LL - LL Flooring Holdings: Investors Should Push For A Deal

2023-05-31 10:01:29 ET

Summary

- LL Flooring Holdings has received a buyout offer at a substantial premium to its current share price, which could provide relief for investors after a significant decline in the company's value.

- The company's financial performance has deteriorated rapidly, with revenue, net profits, and EBITDA all declining significantly in recent years.

- The buyout offer could be a lifeline for the struggling company, but there is no guarantee that the deal will go through, and management has expressed confidence in their current strategy.

After several months of pain, investors in LL Flooring Holdings ( LL ), a firm that operates as a specialty retailer of hard surface flooring, finally received something of a reprieve on May 30th after news broke that an offer had been made to buy out the firm at a rather substantial premium to what shares were trading at immediately before the offer was made. Although shares of the company are still down significantly from where they were even just one year ago, this premium is nice to see considering how much and how rapidly the fundamental condition of the company has deteriorated. As an analyst who has covered the company before, I feel rather conflicted about recent developments. The speed in which the company has all but falling apart has been astounding. When you combine this with the very real probability that the picture for the company will only worsen from here, investors should probably push management to accept this proposal.

Rapid deterioration

After the market closed on May 30th, shares of LL Flooring Holdings spiked, climbing around 15% in after-hours trading. If we incorporate this 15% increase in share price, this implies a market capitalization for the business of $145.2 million. This is a very small figure compared to what the company was worth only a couple of years ago. From December of 2020 through the present day, shares have plunged 84.5%. But this has not been some random occurrence. Rather, it's because the condition of the company has worsened rather quickly.

