FND - LL Flooring: Poor Business Model Makes This An Unattractive Investment

2023-03-16 10:29:28 ET

Summary

- LL Flooring has a heavily indebted balance sheet.

- There's a continued opening of uneconomic stores.

- Macro headwinds exacerbate LL's problems.

LL Flooring ( LL ) was a significant beneficiary of covid lockdowns and the work-from-home movement. However, the company did not capture the full benefit due to inventory shortages and supply chain disruptions. With these tailwinds abating, LL is in a precarious position with elevated inventory and a relatively high debt load. Even with the stock down ~75% over the past year, it's still expensive, and we recommend selling/shorting the stock.

Background

LL Flooring (Previously known as Lumber Liquidators) is a flooring retailer in the United States, operating 442 stores at the end of 2022 after opening 18 in 2021. LL leases all stores for an initial term of 5 to 7 years with an average store size of 6,500 to 7,500 square feet (sq. ft.). Stores are located in 47 states, with the most in California (43), Florida (33), and Texas (31).

The company operates two business segments, Merchandise Sales and Service Sales. In 2022 and 2021, Merchandise Sales represented ~86% of sales, while Service represented ~14%. Merchandise sales relate to the sale of flooring products, and Service is revenue generated from installation work. LL caters to professional builders and Do it Yourself (DIY) and has focused on attaching service work to merchandise sales.

Thesis

LL has a balance sheet problem with excess inventory and a high debt burden. Over the past year, LL acquired inventory during supply chain challenges and high lumber prices. At year-end 2022, they had $332m in inventory compared to $254m and $245m at YE 21 & 20. The economic environment is deteriorating, and management guided 2023 to be a weak year, with cost pressures on SG&A as the labor force remains tight. From the Q4 2022 Call , "In the near term, we continue to navigate an uncertain macroeconomic environment. We see customer spending on home improvement potentially challenged by consumer confidence, inflation, volatile mortgage rates impacting housing affordability, and continued declines in existing home sales."

In Q4, comparable sales (SSS) were down 9.5%, even as average ticket prices increased 8.2% y/y. For the full year, SSS was down 5.8%. Average sales price rose 15.3%, offset by a 21.1% decline in the number of transactions. Transactions will continue to decline, in my opinion, though unlikely to be at the same rate, combined with a decrease in average selling price as the company marks down high-cost inventory to generate sales. Floor & Décor ( FND ), one of LL's competitors, guided 2023 comps flat to down 3%. FND opened 32 stores in the year, which distorts 2023 SSS upward as new stores take time to stabilize, providing a 300-400bps tailwind to the overall comparable sales figure. Mature and stabilized FND stores should decline 3-7% in 2023. With LL's inferior position, I believe they will perform worse, putting comps down 5-10%, with the first half of the year worse than the second half as comps ease. Due to a markdown in inventory prices, gross margins should contract, the opposite of management's 2023 guidance.

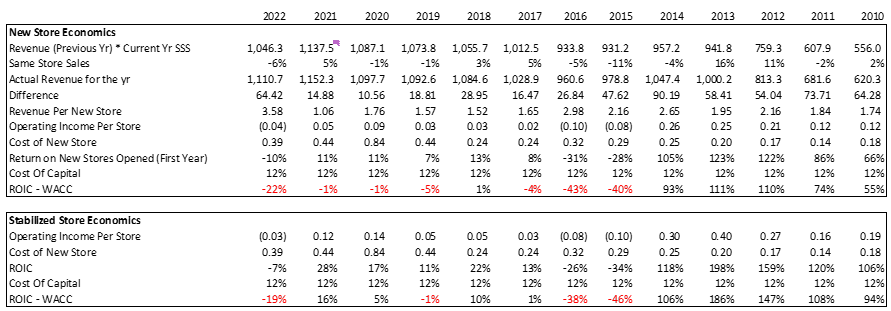

Store count grew over the past decade from 318 in 2013 to 442 in 2022. During LL's prime (pre-2015, before the formaldehyde litigation), the company generated world-class ROIC, a primary reason for the high valuation years ago. New store paybacks were sometimes less than a year, and the ROIC for a stabilized store was more than 100%. With these economics, the company deserved a high valuation. Things changed during the litigation scandal, and the once best-in-class business economics is but a shell of themselves. The formaldehyde scandal is behind the company, and no outstanding litigation remains. This 60 Minutes video described the problems at LL.

