GPC - LKQ Corporation Q4 Earnings Preview: Recent Weakness Does Not Detract From The Firm's Upside Potential

Summary

- LKQ Corporation recently hit a bump in the road, with sales, profits, and cash flows pulling back.

- Actual organic sales have risen, and the long-term outlook for the company should be fine.

- Compared to similar firms, it offers some upside potential and it looks reasonably appealing on an absolute basis.

If you are engaging in the purchase and sale of stock of individual companies, you would be very wise to keep a close eye on your investments. In particular, you should watch to see if the picture changes, either for better or worse. And from there, you should decide whether or not the company in question still makes for an appealing opportunity. One company that has shown a bit of weakness as of late that I previously rated a ‘buy’ is LKQ Corporation ( LKQ ). For those not familiar with the company, it focuses on the global distribution of vehicle products, components, and systems, that are often used in repair and maintenance activities for vehicles. A change in market conditions has resulted in a bit of weakness from a sales, profit, and cash flow perspective. However, this doesn't necessarily mean that investors should bail on the company just yet. Given how shares are priced, it is true that the stock is most certainly not a home-run candidate. But I would argue that it probably does offer a bit more upside from here.

Processing the pain

The last time I wrote an article about LKQ Corporation was back in early August of 2022. At that time, I was following up on the company and I lauded the performance it had achieved over the prior few months, with sales rising even as bottom line performance showed mixed results. I did think at that time that the easy money had already been made with the firm. But even with the appreciation it had experienced up to that point, I felt as though shares were cheap enough to warrant some additional upside. As a result, I kept it at the ‘buy’ rating I had it at previously, indicating that I felt as though shares should outperform the broader market for the foreseeable future. So far, this is exactly what transpired. While the S&P 500 is down 0.3% since the publication of that article, shares of LKQ Corporation have seen upside of 2.6%. While this may not seem all that significant, it is worth noting that, since I first wrote about the company, shares have seen upside of 16.2% compared to the 4.9% rise the broader market experienced.