{kind=link}

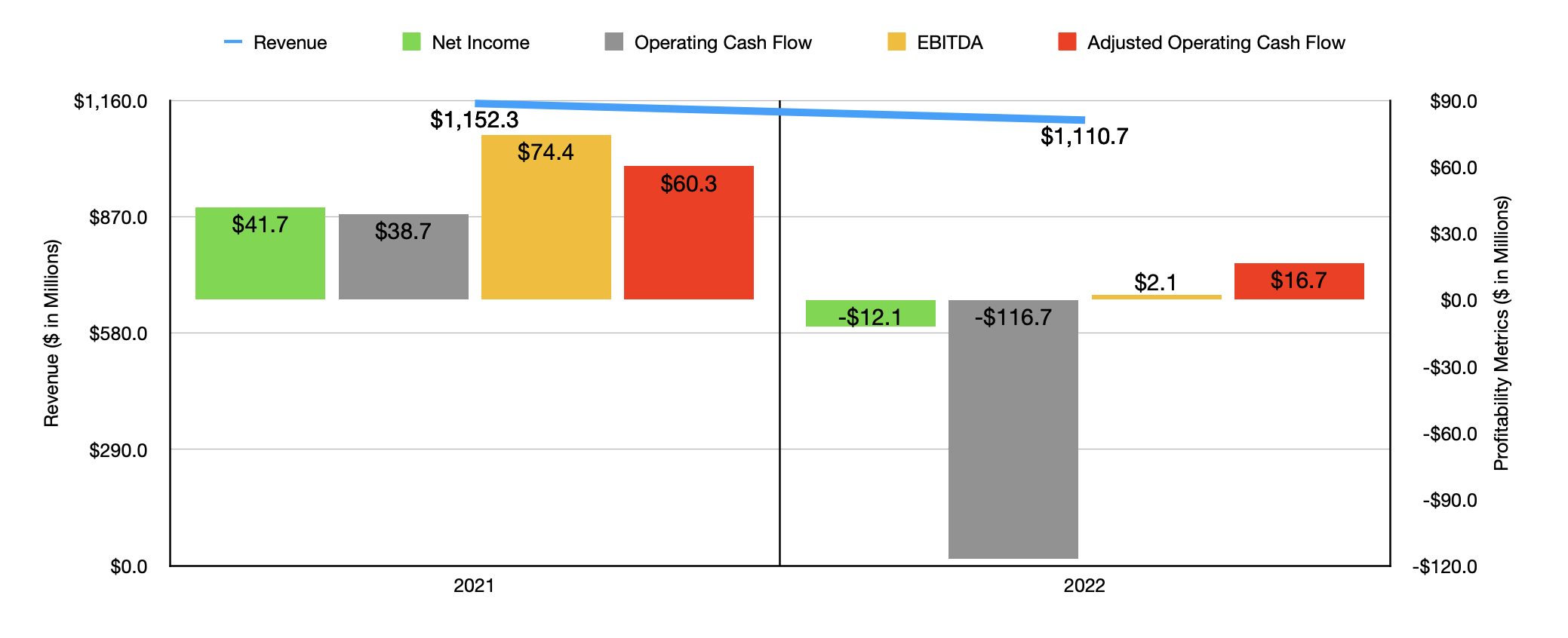

Consider, for instance, the picture between 2021 and 2022 . Revenue dipped slightly from $1.15 billion to $1.11 billion. This on its own would not be enough to push shares of the company down so much. However, the firm's bottom line took a beating during this time. The company went from generating net profits of $41.7 million in 2021 to generating a net loss of $12.1 million last year. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from $38.7 million to negative $116.7 million. If we adjust for changes in working capital, it would have gone from $60.3 million to $16.7 million. And finally, EBITDA for the business dropped from $74.4 million to only $2.1 million.

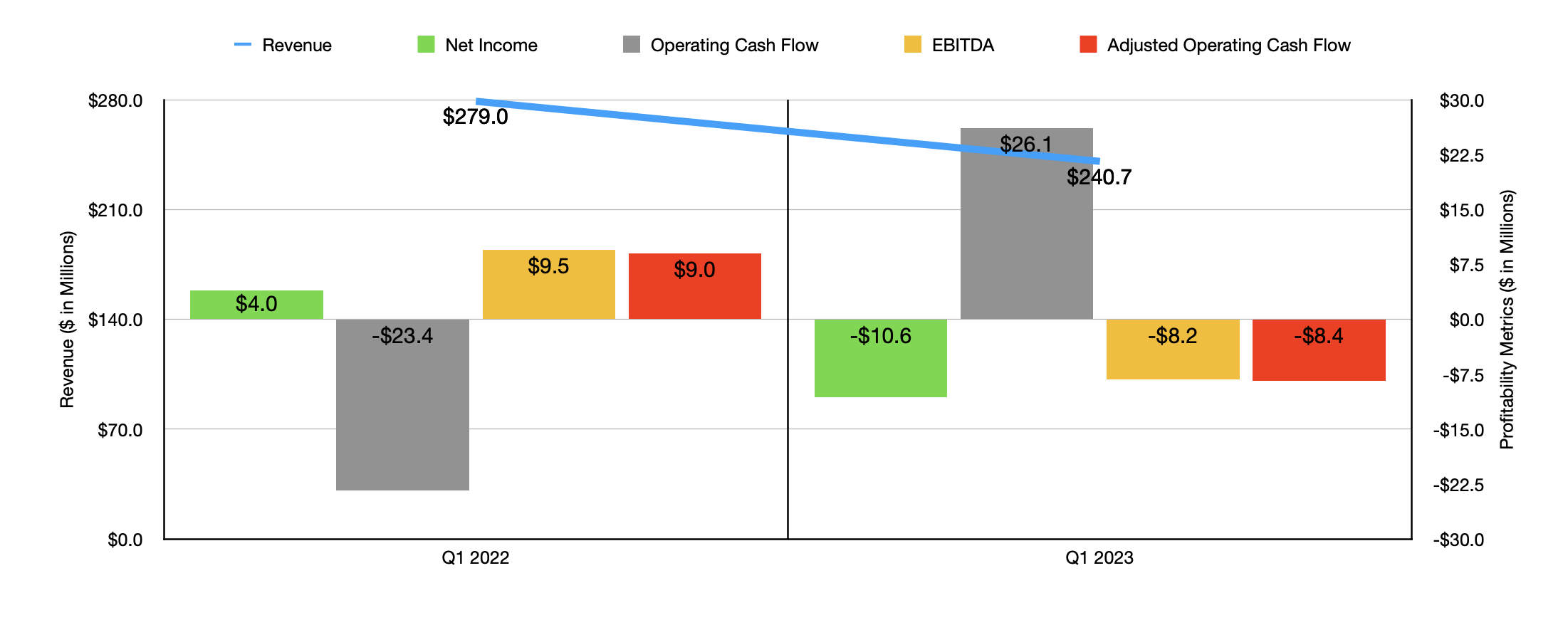

This pain seems to have only accelerated in recent months. Consider how the company performed during the first quarter of its 2023 fiscal year. Sales for that time came in at $240.7 million. That's down 13.7% compared to the $279 million reported one year earlier. Profits have also largely worsened. The company went from generating a net profit of $4 million to generating a net loss of $10.6 million. It is true that operating cash flow improved from negative $23.4 million to positive $26.1 million. But if we adjust for changes in working capital, we would have seen the metric worsen from $9 million to negative $8.4 million. And finally, EBITDA for the business went from $9.5 million to negative $8.2 million.

