLN ($21m) in cash.

LiveChat Software has demonstrated both consistent growth and high profitability, with no signs of slowing. The question now is whether it can maintain such results moving forward.

Strength of Offering

LiveChat Software operates in a very competitive market. There is a relatively low barrier to entry which means there are a number of companies offering similar products. The size of the live chat software market was estimated to be $794 million in 2021 - if we take LiveChat's revenue which was about $48m during that period, this amounts to ~6% market share. The same research estimates the size of the market to grow to about $1.6bn by 2030 at an 8.6% CAGR. While this sounds like a lot, the live chat software market counts for a very small percentage overall of the SaaS market - in 2021 the SaaS total market was valued at around $215 billion , making live chat software amount to less than 0.4% of the total SaaS market. The relative niche of this part of the market explains to some degree the reluctance of large players to enter the market.

Live chat software solutions in general seem to be popular with the end consumer. Anecdotally, live they have worked well for me, it is often more convenient than calling up and having to wait on hold to speak to someone, but you still get the quick answers you require from talking to a real person without having to wait 3 working days for an email response. A Salesforce survey conducted in 2022 found that 70% of service organisations used live chat solutions, and 42% of customers prefer to use live chat solutions, up 4 percentage points from 2020, whilst 'non-live' mediums such as email have seen significant reductions in popularity since 2020 (although email was still more popular with 57% customers preferring email)

It should, however, be noted that there are some larger players in the market: Tawk.to (~22% market share), Facebook ( META ) (~18%), Zendesk (~8%) and Tidio (~8%) all offer competing services. The question is, what differentiates LiveChat from these competitors? And can LiveChat compete?

First of all, LiveChat's offering is very strong. It is consistently highly reviewed online and often ranks high on 'top lists' of live chat software providers, including recently being crowned TechRadar's best live chat software of 2023 citing its 'ease of use and great range of features'.

Many competitors, such as Tawk.to offer a freemium model, whereby the customer gets a very basic package for free, but then has to pay to remove branding and access the full suite of features. From my research, it seems that Tawk.to is easier to set up than LiveChat, but has far fewer features. For a small business that is perhaps unsure as to whether they need this software or not, I can fully understand why they might want to go for a free plan as is offered by Tawk.to. However, for more serious users, the free model is not really suitable so they would need to upgrade, which brings the cost to a level roughly comparable to that of LiveChat, but with fewer features and integrations. It is unclear what proportion of Tawk.to customers are paying customers vs free customers.

Further, LiveChat Software pride themselves on their strong customer service offering: customers can contact the company at any time 24 hours a day, 7 days a week, 365 days a year. They have a low customer acquisition cost, partly due to their high position in Google search results. While the name 'LiveChat Software' might not win any awards for creativity, it has proven to be a clever marketing strategy: If one googles 'live chat software' or similar (as one searching for such services would) LiveChat is consistently the top result. The name also really leaves no doubt as to the services they provide.

Further evidence of the quality of their service can be seen in the churn rate - around 3% which is below average for the SaaS industry. However, this might also be explained by the fact that the vast majority of customers are small businesses which are probably less likely to want to switch providers for marginal savings due to the effort required to switch.

Management

Management has significant skin in the game. Mariusz Ciep?y, long-time CEO and co-founder holds 13% of the stock, with a total of 41.7% of stock in the hands of management and founders, which gives me some confidence that management has their interests aligned with the shareholders. They have not issued new stock or stock options to company employees, which is a rarity in the tech sector, and as such, shareholders have not been diluted.

The Bear case

As mentioned earlier, this market is highly competitive and there is a very low barrier to entry. It wouldn't be all too difficult for a competitor to disrupt the market with a new offering. This is always going to be a looming threat to LiveChat Software. LiveChat Software needs to continue to invest in its product offering and to ensure that they are keeping up with its competitors. Capex in the 12 months ending December 2022 was 29m PLN (~10% of sales) and it has historically been around the 8% level, which is slightly below average for a software company. This can partly be explained by the strategy of the business to focus on developing and improving the already existing products rather than spending vast amounts on R&D to enter into new markets.

Offering me some comfort in this regard is the strength of their offering, the fruits of which can be seen in the low churn rate and laudatory reviews as mentioned earlier.

There are also alternatives to LiveChat which are cheaper. Take Tawk.to for example, the largest in the market. They work on a 'fremium' model, whereby the entry-level service is free but to access the more desirable features you have to pay a subscription. While Tawk.to has a significantly greater market share, it hasn't eroded away at LiveChat's numbers despite having been around since 2011 .

