LKQ - LKQ Corporation: Undervalued Stable Business With A Great Potential Upside

2023-12-28 01:49:37 ET

Summary

- LKQ is undervalued compared to its peers and has a stable business, making it a strong value play.

- The company is a leading provider of alternative and specialty parts for automobiles and has a diverse customer base.

- LKQ's recent financial performance has been positive, with organic growth, strong cash flow, and a commitment to returning value to shareholders.

Executive Summary

LKQ Corporation ( LKQ ) represents a strong value play with a stable business that is undervalued versus its peers (Trading Multiples Analysis) and Discounted Cash Flow Analysis. Value Voyage initiates coverage with a $57.50 price target with a Buy Rating, representing a 25% upside.

Company Overview

LKQ Corporation is a leading provider in the alternative and specialty parts industry for automobiles and other vehicles. The company's core business revolves around distributing vehicle parts, components, and systems needed for the repair and maintenance of vehicles. LKQ's operations encompass a broad range of products, including recycled automotive parts harvested from salvaged vehicles, remanufactured, and refurbished parts, new parts sourced from OEMs (Original Equipment Manufacturers), and aftermarket parts.

The company's business model is centered on providing high-quality, cost-effective alternatives to new OEM parts. LKQ sources its inventory from a variety of channels including salvage auctions, insurance companies, and directly from OEMs. One of the key aspects of their operation is the recycling of parts from vehicles that are no longer roadworthy, a practice that not only supports environmental sustainability but also offers a cost-efficient solution to their customers.

In addition to automotive parts, LKQ also deals in related accessories and products used in the repair process, such as paint and body shop materials. This makes LKQ a one-stop shop for repair shops and vehicle owners seeking a comprehensive range of products and services for vehicle maintenance, repair, and customization.

LKQ's customer base is diverse, catering to collision and mechanical repair shops, new and used car dealerships, as well as retail customers seeking to repair or customize their vehicles. The company has established a strong distribution network that enables efficient and timely delivery of parts to customers across various geographies. This network is supported by advanced logistics and inventory management systems, ensuring that a wide range of parts are readily available to meet customer demand.

Moreover, LKQ has expanded its footprint globally through strategic acquisitions and partnerships, enabling it to serve a wider market and diversify its product offerings. Their global presence not only fortifies their supply chain but also enhances their ability to meet the specific needs of different regional markets.

Most Recent Financial Performance - Q3 Report

{kind=link}

Revenue per Segment (LKQ Q3 Investor Presentation)

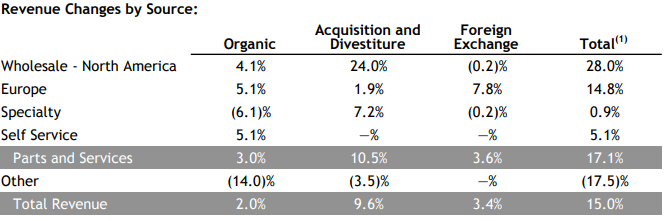

In its recent Q3 2023 report, LKQ showcased notable financial and operational achievements. The company reported a 3.0% organic growth in parts and services, with Europe showing a robust 5.1% growth and the Wholesale - North America segment experiencing a 4.1% increase. However, this growth was offset by a 6.1% decline in the Specialty segment. The Segment EBITDA amounted to $422 million, achieving an EBITDA margin of 11.8%, despite the dilutive impact of the Uni-Select Inc. acquisition. Notably, the Wholesale - North America Segment and the Europe Segment recorded EBITDA margins of 17.0% and 9.3%, respectively. The company's operational efficiency was further evidenced by an operating cash flow of $441 million and a free cash flow of $344 million, keeping LKQ on track to hit the $1 billion free cash flow mark for the year 2023.

LKQ's commitment to returning value to shareholders was evident through its financial maneuvers. The company distributed a quarterly dividend of $0.275 per share and approved a 9% increase for November 2023. Furthermore, LKQ completed strategic acquisitions, including that of Uni-Select, and divested GSF Car Parts.