{kind=link}

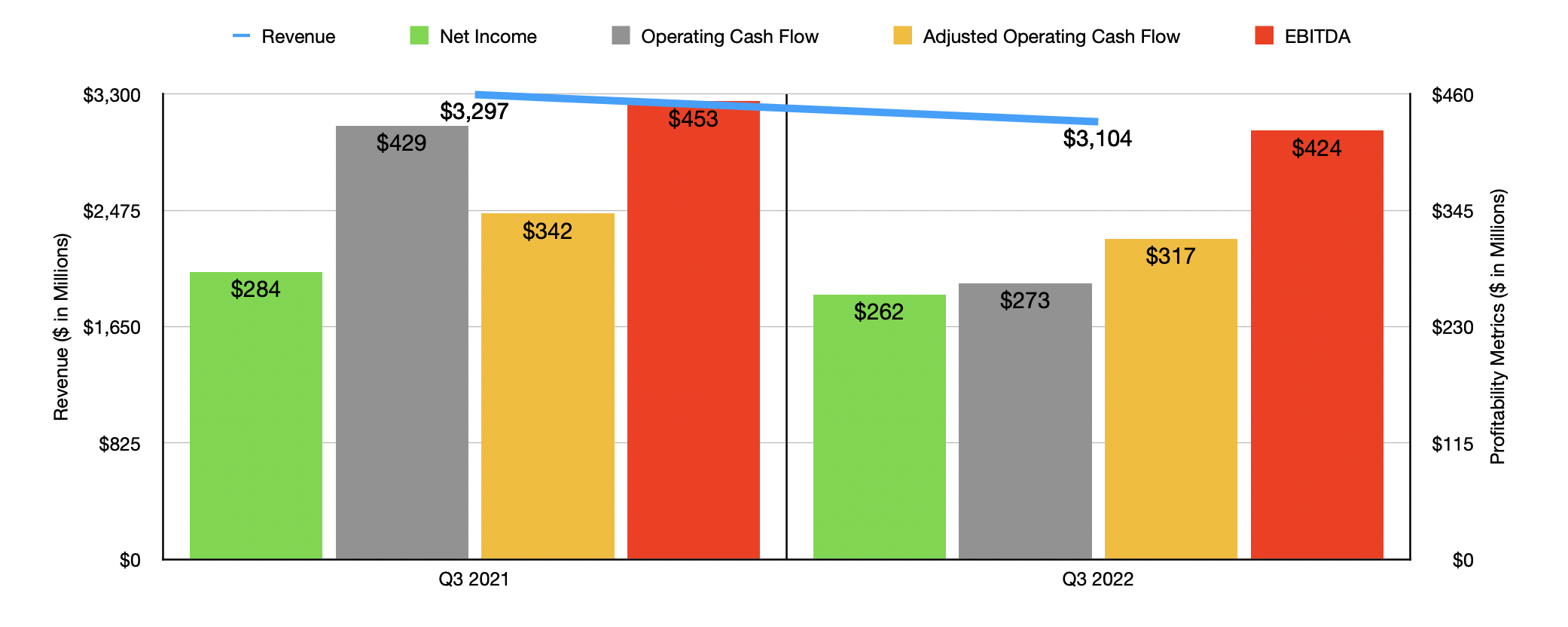

This return disparity came about even though recent performance by the company has been somewhat weak. Consider revenue for the third quarter of its 2022 fiscal year. This is the first and only quarter for which new data has been made available that was not available when I last wrote about the business. Sales during that time totaled $3.10 billion. That's 5.9% lower than the $3.30 billion reported one year earlier. It's important to note here that actual organic revenue for the company came in positive year over year, climbing 3.2%. However, foreign currency fluctuations, combined with a 2.1% hit associated with net acquisition and divestiture activities, pushed sales down during this time.

This drop in revenue brought with it a decline in profits. Net income fell from $284 million to $262 million. Even though the company was hit by the decline in sales, actual gross profit margin rose from 40.8% to 41.1%. For the third quarter alone, that translated to $9.3 million in additional pre-tax profits. This was offset, unfortunately, by a rise in selling, general, and administrative costs. But as a whole, it is nice to see some areas of improvement. Other profitability metrics followed net income lower. Operating cash flow, for instance, plunged from $429 million to $273 million. Even if we adjust for changes in working capital, the metric would have declined, dropping from $342 million to $317 million. Also on the decline was EBITDA. According to management, it dropped from $453 million to $424 million.