Concentration

Despite the emergence of the ChatBot and HelpDesk product lines, LiveChat Software is still very much reliant on its primary business section. Given the susceptibility to competition in the market, the concentration on this one product line does pose a material risk. On the other hand, as the old saying goes 'if it ain't broke, don't fix it'. While this isn't a good rule in general for businesses, particularly in today's ever-changing technological landscape, I do think there is some merit to a company sticking to what they do best. Does it make sense to take a stab in the dark on some completely unrelated business venture? Probably not.

Live Chat Software has demonstrated that they're good at what they do and the business model is clearly successful as it is. While there is significant concentration risk, I think I can make myself comfortable with this due to all the positives. Further, while currently immaterial in the grand scheme of things, the HelpDesk and ChatBot product lines, are growing and I see particular opportunities in the ChatBot segment with the recent emergence of AI technology (more on this later).

Slow in Growth

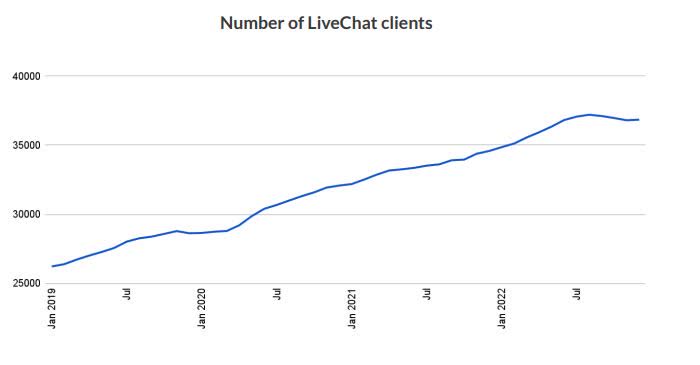

As can be seen from the below chart, user numbers have risen steadily over the last three years, but around July 2022 numbers began to plateau - this can be explained due to price increases which prompted existing customers to re-evaluate their subscriptions with LiveChat. We saw a similar thing happen towards the start of 2020 where price increases, combined with the oversized impact of the pandemic on small businesses (the primary customers of LiveChat) caused a temporary slight drop and then a plateau in paying users. I believe the situation to be the same in this case with the remarkably similar circumstances of the current tough economic climate disproportionately affecting smaller businesses.

{kind=link}

I believe that by now the impact of price increases - implemented from August 2022 - has probably settled and we can expect growth to continue. Indeed, monthly customer churn peaked at 4% (above the long-term average of 3%) in November 2022. It has since decreased below 4% but is not yet back at that 3% level as of December 2022. However, if we look at average revenue per user per month (ARPU) this has hugely spiked since the price increases were implemented, more than offsetting the slowdown in the growth of their client base.

Company accounts

The ChatGPT Question

The artificial intelligence ((AI)) language model Chat GPT has been taking the internet by storm recently, prompting a great discussion about the future of AI and where humans might fit in. Although powerful AIs have been around for a while now, this easy-to-use AI interface has been incredibly popular due to its uncanny ability to have deep human-like conversations on just about any topic. While this might naively seem like an existential threat to LiveChat Software, I propose for a number of reasons that it isn't, rather I think it could be good for business.

First of all, chatbots at the current time account for a very small portion of revenues (~6%) as mentioned earlier, the primary offering is software which only provides the interface between the customer and the customer service agent. Even if a business had a license to use the Chat GPT language model, it would still need a way to integrate the platform into its website, which is where LiveChat comes in.

Further, the majority of customers are SMEs which are more likely to value the personal touch when it comes to customer interactions over often sterile automated solutions. Even for a large company like McDonald's, I think it's likely that there will always be some human element to customer interaction, even if it is in a reduced capacity. Live chat is often preferred by businesses over phone communication due to greater efficiency (an agent can handle multiple conversations at a time).

In fact, hidden away in the most recent quarterly report, it was mentioned that in February of this year, the company signed a Data Processing Agreement with OpenAI (the company behind ChatGPT) allowing for the commercial use of OpenAI's technology in LiveChat's products. This technology is currently being tested and introduced to a number of their products.

Beyond this matter-of-fact statement, the company has been rather quiet on the topic, not issuing a press release, or expressing any views really on what impact the emergence of AI such as Chat GPT will have on the business. I did reach out to their Investor Relations team for clarity on the matter, but they just referred me to their website which was not very helpful. In any case, the Market seems to agree that ChatGPT certainly isn't a bad thing. In fact, the stock is up ~30% since ChatGPT's initial release in December of last year, a significant increase. While correlation does not imply causation, I think this demonstrates at the very least that the market doesn't see a significant risk here, and I agree.

I ultimately believe that AI technologies are a very exciting opportunity for LiveChat Software. If they can position themselves in the obvious way, as a means for businesses to integrate technologies such as ChatGPT into their websites, it could be very good news for LiveChat Software.