Looking forward to the rest of 2023, LKQ provided an optimistic outlook. The company anticipates organic parts and services revenue growth to be between 4.75% and 5.75%, with a projected diluted EPS of $3.41 to $3.55 and an adjusted diluted EPS of $3.68 to $3.82. In terms of cash flow, LKQ expects operating cash flow to be around $1.3 billion and free cash flow to be approximately $1.0 billion, translating to a free cash flow conversion of 55% to 60% of Adjusted EBITDA.

Positive Managerial Change

LKQ also recently announced a leadership change , with Dominick Zarcone seeking retirement. One of his top deputies, Justin Jude, was named the new CEO. Jude's appointment comes after a notable tenure as the President of LKQ's Wholesale – North America segment, where he demonstrated a strong ability to improve margins and cash flow. His leadership has been characterized by a focus on operational efficiency and market expansion, qualities that are important as LKQ navigates the landscape of the auto parts industry.

Jude's previous experience as President of LKQ's Specialty segment is particularly relevant in the context of the rapidly growing electric vehicle ((EV)) market. This segment's focus on diverse and innovative product lines aligns well with the strategic requirements of the EV transition, suggesting that Jude's leadership will be instrumental in positioning LKQ at the forefront of this shift. His approach is expected to be one of continuity, building on the strong foundation laid by his predecessor, Dominick Zarcone.

Industry Analysis

The Auto Parts Wholesaling industry in the United States has experienced steady growth, with an estimated Compound Annual Growth Rate ((CAGR)) of 2.3%, reaching $278.7 billion in 2023, according to IBISWorld. This growth trajectory is set to continue, with a projected increase in revenue of 3.62% from 2023 to 2027 . This uptick is attributed to a rise in motor vehicle registrations and an increase in per capita disposable income. The industry faced challenges during 2020 due to widespread stay-at-home orders and a spike in unemployment, which discouraged large purchases like automobiles and also resulted in deferred maintenance. However, despite these setbacks and a shift in consumer behavior towards working from home, the demand for auto parts has seen a resurgence, coinciding with the recovery in vehicle registrations. This resurgence is reflected in the industry's profit metrics, which have shown a slight increase as wholesalers successfully passed along rising costs to their customers.

Author's Calculations

The Industry Matrix graph above serves as an analytical tool to gauge the attractiveness of the auto parts industry, measuring industries on two axes: 'Volatility' and 'Growth'. The 'Volatility' axis represents the level of uncertainty and risk associated with the industry, while the 'Growth' axis quantifies the expansion potential within the sector. Industries placed within the 'Star' quadrant, such as Auto Parts Wholesaling, are considered to exhibit the ideal combination of low volatility and high growth, indicating a stable yet dynamic market environment. This positioning underscores an industry that is not only growing steadily but also offers a relatively predictable and secure investment landscape. For LKQ, landing in the 'Star' quadrant reinforces the industry's status as a strong performer capable of navigating the complexities of the industry while capitalizing on growth opportunities.

Prior to COVID, the industry displayed strong growth, driven by the strengthening of partnerships between original equipment manufacturers (OEMs) and wholesalers. This was in response to growing consumer spending and evolving preferences. The industry also benefited from increased domestic production by foreign competitors, as it allowed wholesalers to leverage comprehensive distribution networks, local relationships, and workforce. Foreign wholesalers have amplified their operations in the U.S. to cater to existing partnerships with manufacturers, meeting the demand for foreign car parts.

The long-term sales prospects of the industry hinge on the adoption of technologically advanced amenities, such as onboard diagnostic systems, sold to retailers and individual stores. As fuel economy standards evolve, auto manufacturers are required to integrate fuel-efficient technology into new vehicle platforms, driving demand for these advanced auto parts. The industry is expected to maintain steady growth, aligning with moderate increases in consumer spending and total vehicle miles.