{kind=link}

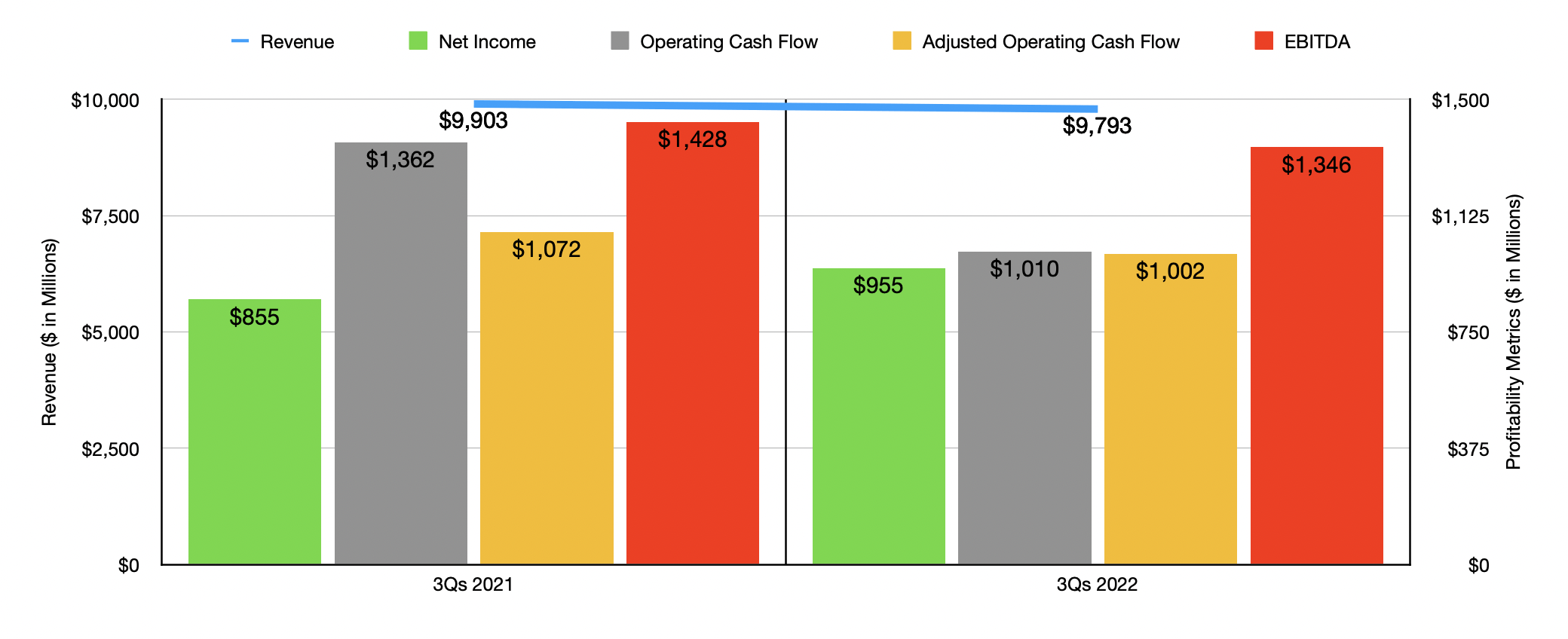

The results experienced in the third quarter were largely responsible for weakness that the company experienced in the first nine months of 2022 relative to the same nine months of 2021. Sales fell from $9.90 billion to $9.79 billion. Profits still managed to increase, jumping from $855 million to $955 million. But when it comes to profitability metrics, that's the only good news. Operating cash flow fell from $1.36 billion to $1.01 billion, while the adjusted figure for this dipped from $1.07 billion to $1 billion. Even EBITDA pulled back, dropping from $1.43 billion to $1.35 billion.

Before the market opens on February 23rd, the management team at LKQ Corporation is expected to announce financial results covering the final quarter of the company's 2022 fiscal year. Leading up to that time, analysts have somewhat mixed expectations . The current expectation is for sales of $3.03 billion. If this comes to fruition, it would translate to a year-over-year decrease of 4.9% compared to the $3.19 billion reported in the final quarter of 2021. As I mentioned already, organic revenue for the company has been positive for the time periods that we have access to. All the pain experienced on the top line has been driven by foreign currency fluctuations. I suspect that any sort of drop seen in the final quarter compared to the same time last year will be due to the same issues. My point on this will become even clearer when we talk about management's own guidance for 2022 as a whole in a moment.

On the bottom line, analysts expect earnings per share of $0.83. This would actually be an increase over the $0.81 per share the company generated in the final quarter of its 2021 fiscal year. This may seem encouraging. And in a sense, it is. However, we can't just take this number in a vacuum. From the third quarter of 2021 to the third quarter of 2022, the company reduced its share count by 6.9%. It is almost certain that the share count will continue to have dropped into the fourth quarter. But instead of speculating, I would like to use data from the third quarter. If LKQ Corporation’s share count remained flat from quarter to quarter, the earnings per share anticipated by analysts would translate to net income of $227.92 million. That's actually down from the $236.28 million in profits achieved in the final quarter of 2021. Even adjusted profits, which analysts are forecasting to be $0.85 per share, would translate to net income falling to $233.41 million. Obviously, investors should also be paying attention to other profitability metrics. Operating cash flow in the final quarter last year was $5 million. But if we adjust for changes in working capital, that number would be $299 million. Meanwhile, EBITDA in the final quarter of last year came in at $357.82 million.