{kind=link}

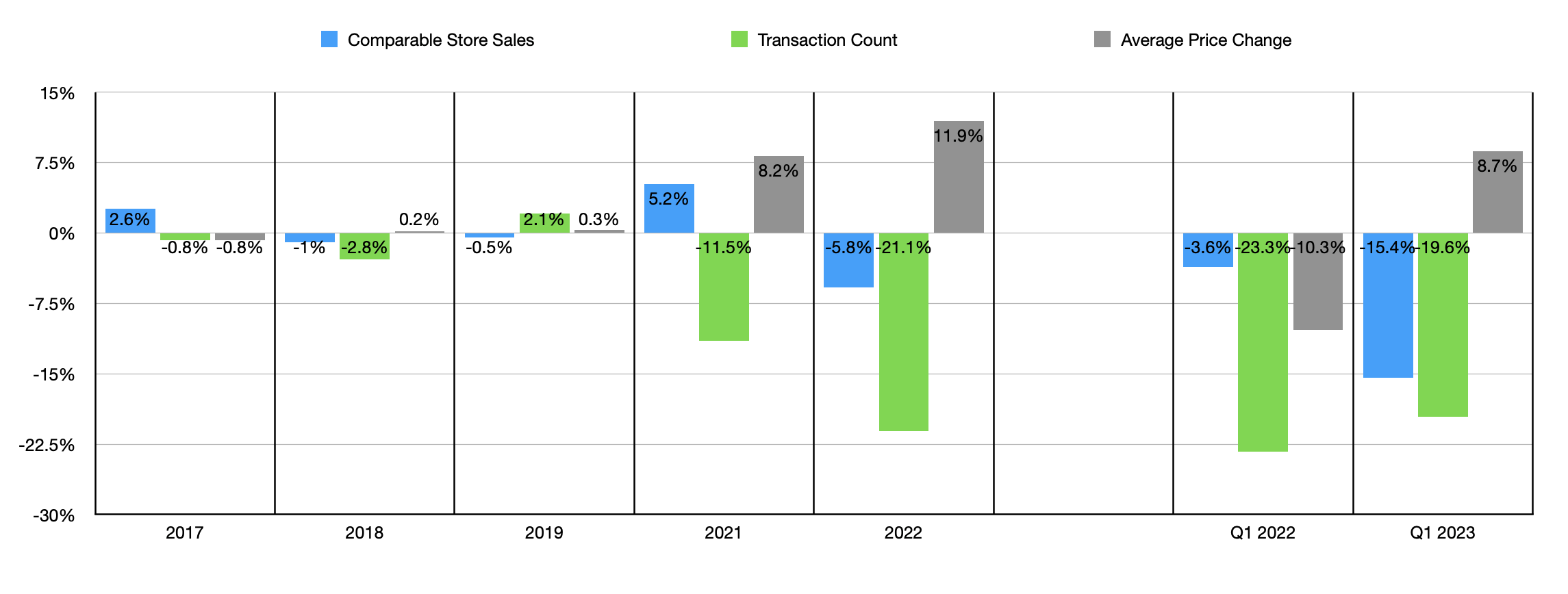

Digging into the data, we can come to understand exactly why all of this happened. In 2022, for instance, the company suffered from a 5.8% decline in comparable store sales. That compares to the 5.2% improvement in comparable store sales seen in 2021. But there's more to this data than meets the eye. The actual number of transactions that the company saw during this time plunged significantly. But that decline actually began even earlier. In four of the past five years, the transaction count for the business came in negative compared to the year prior. In 2021, it was negative by 11.5%. And in 2022, it was negative by 21.1%. Put another way, transaction count over the five years ending in 2022 has dropped by 31.3% in the aggregate.