The competitive landscape of the industry is marked by intense competition and rapid consolidation. Major players, such as LKQ, have managed to secure higher profit margins and significant revenues due to economies of scale and bulk purchasing advantages. The industry is also adapting to changes in environmental regulations and consumer preferences, which are shaping the market and the types of products in demand. Additionally, the industry is leveraging technology to streamline purchasing processes and improve efficiency, which is increasingly important as online shopping gains popularity and new players like Amazon enter the consumer auto parts market. The industry's ability to adapt to these changing dynamics will be critical for its future growth and sustainability.

Correctly Positioned for the Coming EV Transition

The auto parts industry is at the beginning of a transformative shift with the advent of EVs, which brings both challenges and opportunities for established players like LKQ. McKinsey's insights highlight that while fundamental components for light vehicles will remain in demand, the industry is tilting toward EV-specific parts and sophisticated electronics. By the end of this decade, such components are projected to make up over a third of the market, a significant increase from their current share. This pivot necessitates a strategic refocusing on production efficiencies and innovation to stay competitive and tap into emerging growth areas like battery housings, which are anticipated to expand at a CAGR of 23% and become a $30 billion market by 2030.

LKQ's acquisition of Uni-Select strategically expands its footprint, giving it a stronger presence in the distribution of automotive refinish and industrial paint products, a segment that remains vital in both traditional and EV markets. This move can be seen as part of LKQ's broader strategy to diversify its product range and reinforce its distribution channels, ensuring that it remains well-positioned to serve the evolving needs of the industry. As the shift towards EVs progresses, demand for core components will still grow steadily, though at a decelerated pace compared to EV components, which are expected to surge. LKQ's revenue streams have been further diversified because of the acquisition, placing it in a good position to capitalize on long-term market changes.