{kind=link}

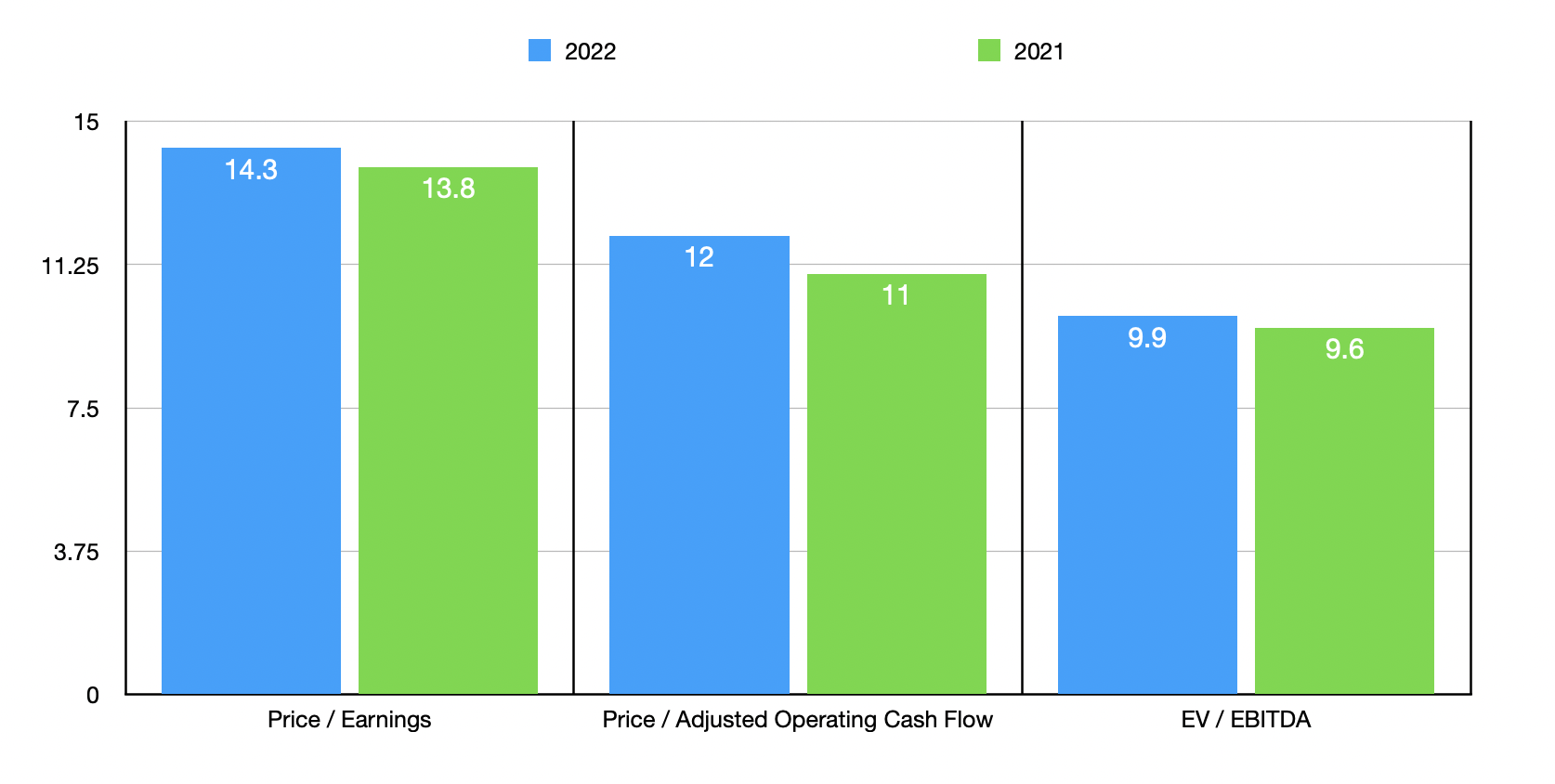

When it comes to the 2022 fiscal year in its entirety, management did say that organic revenue should be between 4.75% and 5.75% higher than it was in 2021. The firm forecasted earnings per share, on an adjusted basis, of between $3.85 and $3.95. That would imply adjusted net income of roughly $1.05 billion. Operating cash flow should be around $1.25 billion according to management, while guidance for EBITDA would translate to a reading of $1.74 billion. Based on these numbers, the company is trading at a price-to-earnings multiple of 14.3. The price to adjusted operating cash flow multiple should be 12, while the EV to EBITDA multiple should come in at 9.9. By comparison, if we use data from 2021, these multiples would be 13.8, 11, and 9.6, respectively. As I do with other companies that I analyze, I decided to compare LKQ Corporation just some similar firms. In this case, I picked out four different companies. On a price-to-earnings basis, these companies ranged from a low of 19.5 to a high of 24.6. Using the price to operating cash flow approach, the range was from 13.9 to 17. And when it comes to the EV to EBITDA approach, the range should be from 10.8 to 16.7.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| LKQ Corporation |