{kind=link}

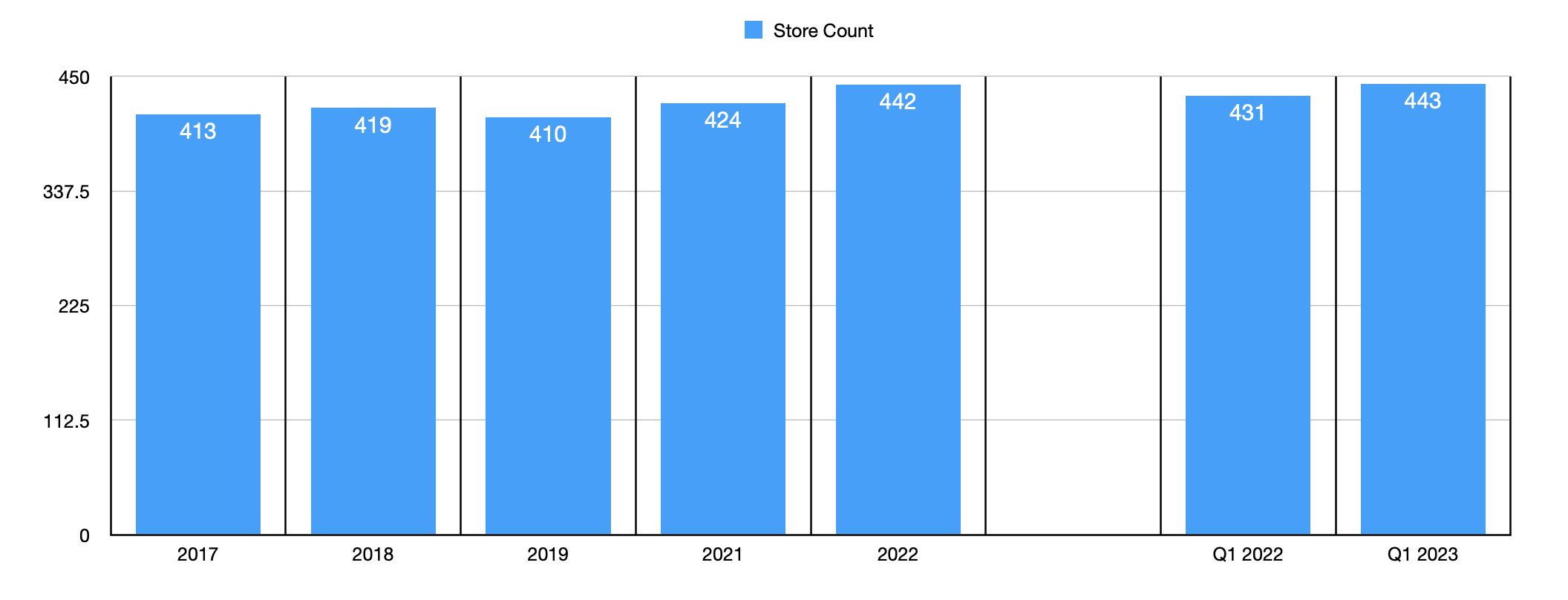

The company was only aided by two factors here. The first was an increase in pricing that it charged its customers. In 2021, for instance, average pricing at its locations jumped 8.2%. This number grew even more at 11.9% last year. On top of this, the number of locations that it operates increased. Back in 2020, for instance, the company had only 410 stores. By the end of last year, this number had grown to 442.

{kind=link}

All combined, this paints a picture of a retailer that continued to hike its prices, and open stores, even though the stores that it already had was experiencing a drop in the number of transactions occurring within them. This is not exactly a recipe for success. And to make matters worse, the picture accelerated this year. Overall comparable store sales in the first quarter of 2023 were negative by 15.4%, with a 19.6% decline in transaction count only partially being offset by an 8.7% increase in pricing. Those who understand retail also know that, as comparable store sales decrease, margins come under significant pressure. This is because there is less revenue to be split between the same value of fixed assets. And with margins in the space already small, the amount of pain that can be experienced on the bottom line is significant.

Recognizing that things have not gone great, the founder of the company, Tom Sullivan, has made an offer to buy up the company in its entirety. In a letter that he wrote to the management team at LL Flooring Holdings, Mr. Sullivan called the financial results that the company achieved in 2022 ‘disappointing’, especially considering how other, larger, rivals fared. His hope is that, by taking the company private and merging it with Cabinets To Go, he can return the enterprise to health. To demonstrate exactly how serious he is about this transaction, Mr. Sullivan and his firm revealed in the letter that he wrote to management that his company already has accumulated more than 9.4% of the economic interests in the company through share purchases.

The effective price, given the current proposal, would come out to $5.76. That's more than double the $2.75 that shares closed at on May 8th of this year. If this offer is ultimately accepted, it would translate to a market capitalization of $175.7 million. The enterprise value would be slightly higher at $215.7 million. Given the historical volatility of the company, it's really difficult to know what is exactly a fair price to pay for the business. For instance, if the company were to revert back to the financial performance that it achieved in 2021, both the price to adjusted operating cash flow multiple and the EV to EBITDA multiple for the business would come out quite low at 2.9. But if we use data from 2022, these numbers should be 83.7 and 12.9, respectively.