Latest Results

On 28th February 2023, results for the quarter ending 31st December 2022 were published , and they look strong. Revenue for the quarter was up 15% QoQ at 86m PLN ($20m) with a gross profit of 73m PLN ($17m) (+13% QoQ) and a net profit of 47m PLN ($11m) (+19% QoQ). Monthly recurring revenue (MRR) was at $6.35m as of December end, up 29% from $4.91m in September. It should be noted that this increase was mainly due to price raises, in fact, the number of customers actually stayed flat/slightly dipped quarter on quarter. The average revenue per user per month was $160.70 vs $121.20 at the end of Sep (+33%). They ended the quarter with a strong cash position of 91m PLN ($21m) and no debt. Free cash flow for the quarter was 50m PLN ($11.7m).

Valuation

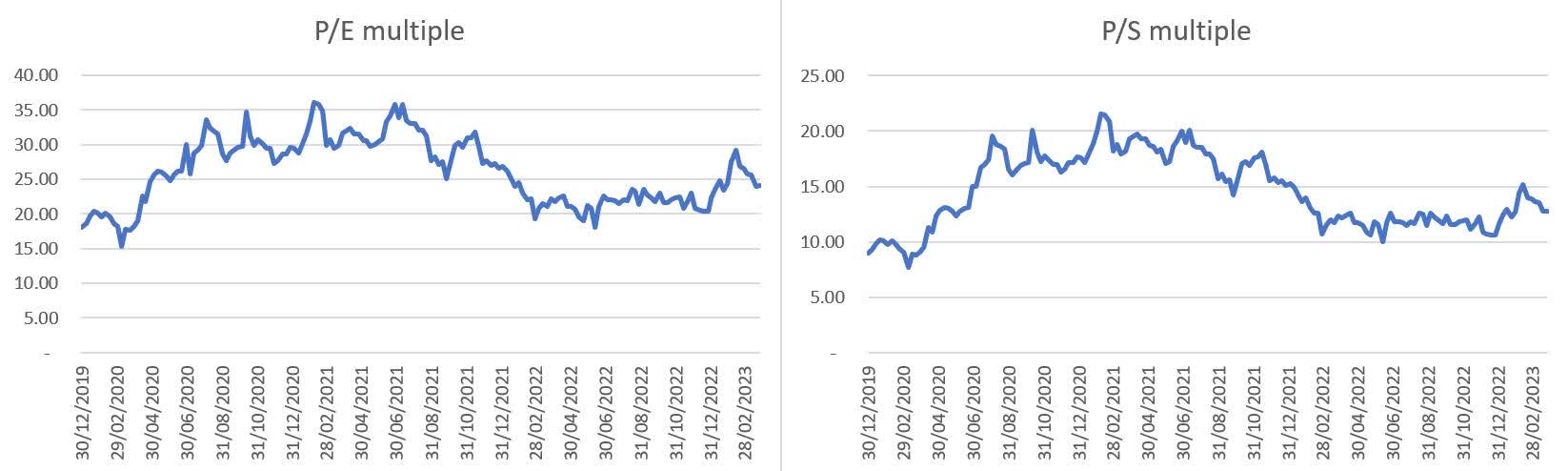

LiveChat Software is currently trading at ~24x TTM earnings which although above the 1yr multiple average of ~22.5x is below the 3yr average of ~26.7x. Perhaps a better indication of relative value in a sector where so many companies are unprofitable is the price to sales multiple, which is ~12.8x, slightly above the 1yr average of 12.1x, but below the 3yr average of 15x.

{kind=link}

Given that the majority of peers are unprofitable, let alone profitable to the level of LiveChat Software, it is unwise to try and precisely compare valuations. Additionally, due to the relative niche of the live chat sector, there aren't really any directly comparable public companies, except for competitor Zendesk which was acquired by private equity in November last year. The business was not profitable, and P/S multiple on sale was ~6.5x, but had historically hovered above 10x.

Some larger SaaS vendors include Adobe ( ADBE )(~10x sales, ~27x earnings, 26% profit margin), Salesforce ( CRM ): (~6x sales, ~38x earnings, NI margin 0.6%), ServiceNow ( NOW ) (~12.9x sales, ~61x earnings, NI margin 4.5%).

Given the superior growth prospects and profitability of LiveChat, a valuation premium is definitely warranted. Such a highly profitable business in an industry where profits are notoriously hard to come by, at such a valuation is an appealing proposition. Given that LiveChat is trading at a sales multiple roughly comparable to much less profitable peers, a significantly lower earnings multiple, as well as below its own long-term average, I believe there is an opportunity here. Buy.

For further details see:

LiveChat Software: An Undiscovered Gem