| 14.3 |

| 12.0 |

| 9.9 |

| Genuine Parts Co ( GPC ) |

| 20.8 |

| 16.5 |

| 13.4 |

| O'Reilly Automotive ( ORLY ) |

| 24.6 |

| 17.0 |

| 16.7 |

| AutoZone ( AZO ) |

| 21.1 |

| 15.8 |

| 14.3 |

| Advance Auto Parts ( AAP ) |

| 19.5 |

| 13.9 |

| 10.8 |

Investors should also be aware that management is making some interesting moves from the perspective of returning capital to shareholders. In October of last year, for instance, the company increased its share repurchase authorization plan by $1 billion, taking it up to $3.5 billion. This expires at the end of October of 2025. While this may seem like a tremendous amount of capital to allocate toward share repurchases, especially for a company with a market capitalization of $15 billion, it's worth noting that, in the first nine months of 2022 alone, management allocated $891 million toward buying back 17.6 million shares. And from October of 2018 through the third quarter of last year, they repurchased 52 million shares for an aggregate purchase price of $2.2 billion. I would prefer if management used this capital for growth initiatives. But either way, it does go to reward shareholders.

Taking a step away from the numbers, I think a lot can be said about a company like LKQ Corporation. For starters, the business is operating in a market that should continue to grow in the long run. The more the global population grows, the more vehicles that would be on the road. However, the overall picture is a bit more complicated than that. As time goes on, cars become more reliable. This means that they break down less often. But it also means that consumers or keeping them longer than they did previously. This is a double-edged sword for the company. Having said that, the picture clearly comes out in favor of a bullish outlook for the business.