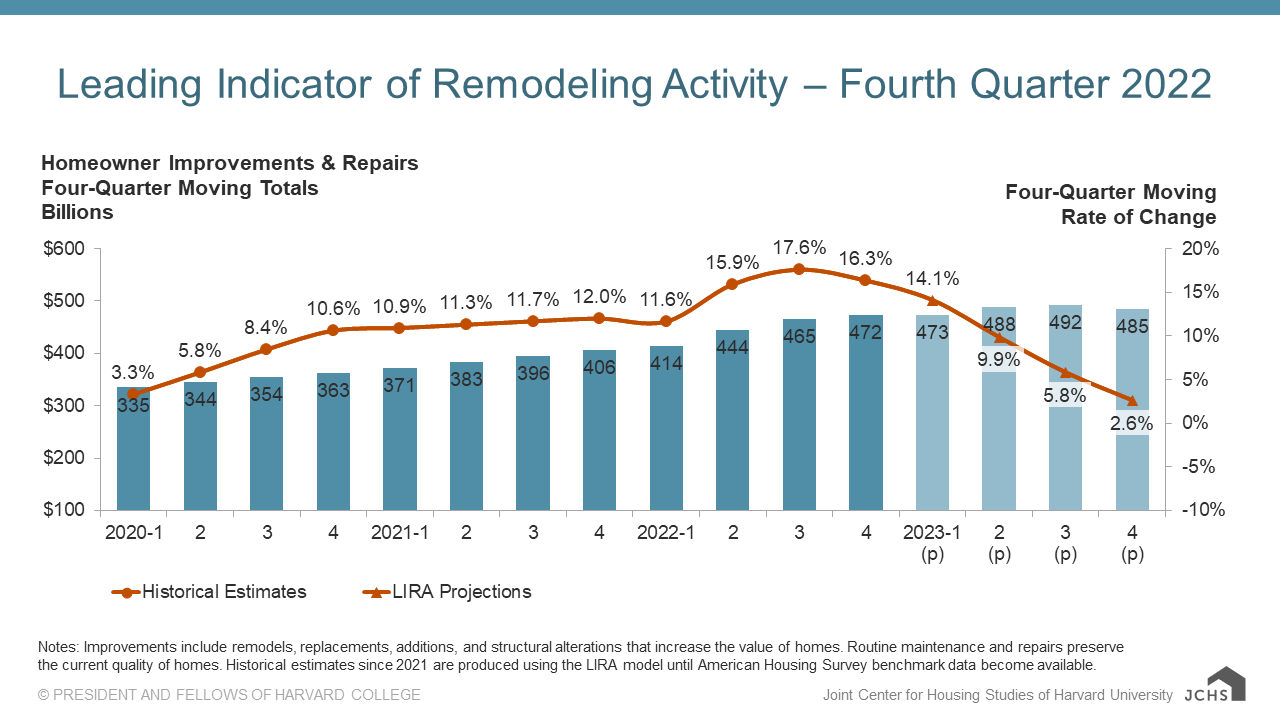

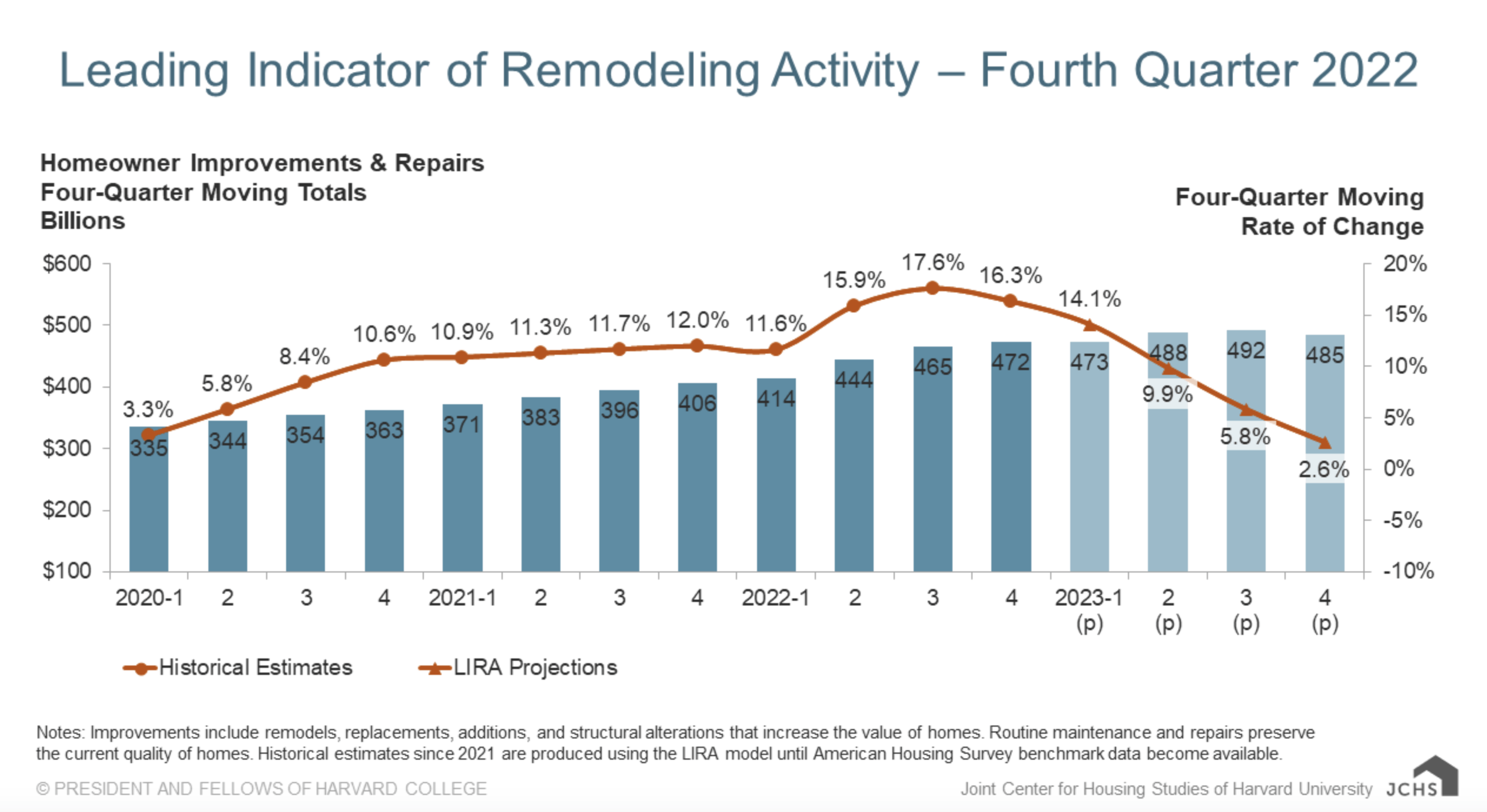

I am a huge fan of buying shares of companies when they are experiencing a bit of pain. If you can accurately point out that a business will survive difficult market conditions and return to health, the upside potential can be significant. But in this case, I have to wonder whether LL Flooring Holdings can survive on its own. Part of my concern is that the company is already experiencing a tremendous amount of pain despite us being in the early stage of a rather difficult market. As I wrote in a prior article , the backlog and the home building market has plummeted over the past year. That should lead to less demand for flooring. But another component to this is the home improvement and repair market. But as the image below illustrates, even that is expected to see a significant slowdown later this year.

{kind=link}

{kind=link}

Takeaway

If we were currently in the later stages of a difficult market, I think I would be a bit more optimistic when it comes to the long-term picture for LL Flooring Holdings. Having said that, the company is experiencing a great deal of pain right now and that picture is likely to worsen from here. It is possible that, by approving a sale of the business, current shareholders may lose out on tremendous upside. But given the risks at the moment, I would make the case that investors would be wise to push for this deal to be approved.

At the moment, there does seem to be a lot of potential on the table, with an additional 21% upside available for shareholders between the after-hours trading price of $4.76 and the proposed buyout price of $5.76. But it's also true that there is no guarantee a deal will transpire. And management's own press release in response to this development involved a rather large paragraph dedicated to explaining to investors that management is confident of the company's current strategy and execution. While the company did say that it will carefully review the proposal, I view this as a red flag. Because of this and the downside potential that the company will experience if the deal does not come into effect, I have decided to take a rather cautious approach and rate the company a ‘hold’. But for those who believe a deal is likely to go through, I can understand why a purchase of the stock might be considered.

For further details see:

LL Flooring Holdings: Investors Should Push For A Deal