Discounted Cash Flow Valuation

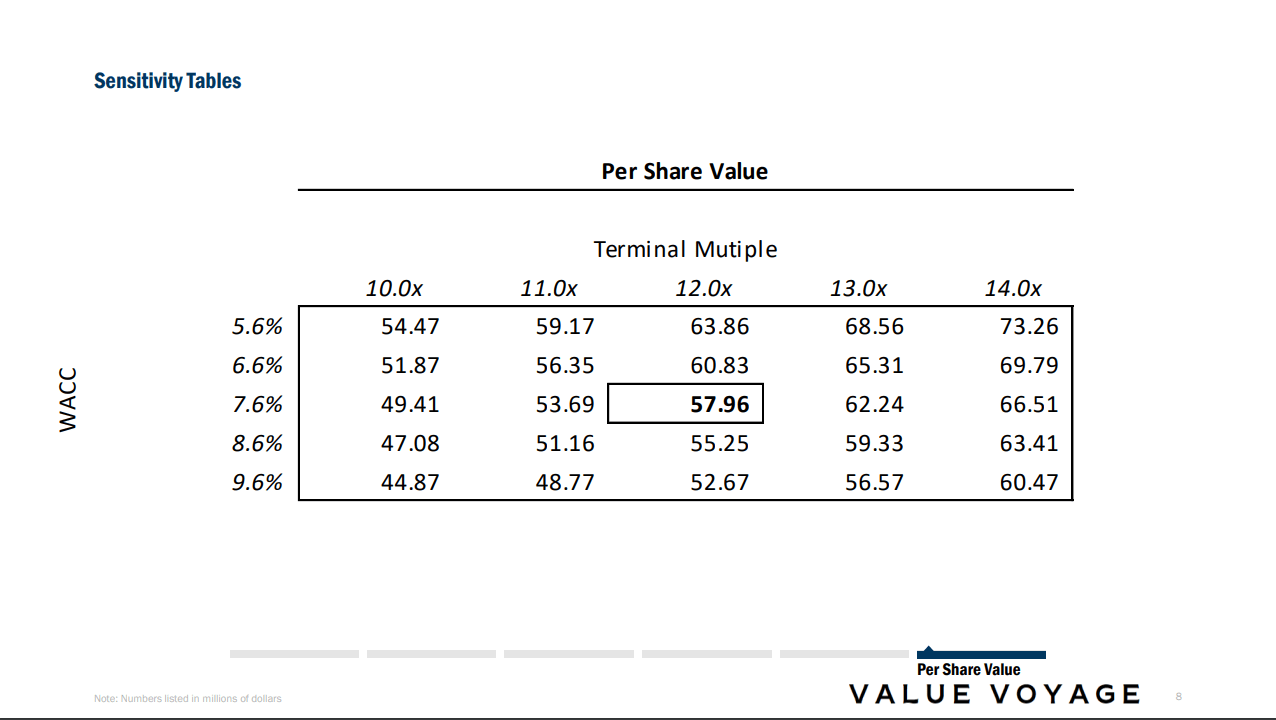

LKQ Per Share Value Calculation with Sensitivities (Author's Calculations)

{kind=link}

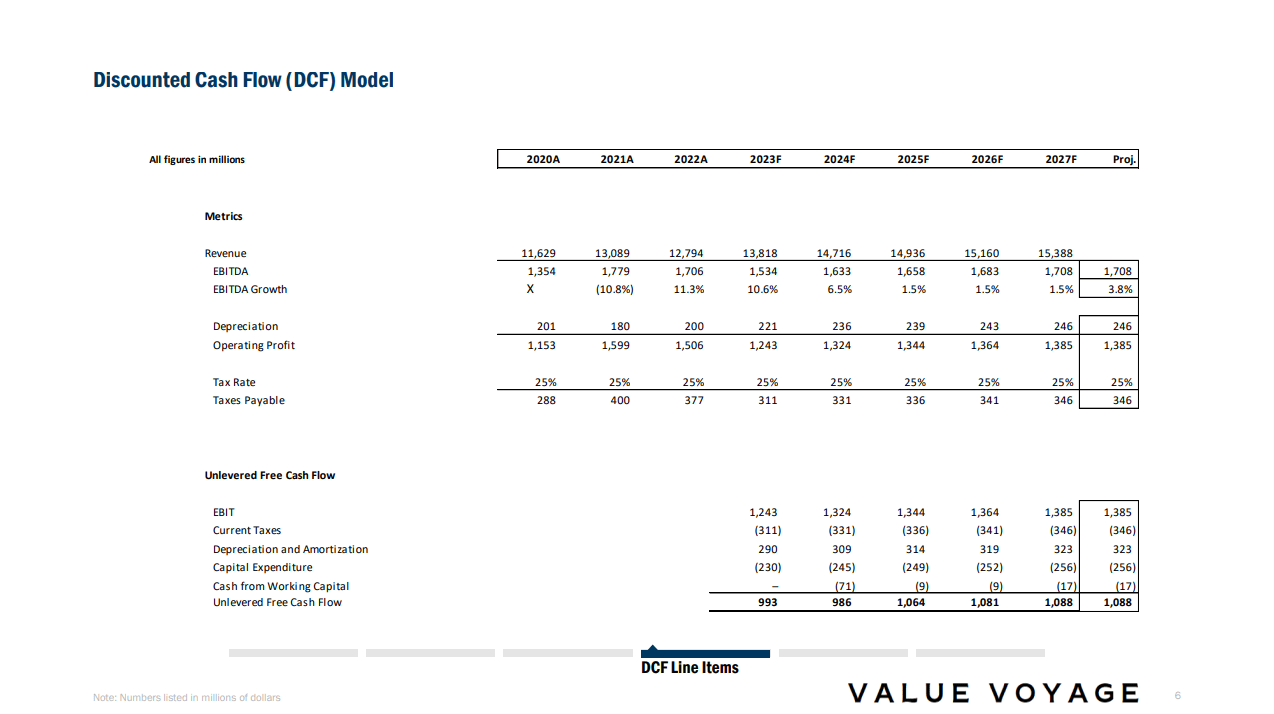

LKQ shows steady earnings and strong growth, as well as boasting a 2.5% dividend. All DCF projections were made independently and then compared with mean estimates via analyst expectations to ensure accuracy.

