RAMP - LiveRamp's Fortunes Grow On Improving Execution (Rating Upgrade)

2023-11-20 15:52:46 ET

Summary

- LiveRamp Holdings, Inc. reported better-than-expected financial results for Q2 2024, with growing revenue and operating profits.

- The company provides identity resolution capabilities for online companies globally.

- The global market for identity resolution services is expected to reach $2.3 billion by the end of 2028.

- My outlook for LiveRamp Holdings is a Buy on improved sales execution and growing operating profit.

A Quick Take On LiveRamp

LiveRamp Holdings, Inc. ( RAMP ) reported its FQ2 2024 financial results on November 8, 2023, beating both revenue and consensus earnings estimates.

The firm provides identity resolution capabilities for online companies globally.

I previously wrote about RAMP with a Hold outlook.

RAMP has produced growing revenue as well as operating profits as a number of tailwinds have propelled the business opportunities forward.

My outlook is a cautious Buy at around $34.00 per share on growing operating income and improved sales execution.

LiveRamp Overview And Market

California-based LiveRamp Holdings, Inc. provides clients with audience identification and data tools for online marketing purposes.

The company is led by Chief Executive Office Scott Howe, who was previously president and CEO of marketing services company Acxiom.

The company’s primary offerings include:

-

Identity resolution

-

Data activation

-

Measurement

-

Data collaboration

-

Marketplace.

RAMP acquires customers via its direct sales teams as well as through partners and cloud provider channels.

According to a 2022 market research report by Business Research Insights, the global market for identity resolution services was an estimated $1.1 billion in 2021 and was forecast to reach $2.3 billion by the end of 2028.

As marketers lose access to some forms of data such as via "cookies" from major mobile platforms from Apple and Google, data from alternative sources is becoming more valuable.

Identity resolution software seeks to "overcome the challenges associated with data fragmentation and duplication."

Different industries are more or less reliant on third-party cookies for their online marketing efforts, with the financial services and travel industries reporting the greatest reliance on cookies.

The COVID-19 pandemic increased the demand for digital transformation efforts across many industries, pulling demand forward.

Major competitive vendors or other industry participants include:

-

Intent IQ

-

Saint-Gobain S.A Tapad

-

Amperity

-

Merkle

-

Zeta Global

-

Throtle

-

Xoriant Katch

-

Signal

-

Neustar

-

BounceX

-

NetOwl

-

Informatica

-

Infutor

-

Criteo.

LiveRamp’s Recent Financial Trends

Total revenue by quarter (blue columns) has grown year-over-year; Operating income by quarter (red line) has turned well into positive territory:

Seeking Alpha

Gross profit margin by quarter (green line) has turned slightly higher recently; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended lower in recent quarters, indicating increasing efficiencies in generating incremental revenue:

Seeking Alpha

Earnings per share (Diluted) have turned sharply higher recently:

Seeking Alpha

(All data in the above charts is GAAP.)

