LPSN - LivePerson: Avoid For Now

2023-07-10 10:54:20 ET

Summary

- I maintain my neutral rating for LPSN.

- I believe that cloud platforms like Salesforce, Oracle, and Five9 have a better position in conversational AI, and may take LPSN's market share.

- LPSN appears overvalued, in my opinion. I set a target price of ~$3.4 per share for FY 2023.

LivePerson (LPSN) is a company developing an enterprise cloud-based platform that enables brands to embed AI-powered conversational technology across different functions, mostly customer service and commerce.

I first covered LPSN almost three years ago , where I rated the stock neutral given the company’s weak competitive positioning in AI. Performance has generally been lackluster since then. Today, LPSN is trading between $4.2 - $4.6 range, down ~$85% from my initial coverage price.

I maintain my neutral rating for the stock. Fundamentals remain weak, and despite the growing trend of conversational AI, I continue to believe that there are companies with better positioning than LPSN to capture the opportunity.

Risk

LPSN presents various potential downside risks, which stem from its relatively weak fundamentals - revenue growth, cash flow generation, and profitability all have been volatile in recent times. LPSN is also exposed to a considerable amount of debt. The debt-to-equity ratio stood at 7.8x as of Q1.

{kind=link}

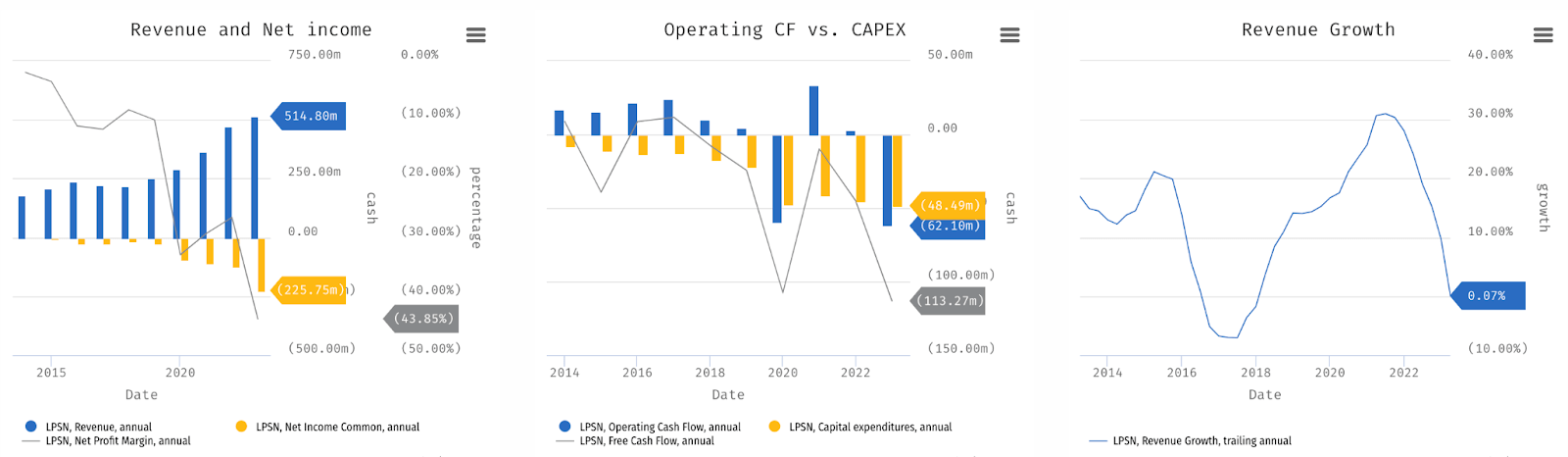

Revenue growth has declined since 2020 when LPSN benefitted from the higher usage revenue due to the increased demand for its AI-powered contact center solution due to COVID-19. In Q1, growth declined by over 17% as the COVID-19 tailwind eased off . Over the same period, net loss margin continued to widen from 26% to 43% while cash flow generation has been choppy. In Q1, operating cash flow / OCF also declined quite significantly to -$62 million.