Starting in 2023 with an expected revenue of $13.8 billion, LKQ is poised for consistent growth in the coming years. I expect revenue to increase to $14.7 billion, followed by a further rise to $14.9 billion. This upward trend continues with the revenue projections reaching $15.1 billion and eventually $15.3 billion in the subsequent years. These figures reflect LKQ's strong market position and its ability to capitalize on increasing demand within the auto parts industry.

{kind=link}

Author's Calculations

The end of the projection period results in a final EBITDA of $1.7 billion, at a 12x multiple (pulled from trading history and comparable companies) leading to an Enterprise Value of $18.40 billion and a corresponding per-share value of $57.50 (57.96).

This represents a roughly 25% upside to the current price at a 12x multiple, with a significantly higher trading price if LKQ trades near the median of the industry.

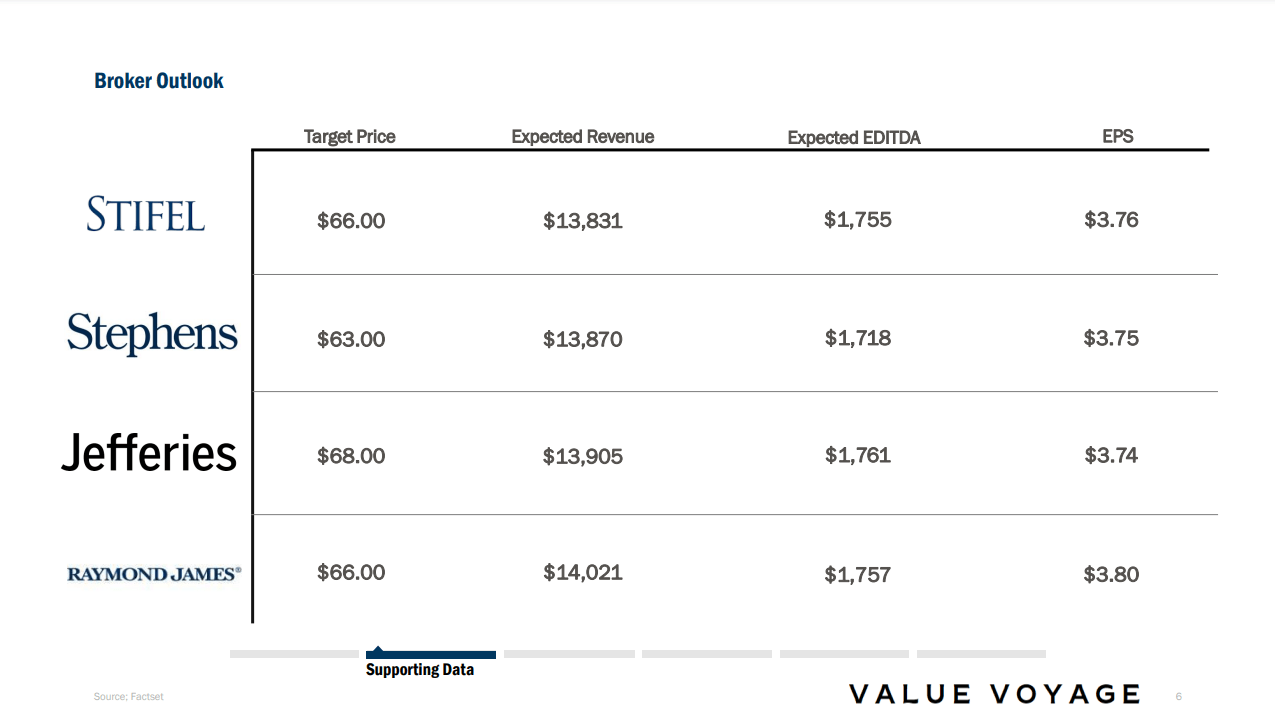

Furthermore, our target price falls below mean estimates for all but one equity research broker, showing even more possible upside:

{kind=link}

The full range of broker range of estimates is $55-$68 a share.

