LPSN - LivePerson: Losing Momentum - Tough Year Ahead

Summary

- The company is showing signs of slowing down, with revenue in the third quarter down from the prior two quarters; Q4 guidance suggests that's going to continue.

- While new logo wins were down 22 percent, the company has shown consistent improvement in ARPU.

- Costs and expenses continue to climb, and the company will need to execute on its strategy to lower costs while improving margins and EBITDA.

The share price of LivePerson, Inc. ( LPSN ) has been under enormous pressure over the last couple of years, falling from a 2-year high of approximately $72.00 per share on February 15, 2021, to a 52-week low of $7.96 on October 14, 2022.

Since then, it has been trading volatile, where it appears to have found a bottom of about $9.20 per share, and a ceiling of approximately $13.00 per share, based upon a double bottom and a double top at those levels. It has traded below and above those levels but hasn't sustainably broken either way since its 52-week low.

{kind=link}

I think that's going to change because LivePerson, Inc. continues to hemorrhage money, even as it's starting to show signs of revenue slowing down over the last three quarters, and based upon guidance, is likely to continue in that direction.

While new logo wins were down 22 percent in the third quarter, the company has managed to book higher value from the business in enterprise it has been winning, primarily because they are frontloaded in the initial stage of doing business.

In this article we'll look at some of the numbers from its latest earnings report and where things appear to be trending, the importance for the company to execute on its strategy to cut costs, and why it's imperative that it consistently wins new logos in enterprise.

Some of the numbers

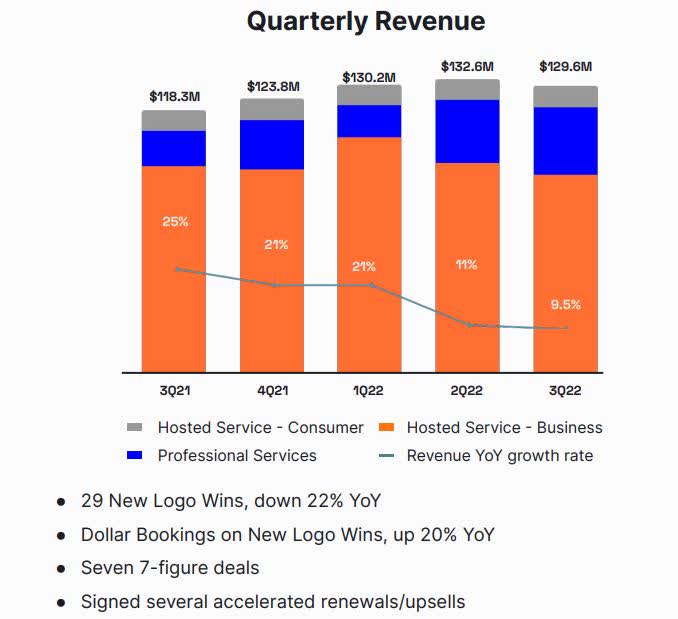

Revenue in the third quarter of 2022 was $129.6 million, up 9.5 percent the $118.3 million in revenue generated in the third quarter of 2021, but slightly down from revenue in the first quarter of 2022, where revenue was $130.2 million, and the second quarter of 2022, where revenue was $132.6 million.

{kind=link}

For the first nine months of 2022 revenue was $392 million, compared to revenue of $346 million in the first nine months of 2021.

Revenue from Hosted Service has been dropping in 2022, while revenue from Professional Services over the last couple of quarters has been increasing.

One positive from the third quarter was the ongoing improvement in average revenue per user (ARPU), which climbed to $675,000, up from $570,000 in the third quarter of 2021.

{kind=link}

Total costs and expenses continued to climb, coming in at $178 million in the third quarter of 2022, resulting in loss from operations of $48.5 million. Total costs and expenses in the third quarter of 2021 were $139 million, producing a loss of $20.8 million in that time period.

Total costs and expenses in the first nine months of 2022 were $575 million, producing a loss from operations of $183 million, compared to total costs and expenses of $394 million in the first nine months of 2021, result in loss from operations of $48 million.

Adjusted EBITDA in the reporting period was $9.1 million, beating prior guidance of $4.8 million. Non-GAAP gross margins in the third quarter were 74 percent, which were on the top of its guidance range, and was attributed to cutting costs and targeting business that had scalable high margin revenue potential.