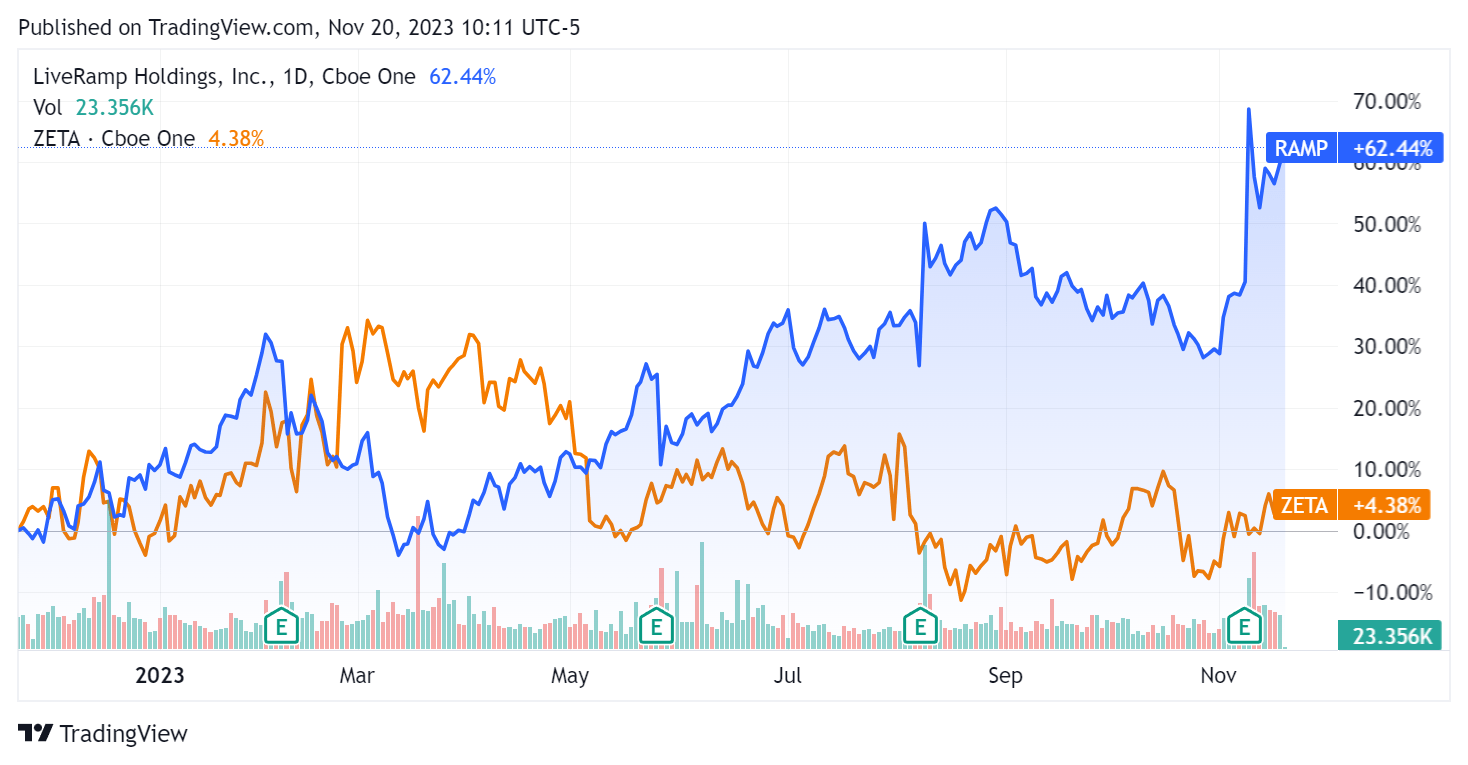

In the past 12 months, RAMP’s stock price has risen 62.44% vs. that of the Zeta Global Holdings Corp. ( ZETA ) rise of 4.38%:

{kind=link}

For balance sheet results, the firm ended the quarter with $524.1 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash flow was $113.2 million, during which capital expenditures were $0.5 million. The company paid $103.3 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For LiveRamp

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 2.8 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 3.6 |

| Revenue Growth Rate |

| 8.7% |

| Net Income Margin |

| -9.3% |

| EBITDA % |

| -1.3% |

| Market Capitalization |

| $2,190,000,000 |

| Enterprise Value |

| $1,710,000,000 |

| Operating Cash Flow |

| $107,890,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.89 |

| Forward EPS Estimate |

| $1.30 |

| Free Cash Flow Per Share |

| $1.72 |

| R&D / Revenue |

| 26.3% |

| SA Quant Score |

| Strong Buy - 4.77 |

(Source - Seeking Alpha.)