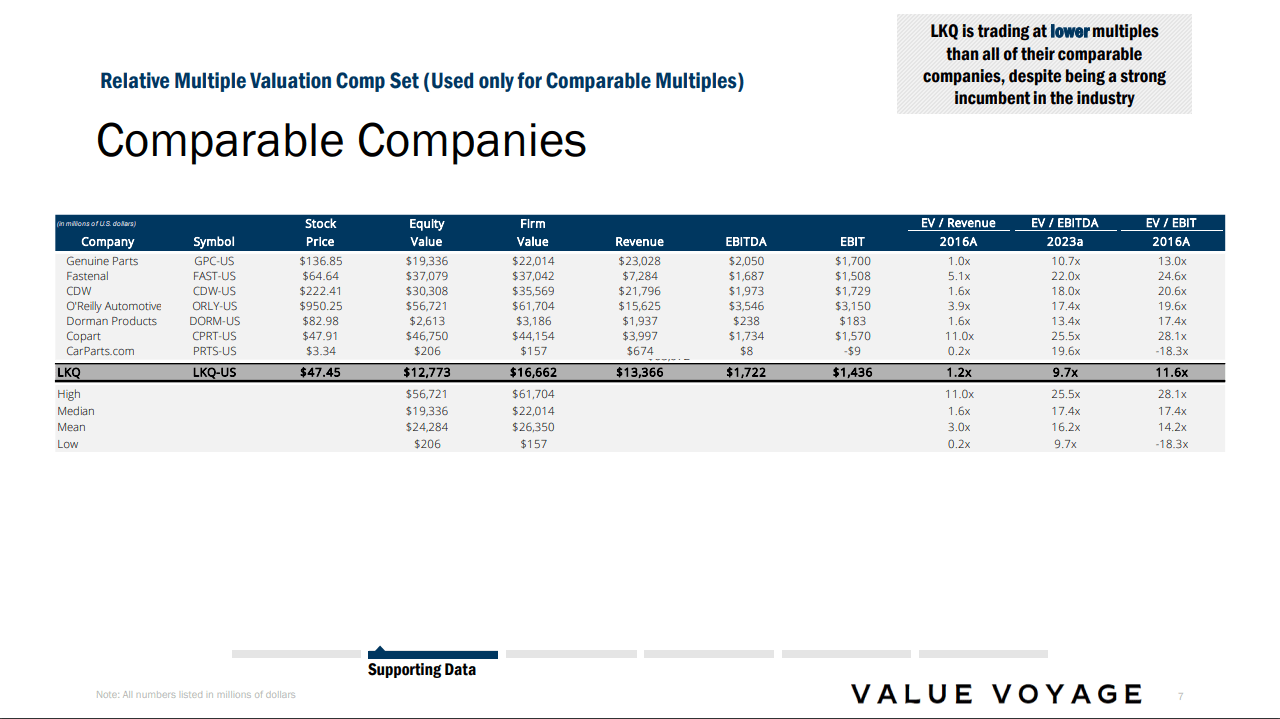

Multiples Analysis

{kind=link}

LKQ, when examined through the lens of key metrics such as EV/Revenue, EV/EBITDA, and EV/EBIT, reveals a company that is undervalued relative to its industry peers. With a lower EV/Revenue multiple compared to the median of its comparable companies, LKQ stands out for its ability to generate significant revenue at a relatively lower enterprise valuation. This suggests that the market has not fully priced in the company’s revenue-generating efficiency, indicating a potential undervaluation.