Management said that restructuring in the third quarter should result in a reduction of its expense run rate compared to the first half of 2022, moving the company toward its goal of reaching double-digit adjusted EBITDA and positive free cash flow in 2023.

Based upon the numbers below, it has a lot of work to do to achieve those results, as net losses in the third quarter and for the first nine months of 2022 continue to grow.

Net loss in the third quarter of 2022 was $(43.2) million, or $(0.56) per share, compared to a net loss of $(33) million, or $(0.47) per share in the third quarter of 2021.

Net loss in the first nine months of 2022 were $(184) million, or $(2.39) per share, compared to a net loss in the first nine months of 2021 of $(75) million, or $(1.09) per share.

The company guided for adjusted EBITDA in the fourth quarter to be in a range of $14.9 million to $24 million, far above full-year 2022 guidance of $1.0 million to $10.0 million. Adjusted EBITDA margin was guided to be in a range of 12 percent to 19 percent, also significantly above full-year 2022 guidance of 0 percent to 2 percent.

Cash and cash equivalents at the end of the third quarter of 2022 was $393 million, compared to cash and cash equivalents of $521.8 million at the end of calendar 2021.

Implication of new logo wins being down

In the third quarter, the company had 29 new logo wins, down 22 percent year-over-year. At the same time, the dollar bookings from the new logo wins jumped 20 percent year-over-year.

When CEO Rob LoCascio was asked about this in the Q&A portion of the earnings call, he said the third quarter had some great new logos, with some of them being bigger deals that in part came from them being optimized to deal size by the sales representative.

Much of the improvement in dollar bookings came from targeting the enterprise market, but LoCascio said that it changes on a quarterly basis, adding that it's not a trend. Even though the booking value increased in the quarter, management was quick to point out it wants to get as many new logos as it can in order to drive company value in the future. With the company saying its enterprise customers have been shifting from 30 percent to 50 percent of their contact volume to LPSN, it's vital to win new logos in order to take full advantage of that trend.

New logos in enterprise initially generates higher booking value, which is why it was up even when new logos were down in the quarter, but over the long term, it's the lifetime value of the enterprise logos that will determine the performance of the company.

So, while increased booking value is important because it reflects new logo wins of higher, short-term value, a decline in new logo wins takes away the future growth momentum in the company in revenue and margins. In other words, it's not a good thing to see the momentum in new logo wins slowing down. It can be covered over by new enterprise wins generating higher booking value in the initial stage, which will give a temporary revenue boost. But the major thing for investors to watch is how many new logos are being won, because it reflects the long-term growth potential of the company.

Ideally what we want to be looking for is an increase in new logos wins in enterprise, which will be a significant, short-term tailwind, and the company successfully upselling those customers over the long term. This is what the company was primarily referring to when it talked about cutting costs while targeting business that had scalable high margin revenue potential. It's the scalability potential that is lost if the new logos wins continue to fall.

I believe this is confirmed in the average revenue per user continuing to climb. But if the number of new logo wins is dropping, there is no ARPU to grow if you don't get the initial business. That's a major challenge the company faces going forward.

Conclusion

At this time, the performance of LPSN is mixed at best. It is showing signs of reducing costs, which it must do in order to move toward profitability. Even so, losses from operations continue to soar, and a lot of things will have to go right for the company to reverse direction in regard to ongoing losses.

I see the key to that happening to be in regard to new logo wins in enterprise, which has both significant short-term and long-term potential for the company, if it can get more consistent in wins and successfully upsell over time, which it has proven it can do if it can get its foot in the door.

At this time, I believe the company could go either way over the next year or so, as there are a lot of questions that must be answered in reference to cutting costs, winning new logos, and what impact the macro-economic environment will have on the company.

I do believe it has a lot of future potential because AI use in customer contact is going to continue to increase. But with upper management pulling spending decisions further up the hierarchy, it's obvious there is a lot of prioritizations going on in relationship to spending because of the lack of visibility in the quarters ahead, and that will probably have a detrimental impact on the performance of LPSN in 2023.

With the revenue numbers showing weakness on a quarterly basis, and new logo wins in decline, I think the company is going to struggle to achieve its revenue and earnings goals in 2023.

At best I think the company will trade sideways for now, but if revenue and earnings fail to meet expectations, it's going to take a much further dive and probably remain there until its performance improves.

I think the company has a far higher percentage chance of underperforming than overperforming in 2023.

For further details see:

LivePerson: Losing Momentum - Tough Year Ahead