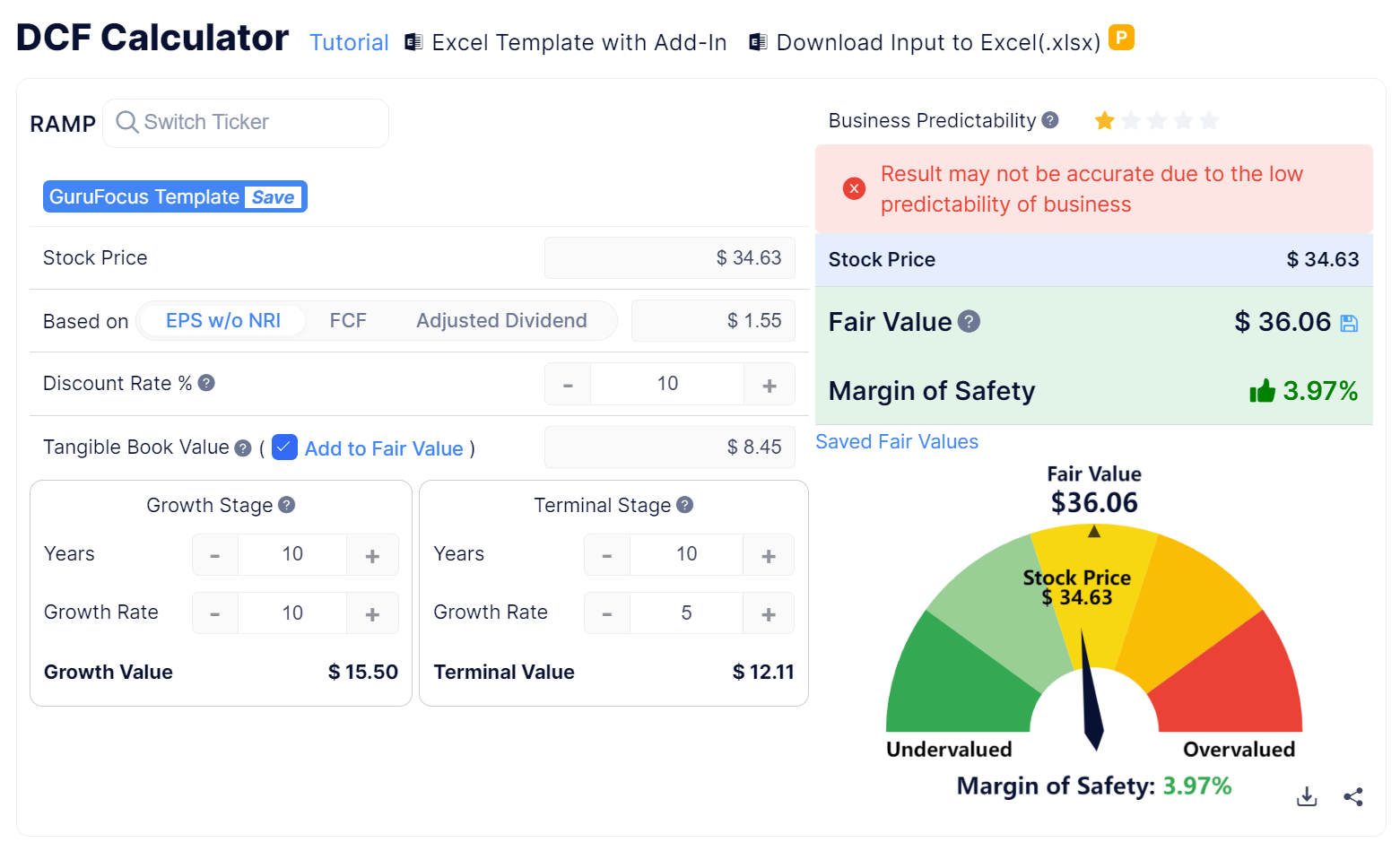

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

{kind=link}

Based on the DCF, the firm’s shares would be valued at approximately $36.06 versus the current price of $34.63, indicating they are potentially currently slightly undervalued.

RAMP’s most recent unadjusted Rule of 40 calculation was 17% as of FQ2 2024’s results, so the firm has recently performed better but needs further improvement, per the table below:

| Rule of 40 Performance (Unadjusted) |

| FQ4 2023 |

| FQ2 2024 |

| Revenue Growth % |

| 12.9% |

| 8.7% |

| Operating Margin |

| -10.2% |

| 9.3% |

| Total |

| 2.7% |

| 17.9% |

(Source - Seeking Alpha.)

Commentary On LiveRamp

In its last earnings call (Source - Seeking Alpha ), covering FQ2 2024’s results, management’s prepared remarks highlighted exceeding its previous guidance for both revenue and operating income.

The quarter also produced the "highest new log bookings…in dollar terms in two years," so the firm is seeing improving leading indicators in this regard.

Management is seeking to reestablish double-digit revenue growth and credit its sales force attrition fully normalizing with ample capacity to grow the business further.

Notably, the company believes that embedding its products within cloud computing partners, along with the trends of the continued growth of retail media networks and CTV, will fuel revenue growth ahead.

In the earnings call, I tracked the frequency of various keywords and terms used by management and analysts on the call.

Seeking Alpha

Analysts asked leadership about customer strategy, sales execution efforts, and its connected TV [CTV] opportunity.

Management said it is focusing on larger, higher-value enterprise customers, which accounted for a decline in total customer count.

The firm has seen increased market demand across retail media, auto, travel and CTV partnerships, resulting in improved sales execution.

Leadership sees CTV business as a tailwind for years ahead as advertisers have been making a quiet shift toward CTV in recent years.

Total revenue for FQ2 2024 rose by 8.7% year-over-year, while gross profit increased by 3.4%.

The subscription net retention rate was 101%, or 3% higher sequentially due to "improved upsell and to a lesser extent reductions in contraction," which I presume to mean a reduction in churn.

Selling and G&A expenses as a percentage of revenue dropped by 6.1%, a positive signal indicating increasing efficiencies in this regard.

Operating income rose to $14.8 million versus a loss of nearly that amount in the prior year’s same quarter.

The company's financial position is quite strong, with ample liquidity, no debt and strong free cash flow.

RAMP’s Rule of 40 performance has been improving in recent quarters, mostly due to a turn to operating profit from a previous loss.

Looking ahead, full fiscal year 2024 revenue is expected to grow at 7.8% over fiscal 2023.

If achieved, this would represent a decline in revenue growth rate versus fiscal 2023’s growth rate of 16.5% over fiscal 2022.

In the past twelve months, the firm's EV/Sales valuation multiple has risen by nearly 64%, as the chart from Seeking Alpha shows below:

{kind=link}

So, while the company's stock price has produced an impressive runup, the question is whether it is still a good value at its current level.

With an EV/Revenue multiple of 2.8x, slightly undervalued DCF calculation and strong growth in operating profit, my outlook for LiveRamp Holdings, Inc. is a cautious Buy at around $34.00.

For further details see:

LiveRamp's Fortunes Grow On Improving Execution (Rating Upgrade)