Diving deeper into profitability, LKQ's EV/EBITDA multiple further underscores this undervaluation narrative. Despite strong EBITDA figures, which are indicative of robust operating performance, LKQ's enterprise value to EBITDA remains modest when compared to the industry's higher median multiple. This could be interpreted by investors as an opportunity, signaling that LKQ's operational earnings are available at a discount to those of similar companies.

Finally, I compared the EV/EBIT multiple, which provides a more direct view of operating profitability by excluding non-cash expenses, and paints a similar picture. LKQ's multiple is lower than the industry's mean, suggesting that its earnings before interest and taxes are not being overvalued by the market. This reinforces the argument that LKQ's stock could represent a value buy in an industry where investors may be paying a premium for profitability. Together, these valuation metrics position LKQ as an attractive investment for those looking for undervalued opportunities in the auto parts sector.

Possible Reasons for Undervaluation

LKQ's recent stock performance, marked by a notable selloff, can be closely associated with the market's reaction to slight misses in earnings expectations. In current market conditions, even small deviations from forecasted financials can trigger significant responses. This sensitivity is often amplified by the high expectations placed on companies like LKQ, known for their consistent financial track record , having beaten earnings in 8 out of the last 10 announcements. As the market digests these earnings reports, the reactions can sometimes overshadow the company's long-term fundamentals, leading to undervaluation.

Compounding the effect of earnings misses is the automotive industry's ongoing transition to electric vehicles. Investors may be uncertain about traditional auto parts suppliers' roles in the EV-dominated future, leading to an overcorrection in the stock prices of these companies. LKQ, despite its strong market position and potential to adapt to the EV shift, has not been immune to these concerns. The company's extensive distribution network and diversification strategy position it well to navigate this transition, suggesting that the current undervaluation may not fully account for its adaptive capabilities and future growth prospects in the evolving automotive landscape.

Risk to Thesis

Our thesis has several potential risks.

First, this industry is heavily regulated by environmental and vehicle safety standards. Any shifts in regulatory policies could result in increased compliance costs for LKQ, affecting its bottom line. Compliance is not only a financial burden but also critical to the company's reputation; failure to adhere to regulations could lead to substantial fines and reputational damage.

Supply chain integrity is another area of concern. LKQ relies on a global network for parts sourcing, making it vulnerable to disruptions from geopolitical instability, trade conflicts, or environmental catastrophes. Such interruptions could affect inventory availability and delay delivery times, which may lead to customer dissatisfaction and potential revenue loss.

Finally, as I've mentioned above, the advent of EVs presents a double-edged sword. While they open new avenues for growth, EVs could also diminish the demand for traditional auto parts due to their fewer mechanical components and lower maintenance requirements. LKQ must stay ahead of technological trends and adjust its offerings to remain relevant in an industry on the cusp of significant transformation. The company's capacity to adapt to these evolving market conditions will be a decisive factor in sustaining its growth and securing its place in the market.

As it pertains to the impending market changes coming from the rise of EV ownership, the most effective way to monitor this risk would be to closely follow the earnings calls of competing firms in the industry. Through these calls, we all can gain insights into how each company is addressing the EV shift, assess their strategic pivots, and understand the broader impacts on the market. This vigilance will be vital to navigating the evolving landscape and ensuring that our assessments remain current and well-informed.

Conclusion

I firmly believe that LKQ presents a compelling investment opportunity, showcasing robust financial health, a diversified product portfolio, and a solid strategy for growth within the dynamic auto parts industry. Our valuation analysis supports a buy recommendation, underpinned by steady earnings, strategic market positioning, and a favorable industry outlook. Despite facing potential regulatory and market challenges, LKQ's proactive measures and resilient business model position it well to navigate these risks. With a target price of $57.50, reflecting a 25% upside potential, LKQ stands out as a value play that offers investors the prospect of significant returns while contributing to a sustainable and evolving automotive landscape.

Supporting Documentation

For further details see:

LKQ Corporation: Undervalued, Stable Business With A Great Potential Upside