While LPSN reiterated its intention to focus on profitable growth in Q1, there are good reasons why LPSN may see challenges there in Q2 and beyond. First, I remain doubtful about the management’s overall execution ability. This was best illustrated by LPSN’s questionable entries into non-core businesses such as Kasamba, which it ended up exiting in Q1, and Wild Health . Overall, I think that these actions should be a red flag for investors.

{kind=link}

Another red flag is LPSN’s continuous involvement in litigation over the past few years, which has been relatively costly. In Q1, LPSN incurred over $9.5 million in litigation costs. The amount paid in Q1 was also surprisingly high, since the figure was almost as much as the litigation cost incurred for the whole FY 2022 ($11 million ).

{kind=link}

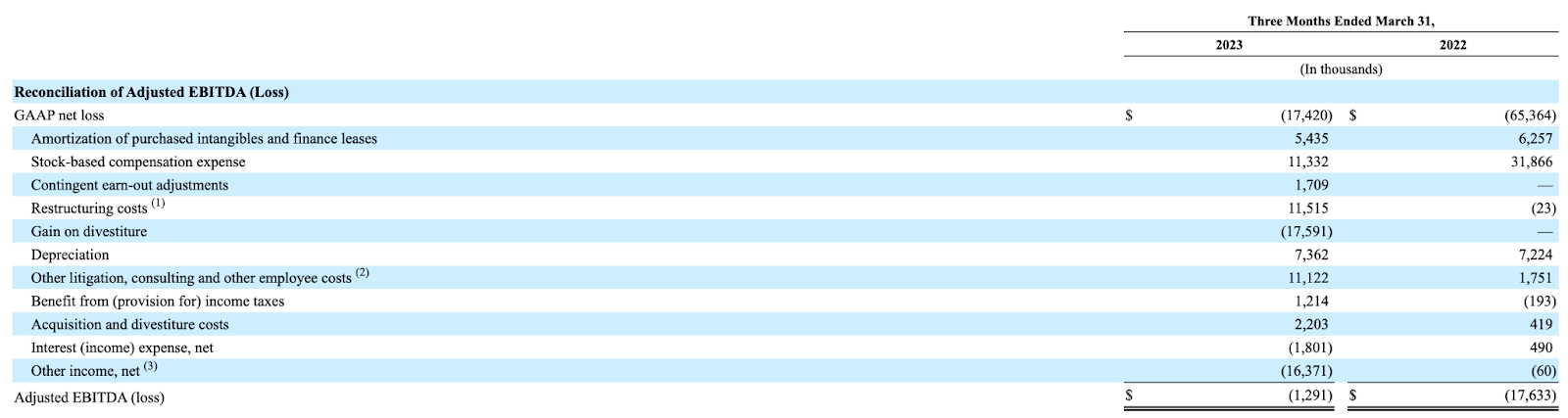

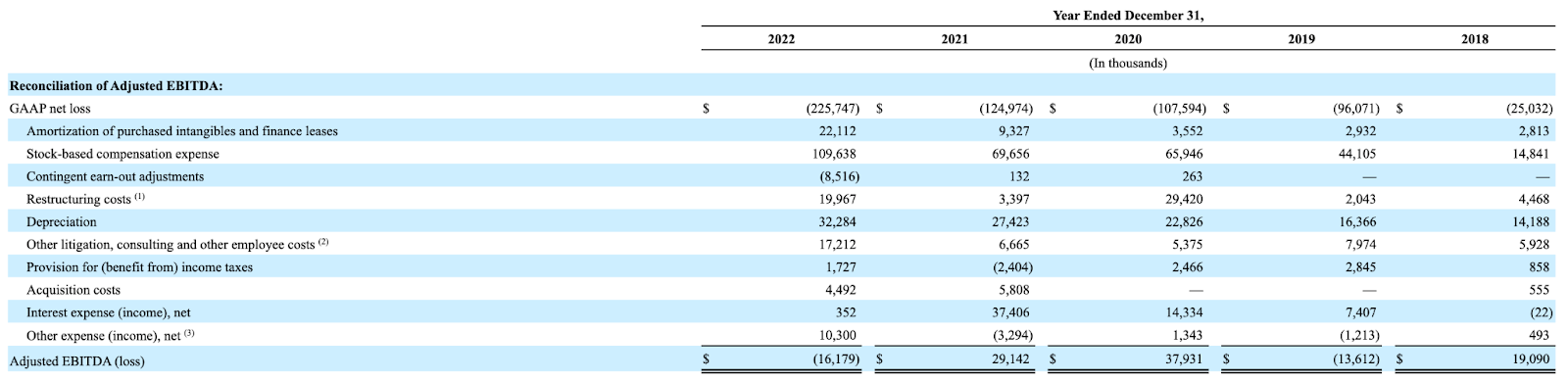

Aside from litigation costs, I also continue to notice how the supposedly non-recurring expenses, such as interest expenses and restructuring costs, have been putting pressure on LPSN’s profitability outlook every single year. Excluding these add-backs, LPSN would have seen negative adjusted EBITDA every year for the last four years. Looking at the situation over the past few years, I feel that LPSN will likely to continue incurring these costs at least until the end of FY 2023.

Secondly, despite the growing trend in conversational AI, I continue to believe that LPSN may continue to face tough competition to gain market share from cloud-based platforms with better go-to-market positioning. My view is that while AI language models as developed by Open AI will definitely not be a commodity, AI technology will eventually be a built-in feature offered by cloud-based software providers addressing the pain point in conversational commerce and CRM / customer relationship management, such as Salesforce (CRM), Oracle (ORCL), or Five9 (FIVN). Given the existing enterprise client base and established SI / System Integrator channel partner ecosystem, I believe that these players will have the upper hand in driving enterprise conversational AI adoption.

Catalyst

