LTHM - Livent: Wonderful Company Fairly Valued

2023-12-15 06:26:21 ET

Summary

- Livent Corporation is a lithium products company that trades below its IPO price and has exposure to the promising lithium industry.

- The company's financial performance has been impacted in recent quarters by cyclicality, but it continues to improve its strategic positioning in the industry.

- LTHM's merger with Allkem is expected to bring synergies and diversification of assets, making it one of the world's largest lithium companies.

- The stock is attractively valued.

Investment thesis

Livent Corporation ( LTHM ) grabbed my attention because this company, with solid exposure to the promising lithium industry, trades below its IPO price and to the lower edge of its 52-week range. The stock price weakness is explained by two weak quarterly earnings in a row, but the financial performance pullback is due to cyclicality and not secular factors. From the fundamental and longer-term perspective, the company continues improving its strategic positioning in the promising lithium industry. I am very optimistic about Livent's merger with Allkem due to the expected synergies and the diversification of the assets the combined business will achieve. My valuation analysis suggests the stock is fairly valued with a moderate upside potential. All in all, I assign LTHM with a "Strong Buy" rating.

Company information

Livent is a fully integrated lithium products company. LTHM's primary products include battery-grade lithium hydroxide, lithium carbonate, butyllithium, and high-purity lithium metal. According to the latest 10-K report , the company has six manufacturing facilities in five countries.

The company's fiscal year ends on December 31 with a sole reportable segment. In FY 2022, more than half of LTHM's sales were generated from lithium hydroxide.

{kind=link}

Financials

Even though Livent's history goes back to the 1940s , the company went public relatively recently. The company went public in 2018 , with the IPO priced at $17 per share. That said, we have a relatively short history of publicly available financial information, but it seems enough to identify key trends. The good part is that the company's revenue more than tripled over the last seven years, representing a 20.6% CAGR. On the other hand, profitability metrics were very volatile. The business is capital-intensive, and that is the main reason why the company generated negative free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] in recent years.

{kind=link}

Despite having a negative FCF margin, I think the company is financially well-positioned to address the necessity to continue investing heavily in production expansion. As of the latest reporting date the company had $113 million in outstanding cash with strong liquidity ratios. The net debt might look high, but the leverage ratio is insignificant, and the major part of the debt is long-term. I also want to highlight that according to the latest 10-Q report , the debt is represented by convertible senior notes due in 2025, which possibly can be converted into equity, meaning that the company might become debt-free. It is also crucial to highlight that the company has an untapped $500 million revolving credit facility. That said, Livent's financial position is robust and positions the company well to continue investing heavily in growth.

Seeking Alpha

The latest quarterly earnings were released on October 31, when the company missed consensus estimates by a notable margin. Despite revenue declining YoY by 9%, the adjusted EPS expanded from $0.41 to $0.44. However, the EPS expansion was caused by non-operating income and the operating margin shrank YoY by three percentage points.

Seeking Alpha

Revenue decrease is explained by lower lithium carbonate pricing and lower butyllithium pricing and volumes, partially offset by an increase in lithium carbonate volumes and higher lithium hydroxide pricing. That said, the negative surprise and revenue decline is explained by cyclicality and not by unfavorable factors.

The earnings for the upcoming quarter are scheduled for release on February 16, 2024. Consensus estimates project quarterly revenue at $208 million, indicating approximately a 5% YoY decline. The adjusted EPS is expected to follow the top line and shrink YoY from $0.40 to $0.36.

Seeking Alpha

While it is apparent that the company currently faces macro headwinds, I think that the company's fortress financial position means the company is resilient enough to weather this temporary storm. What I want to focus on is the company's strong positioning and its solid strategic moves to absorb positive secular trends for the lithium industry.

Livent's latest earnings presentation

{kind=link}

The most important move is apparently the merger with Allkem, which will make the combined business one of the world's largest lithium companies. Apart from getting benefits from complimentary assets, synergies are also expected from the cost side, with operating synergies of approximately $125 million per annum [pre-tax] and one-time capital savings of approximately US$200 million. The merger is expected to be closed by the end of 2023, and all necessary regulatory approvals are already granted .

To conclude, cyclical issues explain the recent softness in financial performance with weakening EV demand , but not secular trends. On the contrary, from the secular perspective, the shift to electric vehicles is a massive tailwind for Livent since the trend looks unstoppable. For example, the European Union approved the ban on internal combustion engine [ICE] vehicle sales starting from 2035. The largest global economies spend massive amounts of taxpayers' money to create incentives for people to buy EVs instead of ICE, which supports the strength of this secular shift, which is favorable for Livent.