LL continues to open new stores and remodel existing stores, even with an unattractive return profile. At best, the company is generating mid-double digit ROICs on stable and new stores. However, given my downbeat outlook, the high ROIC's generated in 2020 & 2021 are unlikely to indicate future business economics. In the first year, they do not meet the company's cost of capital. While it takes a few years for the store to stabilize, given the ongoing headwinds and increasing competition from Floor & Décor, Home Depot ( HD ), and Lowe's ( LOW ), store economics will further deteriorate. See the model below for my unit economics estimate.

At the end of 2022, they had $72m drawn on their $250m line of credit, which bears an interest rate of SOFR + 1.25% putting the current rate at 5.8%, up from 2022's 5.1%, and matures in April 2026. With the challenging environment ahead, the company will likely draw it down further by $55m. I estimate the company would have to issue long-term debt at 9%+ in today's market, the equivalent of a B-rated company. The increase in leverage will further raise the cost of capital as the potential for bankruptcy increases.

In summary, consistently opened uneconomic stores over the past eight years and a heavily indebted balance sheet that will surely further deteriorate given the current economic backdrop. In my opinion, LL must reexamine its portfolio, shut down underperforming locations, and use the liquidity generated to pay down debt. By opening up new stores, the company is straining its balance sheet and increasing the probability of default.

LL Flooring Annual Reports & Dominick D'Angelo Estimates

{kind=link}

(Revenue and SSS are company-provided figures, the remaining numbers are calculated using my best estimate)

Valuation

During LL's Q4 2017 earnings call, management laid out an operating margin target of mid to high single digits and a long-term goal of 10%. "And while there may a gradual rise from the current dollar level of SG&A spend, we will still expect to leverage SG&A as a percent of sales. Taken altogether, we believe these initiatives can drive 3 to 5 points of operating margin improvement over the next 3 years. We consider this strategy evolutionary, not revolutionary, as we still have some work to do to put legacy legal matters behind us while steadily improving the franchise. As we execute on these plans over the next 3 years, we believe we can achieve continued improvement in our operating results and have established 2021 financial goals that include annual comp store sales growth in the mid-single digits, total annual sales growth in the mid-to upper single digits and adjusted operating profit in the upper single digits with a long-term target of 10%. We expect that our march towards upper single-digit adjusted operating profit will unfold over the next 8 to 12 quarters."

These goals appear outlandish, in my opinion, as they posted margins of 5%, 5%, and -1% from 2020 to 2022, years of record sales and home-building spending. Without a dramatic change, I suspect 5% is peak margins. I gave the company the benefit of the doubt in my valuation, returning them to 5% in 2028, though it's a long shot they reach this. The high debt load, poor retail store economics, and challenging industry outlook culminate in an unattractive investment.

Dominick D'Angelo Estimates

Balance Sheet

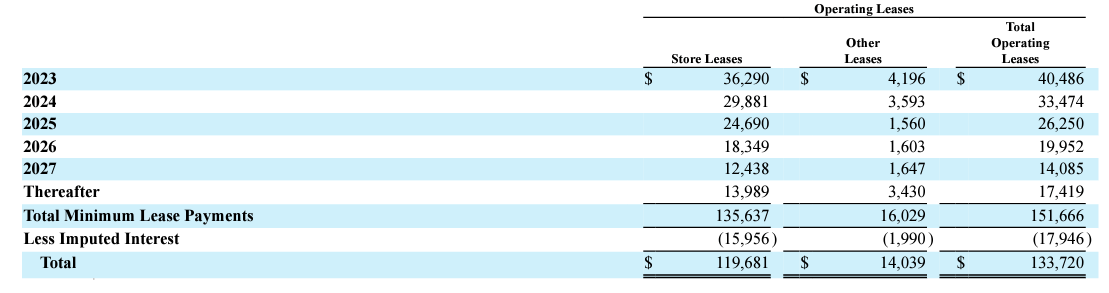

In addition to the noted debt above, LL leases all of its properties. Over the next five years, they have $151m in lease payments shown below.