I think that the catalyst remains minimal. Given the full-year negative growth projection in FY 2023, LPSN’s best move is to continue winning new deals and beat its guidance on quarterly basis. Nonetheless, I believe that the share price may continue to stay at the current level for some time, and may only get a chance to trend upward if there is an indication of surprising outperformance followed by a guidance raise.

Valuation / Pricing

My target price for LPSN is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 target price model:

-

Bull scenario (70% probability) assumptions - LPSN to achieve the top end of its guidance and end FY 2023 with $401 million, reflecting a growth decline of ~22%.

-

Bear scenario (30% probability) assumptions - LPSN to see further setbacks and end FY 2023 with ~$360 million of revenue, reflecting a growth decline of ~30%.

I assigned a P/S of 0.67x, where LPSN is currently trading, across both scenarios. This may lean towards bullish, since I would imagine that P/S may actually contract further if LPSN misses its guidance, as per my assumption in bear scenario. I also assumed a 70% probability for LPSN to achieve its guidance. On the flip side, I probably have also offset those effects by assuming a relatively aggressive 30% growth decline for the bear case.

author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of ~$3.4 per share. With LPSN trading closer to ~$4 per share recently, the stock appears overvalued. I would suggest that the stock may possibly see a near-term correction where it falls closer to the target price.

Conclusion

LPSN has weak fundamentals, including fluctuating revenue growth, cash flow generation, and profitability. Catalysts remain minimal. Considering the projected negative growth, I have set a target price of approximately $3.4 per share for FY 2023. Currently, LPSN's stock is trading at around $4 per share, indicating that it may be overvalued. As a result, there is a possibility of a correction in which the stock price could decline toward the target price. Given these factors, I maintain a neutral stance on the stock.

For further details see:

LivePerson: Avoid For Now