Valuation

LTHM declined in price by 16% year-to-date, significantly underperforming the broader U.S. stock market. Seeking Alpha Quant assigns the stock with a high "A-" valuation grade because ratios are substantially lower than the sector median and LTHM's historical averages. That said, the stock is notably undervalued from the perspective of valuation ratios.

{kind=link}

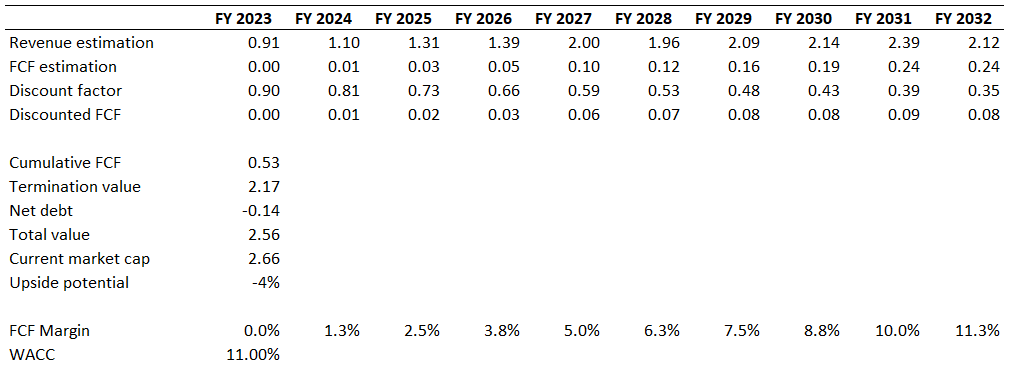

I want to proceed with the discounted cash flow [DCF] simulation. I use an 11% WACC suggested by Gurufocus . I use revenue consensus estimates for the next decade, projecting a 10% CAGR. I expect a zero FCF margin for my base year with a 125 basis points yearly expansion.

{kind=link}

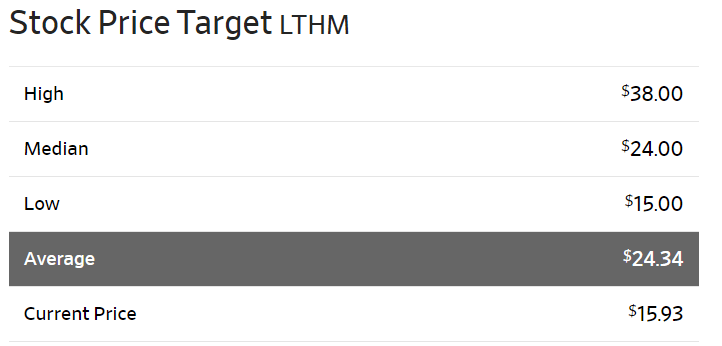

According to my DCF simulation, the business's fair value is $2.56 billion, which is around $100 million lower than the current market cap. That said, the stock is fairly valued from the perspective of discounted cash flow. I think that a well-positioned company in a promising industry deserves a premium, but defining the extent of the premium is tricky and subjective. According to WSJ , the average consensus target price is $24.34, which represents a 52% upside potential.

{kind=link}

Risks to consider

As we have seen in the recent stock performance, it is susceptible to broader economic conditions. As a commodity, lithium's pricing depends on the supply-demand equation, and the demand is driven by the broader economic strength. Promising future prospects for lithium are linked with aggressive expectations for electric vehicle [EVs] adoption and signs of softening in the broader global economy, which significantly undermines lithium demand expectations. That said, potential LTHM investors should be ready to stomach substantial volatility.

While the merger with Allkem will likely open several synergies for the combined entity, success is not guaranteed, and a lot will depend on the ability to manage all challenges inherent to integrating two large companies. Potential risks associated with the merger include cultural differences between the two organizations, which could create obstacles to a seamless integration process. Furthermore, the consolidation of operational systems and processes may pose technical challenges.

Bottom line

To conclude, LTHM is a "Strong Buy". The stock is attractively valued, and the company's fundamentals are improving. Livent is financially strong enough to weather the current cyclical headwinds, and the company continues to improve its strategic positioning to absorb massive secular tailwinds behind its back.

For further details see:

Livent: Wonderful Company Fairly Valued