{kind=link}

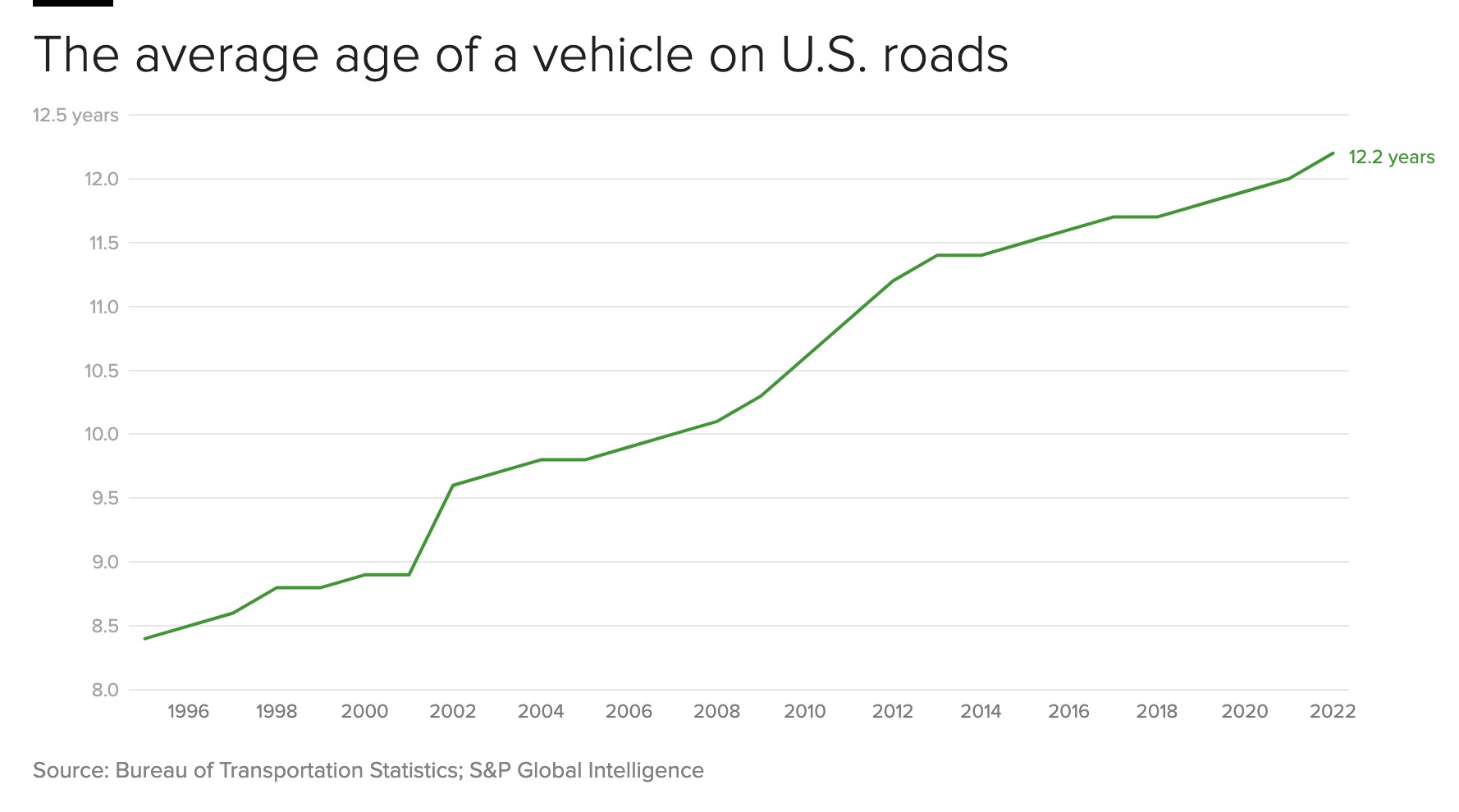

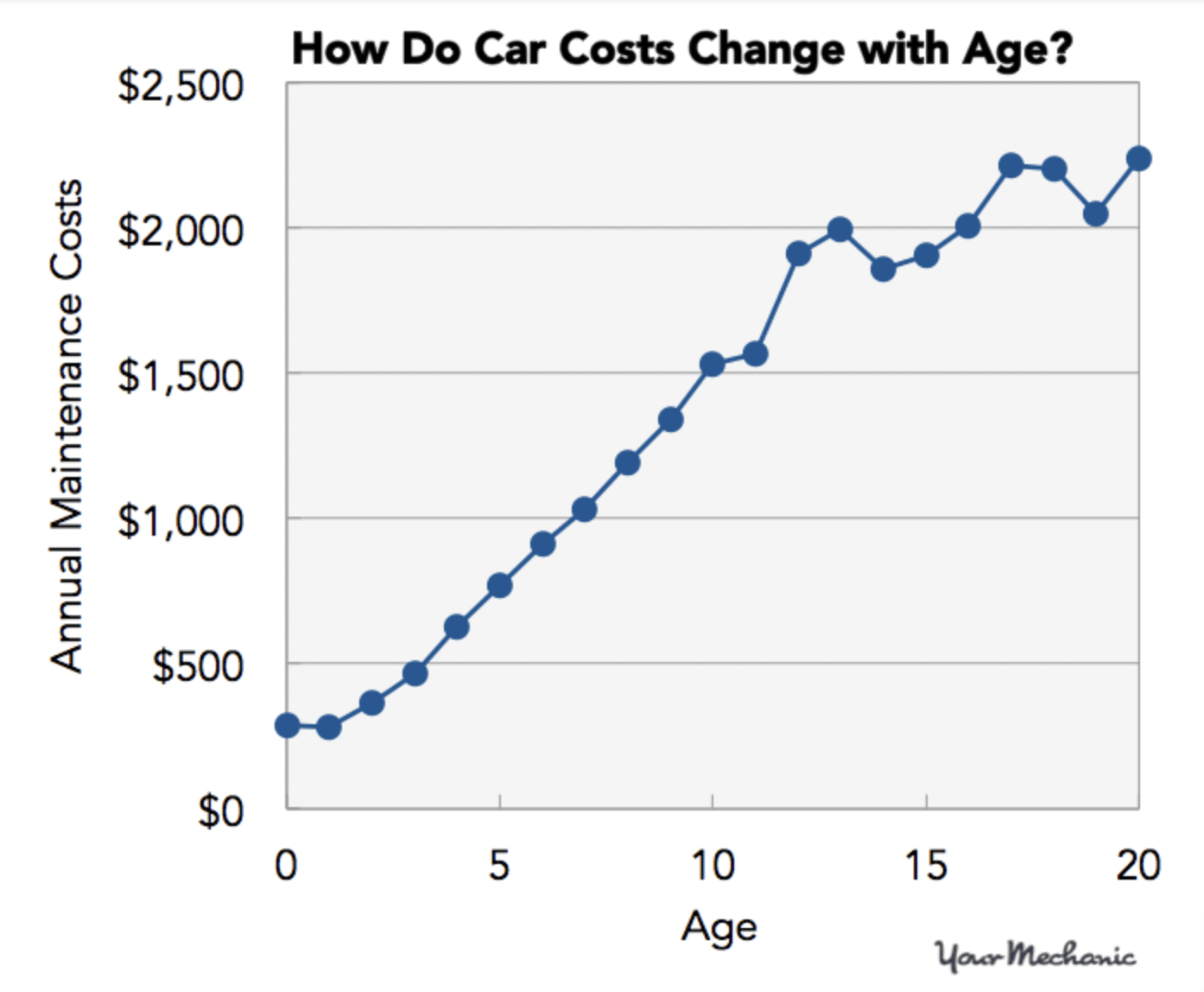

I say this based on a couple of different factors. First and foremost, in the U.S. market, for instance, the general trend has been toward keeping vehicles longer and having to spend more money to keep them on the road. In the image above, you can see that, back in 1995, the average age of a vehicle in the US fleet was 8.4 years. By 2022, that number hit an all-time high of 12.2 years. Admittedly out of date, the image below shows that, on average, the older a vehicle is, the more it costs for repairs and maintenance.

{kind=link}

Of course, some may point out the fact that LKQ Corporation gets only 39.4% of its revenue from its North American operations. By comparison, Europe accounts for 46.3% of sales. While this is true, the first thing we need to keep in mind is that the North American market is still the most important space for the business, as evidenced by the fact that, in 2021, 52.9% of its profits came from here. Only 34.6% of its profits came from Europe. But in addition to that, we need to consider that the average age of a vehicle in the European fleet is also quite old. Using data from 2020, the average age for passenger cars was 11.8 years for the 27 EU member states. Vans are, on average, 11.9 years old, with buses coming in at 12.8 years. Trucks were at the top of the list, averaging 14.1 years. This does vary significantly from country to country. For passenger cars, as an example, Ireland came in at the bottom at only 8.6 years. Lithuania, meanwhile, had an average age of 17 years.

In addition to this favorable trend, the company also has some other areas that it can grow into. For instance, its forecast is for the number of BEVs (Battery-powered Electric Vehicles) that are eight years of age or older in the US to grow by around 42% per annum between 2021 and 2030, eventually hitting around 1.5 million in total. This opens the door for the company's proprietary technology for hybrid battery reconditioning, additional revenue from battery installations, and other offerings. Management is also forecasting that the U.S. market for diagnostics, calibration, and complex sublet repairs will continue to grow at a rate of around 7% per annum between 2021 and 2026. This could also prove beneficial for the company.

Takeaway

Recent weakness experienced by LKQ Corporation is less than desirable. The good news, however, is that its top line pain is really being driven by foreign currency fluctuations. These will not always be problematic for the company. It is true that bottom line results for 2022 will almost certainly come in worse than they did in 2021. But even so, shares look reasonably attractive and are particularly appealing when compared to similar businesses. Because of this, I still do think the company warrants a ‘buy’ rating at this time.

For further details see:

LKQ Corporation Q4 Earnings Preview: Recent Weakness Does Not Detract From The Firm's Upside Potential