LL Flooring 2022 Annual Report

{kind=link}

A critical problem with the retail business model is the constant cash need to rebuild inventory. Just as cash comes in, it leaves to fund new inventory purchases. With $10.8m of cash, they have minimal support for ongoing business operations, especially considering the year's $15-20m capex spend. $125m remains undrawn on the revolver, providing liquidity; however, drawing on this further strains the Balance Sheet and increase interest expense. The company will burn cash this year, resulting in higher interest payments in 2024. If the company makes it to 2026, the interest rate on a new credit line will likely be higher, further hurting them. LL should downsize, liquidate inventory without replenishing it, and pay down debt to lower credit risks.

One of the main arguments of those pitching LL as a long idea, state is the discount to TBV the stock trades. While true, the 55% discount to TBV is attributable to the company's $332m inventory position. Inventory is not liquid and would sell at a discount to move over a short period. The other problem with the TBV discount is that the company is not in liquidation mode (yet). Cash generated from the inventory sales will likely be reinvested into the business at uneconomical returns, warranting this discount. Last, as noted several other times, the cash burn, which I estimate to be $50m in the year, means if we look out a year, the company will trade at a 43% discount to TBV compared to the current 55% discount.

Management

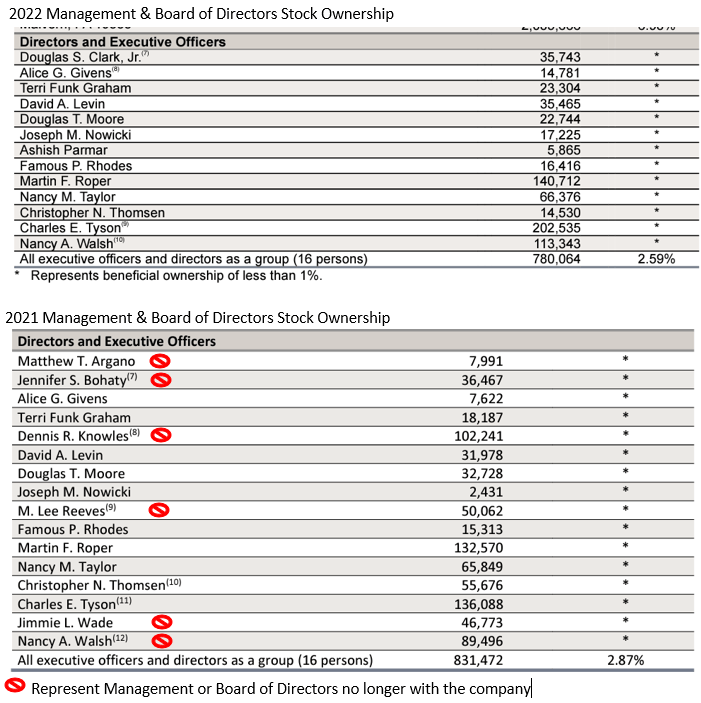

Another red flag is the management turnover over the past several years. From 2021 to 2022, five members from either management or the board of directors left (shown below). Most recently, in November, CFO Nancy Walsh left the company. Lastly, management has little skin in the game, with only 2.59% of the outstanding shares owned by management and the BoD, which, I suspect, mainly were part of their compensation package.

LL 2021 & 2022 Proxy Statement

{kind=link}

Risks

The primary risks associated with this thesis are a management business strategy pivot, where they begin to shrink the store base and reduce leverage. The cost of capital would decline due to a lower debt load, lowering the potential bankruptcy risk. The second risk is a reversal in interest rates that would revitalize the home improvement industry. Higher rates have deterred homeowners from taking equity out of their homes as it is now much more punitive with the higher rates.

Summary

Since the litigation scandal in 2015, LL Flooring's business has deteriorated. They never recovered, and I believe the unit economics of the store are destroying shareholder capital. The housing industry is going through a significant slowdown due to the dramatic rise in interest rates. LL's excess inventory will lead to contracting margins and a cash burn in 2023. The heavy debt load will worsen as the company further draws down its line of credit. Until the management team pivots, the stock remains unattractive as increased interest costs further drag down the business's profitability.

For further details see:

LL Flooring: Poor Business Model Makes This An Unattractive Investment